|

市場調査レポート

商品コード

1248156

住宅ローン/ローンブローカー市場- 成長、動向、予測(2023年-2028年)Mortgage/Loan Brokers Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 住宅ローン/ローンブローカー市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年03月25日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

住宅ローン/ローンブローカー市場は、現在のところ2,600億米ドルと評価されており、予測期間には15%のCAGRで成長すると予想されています。

住宅ローン/ローンブローカーは、融資を許可する金融機関と、お金を借りたい企業との間の接点となる専門家です。ブローカーは、顧客が融資を受けたい場合でも、新規事業を立ち上げたい場合でも、最も優れた金融金利と条件を探します。ブローカーは、融資の承認を得るために金融機関と交渉したり、他の選択肢を検討したりします。銀行の融資担当者は、1社から住宅ローンの金利やプログラムを提供するだけです。これに対し、住宅ローンブローカーは借り手に代わって、複数の金融機関が提供する最良の融資プログラムや最低金利を探し出す仕事をします。

COVID-19の流行は、世界のローンブローカーのビジネス拡大に悪影響を及ぼしました。COVID時代にはローンを求める消費者が減少し、多くのローンブローカーが大きな損失を被っています。COVID-19の流行による影響では、政府や主要機関がこの問題にどのように対処し、回復しているのか、また、貸し手が直面する直接的な影響や継続的な困難について調査しています。金融機関の対応は、「復興への準備」「ビジネスリスクのコントロールと安定化」「大量流入への対応」の3つに大別されます。

住宅ローン/ローンブローカー市場動向

デジタル化が変える、住宅ローンの未来

すべての関係者がバーチャルに住宅ローンを締結できるようになったことで、消費者の体験と貸し手の投資収益が向上し、住宅ローン部門に変革が起きています。

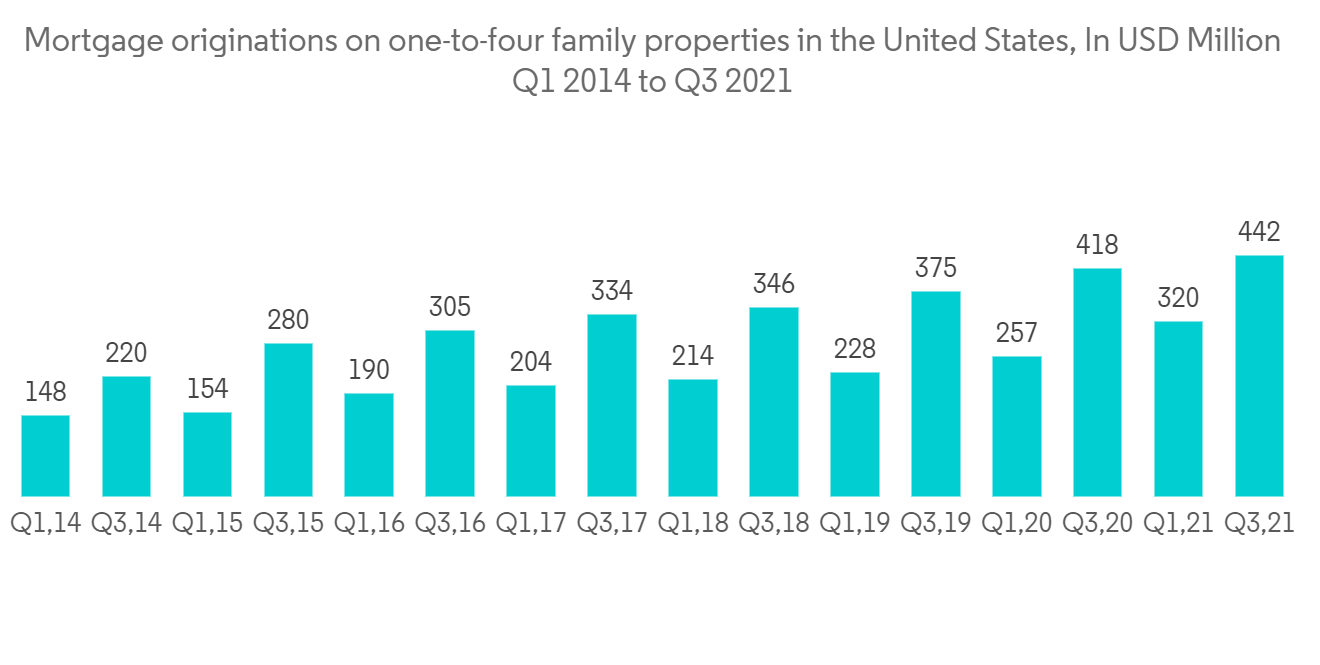

拡大する今日の住宅市場において、住宅ローンは活況を呈しています。米国の住宅市場における住宅ローン組成は、2021年に過去最高の4兆4,000億米ドルを記録しました。これは驚くべき成果であり、2022年は住宅ローン販売にとっても重要な年となるようです。住宅ローン業界には、他の要因もあります。住宅ローンのプロセスがデジタルの変化により大きな影響を受けるため、貸し手は今注目しています。2020年3月から、消費者と企業や互いのやり取りが大きく変化します。パンデミックの後、デジタルチャネルの利用が著しく増加しました。流行によって、デジタル技術の取り込みが数年早まりました。

オンラインバンキング、遠隔地での雇用、オンラインコミュニケーションなどのため、顧客はデジタルでビジネスを行うことを余儀なくされました。住宅ローン事業は、このデジタルへの大幅なシフトの影響を受け、今後も減速することのないデジタル変革の幕開けとなっています。デジタルプロセスがもたらすメリットに加え、オンライン住宅ローン手続きへの需要が高まっていることには、いくつかの要素が寄与しています。まず、現在、新築住宅を購入する人の大半がミレニアル世代であることが挙げられます。彼らはスマートフォンやノートパソコンで育ったため、家探しから住宅ローンの手続きまで、すべてにおいてデジタル体験を好みます。貸し手は、どの世代もデジタル・プラットフォームの利用を増やしてきたとはいえ、若い世代の消費者は古い世代の消費者よりも技術的な意識が高いということを念頭に置く必要があります。

住宅市場の成長により住宅ローンブローカーの需要が高まる

住宅ローン市場の環境が変化する中、デジタル革命やCOVID-19の流行がもたらした経済変動がもたらした大きな課題にもかかわらず、ホールセールチャネルが2020年を通して達成した成果を考える良い機会です。住宅市場は依然として活況を呈していますが、需要が高く供給が不足しているため、どのローンも厳しい競争にさらされています。そこで役に立つのが、ブローカーのダイナミックな柔軟性です。ブローカーが提供するリレーションシップに基づく顧客サービス、多様なローンオプション、テクノロジーリソースにより、ブローカーチャネルは将来的に成功し、市場シェアを拡大し続けることができる立場にあります。

住宅ローンブローカーとして成功することは難しいですが、追求する価値のある目標です。ブローカーは、常に顧客の懸念に対応し、顧客のニーズを最優先する覚悟が必要ですが、競争が激しいため、限界に課題することも必要です。また、信頼できる手順やプロセスを確立する必要がありますが、成長し続け、革新し続けることも必要です。つまり、さまざまな資質の組み合わせが、ブローカーとしての成功につながるのです。例えば、テクノロジーの活用、市場や顧客との交流、学習と発展への寛容さなどが挙げられます。

住宅ローン/ローンブローカー市場の競合他社分析

米国の住宅ローン/ローンブローカー事業における主な海外競合他社を調査したものです。ローンブローカーは、担当する地域の優良な不動産業者や金融業者との関係に依存するため、激しい競合に直面します。以下のリストには、主要な市場参入企業の一部が含まれています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 市場抑制要因

- 住宅ローンブローカー市場を形成する様々な規制動向に関する洞察

- 住宅ローンブローカー市場におけるテクノロジーとイノベーションがオペレーションに与える影響に関する洞察

- アセットマネージャーのパフォーマンスに関する洞察

- 産業の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響について

第5章 市場セグメンテーション

- エンタープライズ

- 大型

- 小型

- 中型

- 用途

- ホームローン

- 商業・工業用ローン

- 自動車ローン

- 政府への貸付金

- その他

- エンドユーザー

- 事業内容

- 個人情報

- 地域

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ地域

- 南米

第6章 競合情勢について

- 市場の集中度と概要

- 企業プロファイル

- Bank of America

- Royal Bank of Canada

- BNP Paribas

- Truist Financial Corporation

- Mitsubishi UFJ Financial Group

- PT Bank Central Asia Tbk

- Qatar National Bank

- Standard Chartered PLC

- China Zheshang Bank

- Federal National Mortgage Association(FNMA)

第7章 市場機会と今後の動向

第8章 免責事項および米国について

The Mortgage/Loans Broker Market is valued at USD 260 billion in the current year and is expected to grow at a CAGR of 15% in the forecasted period.

A mortgage/loan broker is a specialist who serves as a point of contact between lenders who authorize loans and companies looking to borrow money. Brokers search for the finest financial rates and terms whether their customer wants to fund a loan or launch a new business. They bargain with lenders to secure loan approval or look into other options. A bank loan officer offers mortgage rates and programs from just one company. In contrast, a mortgage broker works on behalf of a borrower to locate the best lending programs and/or lowest rates offered by several lenders.

The COVID-19 epidemic had a detrimental effect on the expansion of the global loan brokers' business since fewer consumers were seeking loans during the COVID era, which caused many loan brokers to suffer significant losses. The impact of the COVID-19 epidemic explores how governments and major institutions are handling the issue and recuperating, as well as the immediate repercussions and ongoing difficulties lenders are facing. Institutions' actions can be categorized into one of three broad categories: preparing for recovery, controlling and stabilizing business risk, and responding to volume influxes.

Mortgage/Loan Brokers Market Trends

Digitization is changing the future of Mortgage

The ability for all parties to close on mortgages virtually, which enhances the consumer experience and returns on investment for lenders, is transforming the mortgage sector.

In the expanding housing market of today, mortgages are booming. Mortgage originations in the US housing market hit a record USD 4.4 trillion in 2021. That's a remarkable accomplishment, and 2022 appears to be a significant year for mortgage sales as well. There are other factors at play in the mortgage industry as well. Lenders are now paying attention as the mortgage process is significantly impacted by digital change. Beginning in March 2020, consumers' interactions with companies and one another will drastically change. The use of digital channels significantly increased after the pandemic. The epidemic accelerated the uptake of digital technologies by several years.

Customers were compelled to conduct business digitally because of online banking, remote employment, and online communication. The mortgage business was affected by this significant shift to digital, which marked the beginning of a digital transformation that isn't about to slow down. Several elements contribute to the rise in demand for an online mortgage procedure, in addition to the advantages that digital processes offer. The first is that the majority of people buying new homes now are millennials. These customers prefer a digital experience for everything from house searches to mortgage closings because they grew up with smartphones and laptops. Lenders must keep in mind that younger generations of consumers are more technologically aware than older generations of customers even if every generation has increased its use of digital platforms.

Growth In The Housing Market Leads The Demand For Mortgage Brokers

It is a good moment to consider the achievements that the wholesale channel accomplished throughout 2020 despite the significant challenges provided by the digital revolution and the economic volatility brought on by the COVID-19 epidemic as the mortgage market climate changes. The housing market is still booming, but because of the high demand and short supply, every loan faces stiff competition. This is where the dynamic flexibility of the broker is useful. Due to the relationship-based customer services, variety of loan options, and technology resources they offer, the broker channel is well-positioned to succeed in the future and keep expanding its market share.

Being successful as a mortgage broker is difficult, but it's a goal worth pursuing. Brokers must constantly be able to respond to client concerns and be prepared to put the needs of the customer first, but they must also push the envelope because the competition is fierce. They must set up reliable procedures and processes, but they must also continue to grow and innovate. In other words, a combination of various different qualities will surely contribute to their success as a broker. These include the use of technology, interactions with the market and clients, as well as an openness to learning and development.

Mortgage/Loan Brokers Market Competitor Analysis

The main foreign competitors in the US mortgage/loan broker business are covered in the research. Loan brokers face intense competition since they depend on their relationships with the best real estate agents and lenders in the communities they cover. The following list includes some of the key market participants.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Insights on Various Regulatory Trends Shaping Mortgage Broker Market

- 4.5 Insights on the impact of technology and innovation in Operation in Mortgage Broker Market

- 4.6 Insights on Performance of Asset Managers

- 4.7 Industry Attractiveness - Porters' Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Enterprise

- 5.1.1 Large

- 5.1.2 Small

- 5.1.3 Medium- sized

- 5.2 Application

- 5.2.1 Home Loans

- 5.2.2 Commercial and Industrial Loans

- 5.2.3 Vehicle Loans

- 5.2.4 Loans to Governments

- 5.2.5 Others

- 5.3 End - User

- 5.3.1 Businesses

- 5.3.2 Individuals

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia - Pacific

- 5.4.4 Middle- East & Africa

- 5.4.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration & Overview

- 6.2 Company Profiles

- 6.2.1 Bank of America

- 6.2.2 Royal Bank of Canada

- 6.2.3 BNP Paribas

- 6.2.4 Truist Financial Corporation

- 6.2.5 Mitsubishi UFJ Financial Group

- 6.2.6 PT Bank Central Asia Tbk

- 6.2.7 Qatar National Bank

- 6.2.8 Standard Chartered PLC

- 6.2.9 China Zheshang Bank

- 6.2.10 Federal National Mortgage Association (FNMA)*