|

市場調査レポート

商品コード

1690877

高活性API/HPAPI:市場シェア分析、産業動向、成長予測(2025~2030年)High Potency APIs /HPAPI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 高活性API/HPAPI:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

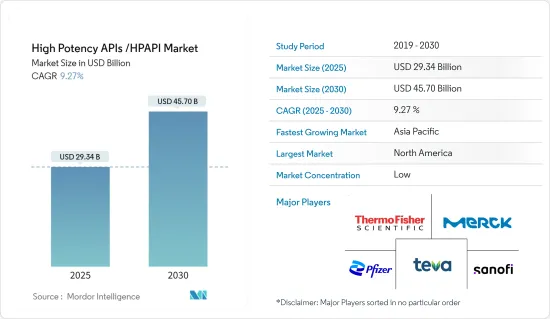

高活性API/HPAPI市場規模は2025年に293億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.27%で、2030年には457億米ドルに達すると予測されます。

COVID-19パンデミックの間、高活性API(HPAPI)市場は悪影響を受けました。COVID-19の流行は主にAPI市場のサプライチェーンに影響を与えました。中国とインドはAPIの生産拠点であり、COVID-19がこの地域で増加したため、市場は深刻な打撃を受けました。2022年6月にEuropean Pharmaceutical Reviewに掲載された記事によると、高活性APIを含むAPIの60%はインドまたは中国で製造されています。

インドだけで世界のジェネリック医薬品製造市場の18%を占め、そのほとんどが他国に輸出されています。中国はインドのジェネリック医薬品産業向けに、高活性APIを含むAPIの70%を製造しています。中国では厳格な封鎖規制が敷かれているため、44社がAPI製造工場を閉鎖しました。その結果、重要なAPIや医薬品へのアクセスが著しく制限されました。

米国では、重要な治療領域の重要な医薬品のAPIの80%が国内で製造されていないと予想され、これは世界保健に重大な影響を及ぼします。全体として、市場は短期的には妨げられると考えられていました。しかし、COVID-19ワクチンの製造には様々なAPIが使用されており、予測期間中に市場は大きく成長すると予想されます。

市場の成長を促す要因としては、医薬品需要の増加、精密医療と高活性APIへの注目の高まり、高活性API製造の技術進歩などが挙げられます。

APIは、がん、心血管疾患、脳卒中、心臓発作、糖尿病などのような慢性的な基礎疾患の治療に使用される医薬品の必須成分です。これらの慢性疾患の有病率の上昇は、HPAPIに対する需要を増加させ、市場の成長を増大させる可能性が高いです。例えば、米国がん協会が2023年1月に発表したCancer Facts and Figures 2023によると、2023年に新たに診断されるがん患者は推定190万人で、そのうち前立腺がんは28万8,300人、次いで肺がん23万8,340人、女性乳がん30万5,590人と推定されています。このように、国内におけるがんの負担増は、効果的な医薬品を製造するためにHPAPIを必要とする先進的治療に対する需要を増加させると予想され、市場の成長を後押しすると考えられます。

市場全体でHPAPI製造施設が設立されることは、市場を大きく牽引すると考えられます。例えば、Novasepは2021年5月、ル・マン(フランス)の拠点で高活性医薬品成分(HPAPI)の製造能力を拡大し、追加投資によってがん治療のための革新的な標的分子を生産します。さらに、2022年3月、インドの保健・家族福祉・化学肥料大臣は、中国から輸入していた35品目の医薬品原料の製造を開始したと発表しました。このようなイニシアチブは、各国におけるAPIのアンメットニーズを満たし、したがって予測期間中の市場を押し上げると期待されています。

このように、慢性疾患の負担増加や製造施設の設立など、上記のすべての要因が市場拡大の原動力になると予測されます。しかし、設備投資が高額であるため、予測期間中は市場が抑制されると予想されます。

高活性API/HPAPI市場動向

ジェネリック高活性APIセグメントが大幅な成長を記録する見込み

ジェネリック高活性APIは、ブランドAPIや革新的なAPIと同じ薬理効果を示します。ジェネリックHPAPIセグメントは、主にジェネリック医薬品に対する需要の高まりと、手頃な価格で高品質の医薬品を製造するためのジェネリックHPAPIに対するニーズの高まりによって牽引されています。企業間の合併・買収の増加も、このセグメントの拡大に寄与しています。

ブランド医薬品の特許切れやコスト低下といった要因も、このセグメントの成長を後押ししています。2021年6月にAmerican Journal of Managed Careが発表した報告書によると、2023年には約20の腫瘍生物製剤の特許が失効するため、がん医療においてより多くのバイオシミラーが生産され、コストが削減される可能性があります。こうした理由から、予測期間中に市場は高い成長率を示す可能性があります。

また、API生産に焦点を当てた政府の取り組みも、調査対象市場の成長に寄与しています。2021年6月、インド財務大臣は、医薬品有効成分、医薬品中間体、重要な出発原料など13の主要セグメントにおける医薬品生産連動奨励金(PLI)スキームに対して、5年間で1兆9,700億インドルピー(240億2,400万米ドル)の追加支出を発表しました。ダイナミックな医薬品原料セグメントに割り当てられた多額の奨励金は、予測期間中の市場成長を大幅に押し上げると考えられます。

さらに、市場参入企業は競合を高めるために拡大戦略にも取り組んでいます。例えば、2021年、MoehsGroupは、高活性API(HPAPI)の開発と商業生産のためのGMP準拠のKilo Lab Unitの組み込みを発表しました。さらに、2021年11月、Hovioneはその能力と能力を高めるために1億7,000万米ドルを投資すると発表しました。ホビオネのこの能力と能力は、高活性API(HPAPI)の生産もアップグレードします。

このように、特許切れの増加やHPAPI製造施設の立ち上げなど、上記の要因はすべて、予測期間中の同セグメントの成長を後押しすると予想されます。

予測期間中、北米が大きな市場シェアを占める見込み

北米は、がんや神経疾患などの疾患の蔓延により、市場で大きなシェアを占めると予想されます。これらの疾患は有病率が増加しているため、同地域ではHPAPIの生産が増加しています。HPAPIは、がんやその他の重要な疾患に関連する多くの治療、創薬、その他の調査研究に広く使用されています。従って、北米地域では他の国に比べて患者人口が増加しているため、HPAPIの需要が大幅に増加します。

この地域における慢性疾患の有病率と発生率の増加は、予測期間にわたって市場を押し上げると予想されます。例えば、カナダ政府が発表し2022年5月に発表された統計によると、2022年には約23万3,900人のカナダ人ががんと診断され、前立腺がんは引き続き最も多く診断されるがんと予想されています。このように、同地域におけるがんの負担増は、予測期間中の市場成長を押し上げると予想されます。

さらに、World Alzheimer's Report 2023によると、2023年には推定670万人の65歳以上の米国人がアルツハイマー型認知症を患うと予想されています。このように、神経疾患の負担が増大することで、効果的な治療・管理方法に対する需要が高まり、予測期間中のHPAPI市場を押し上げると予想されます。

主要市場参入企業による同国の事業拡大も市場成長の要因の一つです。例えば、2021年8月、研究開発・製造受託機関大手のCuria(旧AMRI)は、ニューヨーク州レンセラー施設での商業生産能力の拡大を発表しました。複雑な医薬品API(API)を軟質に製造する能力の増強は、Curiaの顧客との提携能力をさらに強化します。

このように、上記の要因から、米国の高活性API(HPAPI)市場は予測期間中に高い成長率を示すと予想されます。

高活性API/HPAPI産業概要

高活性API/HPAPI市場は細分化され、競合が激しく、複数の大手企業で構成されています。市場シェアの面では、現在、Thermo Fisher Scientific、MerckKGaA、Pfizer、Novartis International AG、Teva Pharmaceutical Industriesなど、少数の大手企業が市場を独占しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 医薬品需要の増加

- 精密医療と高活性APIへの注目の高まり

- 高活性API製造の技術進歩

- 市場抑制要因

- 巨額の設備投資

- 変化し続ける産業標準とガイドライン

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ポダクトタイプ別

- 革新的高活性API

- ジェネリック高活性API

- 用途別

- 腫瘍学

- ホルモン失調症

- 緑内障

- その他

- 合成別

- 合成高活性API

- バイオ高活性API

- メーカー別

- キャプティブHPAPIメーカー

- マーチャントHPAPIメーカー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AbbVie Inc.

- Merck KGaA

- Corden Pharma International

- Pfizer Inc.

- Sanofi(EUROAPI)

- SK BIoTek

- Sun Pharmaceutical Industries Ltd

- Teva Pharmaceutical Industries Ltd

- Thermo Fisher Scientific Inc.

- Viatris Inc.

第7章 市場機会と今後の動向

The High Potency APIs /HPAPI Market size is estimated at USD 29.34 billion in 2025, and is expected to reach USD 45.70 billion by 2030, at a CAGR of 9.27% during the forecast period (2025-2030).

During the COVID-19 pandemic, the high-potency API (HPAPI) market was adversely affected. The COVID-19 outbreak primarily affected the supply chain of the API market. China and India are the hubs for the production of API, and the market was severely hampered as COVID-19 increased in the region. According to the article published in the European Pharmaceutical Review in June 2022, 60% of APIs, including high-potency APIs, are manufactured in India or China.

India alone accounts for 18% of the global generic drug manufacturing market, most of which is exported to other countries. China manufactures 70% of the APIs, including high-potency APIs, for India's generics industry. Due to stringent lockdown restrictions in China, 44 firms closed API manufacturing plants during the outbreak. As a result, access to critical APIs and medicines was severely limited.

It is anticipated that 80 percent of APIs for vital medications in critical therapeutic areas in the United States do not have a domestic manufacturing source, which has significant global health consequences. Overall, the market was considered to be hindered in the short term. However, various APIs are used in producing COVID-19 vaccines, and the market is expected to grow significantly over the forecast period.

Factors driving the market's growth include increasing demand for drugs, increasing focus on precision medicine and high-potency APIs, and technological advancements in high-potency API manufacturing.

APIs are essential components of drugs used to treat chronic underlying health disorders like cancer, cardiovascular disease, strokes, heart attacks, diabetes, and others. The rising prevalence of these chronic diseases is likely to increase demand for HPAPI, increasing market growth. For instance, according to Cancer Facts and Figures 2023, published in January 2023 by the American Cancer Society, an estimated 1.9 million new cancer cases will be diagnosed in 2023, among which prostate cancer is estimated to be 288,300, followed by 238,340 cases of lung cancer, and 300,590 cases of female breast cancer. Thus, the growing burden of cancer in the country is expected to increase demand for advanced treatments that need HPAPI to produce effective medicine, which is likely to boost market growth.

Establishing HPAPI manufacturing facilities across the market will drive the market significantly. For instance, in May 2021, Novasep expanded its highly potent active pharmaceutical ingredients (HPAPIs) manufacturing capabilities on its Le Mans (France) site to produce innovative and targeted molecules to treat cancer by investing in additional capacity. Additionally, in March 2022, the Indian Minister of Health and Family Welfare and Chemicals and Fertilisers announced that India had started manufacturing 35 pharmaceutical ingredients that had been imported earlier from China. Such initiatives are expected to meet the unmet need of API in countries and, hence, boost the market over the forecast period.

Thus, all the factors above, such as the increasing burden of chronic diseases and the establishment of manufacturing facilities, are projected to drive market expansion. However, the high capital investment is expected to restrain the market over the forecast period.

High-Potency APIs /HPAPI Market Trends

Generic High-potency Active Pharmaceutical Ingredients Segment is Expected to Record Significant Growth

Generic high-potency active pharmaceutical ingredients show the same pharmacological effects as branded or innovative API. The generic HPAPI segment is primarily driven by the rising demand for generic pharmaceuticals and the rising need for generic HPAPI to generate high-quality drugs at affordable prices. Rising mergers and acquisitions between businesses have also helped expand the segment.

Factors such as the expiration of patents on branded drugs and lower costs are also driving segment growth. According to the report published by the American Journal of Managed Care in June 2021, patents on around 20 oncology biologics will expire in 2023, which may lead to the production of more biosimilars in cancer care and reduce costs. Due to these reasons, the market may see a high growth rate during the forecast period.

Also, government initiatives focusing on active pharmaceutical ingredient production are contributing to the growth of the studied market. In June 2021, the Indian Finance Minister announced an additional outlay of INR 197,000 crore (USD 24,024 million) for utilization over five years for the pharmaceutical Production Linked Incentive (PLI) Scheme in 13 key sectors such as active pharmaceutical ingredients, drug intermediaries, and critical starting materials. The significant incentives allocated to the dynamic pharmaceutical ingredient segment would significantly boost market growth over the forecast period.

Furthermore, market players are also involved in expansion strategies to gain a competitive edge. For instance, in 2021, MoehsGroup announced the incorporation of the GMP-compliant Kilo Lab Unit for developing and commercially producing high-potency APIs (HPAPIs). Additionally, in November 2021, Hovione announced an investment of USD 170 million to increase its capacity and capabilities. This capacity and capability of Hovione will also upgrade the production of highly potent active pharmaceutical ingredients (HPAPI).

Thus, all the factors above, such as an increase in patent expirations and the launch of HPAPI manufacturing facilities, are anticipated to boost the segment's growth over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America is expected to hold a significant share of the market owing to the prevalence of disorders such as cancer and neurological disorders. These disorders are increasing in prevalence, thus increasing the production of HPAPIs in the region. HPAPIs are widely used in many therapeutic, drug discovery, or other research studies related to oncology and other significant disorders. Thus, the demand for the same will be significantly higher in the North American region as the patient population is increasing compared to other countries.

The increasing prevalence and incidence of chronic diseases in this region are expected to boost the market over the forecast period. For instance, according to statistics published by the Government of Canada and released in May 2022, about 233,900 Canadians were diagnosed with cancer in 2022, and prostate cancer is expected to remain the most commonly diagnosed cancer. Thus, the growing burden of cancer in the region is expected to boost market growth over the forecast period.

Further, according to the World Alzheimer's Report 2023, an estimated 6.7 million Americans age 65 and older are expected to be living with Alzheimer's dementia in 2023. Thus, the growing burden of neurological diseases is expected to increase demand for effective treatment and management methods, thereby boosting the market for HPAPI over the forecast period.

The country's expansion by key market players is another factor in the market's growth. For instance, in August 2021, Curia, formerly AMRI, a leading contract research, development, and manufacturing organization, announced the expansion of its commercial manufacturing capacity at its Rensselaer, New York, facility. The increased capability to flexibly manufacture complex active pharmaceutical ingredients (APIs) will further strengthen Curia's ability to partner with customers.

Thus, owing to the factors above, the United States high-potency API (HPAPI) market is expected to witness a high growth rate over the forecast period.

High-Potency APIs /HPAPI Industry Overview

The high-potency APIs/HPAPI market is fragmented, competitive, and consists of several major players. In terms of market share, a few major players are currently dominating the market, including Thermo Fisher Scientific Inc., Merck KGaA, Pfizer, Novartis International AG, and Teva Pharmaceutical Industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Pharmaceutical Drugs

- 4.2.2 Increasing Focus on Precision Medicine and High-potency APIs

- 4.2.3 Technological Advancements in High-potency API Manufacturing

- 4.3 Market Restraints

- 4.3.1 Huge Capital Investment

- 4.3.2 Ever Changing Industry Standards and Guidelines

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - in USD)

- 5.1 By Poduct Type

- 5.1.1 Innovative High-potency Active Pharmaceutical Ingredients

- 5.1.2 Generic High-potency Active Pharmaceutical Ingredients

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Hormonal Imbalance

- 5.2.3 Glaucoma

- 5.2.4 Other Applications

- 5.3 By Synthesis

- 5.3.1 Synthetic High-potency Active Pharmaceutical Ingredients

- 5.3.2 Biotech High-potency Active Pharmaceutical Ingredients

- 5.4 By Manufacturer

- 5.4.1 Captive HPAPI Manufacturers

- 5.4.2 Merchant HPAPI Manufacturers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AbbVie Inc.

- 6.1.2 Merck KGaA

- 6.1.3 Corden Pharma International

- 6.1.4 Pfizer Inc.

- 6.1.5 Sanofi (EUROAPI)

- 6.1.6 SK Biotek

- 6.1.7 Sun Pharmaceutical Industries Ltd

- 6.1.8 Teva Pharmaceutical Industries Ltd

- 6.1.9 Thermo Fisher Scientific Inc.

- 6.1.10 Viatris Inc.