接着剤およびシーリング剤市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Adhesives and Sealants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801933

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

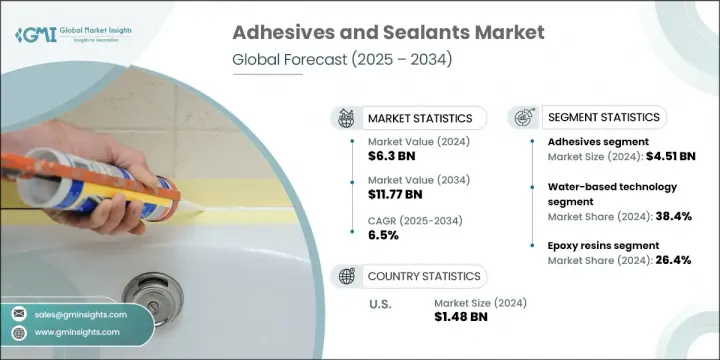

接着剤およびシーリング剤の世界市場規模は、2024年に63億米ドルとなり、CAGR 6.5%で成長し、2034年には117億7,000万米ドルに達すると予測されています。

この市場は、複数の産業にわたる製品の強度、寿命、耐性を高める接着・シーリング材料の開発と使用を中心に展開されています。これらの材料は、建設、自動車、電子機器、包装などの用途で重要な役割を果たし、天候、漏出、外部汚染物質からの保護を提供します。インフラの近代化と軽量でエネルギー効率の高い自動車への世界の後押しにより、需要は加速し続けています。

性能、環境適合性、材料の汎用性に焦点を当てた革新は、製品の信頼性と効率を向上させながら、メーカーが進化する業界標準を満たすのに役立っています。各社は、過酷な条件下でより強力な接着を実現し、化学物質や温度変動に耐え、硬化時間を短縮してより迅速な組立工程をサポートする、高度な接着剤やシーラントの処方を開発する傾向を強めています。こうした改良は作業効率を高めるだけでなく、最終製品のライフサイクルを延長します。同時に、環境に優しいソリューションの推進により、世界の持続可能性目標に沿った低VOC、バイオベース、リサイクル可能な材料へのシフトが進んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 63億米ドル |

| 予測金額 | 117億7,000万米ドル |

| CAGR | 6.5% |

接着剤分野は2024年に45億1,000万米ドルを占め、2034年まで6.5%のCAGRを維持すると予測されます。エポキシやポリウレタンなどの構造用接着剤は、自動車や航空宇宙用途で優れた接着性を発揮するため、市場をリードしています。接着剤分野には、感圧接着剤、ホットメルト、溶剤型と水性型があります。

技術の中では、水性接着剤セグメントが2024年に38.4%のシェアを占め、持続可能な低VOC製品の台頭がその原動力となっています。より安全な塗布と環境適合性により、家具、自動車、包装、建築分野での採用が増加しています。メーカーが大気質規制への適合を目指すなか、水性接着剤は産業用と商業用の両方で引き続き人気を集めています。

米国接着剤およびシーリング剤市場は88.5%のシェアを占め、2024年には14億8,000万米ドルを創出しました。米国市場は、先端製造業、EV生産、国家インフラのアップグレードへの旺盛な投資に支えられ、2034年まで継続的な成長が見込まれています。交通網と公共建築物を対象とした連邦政府の資金援助イニシアティブが、高性能接着剤とシーリング製品の需要を押し上げています。さらに、航空宇宙、エレクトロニクス、持続可能な建設の台頭が、接着技術の主要市場としての同国の役割を強化しています。

接着剤およびシーリング剤の世界市場における有力企業には、BASF SE、Dow Inc.、Henkel AG &Co.KGaA、Sika AG、3M Companyなどです。接着剤およびシーリング剤業界の主要企業は、的を絞った研究開発投資、環境に優しい製品開拓、地域拡大を通じて市場での地位を高めています。環境規制や消費者の持続可能性への要求に対応するため、低VOCやバイオベースの接着剤への戦略的シフトが進んでいます。企業は、リードタイムを短縮し業務効率を高めるため、サプライチェーンを強化し、高成長地域における製造能力を拡大しています。戦略的な合併、買収、パートナーシップは、より幅広い製品ポートフォリオと市場参入を可能にしています。電気自動車、電子機器、スマートインフラに合わせたカスタム接着剤ソリューションも注目されており、次世代産業の需要に応えています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 軽量製造への移行

- グリーンビルディングと環境に優しい配合

- eモビリティとエレクトロニクスの成長

- 包装の革新と安全要件

- 業界の潜在的リスク&課題

- 環境と規制の圧力

- 原材料価格の変動

- 市場機会

- 持続可能でバイオベースの代替品の需要

- モジュール式およびプレハブ式建設の増加

- 拡大するヘルスケア・医療機器市場

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 接着剤市場

- 構造用接着剤

- エポキシ接着剤

- ポリウレタン接着剤

- アクリル系接着剤

- メチルメタクリレート接着剤

- シアノアクリレート接着剤

- 感圧接着剤

- アクリルPSA

- ゴム系PSA

- シリコン粘着剤

- ホットメルト接着剤

- EVAホットメルト

- ポリアミドホットメルト

- ポリオレフィンホットメルト

- 反応性ホットメルト

- 水性接着剤

- 溶剤系接着剤

- その他の接着剤の種類

- 構造用接着剤

- シーラント市場

- シリコンシーラント

- RTVシリコーンシーラント

- 構造用ガラスシーラント

- ポリウレタンシーラント

- アクリルシーラント

- ポリサルファイドシーラント

- ブチルシーラント

- その他のシーラントの種類

- シリコンシーラント

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 水性の技術

- 溶剤系の技術

- ホットメルト技術

- 反応型技術

- UV/光硬化技術

- 圧力感知技術

- その他

第7章 市場推計・予測:樹脂タイプ別、2021年~2034年

- 主要動向

- エポキシ樹脂

- ポリウレタン樹脂

- アクリル樹脂

- シリコーン樹脂

- ポリ酢酸ビニル(PVA)

- エチレン酢酸ビニル(EVA)

- スチレン系ブロック共重合体

- その他

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 構造結合

- 組立作業

- シーリングとガスケット

- 表面保護

- 電気絶縁

- 熱管理

- 振動減衰

- その他

第9章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 建築・建設

- 住宅建設

- 商業建設

- インフラプロジェクト

- 自動車および輸送

- 乗用車

- 商用車

- 電気自動車

- アフターマーケット

- パッケージ

- 軟質包装

- 硬質包装

- ラベルとテープ

- 電子・電気

- コンシューマーエレクトロニクス

- 半導体パッケージング

- PCBアセンブリ

- ディスプレイ技術

- 航空宇宙および防衛

- 商用航空

- 軍事用途

- 宇宙用途

- 医療とヘルスケア

- 医療機器

- 外科手術用途

- 医薬品包装

- 履物と革製品

- 木工と家具

- 海洋用途

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- 3M Company

- Arkema Group(Bostik)

- Ashland Global Holdings Inc.

- Avery Dennison Corporation

- BASF SE

- Dow Inc.

- DuPont de Nemours, Inc.

- H.B. Fuller Company

- Henkel AG &Co. KGaA

- Huntsman Corporation

- Illinois Tool Works Inc.(ITW)

- Momentive Performance Materials Inc.

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

目次

The Global Adhesives and Sealants Market was valued at USD 6.3 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 11.77 billion by 2034. This market revolves around the development and use of bonding and sealing materials that enhance the strength, longevity, and resistance of products across multiple industries. These materials play a key role in construction, automotive, electronics, and packaging applications, where they provide protection against weather, leakage, and external contaminants. With the global push toward infrastructure modernization and lightweight, energy-efficient vehicles, demand continues to accelerate.

Innovations focused on performance, eco-compliance, and material versatility are helping manufacturers meet evolving industry standards while improving product reliability and efficiency. Companies are increasingly developing advanced adhesive and sealant formulations that deliver stronger bonding under extreme conditions, resist chemicals and temperature fluctuations, and reduce cure times to support faster assembly processes. These improvements not only boost operational efficiency but also extend the lifecycle of end-use products. Simultaneously, the push for eco-friendly solutions is driving the shift toward low-VOC, bio-based, and recyclable materials that align with global sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.3 Billion |

| Forecast Value | $11.77 Billion |

| CAGR | 6.5% |

The adhesives segment accounted for USD 4.51 billion in 2024 and is expected to maintain a strong CAGR of 6.5% through 2034. Structural adhesives such as epoxy and polyurethane lead the market due to their superior bonding in automotive and aerospace applications. The adhesives segment includes pressure-sensitive adhesives, hot melts, and both solvent- and water-based variants.

Among technologies, the water-based adhesives segment held 38.4% share in 2024, driven by the rise of sustainable, low-VOC products. Their safer application and environmental compatibility have increased adoption across furniture, automotive, packaging, and construction sectors. As manufacturers aim to align with air quality regulations, water-based adhesives continue to gain popularity for both industrial and commercial applications.

United States Adhesives and Sealants Market held an 88.5% share and generated USD 1.48 billion in 2024. The U.S. market is set for continued growth through 2034, supported by robust investments in advanced manufacturing, EV production, and national infrastructure upgrades. Federal funding initiatives targeting transportation networks and public buildings are boosting the demand for high-performance adhesive and sealing products. Additionally, the rise of aerospace, electronics, and sustainable construction is reinforcing the country's role as a key market for adhesive technologies.

Prominent players in the Global Adhesives and Sealants Market include BASF SE, Dow Inc., Henkel AG & Co. KGaA, Sika AG, and 3M Company. Major companies in the adhesives and sealants industry are enhancing their market position through targeted R&D investments, eco-friendly product development, and regional expansion. There's a strategic shift toward low-VOC and bio-based adhesives to address environmental regulations and consumer sustainability demands. Companies are strengthening supply chains and expanding manufacturing capabilities in high-growth regions to reduce lead times and boost operational efficiency. Strategic mergers, acquisitions, and partnerships are enabling broader product portfolios and market access. Custom adhesive solutions tailored for electric vehicles, electronics, and smart infrastructure are also a focus, helping meet next-gen industrial demands.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Technology

- 2.2.4 Resin type

- 2.2.5 Application

- 2.2.6 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward lightweight manufacturing

- 3.2.1.2 Green building and eco-friendly formulations

- 3.2.1.3 Growth of e-mobility and electronics

- 3.2.1.4 Packaging innovation and safety requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental and regulatory pressure

- 3.2.2.2 Raw material price volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Demand for sustainable and bio-based alternatives

- 3.2.3.2 Rise in modular and prefabricated construction

- 3.2.3.3 Expanding healthcare and medical devices market

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Adhesives market

- 5.2.1 Structural adhesives

- 5.2.1.1 Epoxy adhesives

- 5.2.1.2 Polyurethane adhesives

- 5.2.1.3 Acrylic adhesives

- 5.2.1.4 Methyl methacrylate adhesives

- 5.2.1.5 Cyanoacrylate adhesives

- 5.2.2 Pressure sensitive adhesives

- 5.2.2.1 Acrylic PSA

- 5.2.2.2 Rubber-based PSA

- 5.2.2.3 Silicone PSA

- 5.2.3 Hot melt adhesives

- 5.2.3.1 EVA hot melts

- 5.2.3.2 Polyamide hot melts

- 5.2.3.3 Polyolefin hot melts

- 5.2.3.4 Reactive hot melts

- 5.2.4 Water-based adhesives

- 5.2.5 Solvent-based adhesives

- 5.2.6 Other adhesive types

- 5.2.1 Structural adhesives

- 5.3 Sealants market

- 5.3.1 Silicone sealants

- 5.3.1.1 RTV silicone sealants

- 5.3.1.2 Structural glazing sealants

- 5.3.2 Polyurethane sealants

- 5.3.3 Acrylic sealants

- 5.3.4 Polysulfide sealants

- 5.3.5 Butyl sealants

- 5.3.6 Other sealant types

- 5.3.1 Silicone sealants

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Water-based technology

- 6.3 Solvent-based technology

- 6.4 Hot melt technology

- 6.5 Reactive technology

- 6.6 UV/light curable technology

- 6.7 Pressure sensitive technology

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Resin Type, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Epoxy resins

- 7.3 Polyurethane resins

- 7.4 Acrylic resins

- 7.5 Silicone resins

- 7.6 Polyvinyl acetate (PVA)

- 7.7 Ethylene vinyl acetate (EVA)

- 7.8 Styrenic block copolymers

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Structural bonding

- 8.3 Assembly operations

- 8.4 Sealing and gasketing

- 8.5 Surface protection

- 8.6 Electrical insulation

- 8.7 Thermal management

- 8.8 Vibration damping

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Building and construction

- 9.2.1 Residential construction

- 9.2.2 Commercial construction

- 9.2.3 Infrastructure projects

- 9.3 Automotive and transportation

- 9.3.1 Passenger vehicles

- 9.3.2 Commercial vehicles

- 9.3.3 Electric vehicles

- 9.3.4 Aftermarket

- 9.4 Packaging

- 9.4.1 Flexible packaging

- 9.4.2 Rigid packaging

- 9.4.3 Labels and tapes

- 9.5 Electronics and electrical

- 9.5.1 Consumer electronics

- 9.5.2 Semiconductor packaging

- 9.5.3 PCB assembly

- 9.5.4 Display technologies

- 9.6 Aerospace and defense

- 9.6.1 Commercial aviation

- 9.6.2 Military applications

- 9.6.3 Space applications

- 9.7 Medical and healthcare

- 9.7.1 Medical devices

- 9.7.2 Surgical applications

- 9.7.3 Pharmaceutical packaging

- 9.8 Footwear and leather

- 9.9 Woodworking and furniture

- 9.10 Marine applications

- 9.11 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 3M Company

- 11.2 Arkema Group (Bostik)

- 11.3 Ashland Global Holdings Inc.

- 11.4 Avery Dennison Corporation

- 11.5 BASF SE

- 11.6 Dow Inc.

- 11.7 DuPont de Nemours, Inc.

- 11.8 H.B. Fuller Company

- 11.9 Henkel AG & Co. KGaA

- 11.10 Huntsman Corporation

- 11.11 Illinois Tool Works Inc. (ITW)

- 11.12 Momentive Performance Materials Inc.

- 11.13 RPM International Inc.

- 11.14 Sika AG

- 11.15 Wacker Chemie AG

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日