|

市場調査レポート

商品コード

1801807

BREEAM準拠材料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測BREEAM-Compliant Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| BREEAM準拠材料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年08月07日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

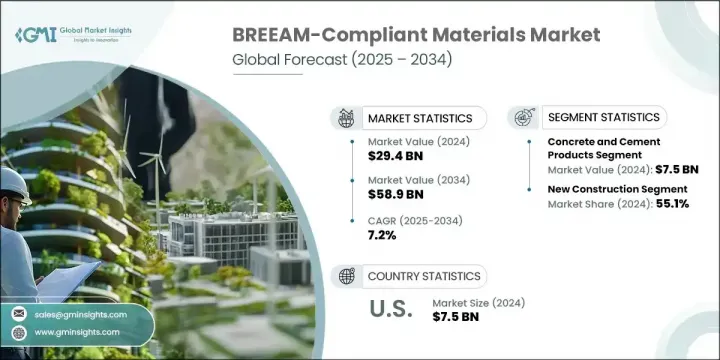

世界のBREEAM準拠材料市場は、2024年に294億米ドルと評価され、CAGR7.2%で成長し、2034年までには589億米ドルに達すると推定されています。

これらの材料は、BREEAMの持続可能性要件に沿うように設計されており、調達、製造から使用後の廃棄に至るまで、ライフサイクル全体を通じて環境への影響を最小限に抑えることができます。環境意識の高まり、規制義務の強化、企業の持続可能性への取り組み強化の推進は、こうした環境配慮型建設資材への需要を大きく後押ししています。産業界や政府が二酸化炭素排出量の削減に努める中、BREEAM認定材料は現代の建築慣行において不可欠な要素となりつつあります。

環境問題が深刻化する中、企業や政策立案者は建設におけるグリーンソリューションの導入に一丸となって取り組んでおり、こうした持続可能な代替案の採用が加速しています。特に、環境政策がより厳しく、グリーン建設に大きなインセンティブが与えられている地域では、強力な規制支援により、市場は継続的な成長を遂げています。持続可能な建設が動向から標準へと進化するにつれて、BREEAM準拠材料の勢いは急成長を続け、環境に優しいインフラの構築における役割を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 294億米ドル |

| 予測金額 | 589億米ドル |

| CAGR | 7.2% |

コンクリート・セメント系材料は2024年に75億米ドルを生み出し、基礎・構造建築における極めて重要な役割により、BREEAM準拠セグメントをリードしています。これらの製品は、新しく建設される構造物でも、環境に焦点を当てた改修でも、そのコスト効率と適応性のおかげで広く採用されています。都市化が拡大し、特に持続可能な開発に重点を置く地域でインフラプロジェクトが増加するにつれ、低炭素の代替物への需要が加速しています。メーカー各社は、進化するグリーンビルディングへの期待に応えるため、これらの材料の環境対応バージョンをますます優先するようになっています。

2024年の新規建設プロジェクト分野のシェアは55.1%に達し、用途分野のトップに躍り出ました。高い環境性能基準を満たすことを目的としたプロジェクトの増加により、新築が市場成長の中心的要因となっています。それにもかかわらず、開発業者や所有者が現在のエネルギー効率基準に合わせて老朽化した建築物のアップグレードを検討しているため、古い建築物の改修や改装が人気を集めています。特に商業不動産分野では、設計の専門家がホスピタリティ、小売、オフィス環境向けの持続可能なソリューションを求めているため、フィットアウトや内装用途も増加傾向にあります。

米国BREEAM準拠材料市場は2024年に75億米ドルを生み出し、持続可能な建設への強い関心とグリーン材料の使用を奨励する規制の枠組みにより、主要プレーヤーとしての地位を確立しています。環境に優しい建築慣行が優先されるようになったことで、商業、住宅、施設プロジェクトにおけるBREEAM認証製品の採用が加速しています。カナダもまた、政府の積極的な政策や学術機関と建設業界の協力的な取り組みによって成長が加速しており、主要部門全体で持続可能性がさらに促進されています。

世界のBREEAM準拠材料市場を形成している著名な企業には、EcoCocon、Kingspan、Holcim、Owens Corning、Amorim Cork、Saint-Gobain、Concrete Centre、BRE Global Ltd.などがあります。これらの企業は、持続可能性のベンチマークを設定し、革新的な建設資材を提供することに貢献しています。主要企業は、BREEAM準拠材料市場での存在感を高めるため、二酸化炭素排出量の削減、エネルギー効率の向上、リサイクル性の改善に重点を置いた製品革新に多額の投資を行っています。その多くは、既存の製品ラインをBREEAM基準以上に改良し、構造用途と内装用途の両方に合わせた新しい環境配慮型ソリューションを導入しています。持続可能性認証機関とのパートナーシップや、建設バリューチェーン内での戦略的協力関係は、ブランドが信頼と知名度を確保するのに役立っています。また、企業はデジタルプラットフォームを活用して、BREEAM準拠製品の利点を顧客に伝えると同時に、需要の拡大に対応するために製造能力を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 素材別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- コンクリート・セメント製品

- 生コンクリート

- プレキャストコンクリート要素

- セメント代替品とブレンド

- 鉄鋼・金属製品

- 構造用鋼

- 鉄筋

- 金属クラッディングと屋根

- リサイクル金属含有製品

- 断熱材

- 木質繊維断熱材

- コルク系断熱材

- 麻とバイオベースの断熱材

- リサイクル素材を使用した断熱材

- 木材・木製品

- 認証された持続可能な木材

- エンジニアリングウッド製品

- 再生木材とリサイクル木材

- 竹と代替木材

- 床材・仕上げ材

- 持続可能な床材ソリューション

- 低VOC塗料とコーティング

- リサイクルコンテンツのタイルと表面

- バイオベースの仕上げ材

- 屋根材・外壁材

- グリーンルーフシステム

- 高性能グレージング

- 持続可能な外装材

- 耐候性バリアシステム

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 新築

- 商業ビル

- 住宅

- 産業施設

- インフラプロジェクト

- 改修・改造

- 歴史的建造物の修復

- エネルギー効率の向上

- 持続可能な改修プロジェクト

- 建物のパフォーマンス向上

- 内装・内装用途

- オフィス設備

- 小売スペース

- ヘルスケア施設

- 教育施設

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 商業用不動産

- オフィスビル

- 小売店とショッピングセンター

- ホテルとホスピタリティ

- 複合開発

- 住宅部門

- 一戸建て住宅

- 集合住宅

- 手頃な価格の住宅プロジェクト

- 高級住宅開発

- 公共施設

- ヘルスケア施設

- 教育機関

- 政府庁舎

- 文化・コミュニティセンター

- 産業とインフラ

- 製造施設

- 倉庫と配送センター

- 交通インフラ

- 公益事業・エネルギープロジェクト

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Amorim Cork

- BRE Global Ltd

- Concrete Centre

- EcoCocon

- Holcim

- Kingspan

- Owens Corning

- Saint-Gobain

The Global BREEAM-Compliant Materials Market was valued at USD 29.4 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 58.9 billion by 2034. These materials are designed to align with BREEAM's sustainability requirements, ensuring minimal environmental impact throughout their lifecycle-from sourcing and manufacturing to end-of-life disposal. Growing environmental awareness, increased regulatory obligations, and the push toward stronger corporate sustainability commitments are significantly fueling demand for these eco-conscious construction products. As industries and governments strive to reduce their carbon footprints, BREEAM-certified materials are becoming an essential component in modern building practices.

With environmental challenges intensifying, companies and policymakers are working in unison to implement green solutions in construction, accelerating the adoption of these sustainable alternatives. The market is seeing continuous growth due to strong regulatory support, especially in regions where environmental policies are more rigorous and green construction is heavily incentivized. As sustainable construction evolves from a trend into a standard, the momentum behind BREEAM-compliant materials continues to grow rapidly, reinforcing their role in creating eco-friendly infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.4 Billion |

| Forecast Value | $58.9 Billion |

| CAGR | 7.2% |

The concrete and cement-based materials generated USD 7.5 billion in 2024, leading the BREEAM-compliant segment due to their pivotal role in foundational and structural construction. These products are widely adopted thanks to their cost-efficiency and adaptability in both newly built structures and eco-focused retrofits. As urbanization expands and infrastructure projects increase, especially in regions focused on sustainable development, demand for low-carbon alternatives is gaining pace. Manufacturers are increasingly prioritizing environmentally responsible versions of these materials to meet evolving green building expectations.

The new construction projects segment held 55.1% share in 2024, emerging as the top application segment. The rise in projects committed to meeting high environmental performance standards has made new builds a central driver of market growth. Nonetheless, retrofitting and refurbishing older buildings are gaining traction as developers and owners look to upgrade outdated structures in line with current energy efficiency benchmarks. Fit outs and interior applications are also on the rise, particularly in the commercial real estate space, as design professionals seek sustainable solutions for hospitality, retail, and office environments.

U.S. BREEAM-Compliant Materials Market generated USD 7.5 billion in 2024, positioning itself as a major player due to a strong focus on sustainable construction and regulatory frameworks that encourage the use of green materials. The increasing prioritization of eco-friendly building practices is boosting the adoption of BREEAM-certified products across commercial, residential, and institutional projects. Canada is also witnessing accelerated growth thanks to proactive governmental policies and collaborative efforts between academic institutions and the construction industry, further promoting sustainability across key sectors.

Prominent players shaping the Global BREEAM-Compliant Materials Market include EcoCocon, Kingspan, Holcim, Owens Corning, Amorim Cork, Saint-Gobain, Concrete Centre, and BRE Global Ltd. These companies are instrumental in setting sustainability benchmarks and delivering innovative construction materials. To enhance their presence in the BREEAM-compliant materials market, leading companies are investing significantly in product innovation focused on lowering carbon emissions, boosting energy efficiency, and improving recyclability. Many are reengineering existing product lines to meet or exceed BREEAM standards and are introducing new eco-conscious solutions tailored to both structural and interior applications. Partnerships with sustainability certifying bodies and strategic collaborations within the construction value chain are helping brands secure trust and visibility. Companies are also leveraging digital platforms to educate customers on the benefits of BREEAM-compliant products while expanding manufacturing capabilities to meet growing demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Application trends

- 2.2.3 End use sector trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Concrete and Cement Products

- 5.2.1 Ready-Mix Concrete

- 5.2.2 Precast Concrete Elements

- 5.2.3 Cement Alternatives and Blends

- 5.3 Steel and Metal Products

- 5.3.1 Structural Steel

- 5.3.2 Reinforcing Steel

- 5.3.3 Metal Cladding and Roofing

- 5.3.4 Recycled Metal Content Products

- 5.4 Insulation Materials

- 5.4.1 Wood Fiber Insulation

- 5.4.2 Cork-based Insulation

- 5.4.3 Hemp and Bio-based Insulation

- 5.4.4 Recycled Content Insulation

- 5.5 Timber and Wood Products

- 5.5.1 Certified Sustainable Timber

- 5.5.2 Engineered Wood Products

- 5.5.3 Reclaimed and Recycled Wood

- 5.5.4 Bamboo and Alternative Wood Materials

- 5.6 Flooring and Finishing Materials

- 5.6.1 Sustainable Flooring Solutions

- 5.6.2 Low-VOC Paints and Coatings

- 5.6.3 Recycled Content Tiles and Surfaces

- 5.6.4 Bio-based Finishing Materials

- 5.7 Roofing and Envelope Materials

- 5.7.1 Green Roofing Systems

- 5.7.2 High-Performance Glazing

- 5.7.3 Sustainable Cladding Materials

- 5.7.4 Weather Barrier Systems

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 New construction

- 6.2.1 Commercial buildings

- 6.2.2 Residential buildings

- 6.2.3 Industrial facilities

- 6.2.4 Infrastructure projects

- 6.3 Refurbishment and retrofit

- 6.3.1 Heritage building restoration

- 6.3.2 Energy efficiency upgrades

- 6.3.3 Sustainable renovation projects

- 6.3.4 Building performance improvements

- 6.4 Fit-out and interior applications

- 6.4.1 Office fit-outs

- 6.4.2 Retail spaces

- 6.4.3 Healthcare facilities

- 6.4.4 Educational buildings

Chapter 7 Market Estimates and Forecast, By End Use Sector, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Commercial real estate

- 7.2.1 Office buildings

- 7.2.2 Retail and shopping centers

- 7.2.3 Hotels and hospitality

- 7.2.4 Mixed-use developments

- 7.3 Residential sector

- 7.3.1 Single-family homes

- 7.3.2 Multi-family housing

- 7.3.3 Affordable housing projects

- 7.3.4 Luxury residential developments

- 7.4 Institutional buildings

- 7.4.1 Healthcare facilities

- 7.4.2 Educational institutions

- 7.4.3 Government buildings

- 7.4.4 Cultural and community centers

- 7.5 Industrial and infrastructure

- 7.5.1 Manufacturing facilities

- 7.5.2 Warehouses and distribution centers

- 7.5.3 Transportation infrastructure

- 7.5.4 Utilities and energy projects

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Amorim Cork

- 9.2 BRE Global Ltd

- 9.3 Concrete Centre

- 9.4 EcoCocon

- 9.5 Holcim

- 9.6 Kingspan

- 9.7 Owens Corning

- 9.8 Saint-Gobain