|

|

市場調査レポート

商品コード

1644772

欧州のスマートメーター-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Smart Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のスマートメーター-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

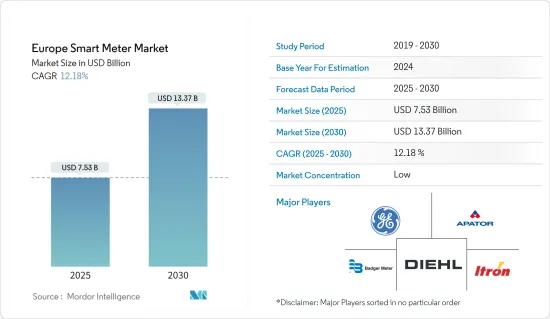

欧州のスマートメーター市場規模は2025年に75億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは12.18%で、2030年には133億7,000万米ドルに達すると予測されます。

スマートグリッドプロジェクトに対する意識の高まり、都市化の進展、政府による支援的な規制が、欧州における調査対象市場の成長を促進する主要要因として引き続き期待されています。

主要ハイライト

- スマートメーターは、消費者と供給者の双方向通信機能により、光熱費の使用状況をリアルタイムで追跡できるほか、供給者による遠隔地での検針/供給開始/停止を容易にするため、ガス、電力、水道などさまざまな配備に採用されています。さらに、スマートメーターの導入は、ホームエネルギーマネジメントシステム(HEMS)やビルエネルギーマネジメントシステム(BEMS)の導入も可能にし、各家庭やビル全体の電力使用量の可視化を可能にします。

- ここ数年、欧州各国でスマートメーターの普及が進み、従来の一般メーターに代わってスマートメーターが導入され、送電網の移行に貢献しています。さらに、スマートメーターは、プロバイダーによる自動検針だけでなく、消費者が自分の消費量を認識できるようにするためにも活用されています。IoT通信のための新しい無線技術の迅速な開発は、欧州のスマートメーター市場に大きな影響を与えています。

- 英国政府の発表によると、2022年9月末現在、英国の家庭や中小企業には約3,030万台のスマートメーターや高度メーターが設置されています。さらに、現在では全メーターの約54%がスマートメーターまたは高度メーターであり、2,650万台がスマートモードで稼働しています。

- さらに、デジタル化によってエネルギー効率化対策も近代化・加速化しています。そのため、欧州ではスマートグリッドの導入が急増しています。スマートグリッドは、供給を動的に最適化し、太陽光発電などの再生可能エネルギー源から大量の電力を供給するのに有効だからです。

- しかし、スマートメーターの設置に伴うコストの高さ、セキュリティ上の懸念の高まり、インフラ設置のための設備投資の不足が、予測期間中の市場の成長を妨げています。

欧州のスマートメーター市場動向

スマートグリッドプロジェクトへの投資の増加が市場成長を牽引する見込み

- 欧州の電力需要は、今後数十年で大幅に増加すると予測されています。例えば、IEAによると、欧州の電力需要は2019~2025年の間に40TWh増加すると予測されています。そのため、電力インフラの近代化、拡大、デジタル化、分散化による回復力の向上と計画的な投資が、同地域のいくつかの市場力学を変化させると予想されます。

- 欧州の公益事業者は、デジタルツインや人工知能のような技術を採用し、政府の支援やイニシアチブの急増と相まって、スマートグリッドプロジェクトへの投資を誘致しています。例えば、エネルギー危機が続く中、ドイツのエネルギー部門に関する省は、連邦政府が資金提供する省エネルギー効果の高いイニシアチブの採用を促進する措置を導入しました。新しい措置では、ベンダーは資金提供の申請書を提出後、直接プロジェクトの実施を開始することができます。

- スマートメーターの導入は、GPRS技術を通じてDISCOMと消費者間の双方向リアルタイム通信を容易にすることで、スマートグリッドへの道を開くものであり、未来対応技術の適切な指標となります。

- 欧州諸国が再生可能エネルギー発電能力の強化にますます注力していることも、この地域のスマートグリッドインフラの開発に貢献しています。2023年までに、フランスの再生可能エネルギーの発電容量は70ギガワットを超えます。水力発電の導入量は再生可能エネルギーの中で最も多く、26ギガワット近くに達しました。設置容量の約24ギガワットは風力発電によるもので、そのほとんどは陸上発電所に設置されています。

大きな市場シェアを占める英国

- 従来の電力・ガスメーターをスマートメーターに置き換えることは、英国にとって重要な国家インフラのアップグレードであり、この地域のエネルギーシステムをより安く、よりクリーンで、より信頼性の高いものにすると期待されています。英国政府によると、2022年9月末時点で、英国全土の家庭や中小企業には約3,030万台のスマートメーターや高度メーターが設置されています。

- さらに、2022年9月末現在、英国全土の家庭用物件で、合計2,380万個のガスメーターと2,880万個の電力メーターが大手エネルギー供給会社によって運用されています。また、2022年9月末時点で、大手エネルギー供給会社によって運用されている家庭用ガスメーターの43%、家庭用電力メーターの50%がスマート化されています。同様に、地域全体の非家庭用サイトでは、ガスメーターよりも電力メーターの方がスマートモードまたはアドバンストモードで稼働している割合が高い(48%対37%)。

- さらに、エネルギー価格の高騰に伴い、この地域の多くの家庭は、ガスや電気の使用量をリアルタイムでモニタリングし、重要な点として、その使用料がいくらかかっているかを把握しようとしており、スマートメーターの普及に拍車をかけています。例えば、英国議会によると、家庭のエネルギー料金は2022年4月に54%上昇し、2022年10月には80%上昇すると予想されています。

- さらに、同地域におけるスマートメーターの普及を促進するために実施されているさまざまな規制が、市場の成長にさらに貢献しています。例えば、2022年1月から、この地域のすべてのガス・電力供給会社は、2025年末までにスマートメーター以外の残りの顧客にもスマートメーターや先進的メーターを普及させるという拘束力のある年間設置目標を掲げています。

欧州のスマートメーター産業概要

欧州のスマートメーター市場は競争が激しく、国内外の参入企業が活躍しています。市場が拡大し、より多くの機会がもたらされることが予想されるため、予測期間中に競合情勢を細分化し、より多くの参入企業がすぐに市場に参入すると考えられます。同市場の主要企業には、Elster Group GmbH、Diehl Stiftung &Co.KGなどがあります。

2023年2月、スウェーデンのIoT事業者であるNetmoreは、スマート水道メーターやその他の大規模IoTと公益事業プロジェクトを対象に、フランスでLoRaWANネットワークの展開を開始しました。NetmoreのLoRaWANインフラは現在、英国、スウェーデン、アイルランド、オランダ、フランス、スペインで利用可能だといいます。

2023年1月、ドイツ政府はエネルギー転換のデジタル化を再開し、スマートメーターの展開を加速するための法律案の採択を発表しました。同政府によると、同法は2023年春に発効する見込みで、大規模なスマートメーター普及が直ちに開始され、2025年には義務化されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- スマートグリッドプロジェクトへの投資の増加

- スマートシティ展開の成長

- 政府による規制強化

- 市場課題/抑制要因

- 高コストとセキュリティへの懸念

- スマートメーターとの統合の難しさ

第6章 市場セグメンテーション

- メータータイプ別(売上高と出荷台数)

- スマートガスメーター

- スマート水道メーター

- スマート電力メーター

- エンドユーザー別

- 住宅用

- 商業用

- 産業用

- ***国別(売上高と出荷台数)

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

第7章 競合情勢

- 企業プロファイル

- General Electric Company

- Apator SA

- Badger Meter Inc.

- Diehl Stiftung & Co. KG

- Elster Group GmbH(Honeywell International Inc)

- AEM

- Itron Inc

- Kamstrup A/S

- Landis+GYR Group AG

- Arad Group

- Ningbo Sanxing Electric Co. Ltd.

- Sensus(Xylem Inc.)

- Zenner International GmbH & Co. KG

第8章 投資分析

第9章 市場の将来

The Europe Smart Meter Market size is estimated at USD 7.53 billion in 2025, and is expected to reach USD 13.37 billion by 2030, at a CAGR of 12.18% during the forecast period (2025-2030).

The growing awareness for smart grid projects, increasing urbanization, and supportive government regulations are expected to remain among the major factors driving the studied market's growth in Europe.

Key Highlights

- Smart meters are being adopted in the region for different deployments, such as gas, electricity, and water, owing to their two-way communication feature, which facilitates real-time tracking of utility usage by both consumer and utility supplier and also facilitates reading/start/cutoff of supply remotely by the supplier. Additionally, the deployment of a smart meter also allows the implementation of a Home Energy Management System (HEMS) or Building Energy Management System (BEMS), allowing visualization of the electric power usage in every home or entire building.

- During the past few years, smart metering rollouts have taken place in various European countries, with smart meters replacing traditional regular meters, thus contributing to the grid transition. Moreover, smart meters are utilized not only for automatic readings by the provider but also for empowering the consumer to be aware of their consumption. The swift development of new wireless technologies for IoT communications has a significant impact on the smart metering market in Europe.

- As per the government of the UK, at the end of September 2022, there were about 30.3 million smart and advanced meters in homes and small businesses in Great Britain. Furthermore, about 54 percent of all meters are now smart or advanced meters, with 26.5 million operating in smart mode.

- Furthermore, digitization is also modernizing and accelerating energy efficiency measures, owing to which the deployment of smart grids is surging in the European region, as they are efficient in dynamically optimizing supply and fostering supply of significant amounts of electricity from renewable energy sources such as solar power.

- However, the high cost linked with installing smart meters, growing security concerns, and shortage of capital investment for infrastructure installations is hampering the market's growth over the forecast period.

Europe Smart Meter Market Trends

Increased investments in smart grid projects in expected to drive the market growth

- Electricity demand in the European region is anticipated to increase significantly in the next few decades. For instance, according to IEA, electricity demand in Europe is anticipated to increase by 40 TWh between 2019-2025. Modernization, expansion, digitization, and decentralization of the electricity infrastructure for improved resiliency and planned investment are, thus, expected to change several market dynamics in the region.

- Utilities in the European region are rising, adopting technologies like digital twinning and artificial intelligence and, coupled with surging government support and initiatives, further attracting investments in smart grid projects. For instance, amid the ongoing energy crisis, the German ministry concerning the energy sector has introduced measures to expedite the adoption of federally funded high-saving energy efficiency initiatives. Under the new measures, vendors can start implementing their projects directly after submitting their funding application, whereas previously, they needed to wait for approval.

- The adoption of smart meters, as they are a suitable measure of future-ready technologies, paves the way for the smart grid by facilitating two-way real-time communication between DISCOMs and consumers through GPRS technologies.

- The increasing focus of European countries towards enhancing renewable energy generation capacity is also contributing to the development of smart grid infrastructure in the region as renewable energy generation plants focus more on applying advanced technologies to enhance production and distribution efficiency. By 2023, France's renewable energy sources had a power capacity exceeding 70 gigawatts. Hydropower had the highest amount of energy installed among renewable sources, reaching nearly 26 gigawatts. Around 24 gigawatts of installed capacity is attributed to wind power, with most of it located in onshore power plants.

United Kingdom to Hold a Significant Market Share

- Replacing traditional electricity and gas meters with smart meters forms an important national infrastructure upgrade for the United Kingdom that is expected to help make the region's energy system cheaper, cleaner, and more reliable. According to the government of the United Kingdom, at the end of September 2022, there were around 30.3 million smart and advanced meters in homes and small businesses across Great Britain.

- Further, as of September 2022, a total of 23.8 million gas meters and 28.8 million electricity meters were operated by large energy suppliers in domestic properties across Great Britain. Also, at the end of September 2022, 43 percent of all domestic gas meters and 50 percent of all domestic electricity meters operated by large energy suppliers were smart. Similarly, in non-domestic sites across the region, more electricity meters operate in smart or advanced mode than gas meters (48 percent versus 37 percent).

- Moreover, with a spike in energy prices, many households in the region seek to monitor their gas and electricity usage in real-time and, crucially, how much it costs them, fueling the adoption of smart meters. For instance, per the UK Parliament, household energy bills increased by 54 percent in April 2022 and were expected to increase by 80 percent in October 2022.

- Further, the different regulations implemented to increase the deployment of smart meters in the region further contribute to the market growth. For instance, starting from January 2022, all gas and electricity suppliers in the region had a binding annual installation target to roll out smart and advanced meters to their remaining non-smart customers by the end of 2025.

Europe Smart Meter Industry Overview

The European smart meter market is competitive, with some local and international players active. With the market expected to broaden and yield more opportunities, more players will enter the market soon, fragmenting the competitive landscape during the forecast period. Key players in the market include Elster Group GmbH, Diehl Stiftung & Co. KG, etc.

In February 2023, Netmore, a Swedish IoT operator, started rolling out a LoRaWAN network in France, targeting smart water metering and other large-scale IoT and utility projects. The rollout forms the next step in expanding Netmore's LoRaWAN infrastructure, which, according to the company, is now available in the UK, Sweden, Ireland, the Netherlands, France, and Spain.

In January 2023, the German government announced the adoption of a draft law to restart the digitalization of the energy transition and accelerate the rollout of smart metering. According to the government, the law will likely enter into force in the Spring of 2023, enabling large-scale smart metering rollout to start immediately before becoming mandatory in 2025.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption And Market Definition

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power Of Suppliers

- 4.2.2 Bargaining Power Of Buyers

- 4.2.3 Threat Of New Entrants

- 4.2.4 Threat Of Substitutes

- 4.2.5 Intensity Of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 On The Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Investments in Smart Grid Projects

- 5.1.2 Growth in Smart City Deployment

- 5.1.3 Supportive Government Regulations

- 5.2 Market Challenges/Restraints

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

6 MARKET SEGMENTATION

- 6.1 By Type of Meter (Revenue and Unit Shipments)

- 6.1.1 Smart Gas Meter

- 6.1.2 Smart Water Meter

- 6.1.3 Smart Electricity Meter

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 ***By Country (Revenue and Unit Shipments)

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 General Electric Company

- 7.1.2 Apator SA

- 7.1.3 Badger Meter Inc.

- 7.1.4 Diehl Stiftung & Co. KG

- 7.1.5 Elster Group GmbH (Honeywell International Inc)

- 7.1.6 AEM

- 7.1.7 Itron Inc

- 7.1.8 Kamstrup A/S

- 7.1.9 Landis+ GYR Group AG

- 7.1.10 Arad Group

- 7.1.11 Ningbo Sanxing Electric Co. Ltd.

- 7.1.12 Sensus (Xylem Inc.)

- 7.1.13 Zenner International GmbH & Co. KG