|

|

市場調査レポート

商品コード

1319498

サーキットブレーカーの世界市場 (~2028年):絶縁タイプ (真空・空気・オイル・ガス)・電圧 (中・高)・設置区分 (屋内・屋外)・エンドユーザー (送配電ユーティリティ・発電・再生可能エネルギー・鉄道)・地域別Circuit Breaker Market by Insulation Type (Vacuum, Air, Gas, & Oil), Voltage (Medium, High), Installation (Indoor, Outdoor), End-User (Transmission & Distribution Utilities, Power Generation, Renewables, & Railways) and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| サーキットブレーカーの世界市場 (~2028年):絶縁タイプ (真空・空気・オイル・ガス)・電圧 (中・高)・設置区分 (屋内・屋外)・エンドユーザー (送配電ユーティリティ・発電・再生可能エネルギー・鉄道)・地域別 |

|

出版日: 2023年07月21日

発行: MarketsandMarkets

ページ情報: 英文 259 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界のサーキットブレーカーの市場規模は、2023年の約65億米ドルから、予測期間中は5.5%のCAGRで推移し、2028年には約86億米ドルの規模に成長すると予測されています。

発電、特に再生可能エネルギー発電への投資の増加など、いくつかの要因がこの成長の原動力となっています。また、信頼性が高く安全な電力供給に対する需要が世界的に高まっており、送配電網の拡張と改善につながっています。さらに、鉄道部門でも投資が加速しており、サーキットブレーカー市場の成長にさらに貢献しています。

絶縁タイプ別では、ガス遮断器の部門が予測期間中に最大のシェアを示すと予測されています。この優位性は、高い誘電特性や省スペースといったガスサーキットブレーカーの有利な特性によるものです。アジア太平洋地域がガスサーキットブレーカーの最大の地域シェアを示し、僅差で欧州がこれに続くと予想されています。これらの地域では再生可能エネルギーへの投資が増加しており、既存の変電所のアップグレードや新規変電所の設置、特にSF6ベースのガス絶縁スイッチギアの需要が高まっているため、市場が活性化しています。

エンドユーザー別では、送配電ユーティリティの部門が予測期間中に最大の成長を示すと予測されています。電力需要の高まりにより、送配電インフラへの投資が増加しています。最新の変電所はデータハブの役割を果たすため、データの効率的なフィルタリング、分析、対応が必要となります。そのため企業は保護を強化し、従来の非効率な機器操作によって引き起こされるエネルギー損失を削減するため、スマートユーティリティソリューションの統合に注力しています。サーキットブレーカーへのセンサーの統合で、電力品質の測定、停電の減少、二次機器の保護、簡素化された安全なメンテナンス、遠隔監視と制御、貴重な原材料の使用の最小化など、いくつかの利点が得られます。

地域別では、アジア太平洋地域が急成長を遂げており、次いで欧州、北米と続いています。この成長は、中国、日本、韓国などの国々で送配電ネットワークの拡大や産業化プロジェクトが増加していることに起因しています。

当レポートでは、世界のサーキットブレーカーの市場を調査し、市場概要、市場影響因子および市場機会の分析、技術・特許の動向、ケーススタディ、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合環境、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 動向

- 平均販売価格

- エコシステムマッピング

- 貿易データ統計

- バリューチェーン分析

- 技術分析

- サーキットブレーカー:コード・規制

- イノベーション・特許登録

- ケーススタディ分析

第6章 サーキットブレーカー市場:絶縁タイプ別

- 真空

- 空気

- ガス

- オイル

第7章 サーキットブレーカー市場:設置区分別

- 屋内

- 屋外

第8章 サーキットブレーカー市場:エンドユーザー別

- 送配電ユーティリティ

- 発電所

- 再生可能エネルギー

- 鉄道

第9章 サーキットブレーカー市場:電圧別

- 中圧

- 高圧

第10章 サーキットブレーカー市場:地域別

- アジア太平洋

- 欧州

- 北米

- 南米

- 中東・アフリカ

第11章 競合情勢

- 主要企業の採用戦略

- 上位5社の市場シェア分析

- 市場評価の枠組み

- 5カ年企業収益分析

- 主要企業の評価マトリックス

- スタートアップ企業の評価マトリックス

- 競合シナリオ

第12章 企業プロファイル

- ABB

- SIEMENS

- EATON

- SCHNEIDER ELECTRIC

- MITSUBISHI ELECTRIC

- TOSHIBA CORPORATION

- POWELL INDUSTRIES

- CG POWER AND INDUSTRIAL SOLUTIONS

- FUJI ELECTRIC

- CHINT ELECTRICS CO., LTD.

- BRUSH GROUP

- TAVRIDA ELECTRIC

- SECHERON

- EFACEC POWER SOLUTIONS

- HYUNDAI ELECTRIC

- TE CONNECTIVITY

- ENTEC ELECTRIC & ELECTRONIC

- LS ELECTRIC

- SCHALTBAU

- KIRLOSKAR ELECTRIC

- YUEQING AISO ELECTRIC

- SRIWIN ELECTRIC

- ORECCO

- ORMAZABAL

- YUEQING LIYOND ELECTRIC

- SAFVOLT SWITCHGEARS

第13章 付録

The circuit breaker market is expected to experience significant growth, with its size expanding from approximately USD 6.5 billion in 2023 to about USD 8.6 billion by 2028. This represents a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2023 to 2028. Several factors are driving this growth, including the increasing investments in power generation, particularly in renewable energy sources. There is also a growing global demand for dependable and secure power supply, leading to the expansion and improvement of transmission and distribution networks. Furthermore, the railway sector is witnessing accelerated investments, further contributing to the growth of the circuit breaker market.

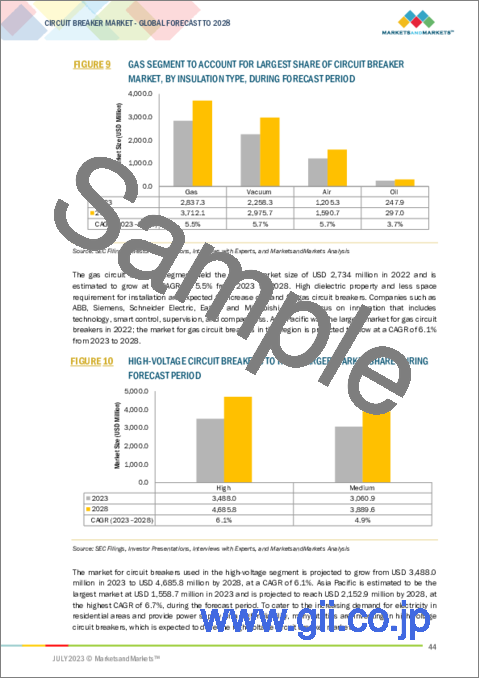

"The gas circuit breaker segment is expected to hold the largest share of the circuit breaker market, by insulation type, during the forecast period."

During the projected timeframe, the gas circuit breakers segment is expected to dominate the circuit breaker market. This dominance is attributed to the favorable characteristics of gas circuit breakers, such as their high dielectric property and space-saving benefits. The Asia Pacific region is anticipated to hold the largest market share for gas circuit breakers, closely followed by Europe. The growing investments in renewable energy sources in these regions are driving the demand for upgrades to existing substations or the installation of new ones, specifically in SF6-based gas-insulated switchgear, thus stimulating the market for gas circuit breakers.

"T&D Utilities: The largest- growing segment of the circuit breaker market"

The industrial segment is expected to exhibit the highest growth rate in the circuit breaker market from 2023 to 2028, based on its application. The rising demand for electrical power has resulted in increased investments in transmission and distribution infrastructure. Modern substations serve as data hubs, necessitating the efficient filtering, analysis, and response to the data. Consequently, companies are focusing on integrating smart utility solutions to enhance protection and reduce energy losses caused by inefficient traditional equipment operation. The integration of sensors in circuit breakers offers several benefits, including power quality measurements, reduced interruptions, protection of secondary equipment, simplified and safe maintenance, remote monitoring and control, and minimized use of valuable raw materials. Among the end-user segments, the transmission and distribution (T&D) sector is experiencing the highest growth rate in the global circuit breaker market. This can be attributed to the replacement of aging infrastructure in power utilities and the growing demand for electricity.

"Asia Pacific: The fastest-growing market for circuit breaker."

The Asia Pacific region is experiencing rapid growth in the circuit breaker market, followed by Europe and North America. This growth can be attributed to the increasing expansion of transmission and distribution networks and industrialization projects in countries such as China, Japan, and South Korea. For example, the State Grid Corporation of China (SGCC) has outlined plans to invest USD 250 billion in upgrading electric power infrastructure, with USD 45 billion allocated specifically for smart grids between 2018 and 2020. Similarly, Korea Electric Power Corp. (KEPCO) in South Korea has planned a USD 7.18 billion investment for the development of a nationwide smart grid infrastructure by 2030. These substantial investments are expected to drive the demand for circuit breakers in the Asia Pacific region.

Breakdown of Primaries:

Primary interviews were conducted with a diverse range of key industry participants, subject-matter experts, C-level executives from key market players, industry consultants, and other relevant experts. These interviews were carried out to gather and verify crucial qualitative and quantitative information, as well as to evaluate the future prospects of the market. The distribution of these primary interviews is as follows:

By Company Type: Tier 1- 65%, Tier 2- 24%, Tier 3- 11%

By Designation: C-Level- 30%, D-Level- 25%, Others- 45%

By Region: North America- 27%, Europe- 20%, Asia Pacific- 33%, Middle East & Africa- 8%, , and South America- 12%

Note: The tier of the companies has been defined based on their total revenue; as of 2017: Tier 1 = >USD 5 billion, Tier 2 = USD 1 billion to USD 5 billion, and Tier 3 = <USD 1 billion.

The key players in the circuit breaker market include companies such as ABB (Switzerland), Schneider Electric (France), Siemens (Germany), Mitsubishi Electric (Japan), and Eaton (Ireland).

Research Coverage:

The report offers a comprehensive overview of the circuit breaker market, covering various regions. Its objective is to estimate the market size and assess the potential for future growth across different segments, including insulation type, voltage, installation, end user, and region. Additionally, the report includes a detailed competitive analysis of key players in the market, featuring their company profiles, recent developments, and key market strategies. The market has been segmented based on insulation type, voltage, installation, end user, and region, with a focus on analyzing industry trends. The report also provides market share analysis of the top players, supply chain analysis, and company profiles, collectively providing insights into the competitive landscape and emerging high-growth segments within the circuit breaker market.

Key Benefits of Buying the Report

The report is designed to assist leaders and new entrants in the circuit breaker market by providing them with reliable revenue estimates for the overall market as well as its sub-segments. This information will enable stakeholders to understand the competitive landscape and gain valuable insights to effectively position their businesses and develop suitable go-to-market strategies. Furthermore, the report helps stakeholders comprehend the current state of the market and provides key information on market drivers, restraints, challenges, and opportunities. By understanding these factors, stakeholders can make informed decisions and stay attuned to market dynamics in the circuit breaker industry.

- Analysis of key drivers (increasing investments in renewable energy-based power generation, expanding t&d network capacity additions and improvements, fortifying the infrastructure for power distribution, more money being invested in industrial production), restraints (regulations that limit the emissions of SF6 gas and competition from the unorganised sector), opportunities (Increasing use of high-voltage direct current systems, the digitalization of emerging smart technologies, the need to replace ageing grid infrastructure, and the requirement for dependable T&D networks are all factors), and challenges (High temperature, arc flashing, and overpressure during operation are risks, as is the installation of modernised circuit breakers) influencing the growth of the ac circuit breaker market.

- Product Development/ Innovation: The circuit breaker market is poised for a promising future, as evidenced by recent developments such as Mitsubishi Electric's acquisition of Scibreak AB. On February 16, Mitsubishi Electric announced its complete acquisition of Scibreak AB, a Swedish company specializing in the development of DC circuit breakers (DCCBs). This strategic move aims to enhance the competitiveness of both companies by fostering close collaboration in the advancement of DCCB technologies for high-voltage direct current (HVDC) systems. This joint effort aligns with the growing global deployment of renewable energy sources and underscores the industry's commitment to supporting the expansion of HVDC systems.

- Market Development: The expansion of power distribution networks can be attributed to several factors, including the rise in per capita income, the growth of the middle-class population, increasing urbanization, and improved access to electricity in remote areas. In some developing countries, rural electrification initiatives are prioritizing distributed power generation over reliance on large national grids. For example, the Indian Government is actively working towards enhancing power supply in villages through initiatives like the Restructured Accelerated Power Development and Reforms Program (R-APDRP) and the Deendayal Upadhyaya Gram Jyoti Yojana (DDUGJY). These schemes present significant opportunities for the circuit breaker market to contribute to the development of robust and reliable power infrastructure.

- Market Diversification: Mitsubishi Electric specializes in offering technologically advanced and integrated products, with a particular emphasis on high-voltage circuit breakers. Recently, the company achieved a significant milestone as its 160 KV high-voltage circuit breaker prototype successfully passed the DC interruption test conducted as part of a research project by the European Commission. This achievement highlights Mitsubishi Electric's commitment to innovation and its ability to deliver reliable solutions in the field of circuit breakers. Furthermore, the company places a strong focus on investments and expansion as key strategies to enhance its market presence. By investing in research and development, Mitsubishi Electric aims to stay at the forefront of technological advancements in the circuit breaker industry. Additionally, the company's expansion efforts aim to penetrate new markets and strengthen its global footprint, further solidifying its position in the market.

- Competitive Assessment: A comprehensive evaluation has been conducted to analyze the market shares, growth strategies, and service offerings of prominent players in the circuit breaker market, including Eaton (Ireland), ABB (Switzerland), Schneider Electric (France), Siemens (Germany), and Mitsubishi Electric (Japan), among others. The assessment provides in-depth insights into the market position of these key players, their strategies for driving growth, and the range of services they offer in the circuit breaker segment.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 CIRCUIT BREAKER MARKET, BY VOLTAGE: INCLUSIONS AND EXCLUSIONS

- 1.2.2 CIRCUIT BREAKER MARKET, BY END USER: INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 CIRCUIT BREAKER MARKET: RESEARCH DESIGN

- 2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 2 DATA TRIANGULATION METHODOLOGY

- 2.2.1 SECONDARY DATA

- 2.2.1.1 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 Key data from primary sources

- 2.2.2.2 Breakdown of primaries

- 2.3 SCOPE

- FIGURE 3 METRICS CONSIDERED WHILE ASSESSING DEMAND FOR CIRCUIT BREAKERS

- 2.4 MARKET SIZE ESTIMATION

- 2.4.1 DEMAND-SIDE ANALYSIS

- FIGURE 4 CIRCUIT BREAKER MARKET: INDUSTRY- AND REGION-/COUNTRY-WISE ANALYSIS

- 2.4.1.1 Calculations for demand-side analysis

- 2.4.1.2 Assumptions for demand-side analysis

- 2.4.2 SUPPLY-SIDE ANALYSIS

- FIGURE 5 KEY METRICS CONSIDERED FOR ASSESSING SUPPLY OF CIRCUIT BREAKERS

- FIGURE 6 CIRCUIT BREAKER MARKET: SUPPLY-SIDE ANALYSIS

- 2.4.2.1 Calculations for supply-side analysis

- 2.4.2.2 Assumptions for supply-side analysis

- FIGURE 7 COMPANY REVENUE ANALYSIS, 2022

- 2.4.3 FORECAST ANALYSIS

3 EXECUTIVE SUMMARY

- TABLE 1 CIRCUIT BREAKER MARKET SNAPSHOT

- FIGURE 8 ASIA PACIFIC DOMINATED CIRCUIT BREAKER MARKET IN 2022

- FIGURE 9 GAS SEGMENT TO ACCOUNT FOR LARGEST SHARE OF CIRCUIT BREAKER MARKET, BY INSULATION TYPE, DURING FORECAST PERIOD

- FIGURE 10 HIGH-VOLTAGE CIRCUIT BREAKERS TO HOLD LARGER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 11 OUTDOOR SEGMENT TO CAPTURE LARGER SHARE OF CIRCUIT BREAKER MARKET, BY INSTALLATION, DURING FORECAST PERIOD

- FIGURE 12 T&D UTILITIES TO LEAD CIRCUIT BREAKER MARKET, BY END USER, DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CIRCUIT BREAKER MARKET

- FIGURE 13 RISING INCLINATION TOWARD RENEWABLE ENERGY SOURCES TO BOOST DEMAND FOR CIRCUIT BREAKERS

- 4.2 CIRCUIT BREAKER MARKET, BY REGION

- FIGURE 14 CIRCUIT BREAKER MARKET IN ASIA PACIFIC TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- 4.3 CIRCUIT BREAKER MARKET IN ASIA PACIFIC, BY END USER AND COUNTRY

- FIGURE 15 T&D UTILITIES AND CHINA DOMINATED CIRCUIT BREAKER MARKET IN ASIA PACIFIC, BY END USER AND COUNTRY, RESPECTIVELY, IN 2022

- 4.4 CIRCUIT BREAKER MARKET, BY INSTALLATION, 2022

- FIGURE 16 OUTDOOR SEGMENT TO DOMINATE CIRCUIT BREAKER MARKET, BY INSTALLATION, IN 2028

- 4.5 CIRCUIT BREAKER MARKET, BY VOLTAGE, 2022

- FIGURE 17 HIGH VOLTAGE SEGMENT TO CAPTURE LARGER SHARE OF CIRCUIT BREAKER MARKET, BY VOLTAGE, IN 2028

- 4.6 CIRCUIT BREAKER MARKET, BY END USER, 2022

- FIGURE 18 T&D UTILITIES SEGMENT TO ACCOUNT FOR LARGEST SHARE OF CIRCUIT BREAKER MARKET, BY END USER, IN 2028

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 19 CIRCUIT BREAKER MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing investments in power generation using renewable energy sources

- FIGURE 20 GLOBAL INVESTMENTS IN POWER SECTOR, BY TECHNOLOGY, 2019-2022

- FIGURE 21 POWER GENERATION CAPACITY, BY RENEWABLE SOURCE (TERAWATT-HOURS)

- 5.2.1.2 Rising global demand for reliable and secure power supply

- 5.2.1.3 Growing focus of developing countries on modifying and upgrading existing T&D infrastructure

- FIGURE 22 GLOBAL T&D INVESTMENTS, 2019-2022 (USD BILLION)

- FIGURE 23 REGION-WISE T&D INVESTMENTS, 2022 (%)

- 5.2.1.4 Rising deployment of modern train control systems to enhance safety

- 5.2.2 RESTRAINTS

- 5.2.2.1 Stringent environmental and safety regulations for SF6 circuit breakers

- 5.2.2.2 Availability of low-cost products by local players from unorganized sector

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing adoption of smart grid technologies to protect and control power equipment

- FIGURE 24 GLOBAL INVESTMENTS IN SMART GRIDS, BY TECHNOLOGY, 2016-2021 (USD BILLION)

- 5.2.3.2 Pressing need to replace aging grid infrastructure and build reliable T&D networks

- 5.2.4 CHALLENGES

- 5.2.4.1 Risk of cyberattacks on modern circuit breakers

- 5.3 TRENDS

- 5.3.1 REVENUE SHIFT AND NEW REVENUE POCKETS FOR CIRCUIT BREAKER MANUFACTURERS

- FIGURE 25 REVENUE SHIFT AND NEW REVENUE POCKETS FOR PLAYERS IN CIRCUIT BREAKER MARKET

- 5.4 AVERAGE SELLING PRICE

- FIGURE 26 AVERAGE SELLING PRICE, 2020-2023

- 5.5 ECOSYSTEM MAPPING

- FIGURE 27 MARKET MAP FOR CIRCUIT BREAKERS

- 5.6 TRADE DATA STATISTICS

- TABLE 2 COUNTRY-WISE EXPORT DATA, 2021 AND 2022 (USD MILLION)

- TABLE 3 COUNTRY-WISE IMPORT DATA, 2021 AND 2022 (USD MILLION)

- 5.7 VALUE CHAIN ANALYSIS

- FIGURE 28 CIRCUIT BREAKER VALUE CHAIN ANALYSIS

- 5.7.1 RAW MATERIAL PROVIDERS/SUPPLIERS

- 5.7.2 COMPONENT MANUFACTURERS

- 5.7.3 ASSEMBLERS/MANUFACTURERS

- 5.7.4 DISTRIBUTORS (BUYERS)/END USERS AND POST-SALES SERVICE PROVIDERS

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 CIRCUIT BREAKER TECHNOLOGY TRENDS

- 5.9 CIRCUIT BREAKER: CODES AND REGULATIONS

- 5.10 INNOVATIONS AND PATENT REGISTRATION

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 CIRCUIT BREAKERS FOR ENERGY MARKET

- 5.11.1.1 ABB introduced HVDC circuit breaker to balance loads and boost grid reliability

- 5.11.1 CIRCUIT BREAKERS FOR ENERGY MARKET

6 CIRCUIT BREAKER MARKET, BY INSULATION TYPE

- 6.1 INTRODUCTION

- FIGURE 29 CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2022

- TABLE 4 CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 5 CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 6.2 VACUUM

- 6.2.1 ENVIRONMENTALLY FRIENDLY AND LONG SERVICE LIFE FEATURES OF VACUUM-INSULATED CIRCUIT BREAKERS TO ACCELERATE SEGMENTAL GROWTH

- TABLE 6 VACUUM: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 7 VACUUM: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.3 AIR

- 6.3.1 RISING ADOPTION OF AIR-INSULATED CIRCUIT BREAKERS TO PROTECT POWER LINES TO BOOST SEGMENTAL GROWTH

- TABLE 8 AIR: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 9 AIR: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.4 GAS

- 6.4.1 HIGH DIELECTRIC PROPERTIES, COMPACT SIZE, AND EASY MAINTENANCE TO FUEL ADOPTION OF GAS-INSULATED CIRCUIT BREAKERS

- TABLE 10 GAS: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 11 GAS: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.5 OIL

- 6.5.1 HIGH DIELECTRIC STRENGTH, RUGGEDNESS, AND ABILITY TO WITHSTAND HIGH CURRENTS TO BOOST DEMAND FOR OIL-INSULATED CIRCUIT BREAKERS

- TABLE 12 OIL: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 13 OIL: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

7 CIRCUIT BREAKER MARKET, BY INSTALLATION

- 7.1 INTRODUCTION

- FIGURE 30 CIRCUIT BREAKER MARKET, BY INSTALLATION, 2022

- TABLE 14 CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 15 CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 7.2 INDOOR

- 7.2.1 RAPID EXPANSION OF INDUSTRIAL AND COMMERCIAL SECTORS IN DEVELOPING COUNTRIES TO DRIVE MARKET

- TABLE 16 INDOOR: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 17 INDOOR: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.3 OUTDOOR

- 7.3.1 WIDESPREAD DEPLOYMENT OF WIND AND SOLAR PLANTS TO BOOST DEMAND FOR CIRCUIT BREAKERS

- TABLE 18 OUTDOOR: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 19 OUTDOOR: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

8 CIRCUIT BREAKER MARKET, BY END USER

- 8.1 INTRODUCTION

- FIGURE 31 CIRCUIT BREAKER MARKET, BY END USER, 2022

- TABLE 20 CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 21 CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 8.2 T&D UTILITIES

- 8.2.1 URGENT NEED TO REPLACE AGING ELECTRIC GRID INFRASTRUCTURE TO BOOST DEMAND FOR CIRCUIT BREAKERS

- TABLE 22 T&D UTILITIES: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 23 T&D UTILITIES: CIRCUIT BREAKER MARKET SIZE, BY REGION, 2023-2028 (USD MILLION)

- 8.3 POWER GENERATION PLANTS

- 8.3.1 INCREASED FOCUS ON ENHANCING SAFETY AND RELIABILITY OF POWER PLANTS TO BOOST DEMAND FOR CIRCUIT BREAKERS

- TABLE 24 POWER GENERATION PLANTS: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 25 POWER GENERATION PLANTS: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.4 RENEWABLES

- 8.4.1 SIGNIFICANT INVESTMENTS IN DEVELOPMENT AND DEPLOYMENT OF RENEWABLE ENERGY SOURCES TO ACCELERATE MARKET GROWTH

- TABLE 26 RENEWABLES: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 27 RENEWABLES: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.5 RAILWAYS

- 8.5.1 HIGH ADOPTION OF RAILWAY ELECTRIFICATION SYSTEMS TO BOOST DEMAND FOR CIRCUIT BREAKERS

- TABLE 28 RAILWAYS: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 29 RAILWAYS: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

9 CIRCUIT BREAKER MARKET, BY VOLTAGE

- 9.1 INTRODUCTION

- FIGURE 32 CIRCUIT BREAKER MARKET, BY VOLTAGE, 2022

- TABLE 30 CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 31 CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 9.2 MEDIUM

- 9.2.1 HIGHER RELIABILITY AND PROTECTION OFFERED BY MEDIUM-VOLTAGE CIRCUIT BREAKERS TO BOOST SEGMENTAL GROWTH

- TABLE 32 MEDIUM: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 33 MEDIUM: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3 HIGH

- 9.3.1 INCREASING INVESTMENTS IN ELECTRICAL TRANSMISSION NETWORKS TO BOOST DEMAND FOR HIGH-VOLTAGE CIRCUIT BREAKERS

- TABLE 34 HIGH: CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 35 HIGH: CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

10 CIRCUIT BREAKER MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 33 ASIA PACIFIC TO RECORD HIGHEST CAGR IN CIRCUIT BREAKER MARKET DURING FORECAST PERIOD

- FIGURE 34 CIRCUIT BREAKER MARKET SHARE (IN TERMS OF VALUE), BY REGION, 2022

- TABLE 36 CIRCUIT BREAKER MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 37 CIRCUIT BREAKER MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.2 ASIA PACIFIC

- FIGURE 35 ASIA PACIFIC: MARKET SNAPSHOT

- 10.2.1 IMPORT AND EXPORT DATA

- TABLE 38 ASIA PACIFIC: IMPORT & EXPORT DATA FOR CIRCUIT BREAKER MARKET, 2019-2022 (USD MILLION)

- 10.2.2 BY INSULATION TYPE

- TABLE 39 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 40 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.2.3 BY VOLTAGE

- TABLE 41 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 42 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.2.4 BY INSTALLATION

- TABLE 43 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 44 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.2.5 BY END USER

- TABLE 45 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 46 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.2.6 BY COUNTRY

- TABLE 47 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 48 ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.2.6.1 China

- 10.2.6.1.1 Increasing focus on developing transmission lines due to rapid urbanization to drive market

- 10.2.6.2 By insulation type

- 10.2.6.1 China

- TABLE 49 CHINA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 50 CHINA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.2.6.3 By voltage

- TABLE 51 CHINA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 52 CHINA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.2.6.4 By installation

- TABLE 53 CHINA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 54 CHINA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.2.6.5 By end user

- TABLE 55 CHINA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 56 CHINA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.2.6.6 Japan

- 10.2.6.6.1 Growing emphasis on rebuilding power grids and substations to boost demand for circuit breakers

- 10.2.6.7 By insulation type

- 10.2.6.6 Japan

- TABLE 57 JAPAN: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 58 JAPAN: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.2.6.8 By voltage

- TABLE 59 JAPAN: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 60 JAPAN: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.2.6.9 By installation

- TABLE 61 JAPAN: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 62 JAPAN: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.2.6.10 By end user

- TABLE 63 JAPAN: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 64 JAPAN: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.2.6.11 India

- 10.2.6.11.1 Increasing investments in infrastructure development projects to create opportunities for circuit breaker providers

- 10.2.6.12 By insulation type

- 10.2.6.11 India

- TABLE 65 INDIA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 66 INDIA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.2.6.13 By voltage

- TABLE 67 INDIA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 68 INDIA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.2.6.14 By installation

- TABLE 69 INDIA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 70 INDIA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.2.6.15 By end user

- TABLE 71 INDIA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 72 INDIA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.2.6.16 South Korea

- 10.2.6.16.1 Government initiatives toward renewable power generation to accelerate market growth

- 10.2.6.17 By insulation type

- 10.2.6.16 South Korea

- TABLE 73 SOUTH KOREA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 74 SOUTH KOREA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.2.6.18 By voltage

- TABLE 75 SOUTH KOREA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 76 SOUTH KOREA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.2.6.19 By installation

- TABLE 77 SOUTH KOREA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 78 SOUTH KOREA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.2.6.20 By end user

- TABLE 79 SOUTH KOREA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 80 SOUTH KOREA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.2.6.21 Australia

- 10.2.6.21.1 Increasing number of renewable power generation projects to drive demand for circuit breakers

- 10.2.6.22 By insulation type

- 10.2.6.21 Australia

- TABLE 81 AUSTRALIA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 82 AUSTRALIA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.2.6.23 By voltage

- TABLE 83 AUSTRALIA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 84 AUSTRALIA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.2.6.24 By installation

- TABLE 85 AUSTRALIA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 86 AUSTRALIA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.2.6.25 By end user

- TABLE 87 AUSTRALIA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 88 AUSTRALIA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.2.6.26 Rest of Asia Pacific

- 10.2.6.27 By insulation type

- TABLE 89 REST OF ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 90 REST OF ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.2.6.28 By voltage

- TABLE 91 REST OF ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 92 REST OF ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.2.6.29 By installation

- TABLE 93 REST OF ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 94 REST OF ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.2.6.30 By end user

- TABLE 95 REST OF ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 96 REST OF ASIA PACIFIC: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.3 EUROPE

- FIGURE 36 EUROPE: MARKET SNAPSHOT

- 10.3.1 IMPORT AND EXPORT DATA

- TABLE 97 EUROPE: IMPORT & EXPORT DATA FOR CIRCUIT BREAKER MARKET, 2019-2022 (USD MILLION)

- 10.3.2 BY INSULATION TYPE

- TABLE 98 EUROPE: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 99 EUROPE: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.3.3 BY VOLTAGE

- TABLE 100 EUROPE: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 101 EUROPE: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.3.4 BY INSTALLATION

- TABLE 102 EUROPE: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 103 EUROPE: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.3.5 BY END USER

- TABLE 104 EUROPE: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 105 EUROPE: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.3.6 BY COUNTRY

- TABLE 106 EUROPE: CIRCUIT BREAKER MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 107 EUROPE: CIRCUIT BREAKER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.3.6.1 Germany

- 10.3.6.1.1 Significant growth in renewable sector to drive market

- 10.3.6.2 By insulation type

- 10.3.6.1 Germany

- TABLE 108 GERMANY: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 109 GERMANY: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.3.6.3 By voltage

- TABLE 110 GERMANY: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 111 GERMANY: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.3.6.4 By installation

- TABLE 112 GERMANY: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 113 GERMANY: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.3.6.5 By end user

- TABLE 114 GERMANY: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 115 GERMANY: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.3.6.6 France

- 10.3.6.6.1 Growing focus on expansion of renewable power sources to present opportunities to circuit breaker vendors

- 10.3.6.7 By insulation type

- 10.3.6.6 France

- TABLE 116 FRANCE: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 117 FRANCE: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.3.6.8 By voltage

- TABLE 118 FRANCE: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 119 FRANCE: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.3.6.9 By installation

- TABLE 120 FRANCE: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 121 FRANCE: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.3.6.10 By end user

- TABLE 122 FRANCE: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 123 FRANCE: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.3.6.11 UK

- 10.3.6.11.1 Rapid transition to cleaner energy sources to drive market

- 10.3.6.12 By insulation type

- 10.3.6.11 UK

- TABLE 124 UK: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 125 UK: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.3.6.13 By voltage

- TABLE 126 UK: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 127 UK: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.3.6.14 By installation

- TABLE 128 UK: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 129 UK: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.3.6.15 By end user

- TABLE 130 UK: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 131 UK: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.3.6.16 Russia

- 10.3.6.16.1 Rising investments in T&D sector and power plant infrastructure development to boost demand for circuit breakers

- 10.3.6.17 By insulation type

- 10.3.6.16 Russia

- TABLE 132 RUSSIA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 133 RUSSIA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.3.6.18 By voltage

- TABLE 134 RUSSIA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 135 RUSSIA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.3.6.19 By installation

- TABLE 136 RUSSIA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 137 RUSSIA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.3.6.20 By end user

- TABLE 138 RUSSIA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 139 RUSSIA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.3.6.21 Italy

- 10.3.6.21.1 Government initiatives toward green energy to stimulate demand for circuit breakers

- 10.3.6.22 By insulation type

- 10.3.6.21 Italy

- TABLE 140 ITALY: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 141 ITALY: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.3.6.23 By voltage

- TABLE 142 ITALY: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 143 ITALY: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.3.6.24 By installation

- TABLE 144 ITALY: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 145 ITALY: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.3.6.25 By end user

- TABLE 146 ITALY: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 147 ITALY: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.3.6.26 Rest of Europe

- 10.3.6.27 By insulation type

- TABLE 148 REST OF EUROPE: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 149 REST OF EUROPE: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.3.6.28 By voltage

- TABLE 150 REST OF EUROPE: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 151 REST OF EUROPE: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.3.6.29 By installation

- TABLE 152 REST OF EUROPE: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 153 REST OF EUROPE: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.3.6.30 By end user

- TABLE 154 REST OF EUROPE: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 155 REST OF EUROPE: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.4 NORTH AMERICA

- 10.4.1 IMPORT AND EXPORT DATA

- TABLE 156 NORTH AMERICA: IMPORT & EXPORT DATA FOR CIRCUIT BREAKER MARKET, 2019-2022 (USD MILLION)

- 10.4.2 BY INSULATION TYPE

- TABLE 157 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 158 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.4.3 BY VOLTAGE

- TABLE 159 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 160 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.4.4 BY INSTALLATION

- TABLE 161 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 162 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.4.5 BY END USER

- TABLE 163 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 164 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.4.6 BY COUNTRY

- TABLE 165 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 166 NORTH AMERICA: CIRCUIT BREAKER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.4.6.1 US

- 10.4.6.1.1 Pressing need to upgrade existing power infrastructure to drive market

- 10.4.6.2 By insulation type

- 10.4.6.1 US

- TABLE 167 US: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 168 US: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.4.6.3 By voltage

- TABLE 169 US: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 170 US: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.4.6.4 By installation

- TABLE 171 US: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 172 US: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.4.6.5 By end user

- TABLE 173 US: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 174 US: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.4.6.6 Canada

- 10.4.6.6.1 Growing investments in expanding T&D networks and upgrading existing infrastructure to accelerate market growth

- 10.4.6.7 By insulation type

- 10.4.6.6 Canada

- TABLE 175 CANADA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 176 CANADA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.4.6.8 By voltage

- TABLE 177 CANADA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 178 CANADA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.4.6.9 By installation

- TABLE 179 CANADA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 180 CANADA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.4.6.10 By end user

- TABLE 181 CANADA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 182 CANADA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.4.6.11 Mexico

- 10.4.6.11.1 Growing deployment of smart grids to drive market

- 10.4.6.12 By insulation type

- 10.4.6.11 Mexico

- TABLE 183 MEXICO: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 184 MEXICO: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.4.6.13 By voltage

- TABLE 185 MEXICO: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 186 MEXICO: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.4.6.14 By installation

- TABLE 187 MEXICO: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 188 MEXICO: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.4.6.15 By end user

- TABLE 189 MEXICO: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 190 MEXICO: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.5 SOUTH AMERICA

- 10.5.1 IMPORT AND EXPORT DATA

- TABLE 191 SOUTH AMERICA: IMPORT & EXPORT DATA FOR CIRCUIT BREAKER MARKET, 2019-2022 (USD MILLION)

- 10.5.2 BY INSULATION TYPE

- TABLE 192 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 193 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.5.3 BY VOLTAGE

- TABLE 194 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 195 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.5.4 BY INSTALLATION

- TABLE 196 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 197 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.5.5 BY END USER

- TABLE 198 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 199 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.5.6 BY COUNTRY

- TABLE 200 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 201 SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.5.6.1 Brazil

- 10.5.6.1.1 Increasing requirement to modernize existing power infrastructure to drive market

- 10.5.6.2 By insulation type

- 10.5.6.1 Brazil

- TABLE 202 BRAZIL: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 203 BRAZIL: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.5.6.3 By voltage

- TABLE 204 BRAZIL: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 205 BRAZIL: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.5.6.4 By installation

- TABLE 206 BRAZIL: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 207 BRAZIL: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.5.6.5 By end user

- TABLE 208 BRAZIL: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 209 BRAZIL: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.5.6.6 Argentina

- 10.5.6.6.1 Significant investments in renewable sector to boost demand for circuit breakers

- 10.5.6.7 By insulation type

- 10.5.6.6 Argentina

- TABLE 210 ARGENTINA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 211 ARGENTINA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.5.6.8 By voltage

- TABLE 212 ARGENTINA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 213 ARGENTINA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.5.6.9 By installation

- TABLE 214 ARGENTINA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 215 ARGENTINA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.5.6.10 By end user

- TABLE 216 ARGENTINA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 217 ARGENTINA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.5.6.11 Rest of South America

- 10.5.6.12 By insulation type

- TABLE 218 REST OF SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD THOUSAND)

- TABLE 219 REST OF SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD THOUSAND)

- 10.5.6.13 By voltage

- TABLE 220 REST OF SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD THOUSAND)

- TABLE 221 REST OF SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD THOUSAND)

- 10.5.6.14 By installation

- TABLE 222 REST OF SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD THOUSAND)

- TABLE 223 REST OF SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD THOUSAND)

- 10.5.6.15 By end user

- TABLE 224 REST OF SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD THOUSAND)

- TABLE 225 REST OF SOUTH AMERICA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD THOUSAND)

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 IMPORT AND EXPORT DATA

- TABLE 226 MIDDLE EAST & AFRICA: IMPORT & EXPORT DATA FOR CIRCUIT BREAKER MARKET, 2019-2022 (USD MILLION)

- 10.6.2 BY INSULATION TYPE

- TABLE 227 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 228 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.6.3 BY VOLTAGE

- TABLE 229 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 230 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.6.4 BY INSTALLATION

- TABLE 231 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 232 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.6.5 BY END USER

- TABLE 233 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 234 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.6.6 BY COUNTRY

- TABLE 235 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 236 MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.6.6.1 Saudi Arabia

- 10.6.6.1.1 Increasing investments in power projects to drive market

- 10.6.6.2 By insulation type

- 10.6.6.1 Saudi Arabia

- TABLE 237 SAUDI ARABIA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 238 SAUDI ARABIA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.6.6.3 By voltage

- TABLE 239 SAUDI ARABIA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 240 SAUDI ARABIA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.6.6.4 By installation

- TABLE 241 SAUDI ARABIA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 242 SAUDI ARABIA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.6.6.5 By end user

- TABLE 243 SAUDI ARABIA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 244 SAUDI ARABIA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.6.6.6 UAE

- 10.6.6.6.1 Growing number of power projects focused on upgrading distribution networks to boost demand for circuit breakers

- 10.6.6.7 By insulation type

- 10.6.6.6 UAE

- TABLE 245 UAE: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 246 UAE: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.6.6.8 By voltage

- TABLE 247 UAE: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 248 UAE: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.6.6.9 By installation

- TABLE 249 UAE: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 250 UAE: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.6.6.10 By end user

- TABLE 251 UAE: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 252 UAE: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.6.6.11 South Africa

- 10.6.6.11.1 Significant efforts to build new power stations and replace aging equipment to boost demand for circuit breakers

- 10.6.6.12 By insulation type

- 10.6.6.11 South Africa

- TABLE 253 SOUTH AFRICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD THOUSAND)

- TABLE 254 SOUTH AFRICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD THOUSAND)

- 10.6.6.13 By voltage

- TABLE 255 SOUTH AFRICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD THOUSAND)

- TABLE 256 SOUTH AFRICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD THOUSAND)

- 10.6.6.14 By installation

- TABLE 257 SOUTH AFRICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD THOUSAND)

- TABLE 258 SOUTH AFRICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD THOUSAND)

- 10.6.6.15 By end user

- TABLE 259 SOUTH AFRICA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD THOUSAND)

- TABLE 260 SOUTH AFRICA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD THOUSAND)

- 10.6.6.16 Kuwait

- 10.6.6.16.1 Growing investments in enhancing renewable energy capacity to propel market

- 10.6.6.17 By insulation type

- 10.6.6.16 Kuwait

- TABLE 261 KUWAIT: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 262 KUWAIT: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.6.6.18 By voltage

- TABLE 263 KUWAIT: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 264 KUWAIT: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.6.6.19 By installation

- TABLE 265 KUWAIT: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 266 KUWAIT: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.6.6.20 By end user

- TABLE 267 KUWAIT: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 268 KUWAIT: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

- 10.6.6.21 Rest of Middle East & Africa

- 10.6.6.22 By insulation type

- TABLE 269 REST OF MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2020-2022 (USD MILLION)

- TABLE 270 REST OF MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY INSULATION TYPE, 2023-2028 (USD MILLION)

- 10.6.6.23 By voltage

- TABLE 271 REST OF MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2020-2022 (USD MILLION)

- TABLE 272 REST OF MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY VOLTAGE, 2023-2028 (USD MILLION)

- 10.6.6.24 By installation

- TABLE 273 REST OF MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 274 REST OF MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 10.6.6.25 By end user

- TABLE 275 REST OF MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 276 REST OF MIDDLE EAST & AFRICA: CIRCUIT BREAKER MARKET, BY END USER, 2023-2028 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 277 OVERVIEW OF KEY STRATEGIES ADOPTED BY TOP PLAYERS, 2019-2022

- 11.2 MARKET SHARE ANALYSIS OF TOP 5 PLAYERS

- FIGURE 37 SHARE OF MAJOR PLAYERS IN CIRCUIT BREAKER MARKET, 2022

- 11.3 MARKET EVALUATION FRAMEWORK

- TABLE 278 MARKET EVALUATION FRAMEWORK

- 11.4 FIVE-YEAR COMPANY REVENUE ANALYSIS

- FIGURE 38 FIVE-YEAR REVENUE ANALYSIS OF TOP PLAYERS IN CIRCUIT BREAKER MARKET, 2018-2022

- 11.5 EVALUATION MATRIX FOR KEY COMPANIES

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- FIGURE 39 COMPANY EVALUATION MATRIX, 2022

- 11.6 EVALUATION MATRIX FOR START-UPS

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 STARTING BLOCKS

- 11.6.4 DYNAMIC COMPANIES

- FIGURE 40 START-UP EVALUATION MATRIX, 2022

- 11.7 COMPETITIVE SCENARIO

- 11.7.1 PRODUCT LAUNCHES

- 11.7.2 DEALS

12 COMPANY PROFILES

- 12.1 ABB

- TABLE 279 ABB: COMPANY OVERVIEW

- FIGURE 41 ABB: COMPANY SNAPSHOT

- TABLE 280 ABB: PRODUCT LAUNCHES/DEVELOPMENTS

- 12.2 SIEMENS

- TABLE 281 SIEMENS LIMITED: COMPANY OVERVIEW

- FIGURE 42 SIEMENS: COMPANY SNAPSHOT

- TABLE 282 SIEMENS: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 283 SIEMENS: DEALS

- 12.3 EATON

- TABLE 284 EATON: COMPANY OVERVIEW

- FIGURE 43 EATON: COMPANY SNAPSHOT

- TABLE 285 EATON: PRODUCT LAUNCHES/DEVELOPMENTS

- 12.4 SCHNEIDER ELECTRIC

- TABLE 286 SCHNEIDER ELECTRIC: COMPANY OVERVIEW

- FIGURE 44 SCHNEIDER ELECTRIC: COMPANY SNAPSHOT

- TABLE 287 SCHNEIDER ELECTRIC: PRODUCT LAUNCHES/DEVELOPMENTS

- 12.5 MITSUBISHI ELECTRIC

- TABLE 288 MITSUBISHI ELECTRIC: COMPANY OVERVIEW

- FIGURE 45 MITSUBISHI ELECTRIC: COMPANY SNAPSHOT

- TABLE 289 MITSUBISHI ELECTRIC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 290 MITSUBISHI ELECTRIC: DEALS

- 12.6 TOSHIBA CORPORATION

- TABLE 291 TOSHIBA CORPORATION: COMPANY OVERVIEW

- FIGURE 46 TOSHIBA: COMPANY SNAPSHOT

- TABLE 292 TOSHIBA CORPORATION: DEALS

- 12.7 POWELL INDUSTRIES

- TABLE 293 POWELL INDUSTRIES: COMPANY OVERVIEW

- FIGURE 47 POWELL INDUSTRIES: COMPANY SNAPSHOT

- 12.8 CG POWER AND INDUSTRIAL SOLUTIONS

- TABLE 294 CG POWER: COMPANY OVERVIEW

- FIGURE 48 CG POWER: COMPANY SNAPSHOT

- TABLE 295 CG POWER: DEALS

- 12.9 FUJI ELECTRIC

- TABLE 296 FUJI ELECTRIC: COMPANY OVERVIEW

- FIGURE 49 FUJI ELECTRIC: COMPANY SNAPSHOT

- TABLE 297 FUJI ELECTRIC: PRODUCT LAUNCHES/DEVELOPMENTS

- 12.10 CHINT ELECTRICS CO., LTD.

- TABLE 298 CHINT ELECTRICS CO., LTD.: COMPANY OVERVIEW

- 12.11 BRUSH GROUP

- TABLE 299 BRUSH GROUP: COMPANY OVERVIEW

- 12.12 TAVRIDA ELECTRIC

- TABLE 300 TAVRIDA ELECTRIC: COMPANY OVERVIEW

- TABLE 301 TAVRIDA ELECTRIC: DEALS

- 12.13 SECHERON

- TABLE 302 SECHERON: COMPANY OVERVIEW

- 12.14 EFACEC POWER SOLUTIONS

- TABLE 303 EFACEC POWER SOLUTIONS: COMPANY OVERVIEW

- 12.15 HYUNDAI ELECTRIC

- TABLE 304 HYUNDAI ELECTRIC: COMPANY OVERVIEW

- FIGURE 50 HYUNDAI ELECTRIC: COMPANY SNAPSHOT

- 12.16 TE CONNECTIVITY

- TABLE 305 TE CONNECTIVITY: COMPANY OVERVIEW

- FIGURE 51 TE CONNECTIVITY: COMPANY SNAPSHOT

- 12.17 ENTEC ELECTRIC & ELECTRONIC

- TABLE 306 ENTEC ELECTRIC & ELECTRONIC: COMPANY OVERVIEW

- 12.18 LS ELECTRIC

- 12.19 SCHALTBAU

- 12.20 KIRLOSKAR ELECTRIC

- 12.21 YUEQING AISO ELECTRIC

- 12.22 SRIWIN ELECTRIC

- 12.23 ORECCO

- 12.24 ORMAZABAL

- 12.25 YUEQING LIYOND ELECTRIC

- 12.26 SAFVOLT SWITCHGEARS

- *Details on Business overview, Products/solutions/services offered, Recent Developments, MNM view might not be captured in case of unlisted companies.

13 APPENDIX

- 13.1 INSIGHTS FROM INDUSTRY EXPERTS

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 CUSTOMIZATION OPTIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS