|

|

市場調査レポート

商品コード

1419622

ボトルウォーター加工の世界市場 (~2028年):製品タイプ (スティルウォーター・スパークリングウォーター)・包装材料・技術 (イオン交換&脱塩・消毒・ろ過・包装)・機器・地域別Bottled Water Processing Market by Product Type (Still Water and Sparkling Water), Packaging Material, Technology (Ion Exchange & Demineralization, Disinfection, Filtration, and Packaging), Equipment and Region - Global Forecast to 2028 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ボトルウォーター加工の世界市場 (~2028年):製品タイプ (スティルウォーター・スパークリングウォーター)・包装材料・技術 (イオン交換&脱塩・消毒・ろ過・包装)・機器・地域別 |

|

出版日: 2024年01月25日

発行: MarketsandMarkets

ページ情報: 英文 322 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

レポート概要

| 調査範囲 | |

|---|---|

| 調査対象年 | 2023-2028年 |

| 基準年 | 2022年 |

| 予測期間 | 2023-2028年 |

| 単位 | 金額 (米ドル)・数量 (ガロン) |

| セグメント | 製品タイプ・包装材料・技術・機器・地域別 |

| 対象地域 | 北米・南米・欧州・アジア太平洋・その他の地域 |

ボトルウォーター加工市場は、ボトルウォーター市場とボトルウォーター機器市場で構成されます。

ボトルウォーターの市場規模は、2023年の3,111億米ドルから、予測期間中は8.0%のCAGRで推移し、2028年には4,571億米ドルに達すると予測されています。また、ボトルウォーター機器の市場規模は、2023年の72億米ドルから、予測期間中は5.7%のCAGRで推移し、2028年には95億米ドルに達すると予測されています。

ボトルウォーター加工の市場は、新興国では水質問題への対処から活況であり、世界的には人口の増加と都市化に伴う清潔な飲料水需要の高まりに応えています。

予測期間中、アジア太平洋地域が最も高い成長率を示すと予測されています。同地域では、中国、インドネシア、インドが支配的な力として浮上し、業界の成長の舵取りをしています。急増する人口、急速な都市化、進化する消費者の嗜好に後押しされ、これらの国々はボトルウォーター加工の成長を形成する重要なプレーヤーとなっています。巨大な人口を抱え、都市化が進む中国は、ボトルウォーター加工市場の主要な牽引役となっています。都市のライフスタイルが進化し、健康意識が高まるにつれて、中国の消費者はパッケージ化された浄水を好み、先進加工技術の需要を後押ししています。

製品タイプ別では、スパークリングウォーターが世界で急速に人気を集めており、最も高い成長率が予測されます。炭酸水や発泡水としても知られるスパークリングウォーターは、嗜好の変化やより健康的な飲料オプションへの注目の高まりに後押しされ、業界内で独自の位置付けを切り開いています。

包装材料別では、プラスチック製が市場を支配しています。プラスチックは、利便性を高めると同時に環境への配慮の対象でもあります。その耐久性、軽量性、手頃な価格から広く採用され、ペットボトルは業界でどこにでもあるものとなっています。持ち運びの利便性と製品の安全性を確保できることが、プラスチック包装の人気に貢献しています。

技術別では、ろ過部門が市場でもっとも高い成長率を示すと予想されています。濾過技術は、最終製品の品質と純度を確保する上で極めて重要な役割を果たしています。消費者が清潔で安全な飲料水へのアクセスをますます優先する中で、ろ過は製造プロセスにおいて重要な要素となっています。

当レポートでは、世界のボトルウォーター加工の市場を調査し、市場概要、市場影響因子および市場機会の分析、技術・特許の動向、法規制環境、ケーススタディ、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- マクロ経済指標

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

第6章 業界の動向

- 顧客のビジネスに影響を与える動向

- バリューチェーン分析

- 技術分析

- 特許分析

- エコシステムマッピング

- サプライチェーン分析

- ポーターのファイブフォース分析

- 貿易分析

- 価格分析

- ケーススタディ分析

- 規制機関、政府機関、その他の組織

- 主なステークホルダーと購入基準

- 主な会議とイベント

第7章 ボトルウォーター市場:製品タイプ別

- スティルウォーター

- ノンフレーバー

- フレーバー

- スパークリングウォーター

- ノンフレーバー

- フレーバー

第8章 ボトルウォーター市場:包装材別

- プラスチック

- ガラス

- 缶

- その他

第9章 ボトルウォーター機器市場:機器別

- フィルター

- ボトル洗浄機

- フィラー・キャッパー

- ブロー成形機

- シュリンクラッパー

- その他

第10章 ボトルウォーター機器市場:技術別

- イオン交換・脱塩

- イオン交換 (IX)

- 逆浸透 (RO)・電気透析

- 消毒

- 塩素化

- 紫外線

- オゾン化

- ろ過

- 膜ろ過

- その他

- 梱包

第11章 ボトルウォーター加工市場:地域別

- 北米

- 欧州

- アジア太平洋

- 南米

- その他の地域

第12章 競合情勢

- 概要

- 主要企業の戦略

- 収益分析

- 年間収益 vs 成長 (主要企業)

- 主要企業のEBITDA分析:主要地域別

- 市場シェア分析

- 主要参入企業のスナップショット

- 企業評価マトリックス

- 競合シナリオ

第13章 企業プロファイル

- ボトルウォーター加工市場:主要企業

- DUPONT

- GEA GROUP AKTIENGESELLSCHAFT

- ALFA LAVAL

- 3M

- VEOLIA

- SPX FLOW, INC.

- PALL CORPORATION

- PENTAIR

- PORVAIR FILTRATION GROUP

- TORAY INDUSTRIES, INC.

- ボトルウォーター市場:主要企業

- NESTLE

- THE COCA-COLA COMPANY

- PEPSICO

- DANONE

- NONGFU SPRING

- TATA CONSUMER PRODUCTS LIMITED

- NATIONAL BEVERAGE CORP.

- KEURIG DR PEPPER, INC.

- GEROLSTEINER BRUNNEN GMBH & CO. KG

- CG ROXANE, LLC

- ボトルウォーター市場:その他の企業

- FERRARELLE

- VOSS OF NORWAY AS

- WATERLOO SPARKLING WATER CORP.

- CRYSTAL MINERAL WATER

- SANPELLEGRINO

第14章 隣接市場・関連市場

第15章 付録

Report Description

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD Million), Volume (Million Gallon) |

| Segments | By Product Type, By Packaging Material, By Technology, By Equipment, and By Region |

| Regions covered | North America, South America, Europe, Asia Pacific, and Rest of the World |

The bottled water processing market comprises the bottled water market and the bottled water equipment market. The bottled water market is projected to reach USD 457.1 billion by 2028 from USD 311.1 billion by 2023, at a CAGR of 8.0% during the forecast period in terms of value. And, the bottled water equipment market is projected to reach USD 9.5 billion by 2028 from USD 7.2 billion by 2023, at a CAGR of 5.7% during the forecast period in terms of value.

The bottled water processing market thrives in emerging economies by addressing water quality challenges and, globally, responds to the escalating demand for clean drinking water amid population growth and urbanization.

The bottled water processing market's significance in emerging economies lies in its ability to address issues of water quality and accessibility, offering a reliable source of clean drinking water. In these markets, where traditional water sources may be unreliable or contaminated, the processing of bottled water becomes a vital solution, catering to the rising consumer demand for safe and convenient hydration options. Moreover, the market's role expands globally as population growth strains existing water resources and infrastructure. The demand for bottled water processing technologies and products becomes a strategic response to the challenges posed by increased urbanization and a growing population, ensuring a consistent supply of clean and safe drinking water. As regulatory standards and consumer preferences evolve, the bottled water processing industry plays a pivotal role in meeting the dynamic demands of a changing global landscape, emphasizing the importance of innovation and sustainability in ensuring water quality and accessibility worldwide.

Asia Pacific is projected to witness the highest growth rate during the forecast period.

The Asia Pacific region, particularly China, Indonesia, and India, emerges as a dominant force, steering the industry's growth. Fueled by burgeoning populations, rapid urbanization, and evolving consumer preferences, these countries have become key players in shaping the trajectory of bottled water processing. China, with its colossal population and increasing urbanization, stands as a major driver for the bottled water processing market. As urban lifestyles evolve and health consciousness rises, Chinese consumers are gravitating towards packaged and purified water options, propelling the demand for advanced processing technologies.

In Indonesia, a nation characterized by its archipelagic geography and diverse demographics, the demand for bottled water processing is driven by factors such as a growing middle class, changing lifestyles, and concerns about the quality of tap water. The market in Indonesia reflects a blend of urban and rural demands, creating a diverse landscape for bottled water processing companies to navigate.

India, with its vast and varied population, is witnessing a surge in the demand for bottled water as access to safe drinking water remains a concern in many regions. The bottled water processing market in India is buoyed by a mix of urbanization, increased disposable income, and a heightened focus on health and hygiene

Sparkling Water is gaining rapid popularity in the bottled water market across the globe and is forecasted to have the highest growth rate.

The global bottled water market has witnessed a dynamic shift in consumer preferences, with a notable surge in the popularity of sparkling water. Sparkling water, also known as carbonated or fizzy water, has carved a distinctive niche within the industry, driven by changing tastes and an increasing focus on healthier beverage options.

Consumers seeking a refreshing and flavorful alternative to traditional still water have fueled the demand for sparkling water. The effervescence and subtle bubbles in sparkling water provide a unique sensory experience, making it an appealing choice for those looking to break away from mundane hydration routines. This trend aligns with the broader movement towards healthier beverage choices, as sparkling water offers a crisp and satisfying option without the added sugars and calories often found in carbonated sodas.

By Packaging Material, plastic form dominated the market for bottled water in value terms

Plastic, as a predominant packaging material in the bottled water market, has been both a facilitator of convenience and a subject of environmental concern. Widely adopted for its durability, lightweight nature, and affordability, plastic bottles have become ubiquitous in the industry. The convenience of portability and the ability to ensure product safety have contributed to the popularity of plastic packaging.

By technology, the filtration segment is expected to have the highest growth rate in the global bottled water equipment market

Filtration technology stands at the forefront of advancements in the bottled water equipment market, playing a pivotal role in ensuring the quality and purity of the final product. As consumers increasingly prioritize access to clean and safe drinking water, filtration has become a critical component in the production process.

Modern filtration technologies deployed in bottled water equipment encompass a spectrum of techniques, including reverse osmosis, activated carbon filtration, and microfiltration. Reverse osmosis, for instance, utilizes semipermeable membranes to remove impurities and contaminants, ensuring a high level of water purity. Activated carbon filtration is effective in eliminating odors and improving taste by adsorbing organic compounds, chlorine, and other undesirable elements. Microfiltration involves the use of microscopic pores to separate particles and bacteria, providing an additional layer of protection. The adoption of advanced filtration technologies not only ensures the removal of impurities but also contributes to enhancing the overall taste and clarity of bottled water. This technological evolution aligns with consumer expectations for premium-quality water products.

The break-up of the profile of primary participants in the bottled water processing market:

- By Value Chain Side: Manufacturers: 85%, and Suppliers: 15%

- By Designation: CXO's - 34%, Managers- 44%, and Executives- 22%

- By Region: North America - 60%, Europe - 18%, Asia Pacific - 10%, South America: 8% and Middle East - 4%

Research Coverage:

This research report categorizes the bottled water processing market by product type (still water, sparkling water), packing material (plastics, glass, cans, and other packing materials), technology (ion exchange and demineralization, disinfection, filtration, and packaging), equipment (filters, fillers & cappers, molders, shrink wrappers, bottle washers, and other equipment), and region (North America, Europe, Asia Pacific, South America and Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the bottled water processing market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products, and services; key strategies; contracts, partnerships, and agreements. New product & service launches, mergers and acquisitions, and recent developments associated with the bottled water processing market. Competitive analysis of upcoming startups in the bottled water processing market ecosystem is covered in this report.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall bottled water processing market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Increasing Water Scarcity and sustainability policies concerning the environment), restraints (Scarcity of energy increases operational cost for the bottled water processing industry), opportunities (Growth opportunities in the Asian market), and challenges (High capital investment for bottled water equipment) influencing the growth of the bottled water processing market.

- Product Development/Innovation: Detailed insights on research & development activities, and new product & service launches in the bottled water processing market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the bottled water processing market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the bottled water processing market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players including DuPont (US), GEA Group Aktiengesellschaft (Germany), Alfa Laval (Sweden), Nestle (Switzerland), The Coca-Cola Company (US), PepsiCo (US), Danone (France) among others in the bottled water processing market strategies.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 BOTTLED WATER PROCESSING MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- FIGURE 2 REGIONAL SEGMENTATION

- 1.3.3 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.5.1 VALUE/CURRENCY UNITS

- TABLE 1 USD EXCHANGE RATES, 2019-2022

- 1.5.2 VOLUME UNITS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

- 1.7.1 RECESSION IMPACT ANALYSIS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 3 BOTTLED WATER PROCESSING MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primaries

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 5 BOTTLED WATER PROCESSING MARKET SIZE ESTIMATION: SUPPLY-SIDE ANALYSIS (TOP-DOWN APPROACH)

- FIGURE 6 BOTTLED WATER PROCESSING MARKET SIZE ESTIMATION: DEMAND-SIDE ANALYSIS

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.3 DATA TRIANGULATION

- FIGURE 8 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS & LIMITATIONS

- 2.4.1 ASSUMPTIONS

- 2.4.2 LIMITATIONS

- 2.5 RECESSION IMPACT ANALYSIS

3 EXECUTIVE SUMMARY

- FIGURE 9 STILL WATER SEGMENT TO DOMINATE OVER SPARKLING IN BOTTLED WATER MARKET THROUGH 2028

- FIGURE 10 PLASTIC PACKAGING MATERIAL TO LEAD SIGNIFICANTLY IN BOTTLED WATER MARKET DURING FORECAST PERIOD

- FIGURE 11 ION EXCHANGE & DEMINERALIZATION TECHNOLOGY TO LEAD IN BOTTLED WATER EQUIPMENT MARKET THROUGH 2028

- FIGURE 12 FILTERS TO BE MOST ADOPTED BOTTLED WATER EQUIPMENT THROUGH 2028

- FIGURE 13 ASIA PACIFIC TO ACCOUNT FOR LARGEST REGIONAL SHARE AND HIGHEST GROWTH IN BOTTLED WATER MARKET DURING FORECAST PERIOD

- FIGURE 14 ASIA PACIFIC TO ACCOUNT FOR LARGEST REGIONAL SHARE AND GROWTH IN BOTTLED WATER EQUIPMENT MARKET AS WELL

4 PREMIUM INSIGHTS

- 4.1 BRIEF OVERVIEW OF BOTTLED WATER EQUIPMENT MARKET

- FIGURE 15 INCREASE IN NEED FOR SAFE DRINKING WATER TO PROPEL GROWTH OF BOTTLED WATER EQUIPMENT MARKET

- 4.2 BRIEF OVERVIEW OF BOTTLED WATER MARKET

- FIGURE 16 INCLINATION TOWARD HEALTH & WELLNESS AND RISE IN CONSUMER DEMAND FOR CLEAN DRINKING WATER TO FUEL MARKET FOR BOTTLED WATER

- 4.3 ASIA PACIFIC: BOTTLED WATER MARKET, BY KEY PRODUCT TYPE AND COUNTRY

- FIGURE 17 CHINA AND STILL WATER TO ACCOUNT FOR LARGEST RESPECTIVE SHARES IN ASIA PACIFIC BOTTLED WATER MARKET IN 2023

- 4.4 BOTTLED WATER MARKET, BY PACKAGING MATERIAL AND REGION

- FIGURE 18 WATER PACKAGED IN PLASTIC BOTTLES TO ACCOUNT FOR LARGEST SHARE ACROSS REGIONS IN 2023

- 4.5 BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE

- FIGURE 19 BOTTLED SPARKLING WATER MARKET SHARE, BY PRODUCT, 2023

- 4.6 BOTTLED STILL WATER MARKET, BY PRODUCT TYPE

- FIGURE 20 BOTTLED STILL WATER MARKET SHARE, BY PRODUCT, 2023

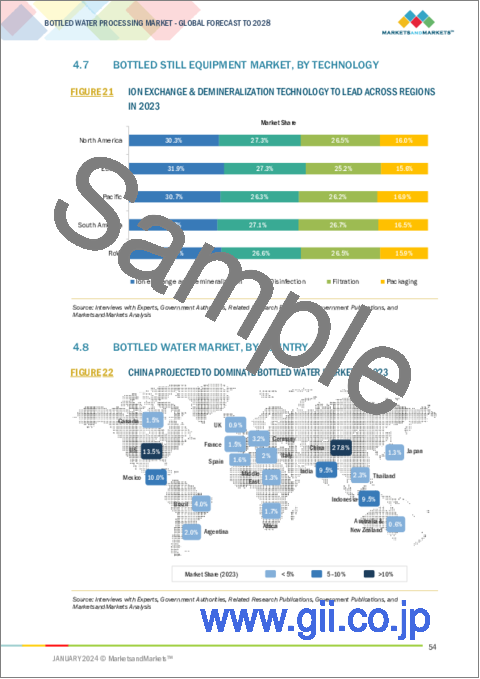

- 4.7 BOTTLED STILL EQUIPMENT MARKET, BY TECHNOLOGY

- FIGURE 21 ION EXCHANGE & DEMINERALIZATION TECHNOLOGY TO LEAD ACROSS REGIONS IN 2023

- 4.8 BOTTLED WATER MARKET, BY COUNTRY

- FIGURE 22 CHINA PROJECTED TO DOMINATE BOTTLED WATER MARKET IN 2023

- 4.9 BOTTLED WATER PROCESSING EQUIPMENT MARKET, BY COUNTRY

- FIGURE 23 US PROJECTED TO DOMINATE BOTTLED WATER EQUIPMENT MARKET IN 2023

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 POPULATION BOOM TO LEAD TO RISE IN DEMAND FOR BOTTLED WATER PROCESSING

- FIGURE 24 INCREASE IN POPULATION, 1950 TO 2021

- 5.3 MARKET DYNAMICS

- FIGURE 25 BOTTLED WATER PROCESSING MARKET: MARKET DYNAMICS

- 5.3.1 DRIVERS

- 5.3.1.1 Increase in water scarcity crisis and sustainability policies concerning environment

- 5.3.1.2 Premiumization and shifting in drinking habits to encourage consumption of bottled water

- 5.3.1.3 Technological innovations in bottled water equipment

- 5.3.2 RESTRAINTS

- 5.3.2.1 High capital costs, including raw material, distribution, and operational costs

- 5.3.2.2 Presence of ultrashort-chain PFAS in bottled water

- 5.3.3 OPPORTUNITIES

- 5.3.3.1 Growth opportunities in Asian market

- 5.3.3.2 Spike in demand for desalinated water

- TABLE 2 TOP TEN LARGEST DESALINATION PLANTS

- 5.3.3.3 Government funds for SMEs

- 5.3.3.4 After-sales services for equipment to enhance operational efficiencies

- 5.3.3.5 Public drinking water system failures to create lucrative business opportunities for bottled water manufacturers

- 5.3.4 CHALLENGES

- 5.3.4.1 High capital investment for bottled water equipment

- 5.3.4.2 Rise in concerns regarding transparency and sustainability of plastic bottles

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TRENDS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 26 TRENDS IMPACTING CUSTOMERS' BUSINESSES

- 6.3 VALUE CHAIN ANALYSIS

- 6.3.1 RAW MATERIAL SOURCING

- 6.3.2 WATER TREATMENT & PROCESSING

- 6.3.3 QUALITY & SAFETY

- 6.3.4 PACKAGING

- 6.3.5 MARKETING & SALES

- 6.3.6 END USERS

- FIGURE 27 VALUE CHAIN ANALYSIS OF BOTTLED WATER PROCESSING MARKET

- 6.4 TECHNOLOGY ANALYSIS

- 6.4.1 UVC-LEDS

- 6.4.2 IOT

- 6.5 PATENT ANALYSIS

- FIGURE 28 NUMBER OF PATENTS GRANTED FOR BOTTLED WATER PROCESSING IN GLOBAL MARKET, 2013-2023

- TABLE 3 PATENTS PERTAINING TO BOTTLED WATER PROCESSING MARKET, 2020-2023

- 6.6 ECOSYSTEM MAPPING

- FIGURE 29 ECOSYSTEM MAPPING

- TABLE 4 ECOSYSTEM ANALYSIS

- 6.7 SUPPLY CHAIN ANALYSIS

- FIGURE 30 BOTTLED WATER PROCESSING MARKET: SUPPLY CHAIN

- 6.8 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 31 PORTER'S FIVE FORCES ANALYSIS

- TABLE 5 PORTER'S FIVE FORCES ANALYSIS

- 6.8.1 THREAT OF NEW ENTRANTS

- 6.8.2 THREAT OF SUBSTITUTES

- 6.8.3 BARGAINING POWER OF SUPPLIERS

- 6.8.4 BARGAINING POWER OF BUYERS

- 6.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.9 TRADE ANALYSIS

- 6.9.1 TRADE DATA: BOTTLED WATER PROCESSING MARKET

- TABLE 6 TOP 10 IMPORTERS AND EXPORTERS OF BOTTLED WATER, 2020 (LITER)

- TABLE 7 TOP 10 IMPORTERS AND EXPORTERS OF BOTTLED WATER, 2021 (LITER)

- TABLE 8 TOP 10 IMPORTERS AND EXPORTERS OF BOTTLED WATER, 2022 (LITER)

- 6.10 PRICING ANALYSIS

- 6.10.1 AVERAGE SELLING PRICE TREND, BY PRODUCT TYPE

- TABLE 9 AVERAGE SELLING PRICE TREND FOR BOTTLED WATER, BY PRODUCT TYPE, 2019-2023 (USD/GALLON)

- 6.10.2 AVERAGE SELLING PRICE TREND, BY REGION

- TABLE 10 AVERAGE SELLING PRICE TREND FOR BOTTLED WATER, BY REGION, 2019-2023 (USD/GALLON)

- 6.11 CASE STUDY ANALYSIS

- 6.11.1 GLOBAL FILTER ENSURED STANDARDIZED FILTRATION PROCESS AT EVERY LOCATION OF ABC BOTTLERS

- 6.11.2 TATA WATER MISSION WAS LAUNCHED TO ADDRESS CRITICAL WATER AND SANITATION CHALLENGES IN INDIA

- 6.12 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.12.1 NORTH AMERICA

- 6.12.1.1 US

- 6.12.1.1.1 Regulatory Authority and Scope

- 6.12.1.1.2 Specific Regulations

- 6.12.1.1.3 Current Good Manufacturing Practice (CGMP)

- 6.12.1.1.4 Labeling Regulations

- 6.12.1.1.5 Inspections and Sampling

- 6.12.1.1.6 Sampling and Testing

- 6.12.1.1.7 Enforcement and Adulteration

- 6.12.1.1.8 State and Local Regulations

- 6.12.1.1.9 Developing New Regulations

- 6.12.1.1.10 Recent Regulatory Activities

- 6.12.1.2 Canada

- 6.12.1.2.1 Legislative Framework

- 6.12.1.2.2 Common Names and Labels

- 6.12.1.2.3 Water Types and Treatments

- 6.12.1.2.4 Blending and Labeling Requirements

- 6.12.1.2.5 Legibility and List of Ingredients

- 6.12.1.2.6 Nutrition Labeling

- 6.12.1.2.7 Fortification and Specific Claims

- 6.12.1.2.8 Vignettes and Pictorial Representations

- 6.12.1.2.9 Additional Information

- 6.12.1.1 US

- 6.12.2 ASIA PACIFIC

- 6.12.2.1 India

- 6.12.2.1.1 Definitions

- 6.12.2.1.2 Characteristics Requirements

- 6.12.2.1.3 Packaging Requirements

- 6.12.2.1.4 Labeling Requirements

- 6.12.2.1.5 Specific Labeling Requirements

- 6.12.2.1.6 Specific Restrictions on Labels

- 6.12.2.1.7 BIS License Categories

- 6.12.2.1 India

- 6.12.3 EUROPE

- 6.12.3.1 European Union (EU)

- 6.12.4 INTERNATIONAL ORGANIZATIONS

- 6.12.4.1 Codex Alimentarius Commission

- 6.12.4.2 International Organization for Standardization (ISO)

- 6.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 32 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR BOTTLED WATER EQUIPMENT MARKET

- TABLE 16 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR BOTTLED WATER EQUIPMENT MARKET

- FIGURE 33 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR BOTTLED WATER MARKET

- TABLE 17 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR BOTTLED WATER MARKET

- 6.13.2 BUYING CRITERIA

- TABLE 18 KEY BUYING CRITERIA FOR EQUIPMENT IN BOTTLED WATER EQUIPMENT MARKET

- FIGURE 34 KEY BUYING CRITERIA FOR EQUIPMENT IN BOTTLED WATER EQUIPMENT MARKET

- TABLE 19 KEY BUYING CRITERIA FOR PRODUCT TYPES IN BOTTLED WATER MARKET

- FIGURE 35 KEY BUYING CRITERIA FOR PRODUCT TYPES IN BOTTLED WATER MARKET

- 6.14 KEY CONFERENCES & EVENTS

- TABLE 20 KEY CONFERENCES & EVENTS IN BOTTLED WATER PROCESSING MARKET, 2023-2024

7 BOTTLED WATER MARKET, BY PRODUCT TYPE

- 7.1 INTRODUCTION

- FIGURE 36 BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023 VS. 2028 (USD MILLION)

- TABLE 21 BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 22 BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 23 BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 24 BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- 7.2 STILL WATER

- TABLE 25 BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 26 BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 27 BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 28 BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 29 BOTTLED STILL WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 30 BOTTLED STILL WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 31 BOTTLED STILL WATER MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 32 BOTTLED STILL WATER MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- 7.2.1 STILL UNFLAVORED

- 7.2.1.1 Health-consciousness and demand for zero-calorie beverages to lead to larger market share

- TABLE 33 BOTTLED STILL UNFLAVORED WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 34 BOTTLED STILL UNFLAVORED WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 35 BOTTLED STILL UNFLAVORED WATER MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 36 BOTTLED STILL UNFLAVORED WATER MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- 7.2.2 STILL FLAVORED

- 7.2.2.1 Lifestyle changes and increase in demand for flavored still water

- TABLE 37 BOTTLED STILL FLAVORED WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 38 BOTTLED STILL FLAVORED WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 39 BOTTLED STILL FLAVORED WATER MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 40 BOTTLED STILL FLAVORED WATER MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

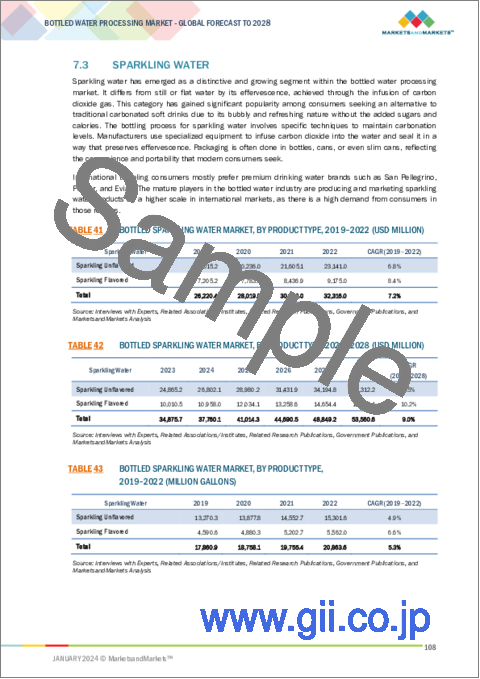

- 7.3 SPARKLING WATER

- TABLE 41 BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 42 BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 43 BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 44 BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 45 BOTTLED SPARKLING WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 46 BOTTLED SPARKLING WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 47 BOTTLED SPARKLING WATER MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 48 BOTTLED SPARKLING WATER MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- 7.3.1 SPARKLING UNFLAVORED

- 7.3.1.1 Increase in awareness regarding health benefits of unflavored sparkling water among diabetic population in mature markets

- TABLE 49 BOTTLED SPARKLING UNFLAVORED WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 50 BOTTLED SPARKLING UNFLAVORED WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 51 BOTTLED SPARKLING UNFLAVORED WATER MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 52 BOTTLED SPARKLING UNFLAVORED WATER MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- 7.3.2 SPARKLING FLAVORED

- 7.3.2.1 Flavored sparkling water segment to continue to dominate in Asia Pacific and Europe

- TABLE 53 BOTTLED SPARKLING FLAVORED WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 54 BOTTLED SPARKLING FLAVORED WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 55 BOTTLED SPARKLING FLAVORED WATER MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 56 BOTTLED SPARKLING FLAVORED WATER MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

8 BOTTLED WATER MARKET, BY PACKAGING MATERIAL

- 8.1 INTRODUCTION

- FIGURE 37 BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2023 VS. 2028 (USD MILLION)

- TABLE 57 BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2019-2022 (USD MILLION)

- TABLE 58 BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2023-2028 (USD MILLION)

- 8.2 PLASTIC

- 8.2.1 CONVENIENCE OF PLASTIC AND INCREASE IN PET BOTTLES MADE FROM BIO-BASED MATERIALS TO MINIMIZE ENVIRONMENTAL IMPACT

- TABLE 59 PLASTIC BOTTLED WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 60 PLASTIC BOTTLED WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.3 GLASS

- 8.3.1 DEVELOPMENT OF IMPROVED GLASS MATERIALS FOR PACKAGING OF BOTTLED WATER PRODUCTS

- TABLE 61 GLASS BOTTLED WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 62 GLASS BOTTLED WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.4 CANS

- 8.4.1 HIGH RECYCLING RATE OF ALUMINUM TO ENCOURAGE SUSTAINABLE SOLUTIONS

- TABLE 63 CANNED WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 64 CANNED WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.5 OTHER PACKAGING MATERIALS

- TABLE 65 OTHER BOTTLED WATER PACKAGING MATERIALS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 66 OTHER BOTTLED WATER PACKAGING MATERIALS MARKET, BY REGION, 2023-2028 (USD MILLION)

9 BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT

- 9.1 INTRODUCTION

- FIGURE 38 BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2023 VS. 2028 (USD MILLION)

- TABLE 67 BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2019-2022 (USD MILLION)

- TABLE 68 BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2023-2028 (USD MILLION)

- 9.2 FILTERS

- 9.2.1 PRESSING NEED TO ELIMINATE MICROORGANISMS FROM WATER

- TABLE 69 BOTTLED WATER FILTERS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 70 BOTTLED WATER FILTERS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3 BOTTLE WASHERS

- 9.3.1 EFFICIENT WASHING AND STERILIZING OF BOTTLES TO INCREASE SHELF LIFE OF WATER IN STORES

- TABLE 71 BOTTLE WASHERS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 72 BOTTLE WASHERS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.4 FILLERS & CAPPERS

- 9.4.1 GROWTH IN NEED FOR AUTOMATED AND INTEGRATED FILLING EQUIPMENT IN PROCESS INDUSTRIES

- TABLE 73 BOTTLED WATER FILLERS & CAPPERS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 74 BOTTLED WATER FILLERS & CAPPERS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.5 BLOW MOLDERS

- 9.5.1 ADVANCEMENTS IN STRETCH BLOW MOLDING DUE TO HIGHER CONSUMER DEMAND FOR LIGHTWEIGHT WATER BOTTLES OF DIFFERENT SIZES

- TABLE 75 BOTTLE BLOW MOLDERS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 76 BOTTLE BLOW MOLDERS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.6 SHRINK WRAPPERS

- 9.6.1 RISE IN NEED FOR FLEXIBLE PACKAGING MATERIALS

- TABLE 77 BOTTLE SHRINK WRAPPERS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 78 BOTTLE SHRINK WRAPPERS MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.7 OTHER EQUIPMENT

- TABLE 79 OTHER BOTTLED WATER EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 80 OTHER BOTTLED WATER EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

10 BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- FIGURE 39 BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023 VS. 2028 (USD MILLION)

- TABLE 81 BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 82 BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 10.2 ION EXCHANGE & DEMINERALIZATION

- TABLE 83 BOTTLED WATER ION EXCHANGE & DEMINERALIZATION EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 84 BOTTLED WATER ION EXCHANGE & DEMINERALIZATION EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.2.1 ION EXCHANGE (IX)

- 10.2.1.1 Decrease in availability of fresh water

- 10.2.2 REVERSE OSMOSIS (RO) AND ELECTRODIALYSIS

- 10.2.2.1 Growth in need for desalination to open opportunities for RO technology for bottled water

- 10.3 DISINFECTION

- TABLE 85 BOTTLED WATER DISINFECTION EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 86 BOTTLED WATER DISINFECTION EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.3.1 CHLORINATION

- 10.3.1.1 Chlorine disinfection method to be majorly adopted by small/medium water processing firms due to low cost

- 10.3.2 ULTRAVIOLET

- 10.3.2.1 Chlorine-free operation and cost-effective nature of UV technology for water processing

- 10.3.3 OZONATION

- 10.3.3.1 High capital costs of ozonation systems and not competitive with available alternatives for disinfection

- 10.4 FILTRATION

- TABLE 87 BOTTLED WATER FILTRATION EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 88 BOTTLED WATER FILTRATION EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.4.1 MEMBRANE FILTRATION

- 10.4.1.1 High investment in microfiltration and ultrafiltration technology by key players

- 10.4.2 OTHER FILTRATION TECHNOLOGIES

- 10.5 PACKAGING

- 10.5.1 EMERGING PACKAGING MATERIALS RESULT IN ADVANCEMENT OF PACKAGING TECHNOLOGY

- TABLE 89 BOTTLED WATER PACKAGING EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 90 BOTTLED WATER PACKAGING EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

11 BOTTLED WATER PROCESSING MARKET, BY REGION

- 11.1 INTRODUCTION

- TABLE 91 BOTTLED WATER MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 92 BOTTLED WATER MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 93 BOTTLED WATER MARKET, BY REGION, 2019-2022 (MILLION GALLONS)

- TABLE 94 BOTTLED WATER MARKET, BY REGION, 2023-2028 (MILLION GALLONS)

- TABLE 95 BOTTLED WATER EQUIPMENT MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 96 BOTTLED WATER EQUIPMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.2 NORTH AMERICA

- 11.2.1 NORTH AMERICA: RECESSION IMPACT ANALYSIS

- FIGURE 40 NORTH AMERICA: INFLATION RATES, BY KEY COUNTRY, 2017-2021

- FIGURE 41 NORTH AMERICA: RECESSION IMPACT ANALYSIS, 2022 VS. 2023

- FIGURE 42 NORTH AMERICA: MARKET SNAPSHOT

- TABLE 97 NORTH AMERICA: BOTTLED WATER MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 98 NORTH AMERICA: BOTTLED WATER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 99 NORTH AMERICA: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 100 NORTH AMERICA: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 101 NORTH AMERICA: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 102 NORTH AMERICA: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 103 NORTH AMERICA: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 104 NORTH AMERICA: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 105 NORTH AMERICA: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 106 NORTH AMERICA: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 107 NORTH AMERICA: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 108 NORTH AMERICA: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 109 NORTH AMERICA: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 110 NORTH AMERICA: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 111 NORTH AMERICA: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2019-2022 (USD MILLION)

- TABLE 112 NORTH AMERICA: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2023-2028 (USD MILLION)

- TABLE 113 NORTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 114 NORTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 115 NORTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2019-2022 (USD MILLION)

- TABLE 116 NORTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2023-2028 (USD MILLION)

- TABLE 117 NORTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 118 NORTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.2.2 US

- 11.2.2.1 Rise in demand for bottled water due to upgraded water treatment techniques

- TABLE 119 US: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 120 US: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.2.3 CANADA

- 11.2.3.1 Higher consumption of bottled water due to lifestyle changes

- TABLE 121 CANADA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 122 CANADA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.2.4 MEXICO

- 11.2.4.1 Increase in consumer awareness regarding high-quality and safe potable drinking water

- TABLE 123 MEXICO: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 124 MEXICO: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.3 EUROPE

- 11.3.1 EUROPE: RECESSION IMPACT ANALYSIS

- FIGURE 43 EUROPE: INFLATION RATES, BY KEY COUNTRY, 2017-2021

- FIGURE 44 EUROPE: RECESSION IMPACT ANALYSIS, 2022 VS. 2023

- TABLE 125 EUROPE: BOTTLED WATER MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 126 EUROPE: BOTTLED WATER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 127 EUROPE: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 128 EUROPE: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 129 EUROPE: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 130 EUROPE: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 131 EUROPE: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 132 EUROPE: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 133 EUROPE: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 134 EUROPE: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 135 EUROPE: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 136 EUROPE: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 137 EUROPE: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 138 EUROPE: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 139 EUROPE: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2019-2022 (USD MILLION)

- TABLE 140 EUROPE: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2023-2028 (USD MILLION)

- TABLE 141 EUROPE: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 142 EUROPE: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 143 EUROPE: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2019-2022 (USD MILLION)

- TABLE 144 EUROPE: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2023-2028 (USD MILLION)

- TABLE 145 EUROPE: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 146 EUROPE: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.3.2 GERMANY

- 11.3.2.1 Strict government regulations for treated water to drive market for bottled water equipment

- TABLE 147 GERMANY: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 148 GERMANY: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.3.3 UK

- 11.3.3.1 Rise in popularity of modern and innovative designs of sparkling bottled water equipment

- TABLE 149 UK: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 150 UK: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.3.4 FRANCE

- 11.3.4.1 Technological advancements in bottled water equipment

- TABLE 151 FRANCE: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 152 FRANCE: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.3.5 SPAIN

- 11.3.5.1 Greater consumer demand for packaged drinking water

- TABLE 153 SPAIN: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 154 SPAIN: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.3.6 ITALY

- 11.3.6.1 Rise in consumer demand for clean drinking water and increase in related investments

- TABLE 155 ITALY: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 156 ITALY: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.3.7 POLAND

- 11.3.7.1 Rise in health consciousness and changes in consumer lifestyle

- TABLE 157 POLAND: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 158 POLAND: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.3.8 REST OF EUROPE

- TABLE 159 REST OF EUROPE: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 160 REST OF EUROPE: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.4 ASIA PACIFIC

- 11.4.1 ASIA PACIFIC: RECESSION IMPACT ANALYSIS

- FIGURE 45 ASIA PACIFIC: INFLATION RATES, BY KEY COUNTRY, 2017-2021

- FIGURE 46 ASIA PACIFIC: RECESSION IMPACT ANALYSIS, 2022 VS. 2023

- FIGURE 47 ASIA PACIFIC: MARKET SNAPSHOT

- TABLE 161 ASIA PACIFIC: BOTTLED WATER MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 162 ASIA PACIFIC: BOTTLED WATER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 163 ASIA PACIFIC: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 164 ASIA PACIFIC: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 165 ASIA PACIFIC: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 166 ASIA PACIFIC: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 167 ASIA PACIFIC: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 168 ASIA PACIFIC: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 169 ASIA PACIFIC: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 170 ASIA PACIFIC: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 171 ASIA PACIFIC: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 172 ASIA PACIFIC: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 173 ASIA PACIFIC: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 174 ASIA PACIFIC: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 175 ASIA PACIFIC: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2019-2022 (USD MILLION)

- TABLE 176 ASIA PACIFIC: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2023-2028 (USD MILLION)

- TABLE 177 ASIA PACIFIC: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 178 ASIA PACIFIC: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 179 ASIA PACIFIC: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2019-2022 (USD MILLION)

- TABLE 180 ASIA PACIFIC: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2023-2028 (USD MILLION)

- TABLE 181 ASIA PACIFIC: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 182 ASIA PACIFIC: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.4.2 CHINA

- 11.4.2.1 Change in consumer preferences due to demographic shift toward aging population

- TABLE 183 CHINA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 184 CHINA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.4.3 JAPAN

- 11.4.3.1 People's preferences for quality products to drive popularity of bottled water

- TABLE 185 JAPAN: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 186 JAPAN: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.4.4 INDIA

- 11.4.4.1 Increase in contamination of drinking water and inefficient water management practices

- TABLE 187 INDIA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 188 INDIA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.4.5 INDONESIA

- 11.4.5.1 Increase in use of water for agricultural purposes

- TABLE 189 INDONESIA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 190 INDONESIA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.4.6 THAILAND

- 11.4.6.1 Highly competitive bottled water market in country to compel players to adopt strategies

- TABLE 191 THAILAND: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 192 THAILAND: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.4.7 AUSTRALIA & NEW ZEALAND

- 11.4.7.1 Increase in health-conscious population to spur consumption of bottled water products

- TABLE 193 AUSTRALIA & NEW ZEALAND: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 194 AUSTRALIA & NEW ZEALAND: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.4.8 REST OF ASIA PACIFIC

- TABLE 195 REST OF ASIA PACIFIC: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 196 REST OF ASIA PACIFIC: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.5 SOUTH AMERICA

- 11.5.1 SOUTH AMERICA: RECESSION IMPACT ANALYSIS

- FIGURE 48 SOUTH AMERICA: INFLATION RATES, BY KEY COUNTRY, 2017-2021

- FIGURE 49 SOUTH AMERICA: RECESSION IMPACT ANALYSIS, 2022 VS. 2023

- TABLE 197 SOUTH AMERICA: BOTTLED WATER MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 198 SOUTH AMERICA: BOTTLED WATER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 199 SOUTH AMERICA: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 200 SOUTH AMERICA: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 201 SOUTH AMERICA: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 202 SOUTH AMERICA: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 203 SOUTH AMERICA: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 204 SOUTH AMERICA: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 205 SOUTH AMERICA: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 206 SOUTH AMERICA: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 207 SOUTH AMERICA: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 208 SOUTH AMERICA: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 209 SOUTH AMERICA: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 210 SOUTH AMERICA: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 211 SOUTH AMERICA: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2019-2022 (USD MILLION)

- TABLE 212 SOUTH AMERICA: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2023-2028 (USD MILLION)

- TABLE 213 SOUTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 214 SOUTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 215 SOUTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2019-2022 (USD MILLION)

- TABLE 216 SOUTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2023-2028 (USD MILLION)

- TABLE 217 SOUTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 218 SOUTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.5.2 BRAZIL

- 11.5.2.1 Expansion of operations by equipment manufacturers due to rapid economic growth

- TABLE 219 BRAZIL: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 220 BRAZIL: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.5.3 ARGENTINA

- 11.5.3.1 Rapid infrastructure and industrial growth to boost market for bottled water equipment

- TABLE 221 ARGENTINA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 222 ARGENTINA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.5.4 REST OF SOUTH AMERICA

- TABLE 223 REST OF SOUTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 224 REST OF SOUTH AMERICA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.6 REST OF THE WORLD (ROW)

- 11.6.1 ROW: RECESSION IMPACT ANALYSIS

- FIGURE 50 ROW: INFLATION RATES, BY KEY COUNTRY, 2018-2021

- FIGURE 51 ROW: RECESSION IMPACT ANALYSIS, 2022 VS. 2023

- TABLE 225 ROW: BOTTLED WATER MARKET, BY COUNTRY/REGION, 2019-2022 (USD MILLION)

- TABLE 226 ROW: BOTTLED WATER MARKET, BY COUNTRY/REGION, 2023-2028 (USD MILLION)

- TABLE 227 ROW: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 228 ROW: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 229 ROW: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 230 ROW: BOTTLED WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 231 ROW: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 232 ROW: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 233 ROW: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 234 ROW: BOTTLED STILL WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 235 ROW: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (USD MILLION)

- TABLE 236 ROW: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (USD MILLION)

- TABLE 237 ROW: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2019-2022 (MILLION GALLONS)

- TABLE 238 ROW: BOTTLED SPARKLING WATER MARKET, BY PRODUCT TYPE, 2023-2028 (MILLION GALLONS)

- TABLE 239 ROW: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2019-2022 (USD MILLION)

- TABLE 240 ROW: BOTTLED WATER MARKET, BY PACKAGING MATERIAL, 2023-2028 (USD MILLION)

- TABLE 241 ROW: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY/REGION, 2019-2022 (USD MILLION)

- TABLE 242 ROW: BOTTLED WATER EQUIPMENT MARKET, BY COUNTRY/REGION, 2023-2028 (USD MILLION)

- TABLE 243 ROW: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2019-2022 (USD MILLION)

- TABLE 244 ROW: BOTTLED WATER EQUIPMENT MARKET, BY EQUIPMENT, 2023-2028 (USD MILLION)

- TABLE 245 ROW: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 246 ROW: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.6.2 SOUTH AFRICA

- 11.6.2.1 Increase in concerns regarding water safety

- TABLE 247 SOUTH AFRICA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 248 SOUTH AFRICA: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- 11.6.3 MIDDLE EAST

- 11.6.3.1 Development of environment-friendly and cost-effective desalination units

- TABLE 249 MIDDLE EAST: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2019-2022 (USD MILLION)

- TABLE 250 MIDDLE EAST: BOTTLED WATER EQUIPMENT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- TABLE 251 OVERVIEW OF STRATEGIES ADOPTED BY KEY BOTTLED WATER PROCESSING PLAYERS

- 12.3 REVENUE ANALYSIS

- FIGURE 52 TOP FIVE PLAYERS TO DOMINATE MARKET IN LAST FIVE YEARS (USD BILLION)

- 12.4 ANNUAL REVENUE VS. GROWTH (KEY PLAYERS)

- FIGURE 53 BOTTLED WATER MARKET: ANNUAL REVENUE, 2022 (USD BILLION) VS. REVENUE GROWTH, 2020-2022

- FIGURE 54 BOTTLED WATER EQUIPMENT MARKET: ANNUAL REVENUE, 2022 (USD BILLION) VS. REVENUE GROWTH, 2020-2022

- 12.5 EBITDA ANALYSIS FOR KEY PLAYERS, BY KEY REGION

- FIGURE 55 BOTTLED WATER MARKET: EBITDA ANALYSIS FOR KEY PLAYERS, BY KEY REGION, 2022 (USD BILLION)

- FIGURE 56 BOTTLED WATER EQUIPMENT MARKET: EBITDA ANALYSIS FOR KEY PLAYERS, BY KEY REGION, 2022 (USD BILLION)

- 12.6 MARKET SHARE ANALYSIS

- TABLE 252 BOTTLED WATER MARKET: DEGREE OF COMPETITION (COMPETITIVE), 2022

- 12.7 GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS

- FIGURE 57 BOTTLED WATER MARKET: GLOBAL SNAPSHOT OF KEY PARTICIPANTS, 2022

- FIGURE 58 BOTTLED WATER EQUIPMENT MARKET: GLOBAL SNAPSHOT OF KEY PARTICIPANTS, 2022

- 12.8 COMPANY EVALUATION MATRIX

- 12.8.1 STARS

- 12.8.2 EMERGING LEADERS

- 12.8.3 PERVASIVE PLAYERS

- 12.8.4 PARTICIPANTS

- FIGURE 59 BOTTLED WATER EQUIPMENT MARKET: COMPANY EVALUATION MATRIX FOR KEY PLAYERS, 2022

- FIGURE 60 BOTTLED WATER MARKET: COMPANY EVALUATION MATRIX FOR KEY PLAYERS, 2022

- 12.8.5 BOTTLED WATER MARKET: PRODUCT FOOTPRINT

- TABLE 253 BOTTLED WATER MARKET: OVERALL COMPANY FOOTPRINT

- TABLE 254 BOTTLED WATER MARKET: COMPANY PRODUCT TYPE FOOTPRINT

- TABLE 255 BOTTLED WATER MARKET: COMPANY PACKAGING MATERIAL FOOTPRINT

- TABLE 256 BOTTLED WATER MARKET: COMPANY REGIONAL FOOTPRINT

- 12.8.6 BOTTLED WATER EQUIPMENT MARKET: PRODUCT FOOTPRINT

- TABLE 257 BOTTLED WATER EQUIPMENT MARKET: OVERALL COMPANY FOOTPRINT

- TABLE 258 BOTTLED WATER EQUIPMENT MARKET: COMPANY FOOTPRINT, BY TECHNOLOGY

- TABLE 259 BOTTLED WATER EQUIPMENT MARKET: COMPANY FOOTPRINT, BY EQUIPMENT

- TABLE 260 BOTTLED WATER EQUIPMENT MARKET: COMPANY FOOTPRINT, BY REGION

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- TABLE 261 BOTTLED WATER PROCESSING MARKET: PRODUCT LAUNCHES, JANUARY 2020-FEBRUARY 2023

- 12.9.2 DEALS

- TABLE 262 BOTTLED WATER PROCESSING MARKET: DEALS, SEPTEMBER 2019-OCTOBER 2023

- 12.9.3 OTHER DEVELOPMENTS

- TABLE 263 BOTTLED WATER PROCESSING MARKET: OTHER DEVELOPMENTS, MAY 2022-AUGUST 2023

13 COMPANY PROFILES

- (Business overview, Products/Solutions/Services offered, Recent developments & MnM View)**

- 13.1 BOTTLED WATER PROCESSING MARKET: KEY PLAYERS

- 13.1.1 DUPONT

- TABLE 264 DUPONT: COMPANY OVERVIEW

- FIGURE 61 DUPONT: COMPANY SNAPSHOT

- TABLE 265 DUPONT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 266 DUPONT: PRODUCT LAUNCHES

- TABLE 267 DUPONT: DEALS

- TABLE 268 DUPONT: OTHERS

- 13.1.2 GEA GROUP AKTIENGESELLSCHAFT

- TABLE 269 GEA GROUP AKTIENGESELLSCHAFT: COMPANY OVERVIEW

- FIGURE 62 GEA GROUP AKTIENGESELLSCHAFT: COMPANY SNAPSHOT

- TABLE 270 GEA GROUP AKTIENGESELLSCHAFT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 271 GEA GROUP AKTIENGESELLSCHAFT: PRODUCT LAUNCHES

- 13.1.3 ALFA LAVAL

- TABLE 272 ALFA LAVAL: COMPANY OVERVIEW

- FIGURE 63 ALFA LAVAL: COMPANY SNAPSHOT

- TABLE 273 ALFA LAVAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.1.4 3M

- TABLE 274 3M: COMPANY OVERVIEW

- FIGURE 64 3M: COMPANY SNAPSHOT

- TABLE 275 3M: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.1.5 VEOLIA

- TABLE 276 VEOLIA: COMPANY OVERVIEW

- FIGURE 65 VEOLIA: COMPANY SNAPSHOT

- TABLE 277 VEOLIA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 278 VEOLIA: PRODUCT LAUNCHES

- TABLE 279 VEOLIA: OTHERS

- 13.1.6 SPX FLOW, INC.

- TABLE 280 SPX FLOW, INC.: COMPANY OVERVIEW

- FIGURE 66 SPX FLOW, INC.: COMPANY SNAPSHOT

- TABLE 281 SPX FLOW, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 282 SPX FLOW, INC.: PRODUCT LAUNCHES

- 13.1.7 PALL CORPORATION

- TABLE 283 PALL CORPORATION: COMPANY OVERVIEW

- FIGURE 67 PALL CORPORATION: COMPANY SNAPSHOT

- TABLE 284 PALL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 285 PALL CORPORATION: DEALS

- TABLE 286 PALL CORPORATION: OTHERS

- 13.1.8 PENTAIR

- TABLE 287 PENTAIR: COMPANY OVERVIEW

- FIGURE 68 PENTAIR: COMPANY SNAPSHOT

- TABLE 288 PENTAIR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 289 PENTAIR: DEALS

- 13.1.9 PORVAIR FILTRATION GROUP

- TABLE 290 PORVAIR FILTRATION GROUP: COMPANY OVERVIEW

- FIGURE 69 PORVAIR FILTRATION GROUP: COMPANY SNAPSHOT

- TABLE 291 PORVAIR FILTRATION GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 292 PORVAIR FILTRATION GROUP: PRODUCT LAUNCHES

- 13.1.10 TORAY INDUSTRIES, INC.

- TABLE 293 TORAY INDUSTRIES, INC.: COMPANY OVERVIEW

- FIGURE 70 TORAY INDUSTRIES, INC.: COMPANY SNAPSHOT

- TABLE 294 TORAY INDUSTRIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 295 TORAY INDUSTRIES, INC.: PRODUCT LAUNCHES

- 13.2 BOTTLED WATER MARKET: KEY PLAYERS

- 13.2.1 NESTLE

- TABLE 296 NESTLE: COMPANY OVERVIEW

- FIGURE 71 NESTLE: COMPANY SNAPSHOT

- TABLE 297 NESTLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 298 NESTLE: DEALS

- 13.2.2 THE COCA-COLA COMPANY

- TABLE 299 THE COCA-COLA COMPANY: COMPANY OVERVIEW

- FIGURE 72 THE COCA-COLA COMPANY: COMPANY SNAPSHOT

- TABLE 300 THE COCA-COLA COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 301 THE COCA-COLA COMPANY: DEALS

- TABLE 302 THE COCA-COLA COMPANY: OTHERS

- 13.2.3 PEPSICO

- TABLE 303 PEPSICO: COMPANY OVERVIEW

- FIGURE 73 PEPSICO: COMPANY SNAPSHOT

- TABLE 304 PEPSICO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 305 PEPSICO: DEALS

- 13.2.4 DANONE

- TABLE 306 DANONE: COMPANY OVERVIEW

- FIGURE 74 DANONE: COMPANY SNAPSHOT

- TABLE 307 DANONE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 308 DANONE: DEALS

- 13.2.5 NONGFU SPRING

- TABLE 309 NONGFU SPRING: COMPANY OVERVIEW

- FIGURE 75 NONGFU SPRING: COMPANY SNAPSHOT

- TABLE 310 NONGFU SPRING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 311 NONGFU SPRING: PRODUCT LAUNCHES

- 13.2.6 TATA CONSUMER PRODUCTS LIMITED

- TABLE 312 TATA CONSUMER PRODUCTS LIMITED: COMPANY OVERVIEW

- FIGURE 76 TATA CONSUMER PRODUCTS LIMITED: COMPANY SNAPSHOT

- TABLE 313 TATA CONSUMER PRODUCTS LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.2.7 NATIONAL BEVERAGE CORP.

- TABLE 314 NATIONAL BEVERAGE CORP.: COMPANY OVERVIEW

- FIGURE 77 NATIONAL BEVERAGE CORP.: COMPANY SNAPSHOT

- TABLE 315 NATIONAL BEVERAGE CORP.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.2.8 KEURIG DR PEPPER, INC.

- TABLE 316 KEURIG DR PEPPER, INC.: COMPANY OVERVIEW

- FIGURE 78 KEURIG DR PEPPER, INC.: COMPANY SNAPSHOT

- TABLE 317 KEURIG DR PEPPER, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 318 KEURIG DR PEPPER, INC.: DEALS

- 13.2.9 GEROLSTEINER BRUNNEN GMBH & CO. KG

- TABLE 319 GEROLSTEINER BRUNNEN GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 320 GEROLSTEINER BRUNNEN GMBH & CO. KG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 13.2.10 CG ROXANE, LLC

- TABLE 321 CG ROXANE, LLC: COMPANY OVERVIEW

- TABLE 322 CG ROXANE, LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 323 CG ROXANE, LLC: OTHERS

- *Details on Business overview, Products/Solutions/Services offered, Recent developments & MnM View might not be captured in case of unlisted companies.

- 13.3 BOTTLED WATER MARKET: OTHER PLAYERS

- 13.3.1 FERRARELLE

- TABLE 324 FERRARELLE: BUSINESS OVERVIEW

- 13.3.2 VOSS OF NORWAY AS

- TABLE 325 VOSS OF NORWAY AS: BUSINESS OVERVIEW

- 13.3.3 WATERLOO SPARKLING WATER CORP.

- TABLE 326 WATERLOO SPARKLING WATER CORP.: BUSINESS OVERVIEW

- 13.3.4 CRYSTAL MINERAL WATER

- TABLE 327 CRYSTAL MINERAL WATER: BUSINESS OVERVIEW

- 13.3.5 SANPELLEGRINO

- TABLE 328 SANPELLEGRINO: BUSINESS OVERVIEW

14 ADJACENT AND RELATED MARKETS

- 14.1 INTRODUCTION

- TABLE 329 ADJACENT MARKETS TO BOTTLED WATER PROCESSING

- 14.2 LIMITATIONS

- 14.3 BEVERAGE PROCESSING EQUIPMENT MARKET

- 14.3.1 MARKET DEFINITION

- 14.3.2 MARKET OVERVIEW

- TABLE 330 BEVERAGE PROCESSING EQUIPMENT MARKET, BY TYPE, 2017-2020 (USD MILLION)

- TABLE 331 BEVERAGE PROCESSING EQUIPMENT MARKET, BY TYPE, 2021-2026 (USD MILLION)

- 14.4 WATER & WASTEWATER TREATMENT EQUIPMENT MARKET

- 14.4.1 MARKET DEFINITION

- 14.4.2 MARKET OVERVIEW

- TABLE 332 WATER & WASTEWATER TREATMENT EQUIPMENT MARKET, BY PRODUCT TYPE, 2015-2022 (USD MILLION)

- 14.5 WATER FILTER MARKET

- 14.5.1 MARKET DEFINITION

- 14.5.2 MARKET OVERVIEW

- TABLE 333 WATER FILTERS MARKET, BY END-USE INDUSTRY, 2016-2023 (USD MILLION)

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 AUTHOR DETAILS