デジタルサイネージの世界市場:オファリング別、製品タイプ別、ディスプレイサイズ別、設置場所別、用途別、最終用途別、企業規模別、地域別 - 2030年までの予測

Digital Signage Market by Product (Video Walls, Kiosks, Billboards, Menu Boards, System-on-chip Displays), Resolution (4K, 8K, FHD, HD), Installation Location (Indoor, Outdoor), Software, Display Size, Application, and Region - Global Forecast to 2030

- 発行日

- ページ情報

- 英文 288 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1993563

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

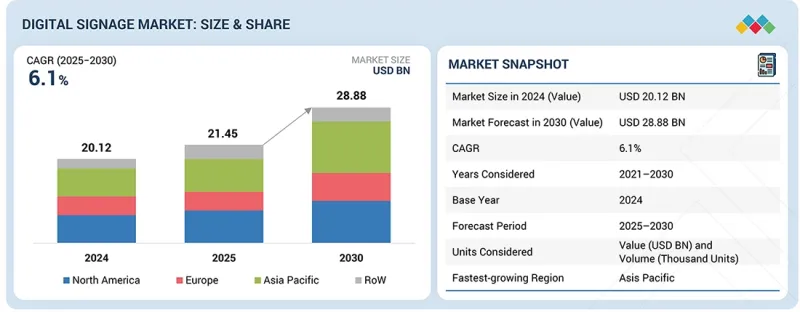

世界のデジタルサイネージの市場規模は、2025年の214億5,000万米ドルから2030年までに288億8,000万米ドルへと拡大すると予測されており、予測期間中のCAGRは6.1%となります。

この成長は、商業施設におけるデジタルサイネージの導入拡大、インフラ関連用途におけるデジタルディスプレイへの需要の高まり、および高解像度の4K・8Kスクリーンへの需要増加によって牽引されています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2021年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 対象単位 | 金額(10億米ドル) |

| セグメント | オファリング別、製品タイプ別、ディスプレイサイズ別、設置場所別、用途別、最終用途別、企業規模別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

ディスプレイ技術の継続的な進歩も、デジタルサイネージソリューション全体の性能、効率、および画質の向上を通じて、市場の成長に寄与しています。

リアルタイムでのコンテンツ配信に対する要件、技術の進歩、およびインテリジェントサイネージソリューションの採用拡大が、デジタルサイネージソフトウェアソリューションへの需要を後押ししています。ソフトウェアのアップグレードやそれに伴うライセンス購入も、このセグメントの成長を促進すると予想されます。同時に、インタラクティブなデジタルサイネージへの需要が高まり続けており、タッチ機能、ジェスチャー認識、その他のインタラクティブ機能をサポートする高度なソフトウェアへのニーズが生まれています。これらの機能はユーザーのエンゲージメントを向上させ、より没入感のある視聴体験を提供します。最新のデジタルサイネージソフトウェアには、通常、ユーザーがコンテンツのスケジュール設定、管理、更新を容易に行える堅牢なコンテンツ管理システム(CMS)が搭載されています。この柔軟性は、ディスプレイの表示内容をタイムリーかつ関連性のある魅力的なものに保つために不可欠です。さらに、分析ツールを内蔵したソフトウェアプラットフォームにより、企業はデジタルサイネージキャンペーンのパフォーマンスを監視し、視聴者のエンゲージメントを評価し、コンテンツの効果を測定することができます。

52インチ以上のディスプレイセグメントは、2025年から2030年にかけて最も急速な成長が見込まれています。この成長は、デジタルサイネージディスプレイ技術における継続的なイノベーションに加え、屋内・屋外を問わず大型スクリーンへの需要が高まっていることが原動力となっています。アジア太平洋全体での急速な都市化も、幅広い用途における屋外デジタルサイネージの利用拡大を後押ししています。さらに、小売業やインフラ分野における大型OLEDディスプレイの利用増加が、市場全体の拡大を支える上で重要な役割を果たしています。

アジア太平洋市場は、予測期間中に最も高い成長率を記録すると予測されています。これは主に、商業、公共機関、インフラ、産業の各セグメントにおける、モノのインターネット(IoT)やデジタルトランスフォーメーション(DX)の取り組みといった技術の導入によって牽引されています。これらの要因により、同地域ではデジタルサイネージに対する需要が高まっています。さらに、都市の発展、消費者の購買力の向上、ユーザー体験の向上に対するニーズの高まりが、アジア太平洋のデジタルサイネージ市場を、様々な商業および公共分野の用途において牽引すると予想されます。

当レポートでは、デジタルサイネージ市場を細分化し、オファリング、ディスプレイサイズ、製品タイプ、設置場所、用途、企業規模、および地域(北米、欧州、アジア太平洋、その他の地域)別に、市場規模(金額ベース)を予測しています。また、デジタルサイネージ市場における市場促進要因・課題についても包括的に分析しています。さらに、これらの市場の定量的側面に加え、定性的側面についても網羅しています。

当レポートは、市場リーダーや新規参入企業に対し、デジタルサイネージ市場全体および関連セグメントの最も正確な売上高に関する情報を提供します。当レポートは、利害関係者が競合情勢を理解し、市場での地位を強化し、効果的な市場参入戦略を策定するための貴重な洞察を得るのに役立ちます。また、主要な市場促進要因、抑制要因、機会、課題に関する情報を提供することで、利害関係者が市場の動向を把握する上でも役立ちます。

当レポートでは、以下のポイントに関する洞察を提供します:

- 主要な促進要因(商業用途におけるデジタルサイネージの導入拡大、インフラ用途におけるデジタルサイネージの需要増加、4Kおよび8K解像度ディスプレイへの需要増、ディスプレイ技術の継続的な進歩)、制約要因(デジタルサイネージの高コスト)、機会(新興国におけるインフラの急速な進展、公共施設でのデジタルサイネージの人気拡大、および産業分野でのデジタルサイネージの採用拡大)、ならびに課題(デジタルサイネージに関連するセキュリティ上の懸念、デジタルサイネージソリューションの設置に伴うインフラ関連の問題、および電力消費と環境への影響)について分析し、デジタルサイネージ市場の成長に影響を与える要因を明らかにしています。

- 製品開発/イノベーション:デジタルサイネージ市場における、今後の技術動向、研究開発活動、および新製品の発売、事業拡大、契約、提携、買収などの戦略に関する詳細な洞察

- 市場開発:収益性の高い市場に関する包括的な情報--当レポートでは、様々な地域におけるデジタルサイネージ市場を分析しています

- 市場の多様化:デジタルサイネージ市場における新製品、未開拓地域、最近の動向、および投資に関する網羅的な情報

- 競合分析:サムスン(韓国)、LGエレクトロニクス(韓国)、シャープ(日本)、LEYARD(中国)、ソニーグループ(日本)などの主要企業の市場シェア、成長戦略、製品ラインナップに関する詳細な評価。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズと未開拓分野

- 相互接続された市場と異業種間の機会

- ティア1/2/3企業による戦略的な動き

第5章 業界動向

- ポーターの5つの競争要因分析

- マクロ経済指標

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 貿易分析

- 2026年~2027年の主な会議およびイベント

- 顧客ビジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ、2021年~2024年

- 事例研究分析

- 2025年米国関税の影響- デジタルサイネージ市場

第6章 技術進歩、AIによる影響、特許、イノベーション、そして将来の応用

- 主要な新興技術

- 補完的技術

- 隣接技術

- 技術/製品ロードマップ

- 特許分析

- AIがデジタルサイネージ市場に与える影響

第7章 規制状況

- 地域規制および遵守事項

- 規制機関、政府機関、その他の組織

- 基準

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 購買プロセスに関わる主要な利害関係者とその評価基準

- 導入における障壁と内部課題

- 様々なエンドユーザーのアンメットニーズ

第9章 デジタルサイネージ市場(オファリング別)

- ハードウェア

- ソフトウェア

- サービス

第10章 デジタルサイネージ市場(製品タイプ別)

- ビデオウォール

- スタンドアロンディスプレイ

第11章 デジタルサイネージ市場(ディスプレイサイズ別)

- 32インチ未満

- 32~52インチ

- 52インチ超

第12章 デジタルサイネージ市場(設置場所別)

- 屋内

- 屋外

第13章 デジタルサイネージ市場(用途別)

- 情報とメッセージング

- 道案内

- 広告・プロモーション

- トランザクション有効化

- エンターテインメント

- 企業コミュニケーションおよびプロセス管理

第14章 デジタルサイネージ市場(用途別)

- 商業

- インフラストラクチャ

- 機関

- 工業

第15章 デジタルサイネージ市場(企業規模別)

- 小規模オフィス/ホームオフィス

- 中小企業

- 大企業

第16章 デジタルサイネージ市場(地域別)

- 北米

- 北米のマクロ経済見通し

- 米国

- カナダ

- メキシコ

- 欧州

- 欧州のマクロ経済見通し

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- ベルギー

- 北欧諸国

- その他

- アジア太平洋

- アジア太平洋のマクロ経済見通し

- 中国

- オーストラリア

- 日本

- インド

- 韓国

- 東南アジア

- その他

- その他の地域

- マクロ経済見通し

- 中東

- アフリカ

- 南米

第17章 競合情勢

- 概要

- 主要参入企業の戦略/強み、2021年~2025年

- 市場シェア分析、2025年

- ブランド/製品比較

- 企業評価マトリックス:主要企業、2025年

- 企業評価マトリックス:スタートアップ/中小企業、2025年

- 企業評価と財務指標

- 競合シナリオ

第18章 企業プロファイル

- 主要参入企業

- SAMSUNG

- LG ELECTRONICS

- SHARP CORPORATION

- LEYARD

- SONY GROUP CORPORATION

- BARCO

- PANASONIC HOLDINGS CORPORATION

- AUO CORPORATION

- DAKTRONICS

- BRIGHTSIGN LLC

- その他の企業

- STRATACACHE

- BENQ

- INTUIFACE

- DELTA ELECTRONICS, INC.

- BROADSIGN INTERNATIONAL, LLC

- CHRISTIE DIGITAL SYSTEMS USA, INC.

- CISCO SYSTEMS, INC.

- AESYS S.P.A.

- TATTILE S.R.L.

- PPDS

- NAVORI LABS

- VIEWSONIC

- 22 MILES

- FLIPNODE LLC

- SPECTRIO LLC

第19章 調査手法

第20章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 288 Pages

- 納期

- 即納可能