|

|

市場調査レポート

商品コード

1678866

船舶の世界市場:運航形態別、トン数別、船舶タイプ別、地域別 - 2030年までの予測Marine Vessels Market by Ship Type (Destroyer, Frigate, Corvette, Patrol Vessels, Passenger Vessels, Container Vessels, Tanker), Tonnage (100 - 500 DWT, 500 - 5,000 DWT, 5,000 - 15,000 DWT, >15,000 DWT), Operation and Region - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 船舶の世界市場:運航形態別、トン数別、船舶タイプ別、地域別 - 2030年までの予測 |

|

出版日: 2025年03月01日

発行: MarketsandMarkets

ページ情報: 英文 379 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

船舶の市場規模は、2024年の1,111億米ドルから2030年には1,336億3,000万米ドルに達し、CAGRは3.1%になると予測されています。

船舶市場は、いくつかの重要な要因の影響を受けています。世界貿易は、さまざまなタイプの船舶に対する需要を増大させています。軍事海軍の成長も市場の拡大に貢献しています。より大型で汎用性の高い船舶のニーズは、世界の効率的な物資輸送の需要に起因します。旅客と観光のニーズの高まりは、船隊の拡大と技術のアップグレードを促進しています。多くのクルーズラインは、ユニークな体験を求める旅行者の増加に対応するため、さらに船を増やしています。市場の改善には、戦略的な船隊更新が重要です。燃費効率の高い新造船は、環境基準を満たし、コストを下げるのに役立ちます。持続可能な海運慣行へのシフトは、排出量を削減する国際規則に従うことがより重要になっています。高いコストと厳しい安全規制は、この分野の成長を鈍らせる可能性があります。新規参入企業は、こうした要因が生み出す課題に直面します。既存企業は、関連性を維持するために継続的なイノベーションを追求しなければなりません。競争力を維持し、変化する市場の需要に対応するためには、研究開発への投資を行う必要があります。したがって、業界関係者と政府は協力関係を促進しなければなりません。この協力が成長を促し、持続可能な海事慣行の確立につながります。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2030年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2030年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント別 | 運航形態別、トン数別、船舶タイプ別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

貨物船は商業海運の最も重要な部分となりつつあります。これらの船舶は、様々な商品を海上輸送することにより、世界貿易において重要な役割を果たしています。このグループにはさまざまなタイプの船舶が含まれます。コンテナ船は包装された製品を運びます。バルクキャリアーは原材料を輸送します。タンカーは液体を運び、ドライカーゴ船は様々な製品を運び、バージ船は浅瀬で商品を運びます。これらの船舶は、製品が大洋をスムーズに流れることを保証します。世界なサプライチェーンを支え、商品が世界中の市場に届くことを保証しています。より速く、より信頼性の高い海運への需要が高まるにつれ、業界は新しい技術を採用しています。最新の航行システム、オートメーション、環境に優しい燃料は、効率を改善し、安全性を高め、環境への影響を軽減します。投資家は、これらの船舶がより効率的に運航できるよう、デジタル追跡システムや予知保全に資金を投入しています。このアプローチは、ダウンタイムを削減し、精度を向上させる。世界貿易が拡大し続ける中、貨物船は国際商業と経済成長に不可欠な存在であり続け、世界中の地域社会をつないでいます。

哨戒艦は国境警備と海上警備に不可欠であるため、軍用艦の種類では最大のセグメントです。これらの小型で効率的な船舶は、領海を守るための長時間のパトロールや監視用に設計されています。密輸や海賊行為などの違法行為を制限する上で重要な役割を果たし、捜索救助活動にも参加します。哨戒艦は、大型の艦艇よりも費用対効果が高いです。沿岸域の法と秩序を維持するための効率的なソリューションとして機能します。各国が効果的な海上安全保障と予算管理をより重視する中、巡視船は今日の海軍艦隊における重要な資産としてますます認識されるようになっています。

欧州は船舶市場で最も急成長している地域です。この成長は、英国、ドイツ、フランス、イタリアにおける様々な造船活動からもたらされています。欧州の造船所は世界的に重要な役割を果たしており、特にクルーズ船やドライカーゴ船の新規受注が増えています。ドライカーゴの人気は、納期が短いことに由来しており、同地域の高い需要に応えています。欧州の造船所は、先進技術と持続可能な手法にも注力しています。環境に優しい燃料や効率的な設計は、厳格な環境規則を遵守するために使用されています。欧州の造船業界には、大規模な造船所と、洋上風力支援船やリバークルーズ船のようなニッチな船舶に特化した小規模な専門施設の両方があります。これらの要因により、欧州は世界の海事産業における影響力を強化し、品質、革新性、適応性に対する評判を確固たるものにしています。

当レポートでは、世界の船舶市場について調査し、運航形態別、トン数別、船舶タイプ別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 運用データ

- 顧客ビジネスに影響を与える動向と混乱

- エコシステムマッピング

- バリューチェーン分析

- 価格分析

- ケーススタディ分析

- 貿易分析

- 2025年~2026年の主な会議とイベント

- 関税と規制状況

- 主な利害関係者と購入基準

- 技術分析

- 投資と資金調達のシナリオ

- 総所有コスト

- ビジネスモデル

- 部品表

- 生成AIが海洋産業に与える影響

- マクロ経済見通し

第6章 業界の動向

- イントロダクション

- 技術動向

- 技術ロードマップ

- メガトレンドの影響

- サプライチェーン分析

- 特許分析

第7章 船舶市場(運航形態別)

- イントロダクション

- 内陸

- 航海

第8章 船舶市場(トン数別)

- イントロダクション

- 100~500 DWT

- 500~5,000 DWT

- 5,000~15,000 DWT

- 15,000 DWT以上

第9章 船舶市場(船舶タイプ別)

- イントロダクション

- 軍隊

- 商用

第10章 船舶市場(地域別)

- イントロダクション

- 北米

- PESTLE分析

- 米国

- カナダ

- 欧州

- PESTLE分析

- 英国

- ドイツ

- フランス

- イタリア

- ノルウェー

- その他

- アジア太平洋

- PESTLE分析

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- シンガポール

- その他

- 中東

- PESTLE分析

- 湾岸協力会議(GCC)

- イスラエル

- トルコ

- その他の地域

- PESTLE分析

- ラテンアメリカ

- アフリカ

第11章 競合情勢

- イントロダクション

- 主要参入企業の戦略/強み、2020年~2024年

- 収益分析

- 市場シェア分析

- ブランド/製品比較

- 会社の財務指標

- 企業評価マトリックス:主要参入企業、2023年

- 企業概要:主要参入企業

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオ

第12章 企業プロファイル

- 主要参入企業

- CHINA STATE SHIPBUILDING CORPORATION

- HD HYUNDAI HEAVY INDUSTRIES CO., LTD.

- HANWHA OCEAN CO., LTD.

- HUNTINGTON INGALLS INDUSTRIES

- FINCANTIERI S.P.A.

- SAMSUNG HEAVY INDUSTRIES CO., LTD

- IMABARI SHIPBUILDING CO., LTD.

- JAPAN MARINE UNITED CORPORATION

- MITSUBISHI HEAVY INDUSTRIES, LTD.

- SUMITOMO HEAVY INDUSTRIES, LTD.

- CHANTIERS DE L'ATLANTIQUE

- MEYER WERFT GMBH & CO. KG

- DAMEN SHIPYARDS GROUP

- NAVANTIA

- SEATRIUM

- MAZAGON DOCK SHIPBUILDERS LIMITED

- COCHIN SHIPYARD LIMITED

- AUSTAL

- NAVAL GROUP

- THYSSENKRUPP AG

- HARLAND & WOLFF

- BRODOSPLIT JSC

- COSCO SHIPPING HEAVY INDUSTRY CO., LTD.

- YANGZIJIANG SHIPBUILDING

- KAWASAKI HEAVY INDUSTRIES, LTD.

- その他の企業

- SILENT YACHTS

- CANDELA

- X SHORE

- MASTER BOAT BUILDERS, INC.

- VELA

第13章 付録

List of Tables

- TABLE 1 INCLUSIONS AND EXCLUSIONS

- TABLE 2 USD EXCHANGE RATES

- TABLE 3 US NAVY FIVE-YEAR SHIPBUILDING PLAN, 2025-2029

- TABLE 4 SEABORNE CRUISE PASSENGERS EMBARKED AND DISEMBARKED IN ALL PORTS IN SELECTED YEARS, 2012-2022

- TABLE 5 CRUISE PASSENGER VOLUME, 2023 (MILLION)

- TABLE 6 WORLD FLEET: TOTAL NUMBER OF SHIPS, BY AGE AND SIZE, 2023

- TABLE 7 ORDER BOOK FOR DUAL FUELS, 2023

- TABLE 8 COMMERCIAL VESSELS, ACTIVE FLEET, BY SHIP TYPE, 2023

- TABLE 9 MILITARY VESSELS, ACTIVE FLEET, BY SHIP TYPE, 2023

- TABLE 10 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 11 IMPORT DATA FOR HS CODE 89-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 12 EXPORT DATA FOR HS CODE 89-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD THOUSAND)

- TABLE 13 KEY CONFERENCES AND EVENTS, 2024-2026

- TABLE 14 TARIFFS FOR SHIPS, BOATS, AND FLOATING STRUCTURES (PRODUCT HARMONIZED SYSTEM CODE: 89)

- TABLE 15 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 MIDDLE EAST: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 LATIN AMERICA & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY SHIP TYPE (%)

- TABLE 21 KEY BUYING CRITERIA, BY SHIP TYPE

- TABLE 22 COMPARISON BETWEEN BUSINESS MODELS

- TABLE 23 IMPACT OF AI ON MARINE APPLICATIONS

- TABLE 24 KEY GREEN TECHNOLOGIES AND THEIR IMPACT

- TABLE 25 AUTONOMOUS SHIP CASES AND REGULATORY GUIDELINES OVERVIEW

- TABLE 26 PATENT ANALYSIS

- TABLE 27 MARINE VESSELS MARKET, ACTIVE FLEETS, BY OPERATION, 2020-2023 (UNITS)

- TABLE 28 MARINE VESSELS MARKET, ACTIVE FLEETS, BY OPERATION, 2024-2030 (UNITS)

- TABLE 29 MARINE VESSELS MARKET, ACTIVE FLEETS, BY TONNAGE, 2020-2023 (UNITS)

- TABLE 30 MARINE VESSELS MARKET, ACTIVE FLEETS, BY TONNAGE, 2024-2030 (UNITS)

- TABLE 31 MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 32 MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 33 MARINE VESSELS MARKET, NEW DELIVERIES, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 34 MARINE VESSELS MARKET, NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 35 MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 36 MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 37 MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 38 MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 39 SPECIFICATIONS AND DIMENSIONS OF CRUISE SHIPS, BY TYPE

- TABLE 40 CRUISE SHIPS DELIVERED IN 2023

- TABLE 41 SPECIFICATIONS AND DIMENSIONS OF CONTAINER SHIPS, BY TYPE

- TABLE 42 MARINE VESSELS MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 43 MARINE VESSELS MARKET, BY REGION, 2024-2030 (USD MILLION)

- TABLE 44 MARINE VESSELS MARKET, ACTIVE FLEETS, BY REGION, 2020-2023 (UNITS)

- TABLE 45 MARINE VESSELS MARKET, ACTIVE FLEETS, BY REGION, 2024-2030 (UNITS)

- TABLE 46 MARINE VESSELS MARKET, NEW DELIVERIES, BY REGION, 2020-2023 (UNITS)

- TABLE 47 MARINE VESSELS MARKET, NEW DELIVERIES, BY REGION, 2024-2030 (UNITS)

- TABLE 48 NORTH AMERICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COUNTRY, 2020-2023 (UNITS)

- TABLE 49 NORTH AMERICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COUNTRY, 2024-2030 (UNITS)

- TABLE 50 NORTH AMERICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 51 NORTH AMERICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 52 NORTH AMERICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 53 NORTH AMERICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 54 NORTH AMERICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 55 NORTH AMERICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 56 US: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 57 US: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 58 US: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 59 US: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 60 US: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 61 US: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 62 CANADA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 63 CANADA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 64 CANADA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 65 CANADA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 66 CANADA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 67 CANADA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 68 EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COUNTRY, 2020-2023 (UNITS)

- TABLE 69 EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COUNTRY, 2024-2030 (UNITS)

- TABLE 70 EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 71 EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 72 EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 73 EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 74 EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 75 EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 76 UK: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 77 UK: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 78 UK: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 79 UK: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 80 UK: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 81 UK: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 82 GERMANY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 83 GERMANY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 84 GERMANY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 85 GERMANY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 86 GERMANY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 87 GERMANY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 88 FRANCE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 89 FRANCE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 90 FRANCE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 91 FRANCE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 92 FRANCE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 93 FRANCE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 94 ITALY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 95 ITALY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 96 ITALY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 97 ITALY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 98 ITALY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 99 ITALY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 100 NORWAY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 101 NORWAY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 102 NORWAY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 103 NORWAY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 104 NORWAY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 105 NORWAY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 106 REST OF EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 107 REST OF EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 108 REST OF EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 109 REST OF EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 110 REST OF EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 111 REST OF EUROPE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 112 ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COUNTRY, 2020-2023 (UNITS)

- TABLE 113 ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COUNTRY, 2024-2030 (UNITS)

- TABLE 114 ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 115 ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 116 ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 117 ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 118 ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 119 ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 120 CHINA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 121 CHINA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 122 CHINA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 123 CHINA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 124 CHINA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 125 CHINA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 126 INDIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 127 INDIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 128 INDIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 129 INDIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 130 INDIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 131 INDIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 132 JAPAN: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 133 JAPAN: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 134 JAPAN: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 135 JAPAN: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 136 JAPAN: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 137 JAPAN: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 138 AUSTRALIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 139 AUSTRALIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 140 AUSTRALIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 141 AUSTRALIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 142 AUSTRALIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 143 AUSTRALIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 144 SOUTH KOREA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 145 SOUTH KOREA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 146 SOUTH KOREA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 147 SOUTH KOREA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 148 SOUTH KOREA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 149 SOUTH KOREA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 150 SINGAPORE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 151 SINGAPORE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 152 SINGAPORE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 153 SINGAPORE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 154 SINGAPORE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 155 SINGAPORE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 156 REST OF ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 157 REST OF ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 158 REST OF ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 159 REST OF ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 160 REST OF ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 161 REST OF ASIA PACIFIC: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 162 MIDDLE EAST: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COUNTRY, 2020-2023 (UNITS)

- TABLE 163 MIDDLE EAST: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COUNTRY, 2024-2030 (UNITS)

- TABLE 164 MIDDLE EAST: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 165 MIDDLE EAST: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 166 MIDDLE EAST: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 167 MIDDLE EAST: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 168 MIDDLE EAST: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 169 MIDDLE EAST: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 170 UAE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 171 UAE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 172 UAE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 173 UAE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 174 UAE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 175 UAE: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 176 SAUDI ARABIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 177 SAUDI ARABIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 178 SAUDI ARABIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 179 SAUDI ARABIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 180 SAUDI ARABIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 181 SAUDI ARABIA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 182 ISRAEL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 183 ISRAEL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 184 ISRAEL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 185 ISRAEL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 186 ISRAEL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 187 ISRAEL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 188 TURKEY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 189 TURKEY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 190 TURKEY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 191 TURKEY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 192 TURKEY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 193 TURKEY: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 194 REST OF THE WORLD: MARINE VESSELS MARKET, ACTIVE FLEETS, BY REGION, 2020-2023 (UNITS)

- TABLE 195 REST OF THE WORLD: MARINE VESSELS MARKET, ACTIVE FLEETS, BY REGION, 2024-2030 (UNITS)

- TABLE 196 REST OF THE WORLD: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 197 REST OF THE WORLD: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 198 REST OF THE WORLD: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 199 REST OF THE WORLD: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 200 REST OF THE WORLD: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 201 REST OF THE WORLD: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 202 BRAZIL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 203 BRAZIL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 204 BRAZIL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 205 BRAZIL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 206 BRAZIL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 207 BRAZIL: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 208 MEXICO: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 209 MEXICO: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 210 MEXICO: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 211 MEXICO: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 212 MEXICO: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 213 MEXICO: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 214 SOUTH AFRICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 215 SOUTH AFRICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 216 SOUTH AFRICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2020-2023 (UNITS)

- TABLE 217 SOUTH AFRICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY MILITARY SHIP TYPE, 2024-2030 (UNITS)

- TABLE 218 SOUTH AFRICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2020-2023 (UNITS)

- TABLE 219 SOUTH AFRICA: MARINE VESSELS MARKET, ACTIVE FLEETS, BY COMMERCIAL SHIP TYPE, 2024-2030 (UNITS)

- TABLE 220 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2024

- TABLE 221 MARINE VESSELS MARKET: DEGREE OF COMPETITION

- TABLE 222 COMPANY MILITARY SHIP TYPE FOOTPRINT

- TABLE 223 COMPANY COMMERCIAL SHIP TYPE FOOTPRINT

- TABLE 224 COMPANY OPERATIONS FOOTPRINT

- TABLE 225 COMPANY REGIONAL FOOTPRINT

- TABLE 226 DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 227 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 228 MARINE VESSELS MARKET: PRODUCT LAUNCHES, MAY 2021-SEPTEMBER 2024

- TABLE 229 MARINE VESSELS MARKET: DEALS, OCTOBER 2020-DECEMBER 2024

- TABLE 230 MARINE VESSELS MARKET: OTHERS, JANUARY 2020-JANUARY 2025

- TABLE 231 CHINA STATE SHIPBUILDING CORPORATION: COMPANY OVERVIEW

- TABLE 232 CHINA STATE SHIPBUILDING CORPORATION: PRODUCTS OFFERED

- TABLE 233 CHINA STATE SHIPBUILDING CORPORATION: OTHER DEVELOPMENTS

- TABLE 234 HD HYUNDAI HEAVY INDUSTRIES CO., LTD.: COMPANY OVERVIEW

- TABLE 235 HD HYUNDAI HEAVY INDUSTRIES CO., LTD.: PRODUCTS OFFERED

- TABLE 236 HD HYUNDAI HEAVY INDUSTRIES CO., LTD.: DEALS

- TABLE 237 HD HYUNDAI HEAVY INDUSTRIES CO., LTD.: OTHER DEVELOPMENTS

- TABLE 238 HANWHA OCEAN CO., LTD.: COMPANY OVERVIEW

- TABLE 239 HANWHA OCEAN CO., LTD.: PRODUCTS OFFERED

- TABLE 240 HANWHA OCEAN CO., LTD.: PRODUCT LAUNCHES

- TABLE 241 HANWHA OCEAN CO., LTD.: DEALS

- TABLE 242 HANWHA OCEAN CO., LTD.: OTHER DEVELOPMENTS

- TABLE 243 HUNTINGTON INGALLS INDUSTRIES: COMPANY OVERVIEW

- TABLE 244 HUNTINGTON INGALLS INDUSTRIES: PRODUCTS OFFERED

- TABLE 245 HUNTINGTON INGALLS INDUSTRIES: OTHER DEVELOPMENTS

- TABLE 246 FINCANTIERI S.P.A.: COMPANY OVERVIEW

- TABLE 247 FINCANTIERI S.P.A.: PRODUCTS OFFERED

- TABLE 248 FINCANTIERI S.P.A.: PRODUCT LAUNCHES

- TABLE 249 FINCANTIERI S.P.A.: DEALS

- TABLE 250 FINCANTIERI S.P.A.: OTHER DEVELOPMENTS

- TABLE 251 SAMSUNG HEAVY INDUSTRIES CO., LTD: COMPANY OVERVIEW

- TABLE 252 SAMSUNG HEAVY INDUSTRIES CO., LTD: PRODUCTS OFFERED

- TABLE 253 SAMSUNG HEAVY INDUSTRIES CO., LTD: OTHER DEVELOPMENTS

- TABLE 254 IMABARI SHIPBUILDING CO., LTD.: COMPANY OVERVIEW

- TABLE 255 IMABARI SHIPBUILDING CO., LTD.: PRODUCTS OFFERED

- TABLE 256 IMABARI SHIPBUILDING CO., LTD.: DEALS

- TABLE 257 IMABARI SHIPBUILDING CO.,LTD: OTHER DEVELOPMENTS

- TABLE 258 JAPAN MARINE UNITED CORPORATION: COMPANY OVERVIEW

- TABLE 259 JAPAN MARINE UNITED CORPORATION: PRODUCTS OFFERED

- TABLE 260 JAPAN MARINE UNITED CORPORATION: PRODUCT LAUNCHES

- TABLE 261 JAPAN MARINE UNITED CORPORATION: OTHER DEVELOPMENTS

- TABLE 262 MITSUBISHI HEAVY INDUSTRIES, LTD.: COMPANY OVERVIEW

- TABLE 263 MITSUBISHI HEAVY INDUSTRIES, LTD.: PRODUCTS OFFERED

- TABLE 264 MITSUBISHI HEAVY INDUSTRIES, LTD.: DEALS

- TABLE 265 MITSUBISHI HEAVY INDUSTRIES, LTD.: OTHER DEVELOPMENTS

- TABLE 266 SUMITOMO HEAVY INDUSTRIES, LTD.: COMPANY OVERVIEW

- TABLE 267 SUMITOMO HEAVY INDUSTRIES, LTD.: PRODUCTS OFFERED

- TABLE 268 CHANTIERS DE L'ATLANTIQUE: COMPANY OVERVIEW

- TABLE 269 CHANTIERS DE L'ATLANTIQUE: PRODUCTS OFFERED

- TABLE 270 CHANTIERS DE L'ATLANTIQUE: DEALS

- TABLE 271 CHANTIERS DE L'ATLANTIQUE: OTHER DEVELOPMENTS

- TABLE 272 MEYER WERFT GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 273 MEYER WERFT GMBH & CO. KG: PRODUCTS OFFERED

- TABLE 274 MEYER WERFT GMBH & CO. KG: DEALS

- TABLE 275 MEYER WERFT GMBH & CO. KG: OTHER DEVELOPMENTS

- TABLE 276 DAMEN SHIPYARDS GROUP: COMPANY OVERVIEW

- TABLE 277 DAMEN SHIPYARDS GROUP: PRODUCTS OFFERED

- TABLE 278 DAMEN SHIPYARDS GROUP: PRODUCT LAUNCHES

- TABLE 279 DAMEN SHIPYARDS GROUP: DEALS

- TABLE 280 DAMEN SHIPYARDS GROUP: OTHER DEVELOPMENTS

- TABLE 281 NAVANTIA: COMPANY OVERVIEW

- TABLE 282 NAVANTIA: PRODUCTS OFFERED

- TABLE 283 NAVANTIA: OTHER DEVELOPMENTS

- TABLE 284 SEATRIUM: COMPANY OVERVIEW

- TABLE 285 SEATRIUM: PRODUCTS OFFERED

- TABLE 286 MAZAGON DOCK SHIPBUILDERS LIMITED: COMPANY OVERVIEW

- TABLE 287 MAZAGON DOCK SHIPBUILDERS LIMITED: PRODUCTS OFFERED

- TABLE 288 MAZAGON DOCK SHIPBUILDERS LIMITED: OTHER DEVELOPMENTS

- TABLE 289 COCHIN SHIPYARD LIMITED: COMPANY OVERVIEW

- TABLE 290 COCHIN SHIPYARD LIMITED: PRODUCTS OFFERED

- TABLE 291 COCHIN SHIPYARD LIMITED: PRODUCT LAUNCHES

- TABLE 292 COCHIN SHIPYARD LIMITED: DEALS

- TABLE 293 COCHIN SHIPYARD LIMITED: OTHER DEVELOPMENTS

- TABLE 294 AUSTAL: COMPANY OVERVIEW

- TABLE 295 AUSTAL: PRODUCTS OFFERED

- TABLE 296 AUSTAL: DEALS

- TABLE 297 AUSTAL: OTHER DEVELOPMENTS

- TABLE 298 NAVAL GROUP: COMPANY OVERVIEW

- TABLE 299 NAVAL GROUP: PRODUCTS OFFERED

- TABLE 300 NAVAL GROUP: PRODUCT LAUNCHES

- TABLE 301 NAVAL GROUP: OTHER DEVELOPMENTS

- TABLE 302 THYSSENKRUPP AG: COMPANY OVERVIEW

- TABLE 303 THYSSENKRUPP AG: PRODUCTS OFFERED

- TABLE 304 HARLAND & WOLFF: COMPANY OVERVIEW

- TABLE 305 HARLAND & WOLFF: PRODUCTS OFFERED

- TABLE 306 BRODOSPLIT JSC: COMPANY OVERVIEW

- TABLE 307 BRODOSPLIT JSC: PRODUCTS OFFERED

- TABLE 308 BRODOSPLIT JSC: PRODUCT LAUNCHES

- TABLE 309 BRODOSPLIT JSC: OTHER DEVELOPMENTS

- TABLE 310 COSCO SHIPPING HEAVY INDUSTRY CO., LTD.: COMPANY OVERVIEW

- TABLE 311 COSCO SHIPPING HEAVY INDUSTRY CO., LTD.: PRODUCTS OFFERED

- TABLE 312 COSCO SHIPPING HEAVY INDUSTRY CO., LTD.: OTHER DEVELOPMENTS

- TABLE 313 YANGZIJIANG SHIPBUILDING: COMPANY OVERVIEW

- TABLE 314 YANGZIJIANG SHIPBUILDING: PRODUCTS OFFERED

- TABLE 315 YANGZIJIANG SHIPBUILDING: OTHER DEVELOPMENTS

- TABLE 316 KAWASAKI HEAVY INDUSTRIES, LTD.: COMPANY OVERVIEW

- TABLE 317 KAWASAKI HEAVY INDUSTRIES, LTD.: PRODUCTS OFFERED

- TABLE 318 KAWASAKI HEAVY INDUSTRIES, LTD.: OTHER DEVELOPMENTS

- TABLE 319 SILENT YACHTS: COMPANY OVERVIEW

- TABLE 320 CANDELA: COMPANY OVERVIEW

- TABLE 321 X SHORE: COMPANY OVERVIEW

- TABLE 322 MASTER BOAT BUILDERS, INC.: COMPANY OVERVIEW

- TABLE 323 VELA: COMPANY OVERVIEW

- TABLE 324 MARINE VESSELS MARKET: LAUNDRY LIST OF COMPANIES

- TABLE 325 DEFENSE PROGRAMS

List of Figures

- FIGURE 1 MARINE VESSELS MARKET SEGMENTATION

- FIGURE 2 RESEARCH PROCESS FLOW

- FIGURE 3 RESEARCH DESIGN

- FIGURE 4 BREAKDOWN OF PRIMARIES

- FIGURE 5 BOTTOM-UP APPROACH

- FIGURE 6 TOP-DOWN APPROACH

- FIGURE 7 DATA TRIANGULATION

- FIGURE 8 COMMERCIAL TO BE FASTER-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 9 >15,000 DWT TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 10 SEAFARING SEGMENT TO SECURE LEADING POSITION DURING FORECAST PERIOD

- FIGURE 11 ASIA PACIFIC TO BE LARGEST MARKET FOR MARINE VESSELS DURING FORECAST PERIOD

- FIGURE 12 EXPANDING GLOBAL TRADE AND MILITARY NAVY MODERNIZATION TO DRIVE MARKET

- FIGURE 13 COMMERCIAL SEGMENT TO ACCOUNT FOR HIGHER SHARE IN 2024

- FIGURE 14 PATROL VESSEL TO BE DOMINANT SEGMENT DURING FORECAST PERIOD

- FIGURE 15 CARGO VESSELS TO LEAD COMMERCIAL SHIPS SEGMENT DURING FORECAST PERIOD

- FIGURE 16 >15,000 DWT SEGMENT TO BE DOMINANT DURING FORECAST PERIOD

- FIGURE 17 SEAFARING SEGMENT TO BE LARGER THAN INLAND SEGMENT DURING FORECAST PERIOD

- FIGURE 18 CHINA TO HAVE LARGEST NUMBER OF ACTIVE FLEETS, 2024

- FIGURE 19 MARINE VESSELS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 20 TREND OF WORLD TRADE FROM 2002 TO 2022

- FIGURE 21 SHIPPING DEMAND IN BILLION TONNES MILES

- FIGURE 22 EVOLUTION OF GOODS LOADED WORLDWIDE, BY TYPE OF SHIPS (MILLION TONNES)

- FIGURE 23 WORLD MILITARY EXPENDITURE, BY REGION, 2014-2024

- FIGURE 24 OCEAN-GOING CRUISE PASSENGERS TREND AND PROJECTION

- FIGURE 25 ORDERBOOK FOR ALTERNATIVE FUEL SHIPS, 2023 (UNITS)

- FIGURE 26 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 27 ECOSYSTEM ANALYSIS

- FIGURE 28 VALUE CHAIN ANALYSIS

- FIGURE 29 IMPORT DATA FOR HS CODE 89-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD THOUSAND)

- FIGURE 30 EXPORT DATA FOR HS CODE 89-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD THOUSAND)

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY SHIP TYPE

- FIGURE 32 KEY BUYING CRITERIA, BY SHIP TYPE

- FIGURE 33 INVESTMENT AND FUNDING SCENARIO, 2020-2024

- FIGURE 34 TOTAL COST OF OWNERSHIP FOR MARINE VESSELS

- FIGURE 35 TOTAL COST OF OWNERSHIP (TCO) COMPARISON OF COMMERCIAL VESSELS, BY PROPULSION

- FIGURE 36 BILL OF MATERIALS FOR MILITARY VESSELS

- FIGURE 37 USE OF AI IN MARINE INDUSTRY

- FIGURE 38 IMPACT OF AI ON MARINE VESSELS MARKET

- FIGURE 39 MACROECONOMIC OUTLOOK FOR NORTH AMERICA, EUROPE, ASIA PACIFIC, AND MIDDLE EAST

- FIGURE 40 TECHNOLOGY TRENDS IN MARINE VESSELS MARKET

- FIGURE 41 EVOLUTION OF MARINE VESSEL TECHNOLOGIES

- FIGURE 42 TECHNOLOGY ROADMAP OF MARINE VESSELS

- FIGURE 43 EMERGING TRENDS IN MARINE VESSELS MARKET

- FIGURE 44 SUPPLY CHAIN ANALYSIS

- FIGURE 45 PATENT ANALYSIS, 2015-2025

- FIGURE 46 SEAFARING TO BE FASTER-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 47 >15,000 DWT TO ACQUIRE LARGEST SHARE DURING FORECAST PERIOD

- FIGURE 48 COMMERCIAL TO BE LARGER AND FASTER-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 49 PATROL VESSEL SEGMENT TO DOMINATE DURING FORECAST PERIOD

- FIGURE 50 CARGO VESSELS TO BE LARGER AND FASTER-GROWING SEGMENT DURING FORECAST PERIOD

- FIGURE 51 MARINE VESSELS MARKET, BY REGION, 2024-2030

- FIGURE 52 NORTH AMERICA: MARINE VESSELS MARKET SNAPSHOT

- FIGURE 53 US: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 54 CANADA: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 55 EUROPE: MARINE VESSELS MARKET SNAPSHOT

- FIGURE 56 UK: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 57 GERMANY: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 58 FRANCE: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 59 ITALY: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 60 NORWAY: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 61 REST OF EUROPE: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 62 ASIA PACIFIC: MARINE VESSELS MARKET SNAPSHOT

- FIGURE 63 CHINA: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 64 INDIA: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 65 JAPAN: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 66 AUSTRALIA: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 67 SOUTH KOREA: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 68 SINGAPORE: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 69 REST OF ASIA PACIFIC: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 70 MIDDLE EAST: MARINE VESSELS MARKET SNAPSHOT

- FIGURE 71 UAE: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 72 SAUDI ARABIA: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 73 ISRAEL: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 74 TURKEY: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 75 REST OF THE WORLD: MARINE VESSELS MARKET SNAPSHOT

- FIGURE 76 BRAZIL: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 77 MEXICO: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 78 SOUTH AFRICA: NEW DELIVERIES, BY SHIP TYPE, 2024-2030 (UNITS)

- FIGURE 79 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2020-2023

- FIGURE 80 MARKET SHARE ANALYSIS OF TOP FIVE PLAYERS, 2023

- FIGURE 81 BRAND/PRODUCT COMPARISON

- FIGURE 82 FINANCIAL METRICS OF PROMINENT PLAYERS

- FIGURE 83 VALUATION OF PROMINENT MARKET PLAYERS

- FIGURE 84 MARINE VESSELS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 85 COMPANY FOOTPRINT

- FIGURE 86 MARINE VESSELS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- FIGURE 87 HD HYUNDAI HEAVY INDUSTRIES CO., LTD.: COMPANY SNAPSHOT

- FIGURE 88 HANWHA OCEAN CO., LTD.: COMPANY SNAPSHOT

- FIGURE 89 HUNTINGTON INGALLS INDUSTRIES: COMPANY SNAPSHOT

- FIGURE 90 FINCANTIERI S.P.A.: COMPANY SNAPSHOT

- FIGURE 91 SAMSUNG HEAVY INDUSTRIES CO., LTD: COMPANY SNAPSHOT

- FIGURE 92 MITSUBISHI HEAVY INDUSTRIES, LTD.: COMPANY SNAPSHOT

- FIGURE 93 SUMITOMO HEAVY INDUSTRIES, LTD.: COMPANY SNAPSHOT

- FIGURE 94 CHANTIERS DE L'ATLANTIQUE: COMPANY SNAPSHOT

- FIGURE 95 SEATRIUM: COMPANY SNAPSHOT

- FIGURE 96 MAZAGON DOCK SHIPBUILDERS LIMITED: COMPANY SNAPSHOT

- FIGURE 97 COCHIN SHIPYARD LIMITED: COMPANY SNAPSHOT

- FIGURE 98 AUSTAL: COMPANY SNAPSHOT

- FIGURE 99 THYSSENKRUPP AG: COMPANY SNAPSHOT

- FIGURE 100 HARLAND & WOLFF: COMPANY SNAPSHOT

- FIGURE 101 YANGZIJIANG SHIPBUILDING: COMPANY SNAPSHOT

- FIGURE 102 KAWASAKI HEAVY INDUSTRIES, LTD.: COMPANY SNAPSHOT

The marine vessels market is projected to reach USD 133.63 billion by 2030, from USD 111.10 billion in 2024, at a CAGR of 3.1%. The marine vessels market is influenced by several key factors. Global trade is increasing the demand for different types of ships. Military navy growth is also helping the market expand. The need for larger and more versatile vessels comes from the demand for efficient transportation of goods worldwide. Rising passenger and tourism needs are driving fleet expansion and technology upgrades. Many cruise lines are adding more ships to serve the growing number of travelers looking for unique experiences. Strategic fleet renewal is important for market improvement. New, fuel-efficient vessels help meet environmental standards and lower costs. The shift toward sustainable shipping practices is becoming more important to follow international rules that reduce emissions. High costs and strict safety regulations may slow growth in the sector. New companies face challenges created by these factors. Established companies must pursue continuous innovation to remain relevant. They need to make investments in research and development to stay competitive and meet changing market demands. Therefore, industry players and governments must foster collaboration. This cooperation will encourage growth and help establish sustainable maritime practices.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2023 |

| Forecast Period | 2024-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Ship Type, Tonnage, Operation and Region |

| Regions covered | North America, Europe, APAC, RoW |

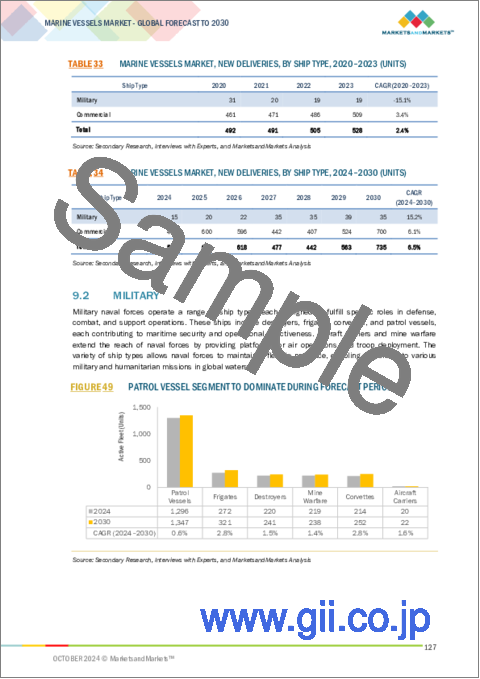

"Based on commercial ship type, cargo vessels segment forecasted to grow at highest CAGR during the forecast period"

Cargo vessels are becoming the most important part of commercial shipping. These vessels play a key role in global trade by transporting various goods across the seas. This group includes different types of ships. Container ships carry packaged products. Bulk carriers transport raw materials. Tankers carry liquids, dry cargo ships transport various products, and barges move goods in shallow waters. These vessels ensure that products flow smoothly across oceans. They support global supply chains and guarantee that goods reach markets worldwide. As the demand for faster and more reliable shipping grows, the industry adopts new technologies. Modern navigation systems, automation, and eco-friendly fuels improve efficiency, enhance safety, and reduce environmental impact. Investors put money into digital tracking systems and predictive maintenance to help these ships operate more effectively. This approach reduces downtime and increases accuracy. As global trade continues to expand, cargo vessels remain essential for international commerce and economic growth, connecting communities around the world.

"Based on military ship type, the patrol vessels segment is estimated to capture the largest share in the market during the forecast period"

Patrol vessels are the largest segment in military ship types because they are crucial for border protection and maritime security. These smaller, efficient ships are designed for long patrols and surveillance to protect territorial waters. They play an important role in restricting illegal activities like smuggling and piracy, and they also take part in search and rescue operations. Patrol vessels are more cost-effective to operate than larger naval ships. They serve as an efficient solution for maintaining law and order in coastal areas. As nations place greater emphasis on effective maritime security and budget management, patrol vessels are increasingly recognized as vital assets in today's naval fleets.

" The Europe region is forecasted to grow at the highest CAGR during the forecast period"

Europe is the fastest-growing area in the marine vessels market. This growth comes from various shipbuilding activities in the UK, Germany, France, and Italy. European shipyards play an important role globally and are receiving more new orders, especially for cruise ships and dry cargo vessels. The popularity of dry cargo is derived from its shorter delivery times, which are met by high demand in the region. Advanced technologies and sustainable practices are also focused on by European shipyards. Eco-friendly fuels and efficient designs are used to comply with strict environmental rules. Europe's shipbuilding industry includes both large shipyards and smaller, specialized facilities that focus on niche vessels like offshore wind support ships and river cruise vessels. These factors allow Europe to strengthen its influence in the global maritime industry, solidifying its reputation for quality, innovation, and adaptability..

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the marine vessels marketplace.

- By Company Type: Tier 1 - 49%, Tier 2 - 37%, and Tier 3 -14%

- By Designation: C-level Executive -55%, Managers -27%, and Others - 18%

- By Region: North America- 32%, Europe - 32%, Asia Pacific- 16%, Middle East -10% and Rest of the World - 10%

China State Shipbuilding Corporation (China), FINCANTIERI S.p.A. (Italy), Huntington Ingalls Industries (US), HD Hyundai Heavy Industries Co., Ltd. (South Korea), Hanwha Ocean Co., Ltd. (South Korea), Samsung Heavy Industries Co., Ltd (South Korea), MITSUBISHI HEAVY INDUSTRIES, LTD. (Japan), Naval Group (France), Austal (Australia), and Mazagon Dock Shipbuilders Limited (India) are some of the leading players operating in the marine vessels market.

Research Coverage

This research report categorizes the marine vessels market by ship type (Commercial (Passenger Vessels, Cargo Vessels, and Others), and Military (Aircraft Carriers, Destroyer, Frigate, Corvette, Patrol Vessels, and Mine Warfare)) by Tonnage (100 - 500 DWT, 500-5,000 DWT, 5,000-15,000 DWT, and >15,000 DWT), by Operation (Inland, and Seafaring), and by Region (North America, Europe, Asia Pacific, Middle East, and Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the marine vessels market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products, and services; key strategies; Contracts, partnerships, agreements, new product launches, and recent developments associated with the marine vessels market. Competitive analysis of upcoming startups in the marine vessels market ecosystem is covered in this report.

Key benefits of buying this report: This report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall marine vessels market and its subsegments. The report covers the entire ecosystem of the marine vessels market. It will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key Drivers (expanding global trade, military navy expansion and modernization, a surge in passenger and tourism demand, and strategic fleet renewal), restrains (High capital cost, stringent regulatory and safety standards), opportunities (Increasing focus on sustainability, technology advancement in propulsion systems, and the transition of trading and logistics companies' preference from traditional shipping to environmentally sustainable shipping) and challenges (Tackling aging fleet management, and supply chain disruptions in marine industry) influencing the growth of the market.

- Product Development/Innovation: Detailed Insights on upcoming technologies, R&D activities, and new products/solutions launched in the market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the marine vessels market across varied regions

- Market Diversification: Exhaustive information about new solutions, recent developments, and investments in the marine vessels market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players including China State Shipbuilding Corporation (China), FINCANTIERI S.p.A. (Italy), Huntington Ingalls Industries (US), HD Hyundai Heavy Industries Co., Ltd. (South Korea), and Hanwha Ocean Co., Ltd. (South Korea) among others in the marine vessels market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 INCLUSIONS AND EXCLUSIONS

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary sources

- 2.1.2.2 Key data from primary sources

- 2.1.1 SECONDARY DATA

- 2.2 FACTOR ANALYSIS

- 2.2.1 INTRODUCTION

- 2.2.2 DEMAND-SIDE INDICATORS

- 2.2.3 SUPPLY-SIDE INDICATORS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Market size estimation and methodology

- 2.3.2 TOP-DOWN APPROACH

- 2.3.1 BOTTOM-UP APPROACH

- 2.4 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MARINE VESSELS MARKET

- 4.2 MARINE VESSELS MARKET, BY SHIP TYPE

- 4.3 MARINE VESSELS MARKET, BY MILITARY SHIP TYPE

- 4.4 MARINE VESSELS MARKET, BY COMMERCIAL SHIP TYPE

- 4.5 MARINE VESSELS MARKET, BY TONNAGE

- 4.6 MARINE VESSELS MARKET, BY OPERATION

- 4.7 MARINE VESSELS MARKET, ACTIVE FLEET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Expanding global trade: Catalyst for marine vessel demand

- 5.2.1.2 Military navy expansion and modernization

- 5.2.1.3 Passenger and tourism demand surge, which accelerated growth of marine vessels market

- 5.2.1.4 Strategic fleet renewal

- 5.2.2 RESTRAINTS

- 5.2.2.1 High capital cost

- 5.2.2.2 Stringent regulatory and safety standards

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing focus on sustainability

- 5.2.3.2 Technology advancement in propulsion system

- 5.2.3.3 Transition of trading and logistics companies' preference from traditional shipping to environmentally sustainable shipping

- 5.2.4 CHALLENGES

- 5.2.4.1 Tackling aging fleet management

- 5.2.4.2 Supply chain disruptions in marine industry

- 5.2.1 DRIVERS

- 5.3 OPERATIONAL DATA

- 5.4 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.5 ECOSYSTEM MAPPING

- 5.5.1 PROMINENT COMPANIES

- 5.5.2 PRIVATE AND SMALL ENTERPRISES

- 5.5.3 END USERS

- 5.6 VALUE CHAIN ANALYSIS

- 5.7 PRICING ANALYSIS

- 5.7.1 INDICATIVE PRICING ANALYSIS, BY COMMERCIAL SHIP TYPE

- 5.7.2 INDICATIVE PRICING ANALYSIS, BY MILITARY SHIP TYPE

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 HYUNDAI HEAVY INDUSTRIES - DIGITAL SHIPYARD TRANSFORMATION

- 5.8.2 FINCANTIERI - ENERGY TRANSITION AND SUSTAINABILITY

- 5.8.3 MITSUBISHI HEAVY INDUSTRIES - TURBOCHARGER PRODUCTION EFFICIENCY

- 5.8.4 IMPROVING NAVY SHIPBUILDING EFFICIENCY: ADOPTING BEST PRACTICES

- 5.8.5 REVOLUTIONIZING FERRY DESIGN WITH MIXED REALITY SOLUTIONS

- 5.9 TRADE ANALYSIS

- 5.10 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.11 TARIFF AND REGULATORY LANDSCAPE

- 5.11.1 TARIFF DATA

- 5.11.2 REGULATORY LANDSCAPE

- 5.11.2.1 Regulatory bodies, government agencies, and other organizations

- 5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 TECHNOLOGY ANALYSIS

- 5.13.1 KEY TECHNOLOGIES

- 5.13.1.1 3D CAD design and simulation

- 5.13.1.2 Robotic welding and automation

- 5.13.1.3 Advanced propulsion systems (LNG, hybrid)

- 5.13.2 COMPLEMENTARY TECHNOLOGIES

- 5.13.2.1 Product Lifecycle Management (PLM)

- 5.13.2.2 Condition monitoring systems

- 5.13.3 ADJACENT TECHNOLOGIES

- 5.13.3.1 Port automation and logistics systems

- 5.13.3.2 Renewable energy integration (solar, wind)

- 5.13.1 KEY TECHNOLOGIES

- 5.14 INVESTMENT AND FUNDING SCENARIO

- 5.15 TOTAL COST OF OWNERSHIP

- 5.15.1 ACQUISITION COST

- 5.15.2 OPERATING COST

- 5.15.3 DOWNTIME AND DISRUPTION COST

- 5.15.4 LIFECYCLE EXTENSION COST

- 5.15.5 END-OF-LIFE COST

- 5.15.6 RISK MANAGEMENT COST

- 5.15.7 OPPORTUNITY COST

- 5.16 BUSINESS MODELS

- 5.17 BILL OF MATERIALS

- 5.18 IMPACT OF GENERATIVE AI ON MARINE INDUSTRY

- 5.18.1 IMPACT OF AI ON MARINE SECTOR: USE CASES

- 5.18.2 IMPACT OF AI ON MARINE VESSELS MARKET

- 5.19 MACROECONOMIC OUTLOOK

- 5.19.1 INTRODUCTION

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TECHNOLOGY TRENDS

- 6.2.1 DIGITAL TWIN TECHNOLOGY

- 6.2.2 GREEN SHIPS

- 6.2.3 CONNECTED SHIPS

- 6.2.4 AUTONOMOUS MARINE VESSELS

- 6.3 TECHNOLOGY ROADMAP

- 6.4 IMPACT OF MEGATRENDS

- 6.4.1 3D PRINTING

- 6.4.2 ARTIFICIAL INTELLIGENCE

- 6.4.3 BIG DATA ANALYTICS

- 6.4.4 INTERNET OF THINGS (IOT)

- 6.5 SUPPLY CHAIN ANALYSIS

- 6.6 PATENT ANALYSIS

7 MARINE VESSELS MARKET, BY OPERATION

- 7.1 INTRODUCTION

- 7.2 INLAND

- 7.2.1 EFFICIENT TRANSPORT ACROSS REGIONAL WATERWAYS TO DRIVE SEGMENT

- 7.3 SEAFARING

- 7.3.1 ABILITY TO FACILITATE GLOBAL TRADE, DEFENSE, AND ENERGY OPERATIONS ACROSS INTERNATIONAL WATERS TO DRIVE MARKET

8 MARINE VESSELS MARKET, BY TONNAGE

- 8.1 INTRODUCTION

- 8.2 100 DWT-500 DWT

- 8.2.1 NEED FOR SMALL-SCALE MARITIME TRANSPORTATION TO DRIVE SEGMENT

- 8.3 500-5,000 DWT

- 8.3.1 SUPPLY CHAINS AND COST-EFFECTIVE CARGO MOVEMENT TO DRIVE SEGMENT

- 8.4 5,000-15,000 DWT

- 8.4.1 OPTIMIZATION OF TRADE ROUTES AND SUPPORTING ECONOMIC ACTIVITIES TO DRIVE SEGMENT

- 8.5 >15,000 DWT

- 8.5.1 TECHNOLOGICAL ADVANCEMENTS AND STRATEGIC INVESTMENTS IN MARITIME INFRASTRUCTURE TO DRIVE SEGMENT

9 MARINE VESSELS MARKET, BY SHIP TYPE

- 9.1 INTRODUCTION

- 9.2 MILITARY

- 9.2.1 AIRCRAFT CARRIER

- 9.2.1.1 Global airpower projection and strategic maritime dominance to drive segment

- 9.2.2 DESTROYER

- 9.2.2.1 Versatile defense and fleet protection to drive segment

- 9.2.3 FRIGATE

- 9.2.3.1 Agility and cost-effective maritime defense to drive segment

- 9.2.4 CORVETTE

- 9.2.4.1 Cost-effective, rapid response capabilities for coastal defense and maritime security to drive segment

- 9.2.5 PATROL VESSEL

- 9.2.5.1 Border protection capabilities to drive segment

- 9.2.6 MINE WARFARE

- 9.2.6.1 Need for safe navigation and protection of strategic waterways from naval mine threats to drive segment

- 9.2.1 AIRCRAFT CARRIER

- 9.3 COMMERCIAL

- 9.3.1 PASSENGER VESSELS

- 9.3.1.1 Yachts

- 9.3.1.1.1 Innovative design and luxury to drive segment

- 9.3.1.2 Ferries

- 9.3.1.2.1 Need for regional transport to drive segment

- 9.3.1.3 Cruise ships

- 9.3.1.3.1 Strong demand, effective financial management, and focus on innovation and sustainability to drive segment

- 9.3.1.1 Yachts

- 9.3.2 CARGO VESSELS

- 9.3.2.1 Container vessels

- 9.3.2.1.1 Adaptability in size, capacity, and efficiency to drive segment

- 9.3.2.2 Bulk carriers

- 9.3.2.2.1 Need for efficient transport of bulk goods to drive segment

- 9.3.2.3 Tanker

- 9.3.2.3.1 Need for efficient and safe movement of vital resources across international waters to drive segment

- 9.3.2.4 Dry cargo ships

- 9.3.2.4.1 Ability to transport diverse goods efficiently to drive segment

- 9.3.2.5 Barges

- 9.3.2.5.1 Cost efficiency in transporting large volumes of cargo over short to medium distances to drive segment

- 9.3.2.1 Container vessels

- 9.3.3 OTHERS

- 9.3.3.1 Fishing vessels

- 9.3.3.1.1 Critical role in food security and advanced technologies to drive segment

- 9.3.3.2 Tugs and workboats

- 9.3.3.2.1 Advanced navigation systems and eco-friendly technologies to drive segment

- 9.3.3.3 Research vessels

- 9.3.3.3.1 Advanced instrumentation and specialized capabilities to drive segment

- 9.3.3.4 Dredgers

- 9.3.3.4.1 Technological advancements and automation to drive segment

- 9.3.3.1 Fishing vessels

- 9.3.1 PASSENGER VESSELS

10 MARINE VESSELS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 PESTLE ANALYSIS

- 10.2.2 US

- 10.2.2.1 Infrastructure investments and stable naval capabilities to drive market

- 10.2.3 CANADA

- 10.2.3.1 Investments and key role in facilitating global maritime trade to drive market

- 10.3 EUROPE

- 10.3.1 PESTLE ANALYSIS

- 10.3.2 UK

- 10.3.2.1 Significant changes in fleet composition and strategic investments to drive market

- 10.3.3 GERMANY

- 10.3.3.1 Advanced shipbuilding capabilities to drive market

- 10.3.4 FRANCE

- 10.3.4.1 Modernization and new acquisitions to fuel market

- 10.3.5 ITALY

- 10.3.5.1 Robust shipbuilding capabilities to drive market

- 10.3.6 NORWAY

- 10.3.6.1 Sustainable shipping and technological advancements to drive market

- 10.3.7 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 PESTLE ANALYSIS

- 10.4.2 CHINA

- 10.4.2.1 Significant advancements in shipbuilding and increasing naval capabilities to drive market

- 10.4.3 INDIA

- 10.4.3.1 Acquisition of international contracts and expansion of naval fleet to drive market

- 10.4.4 JAPAN

- 10.4.4.1 Strategic alliances and focus on innovation to drive market

- 10.4.5 AUSTRALIA

- 10.4.5.1 Focus on modernization and capability enhancement to drive market

- 10.4.6 SOUTH KOREA

- 10.4.6.1 Presence of key shipbuilders to drive market

- 10.4.7 SINGAPORE

- 10.4.7.1 Modernization efforts and strategic acquisitions to drive market

- 10.4.8 REST OF ASIA PACIFIC

- 10.5 MIDDLE EAST

- 10.5.1 PESTLE ANALYSIS

- 10.5.2 GULF COOPERATION COUNCIL (GCC)

- 10.5.2.1 UAE

- 10.5.2.1.1 Strategic partnerships and significant legislative updates to drive market

- 10.5.2.2 Saudi Arabia

- 10.5.2.2.1 Ambitious infrastructure projects and strategic investments to drive market

- 10.5.2.1 UAE

- 10.5.3 ISRAEL

- 10.5.3.1 Investments and innovation to drive market

- 10.5.4 TURKEY

- 10.5.4.1 Need to advance shipbuilding industry to drive market

- 10.6 REST OF THE WORLD

- 10.6.1 PESTLE ANALYSIS

- 10.6.2 LATIN AMERICA

- 10.6.2.1 Brazil

- 10.6.2.1.1 Domestic operations and significant advancements in naval capabilities to drive market

- 10.6.2.2 Mexico

- 10.6.2.2.1 Strategic position to drive market

- 10.6.2.1 Brazil

- 10.6.3 AFRICA

- 10.6.3.1 South Africa

- 10.6.3.1.1 Focus on strengthening naval capabilities to drive market

- 10.6.3.1 South Africa

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2024

- 11.3 REVENUE ANALYSIS

- 11.4 MARKET SHARE ANALYSIS

- 11.5 BRAND/PRODUCT COMPARISON

- 11.6 COMPANY FINANCIAL METRICS

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.8 COMPANY FOOTPRINT: KEY PLAYERS

- 11.9 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 11.9.1 PROGRESSIVE COMPANIES

- 11.9.2 RESPONSIVE COMPANIES

- 11.9.3 DYNAMIC COMPANIES

- 11.9.4 STARTING BLOCKS

- 11.9.5 COMPETITIVE BENCHMARKING

- 11.10 COMPETITIVE SCENARIO

- 11.10.1 PRODUCT LAUNCHES

- 11.10.2 DEALS

- 11.10.3 OTHERS

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 CHINA STATE SHIPBUILDING CORPORATION

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Other developments

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 HD HYUNDAI HEAVY INDUSTRIES CO., LTD.

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Deals

- 12.1.2.3.2 Other developments

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 HANWHA OCEAN CO., LTD.

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.3.3 Other developments

- 12.1.3.4 MnM view

- 12.1.3.4.1 Right to win

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 HUNTINGTON INGALLS INDUSTRIES

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Other developments

- 12.1.4.4 MnM view

- 12.1.4.4.1 Right to win

- 12.1.4.4.2 Strategic choices

- 12.1.4.4.3 Weaknesses and competitive threats

- 12.1.5 FINCANTIERI S.P.A.

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.5.3.3 Other developments

- 12.1.5.4 MnM view

- 12.1.5.4.1 Right to win

- 12.1.5.4.2 Strategic choices

- 12.1.5.4.3 Weaknesses and competitive threats

- 12.1.6 SAMSUNG HEAVY INDUSTRIES CO., LTD

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Other developments

- 12.1.7 IMABARI SHIPBUILDING CO., LTD.

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Deals

- 12.1.7.3.2 Other developments

- 12.1.8 JAPAN MARINE UNITED CORPORATION

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches

- 12.1.8.3.2 Other developments

- 12.1.9 MITSUBISHI HEAVY INDUSTRIES, LTD.

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Deals

- 12.1.9.3.2 Other developments

- 12.1.10 SUMITOMO HEAVY INDUSTRIES, LTD.

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.11 CHANTIERS DE L'ATLANTIQUE

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.11.3 Recent developments

- 12.1.11.3.1 Deals

- 12.1.11.3.2 Other developments

- 12.1.12 MEYER WERFT GMBH & CO. KG

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.12.3 Recent developments

- 12.1.12.3.1 Deals

- 12.1.12.3.2 Other developments

- 12.1.13 DAMEN SHIPYARDS GROUP

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Product launches

- 12.1.13.3.2 Deals

- 12.1.13.3.3 Other developments

- 12.1.14 NAVANTIA

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Other developments

- 12.1.15 SEATRIUM

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.16 MAZAGON DOCK SHIPBUILDERS LIMITED

- 12.1.16.1 Business overview

- 12.1.16.2 Products offered

- 12.1.16.3 Recent developments

- 12.1.16.3.1 Other developments

- 12.1.17 COCHIN SHIPYARD LIMITED

- 12.1.17.1 Business overview

- 12.1.17.2 Products offered

- 12.1.17.3 Recent developments

- 12.1.17.3.1 Product launches

- 12.1.17.3.2 Deals

- 12.1.17.3.3 Other developments

- 12.1.18 AUSTAL

- 12.1.18.1 Business overview

- 12.1.18.2 Products offered

- 12.1.18.3 Recent developments

- 12.1.18.3.1 Deals

- 12.1.18.3.2 Other developments

- 12.1.19 NAVAL GROUP

- 12.1.19.1 Business overview

- 12.1.19.2 Products

- 12.1.19.3 Recent developments

- 12.1.19.3.1 Product launches

- 12.1.19.3.2 Other developments

- 12.1.20 THYSSENKRUPP AG

- 12.1.20.1 Business overview

- 12.1.20.2 Products offered

- 12.1.21 HARLAND & WOLFF

- 12.1.21.1 Business overview

- 12.1.21.2 Products offered

- 12.1.22 BRODOSPLIT JSC

- 12.1.22.1 Business overview

- 12.1.22.2 Products offered

- 12.1.22.3 Recent developments

- 12.1.22.3.1 Product launches

- 12.1.22.3.2 Other developments

- 12.1.23 COSCO SHIPPING HEAVY INDUSTRY CO., LTD.

- 12.1.23.1 Business overview

- 12.1.23.2 Products offered

- 12.1.23.2.1 Other developments

- 12.1.24 YANGZIJIANG SHIPBUILDING

- 12.1.24.1 Business overview

- 12.1.24.2 Products offered

- 12.1.24.3 Recent developments

- 12.1.24.3.1 Other Developments

- 12.1.25 KAWASAKI HEAVY INDUSTRIES, LTD.

- 12.1.25.1 Business overview

- 12.1.25.2 Products offered

- 12.1.25.3 Recent developments

- 12.1.25.3.1 Other developments

- 12.1.1 CHINA STATE SHIPBUILDING CORPORATION

- 12.2 OTHER PLAYERS

- 12.2.1 SILENT YACHTS

- 12.2.2 CANDELA

- 12.2.3 X SHORE

- 12.2.4 MASTER BOAT BUILDERS, INC.

- 12.2.5 VELA

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 ANNEXURE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 CUSTOMIZATION OPTIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS