スマートメーターの市場機会、成長促進要因、産業動向分析、2025年~2034年の予測

Smart Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801893

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

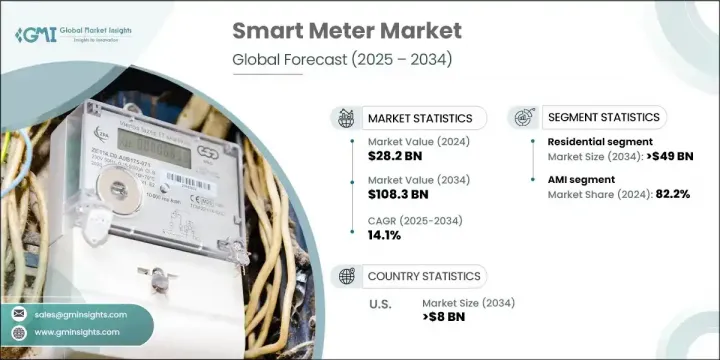

世界のスマートメーター市場は、2024年に282億米ドルと評価され、CAGR 14.1%で成長し、2034年には1,083億米ドルに達すると推定されています。

この著しい成長は、規制当局の支援の高まり、計測技術の継続的な革新、持続可能なエネルギー使用に対する消費者の関心の高まりによって後押しされています。デジタル化が進み、エネルギー事情が再構築される中、スマートメーターはエネルギー管理システムの中心的な要素になりつつあります。これらの機器は、電力、ガス、水道の消費データをリアルタイムで取得し、その情報を電力会社に直接送信することで、業務効率と請求精度を向上させています。

多くの経済圏で、国家送電網のアップグレードを目的とした政府の支援プログラムにより、スマートメーターは近代化戦略の中核に位置づけられています。スマートグリッドへの移行は、信頼性の向上だけでなく、クリーンエネルギーの統合や送電ロスの最小化にもつながります。二酸化炭素排出量の削減とエネルギーの透明性の向上がより重視される中、電力会社は従来のメーターを、双方向通信とリアルタイム分析を実現するインテリジェントシステムに急速に置き換えつつあります。グリッドの最適化、省エネルギー、消費者のエンパワーメントの優先順位が高まるにつれて、住宅、商業、工業の各分野でスマートメーター市場は勢いを増しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 282億米ドル |

| 予測金額 | 1,083億米ドル |

| CAGR | 14.1% |

住宅部門は、家庭用エネルギーインフラを近代化するための広範な政府の取り組みに支えられ、2034年までに490億米ドルに達すると予測されます。エネルギー効率と環境責任に対する一般消費者の意識の高まりも、消費者がスマートメーターソリューションを採用することに影響を与えています。これらのデジタルメーターにより、ユーザーはリアルタイムのデータにアクセスできるようになり、エネルギー消費をより適切に管理できるようになり、持続可能な生活を支援しながら光熱費を削減できるようになります。需要側管理と省エネルギープログラムが定着しつつある中、住宅用アプリケーションセグメントは依然として成長の最前線にあります。

高度計測インフラ(AMI)の2024年のシェアは82.2%で、その幅広い機能が牽引しています。AMIは、電力会社とエンドユーザー間のリアルタイムの双方向データ通信を可能にし、エネルギーの最適化と送電網の信頼性に不可欠なものとなっています。遠隔検針、ダイナミックプライシング、ロードバランシング、迅速な故障検知などの機能を通じて、AMIはエネルギー供給事業者が需要の変化に積極的に対応することを可能にします。これらのシステムはまた、スマートホームや消費者レベルのエネルギーダッシュボードと簡単に統合でき、透明性を高め、効率的なエネルギー行動を促します。

米国スマートメーター市場は2034年までに80億米ドルに達し、産業と住宅のアップグレードが寄与します。米国では、エネルギー需要の増加と再生可能エネルギー源の割合の増加に対応するため、送電網インフラの強化が進められています。規制措置により、高度な監視・管理ツールが求められており、スマートメーターは重要なインフラとして位置づけられています。さらに、スマートメーターはエネルギー集約的なセクターで採用が進んでおり、業務効率、コンプライアンス、供給の信頼性にさらなる付加価値をもたらしています。

世界のスマートメーター市場をリードする有力企業には、シーメンス、シュナイダーエレクトリック、イトロン、ハネウェルインターナショナル、ランディス+ギアなどがあります。スマートメーター業界の主要企業は、技術革新、戦略的提携、地域拡大を組み合わせることで、市場でのポジショニングを強化しています。研究開発への投資は引き続き重要な役割を果たしており、各社はAI、IoT、クラウドベースのアナリティクスを統合した次世代メーターの開発に注力しています。また、大手企業は電力会社や政府とパートナーシップを結び、長期的な展開契約を獲得しています。増大する需要に対応するため、企業は生産能力を拡大し、戦略的地域における製造の現地化を進めています。さらに、顧客価値と運用信頼性を高めるために、エネルギーに関する洞察、遠隔診断、予知保全を提供するソフトウェアプラットフォームを含めることで、サービス提供を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 輸出入貿易分析

- 価格動向分析:地域別

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

- 新たな機会と動向

- デジタル化とIoTの統合

- 新興市場への浸透

- 投資分析と将来展望

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 戦略的取り組み

- 競合ベンチマーキングの描写

- 戦略ダッシュボード

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- ユーティリティ

第6章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- AMI

- AMR

第7章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- スマートガス

- スマートウォーター

- スマート電気

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スウェーデン

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

第9章 企業プロファイル

- Apator SA

- ABB

- AEM

- Aclara Technologies LLC

- ARAD Group

- B Meters Metering Solutions

- Badger Meter, Inc.

- Chint Group

- General Electric

- Honeywell International, Inc.

- Itron, Inc.

- Iskraemeco Group

- Kamstrup

- Larsen &Toubro Limited

- Landis+Gyr

- Ningbo Water Meter Co., Ltd.

- Osaki Electric Co., Ltd.

- Raychem RPG Private Limited

- Schneider Electric SE

- Siemens

- Sensus

- Sontex SA

- Wasion Group

目次

The Global Smart Meter Market was valued at USD 28.2 billion in 2024 and is estimated to grow at a CAGR of 14.1% to reach USD 108.3 billion by 2034. This remarkable growth is being fueled by rising regulatory support, continued innovation in metering technologies, and growing consumer focus on sustainable energy usage. As digitalization continues to reshape the energy landscape, smart meters are becoming a central component of energy management systems. These devices capture real-time consumption data for electricity, gas, or water, transmitting the information directly to utilities for improved operational efficiency and billing accuracy.

Across many economies, government-backed programs aimed at upgrading national grids are placing smart meters at the core of their modernization strategies. The transition to smart grids is not only about enhancing reliability but also about integrating clean energy and minimizing transmission losses. With greater emphasis on reducing carbon footprints and improving energy transparency, utility providers are rapidly replacing conventional meters with intelligent systems that deliver two-way communication and real-time analytics. As grid optimization, energy conservation, and consumer empowerment rise in priority, the smart meter market continues to gain momentum across residential, commercial, and industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $28.2 Billion |

| Forecast Value | $108.3 Billion |

| CAGR | 14.1% |

The residential sector is projected to reach USD 49 billion by 2034, supported by widespread government efforts to modernize household energy infrastructure. Increasing public awareness of energy efficiency and environmental responsibility is also influencing consumers to adopt smart metering solutions. These digital meters allow users to access real-time data, offering better control over energy consumption and helping reduce utility bills while supporting sustainable living. With demand-side management and energy-saving programs gaining ground, the residential application segment remains at the forefront of growth.

The advanced metering infrastructure (AMI) held an 82.2% share in 2024, driven by its wide functionality. AMI enables real-time, bidirectional data communication between utility companies and end users, making it essential for energy optimization and grid reliability. Through features such as remote meter reading, dynamic pricing, load balancing, and quick fault detection, AMI allows energy providers to respond proactively to changes in demand. These systems also integrate easily with smart homes and consumer-level energy dashboards, boosting transparency and encouraging efficient energy behaviors.

U.S. Smart Meter Market will reach USD 8 billion by 2034, with contributions coming from industrial and residential upgrades. The country is strengthening its grid infrastructure to handle growing energy demands and a higher share of variable renewable sources. Regulatory actions are pushing for advanced monitoring and management tools, positioning smart meters as critical infrastructure. Additionally, smart meters are seeing adoption in energy-intensive sectors, adding further value to operational efficiency, compliance, and supply reliability.

Prominent players leading the Global Smart Meter Market include Siemens, Schneider Electric, Itron, Honeywell International, and Landis + Gyr. Major companies in the smart meter industry are enhancing their market positioning through a mix of innovation, strategic alliances, and regional expansion. Investments in R&D continue to play a key role, with companies focusing on developing next-generation meters that integrate AI, IoT, and cloud-based analytics. Leading firms are also forming partnerships with utility providers and governments to win long-term deployment contracts. To meet growing demand, businesses are expanding production capabilities and localizing manufacturing in strategic regions. Furthermore, they are strengthening their service offerings by including software platforms that provide energy insights, remote diagnostics, and predictive maintenance to enhance customer value and operational reliability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Import/Export trade analysis

- 3.4 Price trend analysis, by region (USD/Unit)

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Residential

- 5.3 Commercial

- 5.4 Utility

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 AMI

- 6.3 AMR

Chapter 7 Market Size and Forecast, By Product, 2021 - 2034 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Smart gas

- 7.3 Smart water

- 7.4 Smart electric

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 South Africa

- 8.5.4 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 Apator SA

- 9.2 ABB

- 9.3 AEM

- 9.4 Aclara Technologies LLC

- 9.5 ARAD Group

- 9.6 B Meters Metering Solutions

- 9.7 Badger Meter, Inc.

- 9.8 Chint Group

- 9.9 General Electric

- 9.10 Honeywell International, Inc.

- 9.11 Itron, Inc.

- 9.12 Iskraemeco Group

- 9.13 Kamstrup

- 9.14 Larsen & Toubro Limited

- 9.15 Landis + Gyr

- 9.16 Ningbo Water Meter Co., Ltd.

- 9.17 Osaki Electric Co., Ltd.

- 9.18 Raychem RPG Private Limited

- 9.19 Schneider Electric SE

- 9.20 Siemens

- 9.21 Sensus

- 9.22 Sontex SA

- 9.23 Wasion Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日