|

|

市場調査レポート

商品コード

1328576

デジタルトランスフォーメーションの世界市場 (~2030年):提供区分 (ソリューション・サービス)・技術 (クラウドコンピューティング・ビッグデータ&アナリティクス・ブロックチェーン・サイバーセキュリティ・AI)・ビジネス機能 (会計&財務・IT・人事)・産業・地域別Digital Transformation Market by Offering (Solutions & Services), Technology (Cloud Computing, Big Data & Analytics, Blockchain, Cybersecurity, AI), Business Function (Accounting & Finance, IT, HR), Vertical,& Region - Global Forecast to 2030 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| デジタルトランスフォーメーションの世界市場 (~2030年):提供区分 (ソリューション・サービス)・技術 (クラウドコンピューティング・ビッグデータ&アナリティクス・ブロックチェーン・サイバーセキュリティ・AI)・ビジネス機能 (会計&財務・IT・人事)・産業・地域別 |

|

出版日: 2023年07月21日

発行: MarketsandMarkets

ページ情報: 英文 353 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

デジタルトランスフォーメーションの市場規模は、2023年の6,955億米ドルから、予測期間中は24.1%のCAGRで推移し、2030年には3兆1,449億米ドルの規模に成長すると予測されています。

デジタルトランスフォーメーションとは技術の急速な進歩であり、AI、機械学習、クラウドコンピューティング、IoTといった技術の継続的な発展により、これらのツールを活用して業務を最適化し、顧客体験を向上させ、イノベーションを推進する企業の動きが加速しています。膨大な量のデータをリアルタイムで収集、分析、活用する能力は、企業にとって重要な資産となり、データ主導の意思決定、サービスのパーソナライズ、全体的な効率の改善を可能にしています。さらに、デジタルチャネルの普及とハイテクに精通する顧客の増加により、あらゆるタッチポイントでシームレスに統合されたデジタルエクスペリエンスに対する需要が生まれています。

技術別で見ると、AI技術の部門が最大のCAGRを示す見通しです。AI技術によるデジタルトランスフォーメーションは、カスタマーエクスペリエンスの向上とパーソナライズされたサービスに対する需要の高まりです。AIを活用したソリューションにより、企業は膨大な量のデータをリアルタイムで分析できるようになり、顧客の好みや行動に関する貴重な洞察を得ることができます。これにより、企業はニーズに合わせたプロアクティブなサービスを提供できるようになり、その結果、顧客満足度とロイヤルティが向上します。

産業別では、BFSIの部門が予測期間中最大の市場規模を示す見通しです。シームレスでパーソナライズされたデジタルエクスペリエンスに対する顧客ニーズの高まりにより、金融機関は顧客エンゲージメントの強化、プロセスの合理化、パーソナライズされた金融ソリューションの提供のために、AI、機械学習、データアナリティクスなどの技術に投資しています。規制上の要件やセキュリティ対策強化の必要性から、BFSI部門は安全な取引を確保し、機密データを保護するためにブロックチェーンやバイオメトリクスのような先進技術も採用するようになっています。

当レポートでは、世界のデジタルトランスフォーメーションの市場を調査し、市場概要、市場影響因子および市場機会の分析、技術・特許の動向、ケーススタディ、関連法規制、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合環境、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要・産業動向

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- デジタルトランスフォーメーション:進化

- エコシステム

- ケーススタディ分析

- 技術分析

- 用途別の市場分析

- サプライチェーン/バリューチェーン分析

- ポーターのファイブフォース分析

- 価格モデルの分析

- 特許分析

- 主な会議とイベント

- 関税と規制状況

- バイヤー/クライアントに影響を与える動向/ディスラプション

- 主要なステークホルダーと購入基準

- ベストプラクティス

- 提供価値:産業別

- 技術ロードマップ

- ビジネスモデル

- 成熟モデル

第6章 デジタルトランスフォーメーション市場:提供区分別

- ソリューション

- 導入モード別

- サービス

- コンサルティングサービス

- サポート・保守

- 企画・設計

- エンジニアリング・リエンジニアリングサービス

- ネットワーク・インフラ管理

- アプリケーション開発

第7章 デジタルトランスフォーメーション市場:技術別

- クラウドコンピューティング

- AI

- ビッグデータ・アナリティクス

- ブロックチェーン

- サイバーセキュリティ

- IoT

第8章 デジタルトランスフォーメーション市場:ビジネス機能別

- デジタルトランスフォーメーション:企業での使用例

- 会計・財務

- IT・オペレーション

- 人事

- マーケティング・販売

第9章 デジタルトランスフォーメーション市場:産業別

- BFSI

- 小売・Eコマース

- IT・ITES

- メディア・エンターテイメント

- 製造

- ヘルスケア・ライフサイエンス・医薬品

- エネルギー・ユーティリティ

- 政府・防衛

- 通信

- 教育

- 農業

- 自動車・輸送・物流

- その他

第10章 デジタルトランスフォーメーション市場:地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第11章 競合情勢

- 概要

- 主要企業の採用戦略

- 主要企業の収益分析

- 市場シェア分析

- 企業評価マトリックス

- スタートアップと中小企業の評価マトリックス

- 競合ベンチマーキング

- 競合シナリオ

第12章 企業プロファイル

- 主要企業

- MICROSOFT

- IBM

- SAP

- ORACLE

- SALESFORCE

- HPE

- ADOBE

- BAIDU

- HCL TECHNOLOGIES

- EY

- COGNIZANT

- ACCENTURE

- BROADCOM

- EQUINIX

- ALIBABA

- TIBCO SOFTWARE

- MARLABS

- SME・スタートアップ

- ALCOR SOLUTIONS

- SMARTSTREAM

- YASH TECHNOLOGIES

- INTERFACING

- DEMPTON CONSULTING GROUP

- KISSFLOW

- EMUDHRA

- PROCESSMAKER

- PROCESS STREET

- HAPPIEST MINDS

- SCORO

- BRILLIO

- AEXONIC TECHNOLOGIES

- CLOUD ANGLES

- MAGNETAR IT

- SCITARA

- INTRINSIC

- SOUNDFUL

第13章 付録

The digital transformation market size is to grow from USD 695.5 billion in 2023 to USD 3,144.9 billion by 2030, at a Compound Annual Growth Rate (CAGR) of 24.1% during the forecast period.

Digital transformation is the rapid advancement of technology. With the continuous development of technologies such as artificial intelligence, machine learning, cloud computing, and the Internet of Things, organizations are increasingly leveraging these tools to optimize their operations, enhance customer experiences, and drive innovation. The ability to collect, analyze, and leverage vast amounts of data in real time has become a critical asset for businesses, enabling them to make data-driven decisions, personalize offerings, and improve overall efficiency. Moreover, the widespread adoption of digital channels and the growing tech-savvy nature of customers have created a demand for seamless and integrated digital experiences across all touchpoints.

The AI technology has the highest CAGR during the forecast period.

By technology, the digital transformation market has been segmented into cloud computing, big data & analytics, blockchain, cybersecurity, AI, and IoT. The CAGR of AI technology is estimated to be the highest during the forecast period. Digital transformation with AI technology is the increasing demand for enhanced customer experiences and personalized services. AI-powered solutions enable businesses to analyze vast amounts of data in real time, allowing them to gain valuable insights into customer preferences and behavior. This empowers organizations to deliver tailored and proactive services, resulting in improved customer satisfaction and loyalty.

By offering, the Services segment has the highest CAGR during the forecast period.

By offering, the digital transformation market has been segmented into solutions and services. The CAGR of services is estimated to be the largest during the forecast period. Digital transformation services are experiencing a surge in popularity driven by several key factors. The growing demand for enhanced customer experiences and engagement has pushed organizations to adopt innovative technologies and strategies that enable personalized interactions and seamless omnichannel experiences.

By vertical, the BFSI segment has the largest market size during the forecast period.

The increasing customer demand for seamless and personalized digital experiences has led financial institutions to invest in technologies such as AI, machine learning, and data analytics to enhance customer engagement, streamline processes, and offer personalized financial solutions. The regulatory requirements and the need for enhanced security measures have pushed the BFSI sector to adopt advanced technologies like blockchain and biometrics to ensure secure transactions and protect sensitive data. Additionally, the rise of fintech startups and their disruptive business models have compelled traditional institutions to transform digitally in order to stay competitive, innovate their offerings, and collaborate with fintech players to leverage their technological expertise.

Among regions, Asia Pacific registered the highest CAGR during the forecast period.

By region, the Asia Pacific region has witnessed rapid advancements in technology, such as the proliferation of mobile devices, widespread internet connectivity, and the adoption of cloud computing. These advancements have created a strong foundation for digital transformation initiatives. Governments in the Asia Pacific region are actively promoting digital transformation to drive economic growth and enhance competitiveness. They are implementing policies, providing incentives, and investing in digital infrastructure to facilitate this transformation.

Breakdown of primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the digital transformation market.

- By Company: Tier I: 35%, Tier II: 45%, and Tier III: 20%

- By Designation: C-Level Executives: 35%, D-Level Executives: 25%, and Managers: 40%

- By Region: North America: 30%, Europe: 30%, APAC: 25%, MEA: 10%, Latin America: 5%

The report includes the study of key players offering digital transformation solutions and services. It profiles major vendors in the global digital transformation market. The major vendors in the global digital transformation market include Microsoft (US), SAP (Germany), Baidu (China), Adobe Systems (US), Alibaba (China), IBM (US), Google (US), Marlabs (US), Salesforce (US), Broadcom (US), Equinix (US), Oracle (US), Hewlett Packard Enterprise (US), HCL Technologies (India), EY (UK), Cognizant (US), Accenture (Ireland ), Tibco Software (US), Alcor Solutions (US), Smartstream (US), Yash Technologies (US), Interfacing (US), Kissflow (India), eMudhra (India), ProcessMaker (US), Process Street (US), Happiest Minds (India), Scoro (UK), Dempton Consulting Group (Canada), Brillio (US), Aexonic Technologies (India), CloudAngles (US), Magnetar IT (England), Scitara (US), Intrinsic (US), and Soundful (US).

Research Coverage

The market study covers the digital transformation market across segments. It aims at estimating the market size and the growth potential of this market across different segments, such as components, technology, deployment mode, organization size, business function, vertical, and region. It includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market for digital transformation and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights better to position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Rising adoption of big data and other related technologies, Advent of ML and digital transformation, Cost benefits of cloud-based digital transformation solutions, and Adoption and scaling of digital initiatives), restraints (Changing regional data regulations to lead to a time-consuming restructuring of predictive models, Data privacy and security concerns, Issues about privacy and security of information), opportunities (Rising internet proliferation and growing usage of connected and integrated technologies, Demand for personalized digital transformation, Increasing willingness of organizations to use digital technology ), and challenges (Integration of data from data silos, Issues related to IT modernization, Ownership and privacy of collected data) influencing the growth of the digital transformation market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the digital transformation market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the digital transformation market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in digital transformation market strategies; the report also helps stakeholders understand the pulse of the digital transformation market and provides them with information on key market drivers, restraints, challenges, and opportunities

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Microsoft (US), SAP (Germany), Baidu (China), Adobe Systems (US), Alibaba (China), IBM (US), Google (US), and Marlabs (US) among others in the digital transformation market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATES, 2020-2022

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 DIGITAL TRANSFORMATION MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- TABLE 2 LIST OF PRIMARY INTERVIEWS

- 2.1.2.1 Breakup of primary sources

- 2.1.2.2 Key industry insights

- 2.2 DATA TRIANGULATION

- FIGURE 2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- FIGURE 3 DIGITAL TRANSFORMATION MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY-APPROACH 1 (SUPPLY SIDE): REVENUE OF SOLUTIONS/SERVICES OF DIGITAL TRANSFORMATION MARKET

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY-APPROACH 2 - BOTTOM-UP (SUPPLY SIDE): COLLECTIVE REVENUE OF SOLUTIONS/SERVICES OF DIGITAL TRANSFORMATION MARKET

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY-APPROACH 3, BOTTOM-UP (SUPPLY SIDE): COLLECTIVE REVENUE FROM SOFTWARE/SERVICES OF DIGITAL TRANSFORMATION MARKET

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY-APPROACH 4, BOTTOM-UP (DEMAND SIDE): SHARE OF DIGITAL TRANSFORMATION THROUGH OVERALL DIGITAL TRANSFORMATION SPENDING

- 2.4 MARKET FORECAST

- TABLE 3 FACTOR ANALYSIS

- 2.5 ASSUMPTIONS

- 2.6 LIMITATIONS

- 2.7 IMPLICATIONS OF RECESSION ON DIGITAL TRANSFORMATION MARKET

3 EXECUTIVE SUMMARY

- TABLE 4 DIGITAL TRANSFORMATION MARKET AND GROWTH RATE, 2018-2022 (USD MILLION, Y-O-Y %)

- TABLE 5 DIGITAL TRANSFORMATION MARKET AND GROWTH RATE, 2023-2030 (USD MILLION, Y-O-Y %)

- FIGURE 8 SOLUTIONS SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE IN 2023

- FIGURE 9 CONSULTING SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2023

- FIGURE 10 CLOUD COMPUTING SEGMENT TO DOMINATE MARKET IN 2023

- FIGURE 11 CLOUD SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE IN 2023

- FIGURE 12 BFSI SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2023

- FIGURE 13 MARKETING & SALES SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2023

- FIGURE 14 NORTH AMERICA TO ACCOUNT FOR LARGEST MARKET SHARE IN 2023

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DIGITAL TRANSFORMATION MARKET

- FIGURE 15 DEMAND FOR PERSONALIZED DIGITAL TRANSFORMATION TO DRIVE MARKET GROWTH DURING FORECAST PERIOD

- 4.2 OVERVIEW OF RECESSION IN GLOBAL DIGITAL TRANSFORMATION MARKET

- FIGURE 16 DIGITAL TRANSFORMATION MARKET TO WITNESS MINOR DECLINE IN Y-O-Y GROWTH IN 2023

- 4.3 DIGITAL TRANSFORMATION MARKET: BY REGION

- FIGURE 17 NORTH AMERICA TO ACCOUNT FOR LARGEST MARKET SHARE IN 2023

- 4.4 DIGITAL TRANSFORMATION MARKET: TOP THREE VERTICALS

- FIGURE 18 BFSI TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.5 DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY AND VERTICAL

- FIGURE 19 CLOUD COMPUTING AND BFSI SEGMENTS TO ACCOUNT FOR LARGEST SHARES IN 2023

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 20 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: DIGITAL TRANSFORMATION MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Rising adoption of big data and other related technologies

- 5.2.1.2 Advent of ML and digital transformation

- 5.2.1.3 Cost benefits of cloud-based digital transformation solutions

- 5.2.1.4 Rapid proliferation of mobile devices and apps

- 5.2.1.5 Adoption and scaling of digital initiatives

- 5.2.2 RESTRAINTS

- 5.2.2.1 Changing regional data regulations to lead to time-consuming restructuring of predictive models

- 5.2.2.2 Data security concerns

- 5.2.2.3 Issues about privacy and security of information

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising internet proliferation and growing usage of connected and integrated technologies

- 5.2.3.2 Demand for personalized digital transformation

- 5.2.3.3 Increasing willingness of organizations to use digital technology

- 5.2.4 CHALLENGES

- 5.2.4.1 Integration of data from data silos

- 5.2.4.2 Issues related to IT modernization

- 5.2.4.3 Ownership and privacy of collected data

- 5.3 DIGITAL TRANSFORMATION: EVOLUTION

- FIGURE 21 EVOLUTION OF DIGITAL TRANSFORMATION

- 5.4 ECOSYSTEM

- FIGURE 22 DIGITAL TRANSFORMATION MARKET: ECOSYSTEM

- TABLE 6 DIGITAL TRANSFORMATION MARKET: ECOSYSTEM

- 5.5 CASE STUDY ANALYSIS

- 5.5.1 BFSI

- 5.5.1.1 Case study 1: Cognizant's AI and automation solution helped insurance company improve insurance claims process

- 5.5.1.2 Case study 2: Microsoft Azure platform enabled Milliman Consulting to improve its business models

- 5.5.1.3 Case study 3: BSE made real-time decisions and reduced operational costs with Cloudera solutions

- 5.5.2 TELECOMMUNICATION

- 5.5.2.1 Case study 1: American telecommunication service provider (TSP) collaborated with HCL to refine its digital journey

- 5.5.2.2 Case study 2: A1 Srbija accelerated 5G, revolutionizing digital services with HPE solutions

- 5.5.3 RETAIL & ECOMMERCE

- 5.5.3.1 Case study 1: ASOS used Microsoft Azure ML service to reduce time-to-market for recommendation model

- 5.5.3.2 Case study 2: Walmart optimized shopping experience by applying data mining

- 5.5.3.3 Case study 3: DOCOMO Digital categorized user behavior and improved campaign targeting by deploying Cloudera solutions

- 5.5.4 ENERGY & UTILITIES

- 5.5.4.1 Case study 1: Searcher Seismic made easy access in oil & gas industry with Cloudera solutions

- 5.5.4.2 Case study 2: TechnipFMC created data centralization by deploying Cloudera solutions

- 5.5.5 HEALTHCARE & LIFE SCIENCES

- 5.5.5.1 Case study 1: Leading healthcare company adopted Cognizant's AI-driven solution to identify drug-seeking behavior

- 5.5.5.2 Case study 2: Inspire used ML to connect millions of patients and caregivers on AWS

- 5.5.6 MANUFACTURING

- 5.5.6.1 Case Study 1: IBM helped SHENZHEN CSOT boost production quality and output

- 5.5.6.2 Case study 2: Dell built 360-degree customer view with Cloudera

- 5.5.7 MEDIA & ENTERTAINMENT

- 5.5.7.1 Case study 1: Leading media conglomerate adopted HCL's digital transformation solution to redefine user experience through human-centric design

- 5.5.7.2 Case study 2: Gaia boosted subscriber engagement and data-driven decision-making

- 5.5.8 GOVERNMENT & DEFENSE

- 5.5.8.1 Case study 1: OANDA provided real-time access to foreign exchange trading market by moving to Equinix's TY3 facility

- 5.5.8.2 Case study 2: Dubai government monetized and harnessed real-time data for community benefit with Cloudera

- 5.5.1 BFSI

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 KEY TECHNOLOGIES

- 5.6.1.1 Cloud computing

- 5.6.1.2 Artificial intelligence and machine learning

- 5.6.1.3 Internet of things

- 5.6.1.4 Big data analytics

- 5.6.1.5 Blockchain

- 5.6.2 ADJACENT TECHNOLOGIES

- 5.6.2.1 Edge computing

- 5.6.2.2 5G networks

- 5.6.2.3 API management

- 5.6.2.4 DevOps

- 5.6.2.5 Digital twin

- 5.6.2.6 AR/VR

- 5.6.1 KEY TECHNOLOGIES

- 5.7 MARKET ANALYSIS, BY APPLICATION

- 5.7.1 CUSTOMER TRANSFORMATION

- 5.7.2 WORKFORCE TRANSFORMATION

- 5.7.3 OPERATIONAL TRANSFORMATION

- 5.7.4 PRODUCT TRANSFORMATION

- 5.8 SUPPLY/VALUE CHAIN ANALYSIS

- FIGURE 23 SUPPLY/VALUE CHAIN ANALYSIS

- 5.9 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 24 DIGITAL TRANSFORMATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 7 DIGITAL TRANSFORMATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.9.1 THREAT OF NEW ENTRANTS

- 5.9.2 THREAT OF SUBSTITUTES

- 5.9.3 BARGAINING POWER OF SUPPLIERS

- 5.9.4 BARGAINING POWER OF BUYERS

- 5.9.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.10 PRICING MODEL ANALYSIS

- 5.10.1 INDICATIVE PRICING OF KEY OFFERINGS

- TABLE 8 PRICING ANALYSIS

- 5.11 PATENT ANALYSIS

- 5.11.1 METHODOLOGY

- 5.11.2 DOCUMENT TYPE

- TABLE 9 PATENTS FILED, 2013-2023

- 5.11.3 INNOVATION AND PATENT APPLICATIONS

- FIGURE 25 TOTAL NUMBER OF PATENTS GRANTED ANNUALLY, 2013-2023

- 5.11.3.1 Top applicants

- FIGURE 26 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS, 2013-2023

- TABLE 10 TOP 20 PATENT OWNERS IN DIGITAL TRANSFORMATION MARKET, 2013-2023

- 5.12 KEY CONFERENCES & EVENTS IN 2023-2024

- TABLE 11 DIGITAL TRANSFORMATION MARKET: LIST OF CONFERENCES & EVENTS

- 5.13 TARIFF AND REGULATORY LANDSCAPE

- 5.13.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 LATIN AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14 TRENDS/DISRUPTIONS IMPACTING BUYERS/CLIENTS IN DIGITAL TRANSFORMATION MARKET

- FIGURE 27 DIGITAL TRANSFORMATION MARKET: TRENDS/DISRUPTIONS IMPACTING BUYERS/CLIENTS

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

- TABLE 17 INFLUENCE OF STAKEHOLDERS IN BUYING PROCESS FOR TOP THREE VERTICALS (%)

- 5.15.2 BUYING CRITERIA

- FIGURE 29 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- TABLE 18 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- 5.16 BEST PRACTISES IN DIGITAL TRANSFORMATION MARKET

- 5.16.1 SYNCHRONIZING EFFORTS

- 5.16.2 ALIGNING STAFFS

- 5.16.3 LOOKING THROUGH PERSPECTIVE OF CUSTOMERS

- 5.16.4 LEVERAGING LATEST TECHNOLOGY

- 5.17 VALUE PROPOSITION - BY INDUSTRY

- TABLE 19 VALUE PROPOSITION

- 5.18 TECHNOLOGY ROADMAP OF DIGITAL TRANSFORMATION MARKET

- TABLE 20 TECHNOLOGY ROADMAP OF DIGITAL TRANSFORMATION MARKET, 2023-2030

- 5.19 BUSINESS MODELS OF DIGITAL TRANSFORMATION MARKET

- FIGURE 30 BUSINESS MODELS OF DIGITAL TRANSFORMATION MARKET

- 5.20 MATURITY MODELS OF DIGITAL TRANSFORMATION MARKET

- FIGURE 31 MATURITY MODELS OF DIGITAL TRANSFORMATION MARKET

6 DIGITAL TRANSFORMATION MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERING: DIGITAL TRANSFORMATION MARKET DRIVERS

- FIGURE 32 SERVICES SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 21 DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 22 DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- 6.2 SOLUTIONS

- 6.2.1 DIGITAL TRANSFORMATION SOLUTIONS TO BE USED ACROSS ALL SECTORS TO DIGITALIZE PROCESS

- TABLE 23 SOLUTIONS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 24 SOLUTIONS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.2.2 BY DEPLOYMENT MODE

- TABLE 25 DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 26 DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- 6.2.2.1 Cloud

- 6.2.2.1.1 Availability of subscription-based cloud solutions to offer flexibility and ease of adoption to end users

- 6.2.2.1 Cloud

- TABLE 27 CLOUD: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 28 CLOUD: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.2.2.2 On-Premises

- 6.2.2.2.1 Security concerns over sensitive data to drive adoption of on-premises solutions

- 6.2.2.2 On-Premises

- TABLE 29 ON-PREMISES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 30 ON-PREMISES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3 SERVICES

- 6.3.1 COMPLEX ALGORITHMS OF ADVANCED TECHNOLOGIES TO PROVIDE ONLINE AND OFFLINE SUPPORT SERVICES TO AI VENDORS

- TABLE 31 DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 32 DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2023-2030 (USD MILLION)

- TABLE 33 SERVICES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 34 SERVICES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3.2 CONSULTING SERVICES

- TABLE 35 CONSULTING SERVICES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 36 CONSULTING SERVICES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3.3 SUPPORT & MAINTENANCE

- TABLE 37 SUPPORT & MAINTENANCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 38 SUPPORT & MAINTENANCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3.4 PLANNING & DESIGNING

- TABLE 39 PLANNING & DESIGNING: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 40 PLANNING & DESIGNING: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3.5 ENGINEERING & RE-ENGINEERING SERVICES

- TABLE 41 ENGINEERING & RE-ENGINEERING SERVICES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 42 ENGINEERING & RE-ENGINEERING SERVICES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3.6 NETWORK & INFRASTRUCTURE MANAGEMENT

- TABLE 43 NETWORK & INFRASTRUCTURE MANAGEMENT: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 44 NETWORK & INFRASTRUCTURE MANAGEMENT: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3.7 APPLICATION DEVELOPMENT

- TABLE 45 APPLICATION DEVELOPMENT: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 46 APPLICATION DEVELOPMENT: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

7 DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.1.1 TECHNOLOGY: DIGITAL TRANSFORMATION MARKET DRIVERS

- FIGURE 33 ARTIFICIAL INTELLIGENCE SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 47 DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 48 DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- 7.2 CLOUD COMPUTING

- 7.2.1 NEED FOR DATA SECURITY, FASTER DISASTER RECOVERY, AND MEETING COMPLIANCE REQUIREMENTS TO DRIVE GROWTH

- TABLE 49 CLOUD COMPUTING: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 50 CLOUD COMPUTING: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 7.3 ARTIFICIAL INTELLIGENCE

- 7.3.1 CUSTOMER SATISFACTION ENHANCEMENT AND INCREASED PRODUCTIVITY TO DRIVE GROWTH

- TABLE 51 ARTIFICIAL INTELLIGENCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 52 ARTIFICIAL INTELLIGENCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

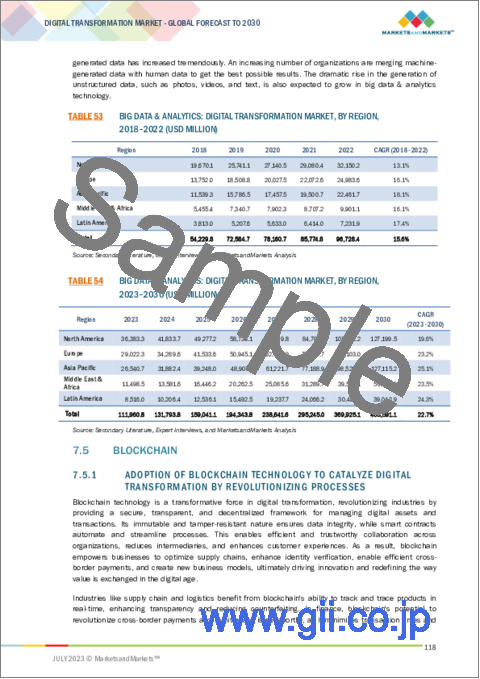

- 7.4 BIG DATA & ANALYTICS

- 7.4.1 RISING UNSTRUCTURED DATA AND NEED TO OPTIMIZE LARGE DATA WORKLOADS TO DRIVE DEMAND

- TABLE 53 BIG DATA & ANALYTICS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 54 BIG DATA & ANALYTICS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 7.5 BLOCKCHAIN

- 7.5.1 ADOPTION OF BLOCKCHAIN TECHNOLOGY TO CATALYZE DIGITAL TRANSFORMATION BY REVOLUTIONIZING PROCESSES

- TABLE 55 BLOCKCHAIN: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 56 BLOCKCHAIN: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 7.6 CYBERSECURITY

- 7.6.1 GROWING CYBERATTACKS, DATA BREACHES, AND IDENTITY THEFTS TO INCREASE DEMAND FOR CYBERSECURITY

- TABLE 57 CYBERSECURITY: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 58 CYBERSECURITY: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 7.7 INTERNET OF THINGS

- 7.7.1 INTERNET OF THINGS TO HELP ORGANIZATIONS INCREASE OPERATIONAL EFFICIENCY AND PROVIDE PROFICIENT CUSTOMER SERVICE

- TABLE 59 INTERNET OF THINGS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 60 INTERNET OF THINGS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

8 DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION

- 8.1 INTRODUCTION

- 8.1.1 BUSINESS FUNCTION: DIGITAL TRANSFORMATION MARKET DRIVERS

- FIGURE 34 HUMAN RESOURCE SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 61 DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2018-2022 (USD MILLION)

- TABLE 62 DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2023-2030 (USD MILLION)

- 8.2 DIGITAL TRANSFORMATION: ENTERPRISE USE CASES

- 8.3 ACCOUNTING & FINANCE

- 8.3.1 ADVANCED TECHNOLOGIES TO GENERATE NEW POSSIBILITIES AND ACCELERATE REVOLUTION OF FINANCE ACROSS BUSINESSES

- TABLE 63 ACCOUNTING & FINANCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 64 ACCOUNTING & FINANCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 8.4 IT & OPERATIONS

- 8.4.1 RAPID ADOPTION OF DIGITAL TRANSFORMATION SOLUTIONS TO HELP MAINTAIN DATA CONFIDENTIALITY AND INTEGRITY

- TABLE 65 IT & OPERATIONS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 66 IT & OPERATIONS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 8.5 HUMAN RESOURCES

- 8.5.1 DIGITAL TRANSFORMATION IN HUMAN RESOURCES TO PROVIDE ENHANCED DATA-DRIVEN JUDGMENT AND IMPROVED STAFF ENGAGEMENT

- TABLE 67 HUMAN RESOURCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 68 HUMAN RESOURCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 8.6 MARKETING & SALES

- 8.6.1 DIGITAL TRANSFORMATION IN SALES & MARKETING TO PROVIDE WIDER MARKETING INSIGHTS AND CUSTOMER DATA

- TABLE 69 MARKETING & SALES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 70 MARKETING & SALES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

9 DIGITAL TRANSFORMATION MARKET, BY VERTICAL

- 9.1 INTRODUCTION

- 9.1.1 VERTICAL: DIGITAL TRANSFORMATION MARKET DRIVERS

- FIGURE 35 BFSI TO ACCOUNT FOR LARGEST MARKET SIZE DURING FORECAST PERIOD

- TABLE 71 DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 72 DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2023-2030 (USD MILLION)

- 9.2 BFSI

- 9.2.1 IMPROVED BUSINESS PERFORMANCE AND REDUCED COST TO BOOST DEMAND FOR DIGITAL TRANSFORMATION SOLUTIONS

- TABLE 73 BFSI: USE CASES

- TABLE 74 BFSI: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 75 BFSI: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.2.2 FRAUD DETECTION AND PREVENTION

- 9.2.3 ASSET AND INVESTMENT MANAGEMENT

- 9.2.4 CUSTOMER SERVICE AUTOMATION (CHATBOTS)

- 9.2.5 PERSONALIZED FINANCIAL RECOMMENDATIONS

- 9.2.6 REGULATORY COMPLIANCE MONITORING

- 9.2.7 OTHERS

- 9.3 RETAIL & E-COMMERCE

- 9.3.1 ADOPTION OF DIGITAL TRANSFORMATION SOLUTIONS TO BOOST BUSINESS DECISION PERFORMANCE AND PROFIT MARGINS

- TABLE 76 RETAIL & E-COMMERCE: USE CASES

- TABLE 77 RETAIL & E-COMMERCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 78 RETAIL & E-COMMERCE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.3.2 PERSONALIZED PRODUCT RECOMMENDATIONS

- 9.3.3 CUSTOMER RELATIONSHIP MANAGEMENT

- 9.3.4 PAYMENT SERVICES MANAGEMENT

- 9.3.5 VIRTUAL CUSTOMER SUPPORT

- 9.3.6 CONTACTLESS PAYMENTS AND MOBILE WALLETS

- 9.3.7 OTHERS

- 9.4 INFORMATION TECHNOLOGY/INFORMATION TECHNOLOGY-ENABLED SERVICES

- 9.4.1 DIGITALIZING BUSINESS PROCESSES TO MEET GROWING CUSTOMER DEMANDS TO DRIVE MARKET

- TABLE 79 INFORMATION TECHNOLOGY/INFORMATION TECHNOLOGY-ENABLED SERVICES: USE CASES

- TABLE 80 INFORMATION TECHNOLOGY/INFORMATION TECHNOLOGY-ENABLED SERVICES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 81 INFORMATION TECHNOLOGY/INFORMATION TECHNOLOGY-ENABLED SERVICES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.4.2 AUTOMATED CODE GENERATION AND OPTIMIZATION

- 9.4.3 AUTOMATED IT ASSET MANAGEMENT

- 9.4.4 IT TICKETING AND SUPPORT AUTOMATION

- 9.4.5 INTELLIGENT DATA BACKUP AND RECOVERY

- 9.4.6 AUTOMATED SOFTWARE TESTING AND QUALITY ASSURANCE

- 9.4.7 OTHERS

- 9.5 MEDIA & ENTERTAINMENT

- 9.5.1 RISING CONTENT CONSUMPTION, DIGITAL ENTERTAINMENT, AND CLOUD ADOPTION TO GENERATE DEMAND FOR DIGITAL TRANSFORMATION

- TABLE 82 MEDIA & ENTERTAINMENT: USE CASES

- TABLE 83 MEDIA & ENTERTAINMENT: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 84 MEDIA & ENTERTAINMENT: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.5.2 CONTENT RECOMMENDATION SYSTEMS

- 9.5.3 CONTENT CREATION AND GENERATION

- 9.5.4 CONTENT COPYRIGHT PROTECTION

- 9.5.5 AUDIENCE ENGAGEMENT AND PERSONALIZATION

- 9.5.6 PERSONALIZED ADVERTISING

- 9.5.7 OTHERS

- 9.6 MANUFACTURING

- 9.6.1 ADOPTION OF DIGITAL TRANSFORMATION WITH NEW TECHNOLOGIES TO BOOST PERFORMANCE AND IMPROVE DECISION-MAKING

- TABLE 85 MANUFACTURING: USE CASES

- TABLE 86 MANUFACTURING: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 87 MANUFACTURING: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.6.2 PREDICTIVE MAINTENANCE AND MACHINERY INSPECTION

- 9.6.3 PRODUCTION PLANNING

- 9.6.4 DEFECT DETECTION AND PREVENTION

- 9.6.5 QUALITY CONTROL

- 9.6.6 PRODUCTION LINE OPTIMIZATION

- 9.6.7 INTELLIGENT INVENTORY MANAGEMENT

- 9.6.8 OTHERS

- 9.7 HEALTHCARE, LIFE SCIENCES & PHARMACEUTICALS

- 9.7.1 REAL-TIME DECISION-MAKING TO DELIVER PROPER INSIGHTS FOR PATIENTS TO BOOST NEED FOR DIGITAL TRANSFORMATION SOLUTIONS

- TABLE 88 HEALTHCARE, LIFE SCIENCES & PHARMACEUTICALS: USE CASES

- TABLE 89 HEALTHCARE, LIFE SCIENCES & PHARMACEUTICALS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 90 HEALTHCARE, LIFE SCIENCES & PHARMACEUTICALS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.7.2 ELECTRONIC HEALTH RECORDS AND ELECTRONIC MEDICAL RECORDS (E-HR & E-MR)

- 9.7.3 TELEMEDICINE AND REMOTE PATIENT MONITORING

- 9.7.4 HEALTH INFORMATION EXCHANGE

- 9.7.5 MEDICAL IMAGING AND DIAGNOSTICS

- 9.7.6 HEALTH APPLICATIONS

- 9.7.7 OTHERS

- 9.8 ENERGY & UTILITIES

- 9.8.1 RISING NEED TO MANAGE MASSIVE AMOUNT OF MISSION-CRITICAL MATERIAL IN REAL TIME TO DRIVE MARKET

- TABLE 91 ENERGY & UTILITIES: USE CASES

- TABLE 92 ENERGY & UTILITIES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 93 ENERGY & UTILITIES: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.8.2 ENERGY DEMAND FORECASTING

- 9.8.3 GRID OPTIMIZATION AND MANAGEMENT

- 9.8.4 ENERGY CONSUMPTION ANALYTICS

- 9.8.5 SMART METERING AND ENERGY DATA MANAGEMENT

- 9.8.6 REAL-TIME ENERGY MONITORING AND CONTROL

- 9.8.7 OTHERS

- 9.9 GOVERNMENT & DEFENSE

- 9.9.1 TAX COLLECTION, SAFETY, PUBLIC INTEREST, AND CRITICAL INTERNATIONAL DATA SHARING TO BOOST GROWTH

- TABLE 94 GOVERNMENT & DEFENSE: USE CASES

- TABLE 95 GOVERNMENT & DEFENSE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 96 GOVERNMENT & DEFENSE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.9.2 INTELLIGENCE ANALYSIS AND DATA PROCESSING

- 9.9.3 E-GOVERNANCE AND DIGITAL CITY SERVICES

- 9.9.4 BORDER SECURITY AND SURVEILLANCE

- 9.9.5 DIGITAL IDENTITY AND AUTHENTICATION

- 9.9.6 COMMAND AND CONTROL SYSTEMS

- 9.9.7 TAX AND REVENUE MANAGEMENT

- 9.9.8 OTHERS

- 9.10 TELECOMMUNICATIONS

- 9.10.1 INCREASING USE OF CONNECTED DEVICES, IOT, AND 5G TO HELP ADOPTION OF DIGITAL TRANSFORMATION SOLUTIONS

- TABLE 97 TELECOMMUNICATIONS: USE CASES

- TABLE 98 TELECOMMUNICATIONS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 99 TELECOMMUNICATIONS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.10.2 NETWORK OPTIMIZATION

- 9.10.3 NETWORK SECURITY

- 9.10.4 CUSTOMER SERVICE AND SUPPORT

- 9.10.5 NETWORK PLANNING AND OPTIMIZATION

- 9.10.6 VOICE AND SPEECH RECOGNITION

- 9.10.7 OTHERS

- 9.11 EDUCATION

- 9.11.1 NEED FOR INNOVATIVE AND FLEXIBLE LEARNING SOLUTIONS IN DIGITAL AGE TO DRIVE MARKET

- TABLE 100 EDUCATION: USE CASES

- TABLE 101 EDUCATION: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 102 EDUCATION: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.11.2 MOBILE LEARNING

- 9.11.3 LEARNING MANAGEMENT SYSTEMS

- 9.11.4 ADAPTIVE LEARNING AND ASSESSMENT

- 9.11.5 DIGITAL TEXTBOOKS AND E-BOOKS

- 9.11.6 E-LEARNING

- 9.11.7 ADMINISTRATIVE AUTOMATION

- 9.11.8 OTHERS

- 9.12 AGRICULTURE

- 9.12.1 NEED FOR INCREASED FOOD PRODUCTION TO DRIVE MARKET

- TABLE 103 AGRICULTURE: USE CASES

- TABLE 104 AGRICULTURE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 105 AGRICULTURE: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.12.2 CROP MONITORING

- 9.12.3 YIELD MONITORING AND PREDICTION

- 9.12.4 IRRIGATION AND WATER MANAGEMENT

- 9.12.5 FEEDING MANAGEMENT

- 9.12.6 WEATHER AND CLIMATE MONITORING

- 9.12.7 FARM MANAGEMENT SYSTEMS

- 9.12.8 OTHERS

- 9.13 AUTOMOTIVE, TRANSPORTATION & LOGISTICS

- 9.13.1 INCREASING DEMAND FOR SEAMLESS CONNECTIVITY, AUTONOMOUS VEHICLES, AND EFFICIENT LOGISTICS TO DRIVE MARKET

- TABLE 106 AUTOMOTIVE, TRANSPORTATION & LOGISTICS: USE CASES

- TABLE 107 AUTOMOTIVE, TRANSPORTATION & LOGISTICS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 108 AUTOMOTIVE, TRANSPORTATION & LOGISTICS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.13.2 ROUTE OPTIMIZATION

- 9.13.3 TRAFFIC MANAGEMENT

- 9.13.4 DRIVER ASSISTANCE SYSTEMS

- 9.13.5 FLEET MANAGEMENT

- 9.13.6 INTELLIGENT PARKING SYSTEMS

- 9.13.7 OTHERS

- 9.14 OTHER VERTICALS

- TABLE 109 OTHER VERTICALS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 110 OTHER VERTICALS: DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

10 DIGITAL TRANSFORMATION MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 36 ASIA PACIFIC TO ACCOUNT FOR HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 111 DIGITAL TRANSFORMATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 112 DIGITAL TRANSFORMATION MARKET, BY REGION, 2023-2030 (USD MILLION)

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET DRIVERS

- 10.2.2 NORTH AMERICA: RECESSION IMPACT

- TABLE 113 NORTH AMERICA: PROMINENT PLAYERS

- FIGURE 37 NORTH AMERICA: MARKET SNAPSHOT

- TABLE 114 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 115 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 116 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 117 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 118 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 119 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2023-2030 (USD MILLION)

- TABLE 120 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 121 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 122 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2018-2022 (USD MILLION)

- TABLE 123 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2023-2030 (USD MILLION)

- TABLE 124 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 125 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2023-2030 (USD MILLION)

- TABLE 126 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 127 NORTH AMERICA: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- 10.2.3 US

- 10.2.3.1 Increase in digitalization in various verticals to drive growth

- TABLE 128 US: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 129 US: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 130 US: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 131 US: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 132 US: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 133 US: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- 10.2.4 CANADA

- 10.2.4.1 Huge investments and growing availability of advanced technologies to drive growth

- 10.3 EUROPE

- 10.3.1 EUROPE: DIGITAL TRANSFORMATION MARKET DRIVERS

- 10.3.2 EUROPE: RECESSION IMPACT

- TABLE 134 EUROPE: PROMINENT PLAYERS

- TABLE 135 EUROPE: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 136 EUROPE: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 137 EUROPE: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 138 EUROPE: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 139 EUROPE: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 140 EUROPE: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2023-2030 (USD MILLION)

- TABLE 141 EUROPE: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 142 EUROPE: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 143 EUROPE: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2018-2022 (USD MILLION)

- TABLE 144 EUROPE: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2023-2030 (USD MILLION)

- TABLE 145 EUROPE: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 146 EUROPE: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2023-2030 (USD MILLION)

- TABLE 147 EUROPE: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 148 EUROPE: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- 10.3.3 UK

- 10.3.3.1 Advanced IT infrastructure and initiatives boosting digital transformation to drive demand

- TABLE 149 UK: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 150 UK: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 151 UK: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 152 UK: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 153 UK: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 154 UK: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- 10.3.4 GERMANY

- 10.3.4.1 Huge investments in technological developments and government initiatives to drive demand

- 10.3.5 FRANCE

- 10.3.5.1 Heavy demand for digitalization along with huge investments in R&D to drive growth

- 10.3.6 POLAND

- 10.3.6.1 Private and public sectors to rapidly adopt digital transformation solutions

- 10.3.7 SPAIN

- 10.3.7.1 Initiatives taken by government to promote widespread adoption of AI

- 10.3.8 ITALY

- 10.3.8.1 Rising adoption of cutting-edge technologies to drive growth

- 10.3.9 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET DRIVERS

- 10.4.2 ASIA PACIFIC: IMPACT OF RECESSION

- TABLE 155 ASIA PACIFIC: PROMINENT PLAYERS

- FIGURE 38 ASIA PACIFIC: MARKET SNAPSHOT

- TABLE 156 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 157 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 158 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 159 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 160 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 161 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2023-2030 (USD MILLION)

- TABLE 162 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 163 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 164 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2018-2022 (USD MILLION)

- TABLE 165 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2023-2030 (USD MILLION)

- TABLE 166 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 167 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2023-2030 (USD MILLION)

- TABLE 168 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 169 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 170 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY ASEAN COUNTRY, 2018-2022 (USD MILLION)

- TABLE 171 ASIA PACIFIC: DIGITAL TRANSFORMATION MARKET, BY ASEAN COUNTRY, 2023-2030 (USD MILLION)

- 10.4.3 CHINA

- 10.4.3.1 Investments in infrastructure and advanced technologies to fuel adoption of digital transformation

- TABLE 172 CHINA: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 173 CHINA: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 174 CHINA: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 175 CHINA: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 176 CHINA: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 177 CHINA: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- 10.4.4 JAPAN

- 10.4.4.1 Investments in private and government sector to increase competitiveness

- 10.4.5 INDIA

- 10.4.5.1 Rapid adoption of modern technologies and investments by global players to drive growth

- 10.4.6 AUSTRALIA & NEW ZEALAND

- 10.4.6.1 Government initiatives to drive growth

- 10.4.7 SOUTH KOREA

- 10.4.7.1 Rapid adoption and government investments to enable growth

- 10.4.8 ASEAN COUNTRIES

- 10.4.8.1.1 Singapore

- 10.4.8.1.2 Malaysia

- 10.4.8.1.3 Indonesia

- 10.4.9 REST OF ASIA PACIFIC

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET DRIVERS

- 10.5.2 MIDDLE EAST & AFRICA: IMPACT OF RECESSION

- TABLE 178 MIDDLE EAST & AFRICA: PROMINENT PLAYERS

- TABLE 179 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 180 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 181 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 182 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 183 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 184 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2023-2030 (USD MILLION)

- TABLE 185 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 186 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 187 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2018-2022 (USD MILLION)

- TABLE 188 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2023-2030 (USD MILLION)

- TABLE 189 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 190 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2023-2030 (USD MILLION)

- TABLE 191 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 192 MIDDLE EAST & AFRICA: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- 10.5.3 UAE

- 10.5.3.1 Investments by global players to drive adoption of digital transformation solutions

- 10.5.4 SOUTH AFRICA

- 10.5.4.1 Various government initiatives to encourage growth of digital transformation solutions

- 10.5.5 ISRAEL

- 10.5.5.1 Government support to propel growth of digital transformation

- 10.5.6 SAUDI ARABIA

- 10.5.6.1 Growing application of technologies across various industry verticals to drive growth

- 10.5.7 TURKEY

- 10.5.7.1 Initiatives by government to foster innovation and drive economic growth

- 10.5.8 REST OF MIDDLE EAST & AFRICA

- 10.5.8.1 Growing adoption of cloud technologies to boost digital transformation solutions

- 10.6 LATIN AMERICA

- 10.6.1 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET DRIVERS

- 10.6.2 LATIN AMERICA: IMPACT OF RECESSION

- TABLE 193 LATIN AMERICA: PROMINENT PLAYERS

- TABLE 194 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2018-2022 (USD MILLION)

- TABLE 195 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2023-2030 (USD MILLION)

- TABLE 196 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 197 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY DEPLOYMENT MODE, 2023-2030 (USD MILLION)

- TABLE 198 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2018-2022 (USD MILLION)

- TABLE 199 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY SERVICE, 2023-2030 (USD MILLION)

- TABLE 200 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 201 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 202 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2018-2022 (USD MILLION)

- TABLE 203 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2023-2030 (USD MILLION)

- TABLE 204 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 205 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2023-2030 (USD MILLION)

- TABLE 206 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 207 LATIN AMERICA: DIGITAL TRANSFORMATION MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- 10.6.3 BRAZIL

- 10.6.3.1 Enhanced customer experience and customized products and services to drive market

- 10.6.4 MEXICO

- 10.6.4.1 Various government investments and initiatives to boost demand for digital transformation

- 10.6.5 ARGENTINA

- 10.6.5.1 Rising adoption of artificial intelligence to improve decision-making and boost market growth

- 10.6.6 CHILE

- 10.6.6.1 Leveraging digital technologies to enhance its economic competitiveness

- 10.6.7 REST OF LATIN AMERICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 208 OVERVIEW OF STRATEGIES DEPLOYED BY KEY PLAYERS IN DIGITAL TRANSFORMATION MARKET

- 11.3 HISTORICAL REVENUE ANALYSIS OF KEY PLAYERS

- FIGURE 39 HISTORICAL REVENUE ANALYSIS OF TOP PLAYERS, 2020-2022 (USD MILLION)

- 11.4 MARKET SHARE ANALYSIS

- FIGURE 40 DIGITAL TRANSFORMATION MARKET: MARKET SHARE ANALYSIS

- TABLE 209 DIGITAL TRANSFORMATION MARKET: DEGREE OF COMPETITION

- 11.5 COMPANY EVALUATION MATRIX

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- FIGURE 41 KEY DIGITAL TRANSFORMATION MARKET PLAYERS, COMPANY EVALUATION MATRIX, 2022

- 11.6 STARTUPS AND SMES EVALUATION MATRIX

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- FIGURE 42 DIGITAL TRANSFORMATION MARKET EVALUATION MATRIX FOR STARTUPS AND SMES, 2022

- 11.7 COMPETITIVE BENCHMARKING

- TABLE 210 DIGITAL TRANSFORMATION MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 211 DIGITAL TRANSFORMATION MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS

- TABLE 212 DIGITAL TRANSFORMATION MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- 11.8 COMPETITIVE SCENARIO

- 11.8.1 PRODUCT LAUNCHES

- TABLE 213 PRODUCT LAUNCHES, 2018-2023

- 11.8.2 DEALS

- TABLE 214 DEALS, 2018-2023

- 11.8.3 OTHERS

- TABLE 215 OTHERS, 2018-2022

12 COMPANY PROFILES

- 12.1 INTRODUCTION

- 12.2 KEY PLAYERS

- (Business overview, Products/Solutions/Services offered, Recent developments, MnM view, Key strengths, Strategic choices, and Weaknesses and competitive threats)**

- 12.2.1 MICROSOFT

- TABLE 216 MICROSOFT: BUSINESS OVERVIEW

- FIGURE 43 MICROSOFT: COMPANY SNAPSHOT

- TABLE 217 MICROSOFT: SOLUTIONS OFFERED

- TABLE 218 MICROSOFT: SERVICES OFFERED

- TABLE 219 MICROSOFT: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 220 MICROSOFT: DEALS

- 12.2.2 IBM

- TABLE 221 IBM: BUSINESS OVERVIEW

- FIGURE 44 IBM: COMPANY SNAPSHOT

- TABLE 222 IBM: SOLUTIONS OFFERED

- TABLE 223 IBM: SERVICES OFFERED

- TABLE 224 IBM: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 225 IBM: DEALS

- TABLE 226 IBM: OTHERS

- 12.2.3 SAP

- TABLE 227 SAP: BUSINESS OVERVIEW

- FIGURE 45 SAP: COMPANY SNAPSHOT

- TABLE 228 SAP: SOLUTIONS OFFERED

- TABLE 229 SAP: SERVICES OFFERED

- TABLE 230 SAP: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 231 SAP: DEALS

- TABLE 232 SAP: OTHERS

- 12.2.4 ORACLE

- TABLE 233 ORACLE: BUSINESS OVERVIEW

- FIGURE 46 ORACLE: COMPANY SNAPSHOT

- TABLE 234 ORACLE: SOLUTIONS OFFERED

- TABLE 235 ORACLE: SERVICES OFFERED

- TABLE 236 ORACLE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 237 ORACLE: DEALS

- TABLE 238 ORACLE: OTHERS

- 12.2.5 GOOGLE

- TABLE 239 GOOGLE: BUSINESS OVERVIEW

- FIGURE 47 GOOGLE: COMPANY SNAPSHOT

- TABLE 240 GOOGLE: SOLUTIONS OFFERED

- TABLE 241 GOOGLE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 242 GOOGLE: DEALS

- 12.2.6 SALESFORCE

- TABLE 243 SALESFORCE: BUSINESS OVERVIEW

- FIGURE 48 SALESFORCE: COMPANY SNAPSHOT

- TABLE 244 SALESFORCE: SOLUTIONS OFFERED

- TABLE 245 SALESFORCE: SERVICES OFFERED

- TABLE 246 SALESFORCE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 247 SALESFORCE: DEALS

- 12.2.7 HPE

- TABLE 248 HPE: BUSINESS OVERVIEW

- FIGURE 49 HPE: COMPANY SNAPSHOT

- TABLE 249 HPE: SOLUTIONS OFFERED

- TABLE 250 HPE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 251 HPE: DEALS

- TABLE 252 HPE: OTHERS

- 12.2.8 ADOBE

- TABLE 253 ADOBE: BUSINESS OVERVIEW

- FIGURE 50 ADOBE: COMPANY SNAPSHOT

- TABLE 254 ADOBE: SOLUTIONS OFFERED

- TABLE 255 ADOBE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 256 ADOBE: DEALS

- 12.2.9 BAIDU

- TABLE 257 BAIDU: BUSINESS OVERVIEW

- FIGURE 51 BAIDU: COMPANY SNAPSHOT

- TABLE 258 BAIDU: SOLUTIONS OFFERED

- TABLE 259 BAIDU: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 260 BAIDU: DEALS

- 12.2.10 HCL TECHNOLOGIES

- TABLE 261 HCL TECHNOLOGIES: BUSINESS OVERVIEW

- FIGURE 52 HCL TECHNOLOGIES: COMPANY SNAPSHOT

- TABLE 262 HCL TECHNOLOGIES: SOLUTIONS OFFERED

- TABLE 263 HCL TECHNOLOGIES: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 264 HCL TECHNOLOGIES: DEALS

- 12.2.11 EY

- TABLE 265 EY: BUSINESS OVERVIEW

- FIGURE 53 EY: COMPANY SNAPSHOT

- TABLE 266 EY: SERVICES OFFERED

- TABLE 267 EY: DEALS

- 12.2.12 COGNIZANT

- TABLE 268 COGNIZANT: BUSINESS OVERVIEW

- FIGURE 54 COGNIZANT: COMPANY SNAPSHOT

- TABLE 269 COGNIZANT: SERVICES OFFERED

- TABLE 270 COGNIZANT: DEALS

- 12.2.13 ACCENTURE

- TABLE 271 ACCENTURE: BUSINESS OVERVIEW

- FIGURE 55 ACCENTURE: COMPANY SNAPSHOT

- TABLE 272 ACCENTURE: SERVICES OFFERED

- TABLE 273 ACCENTURE: DEALS

- 12.2.14 BROADCOM

- TABLE 274 BROADCOM: BUSINESS OVERVIEW

- FIGURE 56 BROADCOM: COMPANY SNAPSHOT

- TABLE 275 BROADCOM: SOLUTIONS OFFERED

- TABLE 276 BROADCOM: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 277 BROADCOM: DEALS

- 12.2.15 EQUINIX

- TABLE 278 EQUINIX: BUSINESS OVERVIEW

- FIGURE 57 EQUINIX: COMPANY SNAPSHOT

- TABLE 279 EQUINIX: SOLUTIONS OFFERED

- TABLE 280 EQUINIX: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 281 EQUINIX: DEALS

- TABLE 282 EQUINIX: OTHERS

- 12.2.16 ALIBABA

- TABLE 283 ALIBABA: BUSINESS OVERVIEW

- TABLE 284 ALIBABA: SOLUTIONS OFFERED

- TABLE 285 ALIBABA: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 286 ALIBABA: DEALS

- TABLE 287 ALIBABA: OTHERS

- 12.2.17 TIBCO SOFTWARE

- TABLE 288 TIBCO SOFTWARE: BUSINESS OVERVIEW

- TABLE 289 TIBCO SOFTWARE: SOLUTIONS OFFERED

- TABLE 290 TIBCO SOFTWARE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 291 TIBCO SOFTWARE: DEALS

- 12.2.18 MARLABS

- TABLE 292 MARLABS: BUSINESS OVERVIEW

- TABLE 293 MARLABS: SOLUTIONS OFFERED

- TABLE 294 MARLABS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 295 MARLABS: DEALS

- TABLE 296 MARLABS: OTHERS

- 12.3 SMES AND STARTUPS

- 12.3.1 ALCOR SOLUTIONS

- 12.3.2 SMARTSTREAM

- 12.3.3 YASH TECHNOLOGIES

- 12.3.4 INTERFACING

- 12.3.5 DEMPTON CONSULTING GROUP

- 12.3.6 KISSFLOW

- 12.3.7 EMUDHRA

- 12.3.8 PROCESSMAKER

- 12.3.9 PROCESS STREET

- 12.3.10 HAPPIEST MINDS

- 12.3.11 SCORO

- 12.3.12 BRILLIO

- 12.3.13 AEXONIC TECHNOLOGIES

- 12.3.14 CLOUD ANGLES

- 12.3.15 MAGNETAR IT

- 12.3.16 SCITARA

- 12.3.17 INTRINSIC

- 12.3.18 SOUNDFUL

- *Details on Business overview, Products/Solutions/Services offered, Recent developments, MnM view, Key strengths, Strategic choices, and Weaknesses and competitive threats might not be captured in case of unlisted companies.

13 APPENDIX

- 13.1 ADJACENT AND RELATED MARKETS

- 13.1.1 INTRODUCTION

- 13.1.2 CLOUD COMPUTING MARKET-GLOBAL FORECAST TO 2027

- 13.1.2.1 Market definition

- 13.1.2.2 Market overview

- 13.1.2.2.1 Cloud computing market, by service model

- TABLE 297 CLOUD COMPUTING MARKET, BY SERVICE MODEL, 2017-2021 (USD BILLION)

- TABLE 298 CLOUD COMPUTING MARKET, BY SERVICE MODEL, 2022-2027 (USD BILLION)

- 13.1.2.2.2 Cloud computing market, by deployment model

- TABLE 299 CLOUD COMPUTING MARKET, BY DEPLOYMENT MODEL, 2017-2021 (USD BILLION)

- TABLE 300 CLOUD COMPUTING MARKET, BY DEPLOYMENT MODEL, 2022-2027 (USD BILLION)

- 13.1.2.2.3 Cloud computing market, by organization size

- TABLE 301 CLOUD COMPUTING MARKET, BY ORGANIZATION SIZE, 2017-2021 (USD BILLION)

- TABLE 302 CLOUD COMPUTING MARKET, BY ORGANIZATION SIZE, 2022-2027 (USD BILLION)

- 13.1.2.2.4 Cloud computing market, by industry vertical

- TABLE 303 CLOUD COMPUTING MARKET, BY VERTICAL, 2017-2021 (USD BILLION)

- TABLE 304 CLOUD COMPUTING MARKET, BY VERTICAL, 2022-2027 (USD BILLION)

- 13.1.2.2.5 Cloud computing market, by region

- TABLE 305 CLOUD COMPUTING MARKET, BY REGION, 2017-2021 (USD BILLION)

- TABLE 306 CLOUD COMPUTING MARKET, BY REGION, 2022-2027 (USD BILLION)

- 13.1.3 ARTIFICIAL INTELLIGENCE MARKET-GLOBAL FORECAST TO 2027

- 13.1.3.1 Market definition

- 13.1.3.2 Market overview

- 13.1.3.2.1 Artificial intelligence market, by offering

- TABLE 307 ARTIFICIAL INTELLIGENCE MARKET, BY OFFERING, 2016-2021 (USD BILLION)

- TABLE 308 ARTIFICIAL INTELLIGENCE MARKET, BY OFFERING, 2022-2027 (USD BILLION)

- 13.1.3.2.2 Artificial intelligence market, by deployment type

- TABLE 309 ARTIFICIAL INTELLIGENCE MARKET, BY DEPLOYMENT TYPE, 2016-2021 (USD BILLION)

- TABLE 310 ARTIFICIAL INTELLIGENCE MARKET, BY DEPLOYMENT TYPE, 2022-2027 (USD BILLION)

- 13.1.3.2.3 Artificial intelligence market, by organization size

- TABLE 311 ARTIFICIAL INTELLIGENCE MARKET, BY ORGANIZATION SIZE, 2016-2021 (USD BILLION)

- TABLE 312 ARTIFICIAL INTELLIGENCE MARKET, BY ORGANIZATION SIZE, 2022-2027 (USD BILLION)

- 13.1.3.2.4 Artificial intelligence market, by technology

- TABLE 313 ARTIFICIAL INTELLIGENCE MARKET, BY TECHNOLOGY, 2016-2021 (USD BILLION)

- TABLE 314 ARTIFICIAL INTELLIGENCE MARKET, BY TECHNOLOGY, 2022-2027 (USD BILLION)

- 13.1.3.2.5 Artificial intelligence market, by industry vertical

- TABLE 315 ARTIFICIAL INTELLIGENCE MARKET, BY VERTICAL, 2016-2021 (USD BILLION)

- TABLE 316 ARTIFICIAL INTELLIGENCE MARKET, BY VERTICAL, 2022-2027 (USD BILLION)

- 13.1.3.2.6 Artificial intelligence market, by region

- TABLE 317 ARTIFICIAL INTELLIGENCE MARKET, BY REGION, 2016-2021 (USD BILLION)

- TABLE 318 ARTIFICIAL INTELLIGENCE MARKET, BY REGION, 2022-2027 (USD BILLION)

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 CUSTOMIZATION OPTIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS