冷凍食品用食用包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Edible Packaging for Frozen Foods Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 184 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801861

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

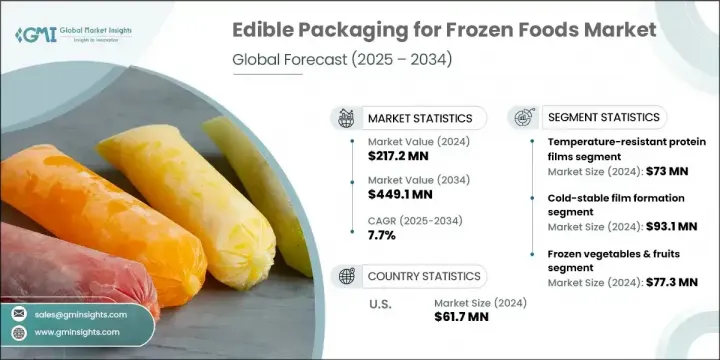

世界の冷凍食品用食用包装市場は、2024年には2億1,720万米ドルとなり、CAGR 7.7%で成長し、2034年には4億4,910万米ドルに達すると予測されています。

この成長市場は、特に個別急速冷凍(IQF)果物、野菜、電子レンジで加熱可能な冷凍食品、調理済み食品のため、低温安定性、生分解性包装に対する需要の増加が原動力となっています。この需要は特に北米、欧州、日本、韓国、オーストラリアなどアジア太平洋の一部で顕著です。食用包装の需要は主に北米のと欧州のでの冷凍果物や植物性食品の販売によって、またアジア太平洋の一部ではキトサンやデンプンベース包装のような、より手頃な代替品によって促進されています。

多糖類フィルムはその手頃な価格と冷凍安定性から、市場内で最も高い成長が見込まれています。さらに、コールドチェーンの最適化のニーズと食用コーティングへのフレーバーの統合が、高級製品カテゴリーの成長を促進すると予想されます。北米のと西欧におけるプライベートブランド冷凍食品の台頭も、可食包装の採用拡大に大きく寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 2億1,720万米ドル |

| 予測金額 | 4億4,910万米ドル |

| CAGR | 7.7% |

多糖類フィルムセグメントは2034年までにシェア34.9%に達します。デンプン、アルギン酸、セルロースなどの材料から作られるこれらのフィルムは、低コスト、アレルゲンリスクの最小化、冷凍環境での強力な性能のために好まれています。また、柔軟性があるため、野菜、魚介類、調理済み食品など様々な冷凍食品に適しています。

2024年には、冷凍野菜・果物セグメントは輸出量の多さと、水分保持とエコフレンドリーブランド強化に役立つ食用コーティングの早期採用により、35.6%のシェアを占めました。欧州のとアジアの一部を含む様々な地域で、有機表示規制が厳しくなり、冷凍食品のプラスチック包装が禁止されたため、食用包装の使用がさらに勢いを増しています。

北米の冷凍食品用食用包装市場は2024年に33%のシェアを占め、小売業者の採用、食用包装の革新的新興企業、持続可能性に対する消費者の意識の高まりがその原動力となっています。米国だけで6,170万米ドルを占めています。さらに、サステイナブル差別化ポイントとして可食フィルムを採用したプライベートブランド冷凍食品製品の台頭が、市場のさらなる成長に拍車をかけています。しかし、原料の高コストや規制遵守などの課題は、市場の拡大を鈍らせる可能性があります。

世界の冷凍食品用食用包装市場の主要参入企業には、Ingredion Incorporated、Tate & Lyle PLC、BASF SE、WikiCell Designs Inc.、Amcor Plc.などが含まれます。市場ポジションを維持・拡大するため、食用包装セグメントの企業は様々な戦略を採用しています。これには、冷凍安定性の向上や冷凍食品の保湿性の改善など、製品性能を高めるための継続的な材料の革新が含まれます。また、企業は持続可能性にも重点を置き、製品が生分解性であることを保証し、エコフレンドリーソリューションを求める消費者の需要に合致させてきました。冷凍食品メーカーとの戦略的パートナーシップや協力関係により、各社は食用包装をより広範な製品に統合することができるようになり、特に成長著しい植物由来食品や有機食品セグメントではその傾向が顕著です。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主要動向

- 一次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- サプライチェーンの複雑さ

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブル実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:材料別、2025~2034年

- 主要動向

- 耐熱性タンパク質フィルム

- 多糖類フィルム

- 脂質ベースコーティング

- 複合材料とハイブリッド材料

第6章 市場推定・予測:技術タイプ別、2025~2034年

- 主要動向

- 冷安定性フィルム形成

- バリア強化

- コールドチェーンの統合

第7章 市場推定・予測:用途タイプ別、2025~2034年

- 主要動向

- 冷凍野菜・果物

- 冷凍肉と魚介類

- 冷凍調理済み食品

- 冷凍乳製品とデザート

第8章 市場推定・予測:地域別、2025~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第9章 企業プロファイル

- Tate & Lyle PLC

- Kerry Group plc

- Ingredion Incorporated

- Cargill, Incorporated

- Archer-Daniels-Midland Company

- DuPont de Nemours, Inc.

- BASF SE

- Corbion N.V.

- Roquette Freres

- CP Kelco(J.M. Huber Corporation)

- FMC Corporation

- Ashland Global Holdings Inc.

- Novamont S.p.A.

- WikiCell Designs Inc.

- MonoSol LLC

目次

The Global Edible Packaging for Frozen Foods Market was valued at USD 217.2 million in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 449.1 million by 2034. This growing market is driven by an increasing demand for cold-stable, biodegradable packaging, particularly for individually quick frozen (IQF) fruits, vegetables, microwaveable frozen meals, and ready-to-heat meals. This demand is particularly evident in North America, Europe, and select parts of Asia-Pacific, such as Japan, South Korea, and Australia. The demand for edible packaging has been primarily fueled by the sales of frozen fruits and plant-based meals in North America and Europe, alongside more affordable alternatives like chitosan and starch-based packaging in parts of Asia-Pacific.

Polysaccharide films, due to their affordability and freeze stability, are expected to see the highest growth within the market. Additionally, the need for cold-chain optimization and the integration of flavors into edible coatings is expected to drive growth in premium product categories. The rise of private-label frozen foods in North America and Western Europe is another significant contributor to the increasing adoption of edible packaging.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $217.2 Million |

| Forecast Value | $449.1 Million |

| CAGR | 7.7% |

The polysaccharide films segment will reach 34.9% share by 2034. These films, derived from materials like starch, alginate, and cellulose, are preferred for their low cost, minimal allergen risk, and strong performance in frozen environments. They also offer flexibility, making them suitable for various frozen foods, such as vegetables, seafood, and ready-to-eat meals.

In 2024, the frozen vegetables and fruits segment accounted for 35.6% share driven by their high export volumes and early adoption of edible coatings, which help preserve moisture and enhance eco-friendly branding. The use of edible packaging has gained further momentum due to stricter organic labeling regulations and bans on plastic wraps for frozen produce in various regions, including Europe and parts of Asia.

North America Edible Packaging for Frozen Foods Market held 33% share in 2024, driven by retailer adoption, innovative start-ups in edible packaging, and growing consumer awareness of sustainability. The U.S. alone represented USD 61.7 million. Additionally, the rise of private-label frozen food products featuring edible films as a sustainable differentiation point has fueled further market growth. However, challenges such as the high cost of raw materials and regulatory compliance may slow the market's expansion.

Key players in the Global Edible Packaging for Frozen Foods Market include Ingredion Incorporated, Tate & Lyle PLC, BASF SE, WikiCell Designs Inc., and Amcor Plc. To maintain and expand their market position, companies in the edible packaging sector have employed a variety of strategies. These include ongoing innovation in materials to enhance product performance, such as increasing freeze stability and improving moisture retention for frozen foods. Companies have also focused on sustainability, ensuring their products are biodegradable and aligned with consumer demand for eco-friendly solutions. Strategic partnerships and collaborations with frozen food manufacturers have allowed companies to integrate their edible packaging into a broader range of products, especially in the growing plant-based and organic food sectors.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Technology

- 2.2.4 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain complexity

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2025 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Temperature-resistant protein films

- 5.3 Polysaccharide films

- 5.4 Lipid-based coatings

- 5.5 Composite & hybrid materials

Chapter 6 Market Estimates and Forecast, By Technology Type, 2025 - 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Cold-stable film formation

- 6.3 Barrier enhancements

- 6.4 Cold chain integration

Chapter 7 Market Estimates and Forecast, By Application type, 2025 - 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 Frozen vegetables & fruits

- 7.3 Frozen meat & seafood

- 7.4 Frozen ready meals

- 7.5 Frozen dairy & desserts

Chapter 8 Market Estimates and Forecast, By Region, 2025 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 Tate & Lyle PLC

- 9.2 Kerry Group plc

- 9.3 Ingredion Incorporated

- 9.4 Cargill, Incorporated

- 9.5 Archer-Daniels-Midland Company

- 9.6 DuPont de Nemours, Inc.

- 9.7 BASF SE

- 9.8 Corbion N.V.

- 9.9 Roquette Freres

- 9.10 CP Kelco (J.M. Huber Corporation)

- 9.11 FMC Corporation

- 9.12 Ashland Global Holdings Inc.

- 9.13 Novamont S.p.A.

- 9.14 WikiCell Designs Inc.

- 9.15 MonoSol LLC

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 184 Pages

- 納期

- 2~3営業日