|

市場調査レポート

商品コード

1639479

金属缶-市場シェア分析、産業動向・統計、成長予測(2025~2030年)Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 金属缶-市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

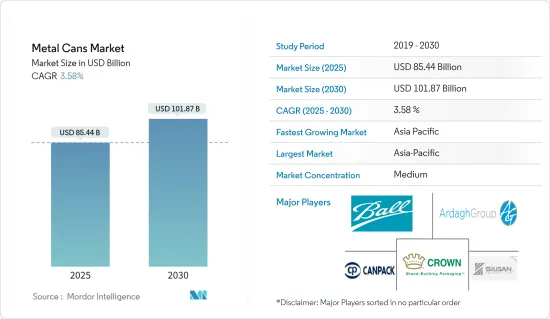

金属缶市場規模は2025年に854億4,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは3.58%で、2030年には1,018億7,000万米ドルに達すると予測されます。

金属缶市場が脚光を浴びているのは、輸送耐性、密閉カバー、粗雑な取り扱い、容易なリサイクル性など、明確な特徴があるためです。

主要ハイライト

- 金属缶の高いリサイクル性は市場促進要因のひとつです。アルミ缶は湿気から完全に保護されます。缶は錆びず、耐腐食性があり、あらゆる包装の中で最も賞味期限が長いもの1つです。また、剛性、安定性、高いバリア性など多くの利点があります。

- アルミ缶の不足は飲食品産業に影響を与え続けており、外食産業に比べて家庭用や食料品向けの飲料需要が増加しています。多くの著名な市場関係者が、増加する注文に対応しアルミ缶不足に対処するため、新たな製造インフラを設置するための投資を発表しています。

- 2023年9月、サステイナブルアルミニウムソリューションの著名なプロバイダーであるNovelis Inc.は、北米の大手アルミ缶メーカーであるBall Corporationと重要な契約を締結しました。この契約は、Novelisが北米全域にあるボールの製造施設にアルミニウム板を供給するものです。

- 包装における非発がん性材料の適用に関する消費者の意識の高まりと、軽量包装に対する需要の増加は、金属缶市場に高い成長展望をもたらしています。しかし、金属缶は、ポリエチレンやポリエチレンテレフタレート(PET)などのポリマーベースの包装材料に置き換わる可能性があるため、使用に難があります。

金属缶産業のセグメンテーション

食品セグメントが市場で大きなシェアを占めると予想される

- 世界レベルでのライフスタイルの変化により、消費者は調理しやすい食品を選ぶようになりました。若年層や個人で生活する人々は、缶食品をより多く消費しています。これらのユーザーは時間がなく、予算に制約があるため、より低コストで利便性の高い製品を選んでいます。

- 缶の常用消費者の多くは、提供される利便性と低コストのために缶を選んでいます。缶はより便利で、エネルギーも調理時間も少なくて済みます。ほとんどの缶食品は、通常の食事よりも調理にかかる時間が40%短いです。

- アルミ缶は食品の品質を長期間保つのに役立ちます。アルミ缶は、酸素、光、湿気、その他の汚染物質をまったく通しません。錆びず、腐食に強く、賞味期限が最も長い包装のひとつです。アルミ缶の安全性は他の追随を許しません。

- 改ざん防止加工が施され、改ざんが確認できる包装であるため、消費者は自分の商品が安全に調理され、配送されたことを確信することができます。飲食品以外にも、アルミニウムはエアロゾル、塗料、その他の消費財を含む様々な製品の包装に使用されています。ジャマイカ農産物規制庁(JACRA)によると、2023年の日本へのアルミ缶の輸入量は、空缶が約6,000万個、実缶が約4億3,000万個です。

- FCCとカナダ統計局の報告によると、2024年には、特にプライベート・ラベルの缶と冷凍食品において、激しい競争が確認されることになりそうです。さらに、原料費や包装費の高騰から賃金の上昇に至るまで、さまざまな要因が重なり、名目売上高の伸びを上回ることが予想され、その結果、2024年のマージン拡大が抑制されることになります。

北米が市場で大きなシェアを占める見込み

- 北米は、健康飲料、炭酸清涼飲料、健康飲料、スクラロースジュースの需要増加により、予測期間中、金属缶の需要にプラスの影響を与えると予測されます。さらに、いくつかの重要な参入企業は、広範なプロモーション活動や新しい研究を通じて、ビジネスの開発に影響を与えます。

- 米国における製品需要に影響を与える主要要因は、食品産業と小売産業です。同国にはかつてないほど多くの食料品店やスーパーストアがあり、同国の食品・小売産業の拡大は主に小規模家庭の増加によるものです。その結果、より小型の包装ユニットの需要が高まっている

- 2023年6月、サステイナブルアルミニウムソリューション・プロバイダーの主要企業であるNovelis Inc.は、Coca-Cola Companyの北米正規ボトラーの契約代理店であるCoca-Cola Bottlers' Sales & Services Companyと新たな長期契約を締結したと発表しました。Novelisは、Coca-Cola Companyの北米の正規ボトラーに、Coca-Cola Companyのブランドファミリー用のアルミ缶シートを供給する予定です。これには、現在建設中で、2025年に試運転を開始する予定のベイ・ミネットにあるNovelisの工場からの供給も含まれます。

- また、米国の生活様式から、金属缶のニーズが高まっています。慌ただしいスケジュールで料理をする時間がほとんどないため、レディトゥイート健康的な食品が選ばれているのです。簡単な包装とすぐに使える食品を提供することで、缶はこの目標を達成しています。金属缶は食品の鮮度と品質を長期間保つことができるため、市場の成長を後押しすると期待されています。

金属缶産業概要

金属缶市場は半固体化しており、Ball Corporation、Ardagh Group、Mauser Packaging Solutions、Silgan Containers LLC、Crown Holdings Inc.などの大手企業が存在します。市場の参入企業は、製品提供を強化し、サステイナブル競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年11月、Mauser Packaging Solutionsは、スズ-スチール製エアロゾル缶とスチールペール缶を専門とするメキシコの著名メーカーTaenza SA de CVを買収しました。メキシコシティを拠点とするTaenzaは、メキシコ全土に5つの製造施設を持ち、従業員数は850人を超えます。同社の製品ラインには、エアロゾルスプレー缶、スチールペール缶、塗料缶などがあり、塗料、コーティング剤、化学品セクターの多様な顧客に対応しています。

- 2023年11月、SonocoとBall Corporationが重要な契約を締結。この契約に基づき、Sonocoは特にSonoco Phoenix事業部を通じて、食品缶用のイージーオープン、フルパネルエンドを備えたボールを独占的に供給。この提携により、Ballの主要サプライヤーとしてのSonocoの役割が強化され、この革新的な食品缶の共同マーケティングと販売活動も拡大しました。

- 2023年9月、Ardagh GroupとCrown Holdings Inc.はCan Manufacturers Institute(CMI)と協力し、飲料用アルミ缶のリサイクル率を高めています。カリフォルニア州のリサイクル施設に人工知能とロボット工学の会社であるEverestLabのロボットに資金を提供することでこれを実現します。カリフォルニア州フレズノで操業するCaglia Environmentalは、このロボットを材料回収施設(MRF)の「ラスト・チャンス・ライン」に配備しました。この戦略的な動きにより、年間100万個以上の使用済み飲料缶(UBC)を回収することを目指しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19パンデミックの市場への影響評価

第5章 市場力学

- 市場促進要因

- エネルギー使用量の減少による包装の高いリサイクル性

- アルコール飲料とノンアルコール飲料の消費の増加

- 市場抑制要因

- ポリエチレンテレフタレートなどの代替包装ソリューションの存在

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- エンドユーザー産業別

- 食品

- 飲料

- 化粧品・パーソナルケア

- 医薬品

- 塗料

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Ball Corporation

- Ardagh Group

- Mauser Packaging Solutions

- Silgan Containers LLC

- Crown Holdings Inc.

- DS Containers Inc.

- CCL Container Inc.

- Toyo Seikan Group Holdings Ltd

- Pacific Can China Holdings Limited

- Universal Can Corporation

- CPMC HOLDINGS Limited(COFCO Group)

- Showa Denko KK

- Independent Can Company

- Hindustan Tin Works Ltd

- Saudi Arabian Packaging Industry WLL(SAPIN)

第8章 投資分析

第9章 市場機会と今後の動向

The Metal Cans Market size is estimated at USD 85.44 billion in 2025, and is expected to reach USD 101.87 billion by 2030, at a CAGR of 3.58% during the forecast period (2025-2030).

The metal cans market is gaining prominence because of its distinct features, like transportation resistance, hermetically sealed cover, rough handling, and easy recyclability.

Key Highlights

- The high recyclability of metal cans is one of the significant drivers of the market. Aluminum cans deliver complete protection against moisture. Cans do not rust, are corrosion-resistant, and provide one of the most extended shelf lives considering any packaging. It also offers many benefits, such as rigidity, stability, and high barrier properties.

- The aluminum can shortage continues to affect the food and beverage industry, as the beverage demand for home consumption and grocery increased compared to restaurants. Many prominent market players have announced investments to set up new manufacturing infrastructures to fulfill the increased orders and tackle the shortage of aluminum cans.

- In September 2023, Novelis Inc., a prominent provider of sustainable aluminum solutions, signed a significant deal with Ball Corporation, a leading aluminum can manufacturer in North America. The agreement entails Novelis supplying aluminum sheets to Ball's manufacturing facilities across North America.

- The rise in consumer awareness concerning the application of non-carcinogenic materials in packaging and increased demand for lightweight packing are generating high growth prospects for the metal cans market. However, metal cans are challenging to use due to the possibility of replacing them with polymer-based packaging materials, including polyethylene and polyethylene terephthalate (PET).

Metal Cans Industry Segmentation

The Food Segment is Expected to Hold a Significant Share in the Market

- Changing lifestyles at a global level resulted in consumers opting for easy-to-cook food. The younger and individually living populations are consuming more canned food. These users have less time and are budget-restrained, thus opting for products with lower costs and higher convenience.

- Many regular consumers of canned foods choose the products due to the convenience offered and lower cost. Canned foods are more convenient and require less energy and cooking time. Most canned foods take 40% less time to prepare than regular meals.

- Aluminum cans help to preserve the quality of food for a long time. Aluminum cans are completely impervious to oxygen, light, moisture, and other pollutants. They don't rust, are corrosion-resistant, and have one of any package's most extended shelf life. The safety record of aluminum-based food canning is unrivaled.

- Consumers may rest certain that their items have been safely prepared and delivered as they are tamper-resistant and have tamper-evident packaging. Aside from food and beverages, aluminum is used for packaging various products, including aerosols, paint, and other consumer goods. According to the Jamaica Agricultural Commodities Regulatory Authority (JACRA), the import volume of aluminum cans to Japan in 2023 was around 60 million empty aluminum cans and 430 million actual aluminum cans.

- According to reports from the FCC and Statistics Canada, 2024 is poised to witness intense rivalry, particularly in private-label canned and frozen goods. Moreover, a confluence of factors, ranging from rising raw material and packaging expenses to escalating wages, is projected to outpace nominal sales growth, thereby constraining margin enhancements for the year.

North America is Expected to Hold a Significant Share in the Market

- North America is anticipated to positively influence the demand for metal cans during the forecast period due to the increasing demand for healthy beverages, carbonated soft drinks, health drinks, and sucralose juices. Additionally, several significant players impact the business's development through extensive promotional efforts and new research.

- The food and retail industries are the primary factors influencing product demand in the United States. The country has more grocery shops and superstores than ever before, and the expansion of the country's food and retail industries is primarily due to the rise in the number of smaller homes. Consequently, it is driving the demand for smaller packing units.

- In June 2023, Novelis Inc., a leading sustainable aluminum solutions provider, announced it had signed a new long-term contract with Coca-Cola Bottlers' Sales & Services Company, the contracting agent for The Coca-Cola Company's authorized North American bottlers. Novelis is expected to supply Coca-Cola's authorized North American bottlers with aluminum can sheets for The Coca-Cola Company's family of brands. This includes supply from Novelis' plant in Bay Minette, which is currently under construction and expected to begin commissioning in 2025.

- Also, because of the way of life in the United States, there is a greater need for metal cans. Individuals choose wholesome food that is ready to eat and can make it quickly since they have hectic schedules that leave them with little time for cooking. By offering easy packaging and foods that are ready to use, canned food accomplishes this goal. Metal cans are expected to boost the market's growth because they can keep food fresh and high-quality for an extended period.

Metal Cans Industry Overview

The metal cans market is semi-consolidated, with the presence of major players like Ball Corporation, Ardagh Group, Mauser Packaging Solutions, Silgan Containers LLC, and Crown Holdings Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- November 2023: Mauser Packaging Solutions acquired Taenza SA de CV, a prominent Mexican manufacturer specializing in tin-steel aerosol cans and steel pails. Based in Mexico City, Taenza has an extensive presence with five manufacturing facilities across the country and a workforce exceeding 850 employees. Its product line includes aerosol spray cans, steel pails, and paint cans, catering to a varied clientele in the paint, coatings, and chemical sectors.

- November 2023: Sonoco and Ball Corporation signed a significant agreement. Under this agreement, Sonoco, specifically through its Sonoco Phoenix business unit, exclusively supplies balls with easy-open, full-panel ends for their food cans. This collaboration solidifies Sonoco's role as Ball's primary supplier and also extends to a joint marketing and sales effort for these innovative food cans.

- September 2023: Ardagh Group and Crown Holdings Inc. are collaborating with the Can Manufacturers Institute (CMI) to boost aluminum beverage can recycling rates. They are achieving this by funding a robot from EverestLab, an artificial intelligence and robotics company, for a California recycling facility. Caglia Environmental, operating in Fresno, CA, deployed this robot on its "last chance line" at the material recovery facility (MRF). This strategic move aims to salvage over 1 million additional used beverage cans (UBC) annually, which would otherwise head to the landfill.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability of the Packaging Due to Less Usage of Energy

- 5.1.2 Increasing Consumption of Alcoholic and Non-alcoholic Beverages

- 5.2 Market Restraints

- 5.2.1 Presence of Alternate Packaging Solutions as Polyethylene Terephthalate

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By End-user Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Cosmetics and Personal Care

- 6.2.4 Pharmaceuticals

- 6.2.5 Paint

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Spain

- 6.3.2.5 Italy

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Ball Corporation

- 7.1.2 Ardagh Group

- 7.1.3 Mauser Packaging Solutions

- 7.1.4 Silgan Containers LLC

- 7.1.5 Crown Holdings Inc.

- 7.1.6 DS Containers Inc.

- 7.1.7 CCL Container Inc.

- 7.1.8 Toyo Seikan Group Holdings Ltd

- 7.1.9 Pacific Can China Holdings Limited

- 7.1.10 Universal Can Corporation

- 7.1.11 CPMC HOLDINGS Limited (COFCO Group)

- 7.1.12 Showa Denko KK

- 7.1.13 Independent Can Company

- 7.1.14 Hindustan Tin Works Ltd

- 7.1.15 Saudi Arabian Packaging Industry WLL (SAPIN)