|

市場調査レポート

商品コード

1636158

アジア太平洋地域の先進建材:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)APAC Advanced Building Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の先進建材:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

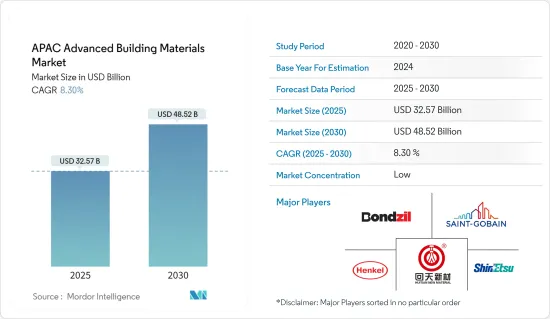

アジア太平洋地域の先進建材の市場規模は2025年に325億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.3%で、2030年には485億2,000万米ドルに達すると予測されます。

主なハイライト

- パンデミックは建材製造に影響を与え、サプライチェーンを混乱させました。さらに、パンデミックは建設プロジェクトの遅れを引き起こし、先進建材産業にさらなる影響を与えました。その後、規制が緩和されたことで、パンデミック以前の水準と比較すると市場は回復しました。

- 建築物建設とインフラ部門の成長は、先進建材業界の主要な牽引役です。これらの材料は、構造強度、エネルギー効率、脱炭素目標などを達成するための建設プロジェクトに採用されています。加えて、国が定めたネット・ゼロ目標を達成するため、開発業者の多くは、開発プロジェクトにグリーン建材を採用することに関心を持っています。

- 一方、2023年4月、インド不動産開発業者連合会(Credai)はインドグリーンビルディング協会(IGBC)と提携し、今後2年間でインド全土に1,000件以上、2030年までに4,000件のグリーン認定プロジェクトを建設することを決定しました。

- さらに、建設期間の短縮と費用対効果の高い製品の利用に対するニーズの高まりが、先進建材の需要を促進しています。加えて、生コンクリートやプレキャスト製品の利用は、建築建設業界における時間の節約につながります。

- 例えば、2022年7月、AboitizLandは三井住友建設、SMCC Philippines Inc.と提携し、日本のプレキャストコンクリート技術を導入して住宅プロジェクトを革新しました。このように、建設プロジェクトの増加とインフラ部門への投資の増加は、同地域の先進建材産業の需要を促進すると予想されます。

アジア太平洋地域の先進建材市場の動向

市場需要を牽引するインフラ開発

- アジア太平洋地域では現在、主に投資の増加によってインフラ開発プロジェクトが大きく成長しています。このような投資の急増は、ひいてはこれらのプロジェクトにおける先進建材の需要を強化しています。例えば、米国、インド、オーストラリアは2022年5月、アジア太平洋地域のインフラ・プロジェクトに500億米ドル以上を投資する計画を発表しました。

- さらに、インド、中国、日本などの新興諸国では、数多くのインフラ・プロジェクトが進行中で、それぞれの経済をさらに促進しています。2023年4月、インド政府は7億4,000万米ドルを超えるインフラ・プロジェクトの計画を明らかにしました。さらに、国家インフラ・パイプラインを通じて、政府はインドのインフラ開発プロジェクトに1兆3,000億米ドル以上を割り当てることを目指しています。

- 一方、日本は2023年5月、パトナ地下鉄建設プロジェクトやラジャスタン水セクター生活改善プロジェクトを含む3つのインフラプロジェクトに8億6,000万米ドルを超える資金をインドに提供することを約束しました。さらに、2022年の中国の公共支出は前年比5%以上の大幅な伸びを示しました。その結果、アジア太平洋地域全体のインフラ開発プロジェクトに対するこうした投資の増加は、高度な建築材料に対する大きな需要を生み出しています。

中国建設セクターが市場成長を牽引

- 中国の建設業界は、パンデミック危機にもかかわらず、第14次5ヵ年計画(2021年から2025年まで)に示されたインフラへの大幅な投資によって著しい成長を遂げています。この計画は、5つのカテゴリーにわたる20の定量的目標で構成されています。中国政府は、2023年までに全国の多様なインフラ・プロジェクトに1兆1,000億米ドル以上を割り当て、国内の先進建材製造工場の開発をさらに後押ししています。

- さらに2022年、中国政府は建物に関連する汚染を抑制することを目的としたグリーン建設プロジェクトに140億米ドル以上を計上しました。炭素排出量正味ゼロの目標を達成するため、政府は7億8,000万米ドル以上を建物関連の汚染軽減に割り当てた。

- さらに、文化遺産を保護するための取り組みとして、全国に数多くの博物館が建設されています。例えば、北京市文化財局は2023年2月までに市内に460以上の博物館を建設する計画で、すでに215以上の博物館が登録されています。このような継続的な投資とプロジェクトの拡大により、同国の建設生産高は前年比6%以上の成長を遂げ、その結果、先進建材メーカーに対する需要が増加しています。

アジア太平洋地域の先進建材産業の概要

本レポートでは、アジア太平洋地域の先進建材市場で事業を展開する有力企業を取り上げています。同市場は競争が激しく断片化しており、大きなシェアを占めるプレーヤーはいないです。競争力を維持するため、主要企業は常に製品提供の強化に努め、地理的プレゼンスを拡大し、M&Aに絶えず関与しています。市場の主要企業には、Huitian、Bondzil、Saint-Gobain Group、Henkel Balti OU、信越化学工業などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 技術動向に関する洞察

- 業界のバリューチェーン/サプライチェーン分析

- 市場に関する政府規制と主要イニシアチブ

- 市場力学

- 促進要因

- インフラ開発のための政府支出の増加

- 工期短縮と費用対効果の高い製品へのニーズ

- 抑制要因

- 初期投資の高さ

- 機会

- 促進要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- 用途別

- ビル建設

- インフラストラクチャー

- タイプ別

- グリーン材料

- 先端技術

- 材料別

- 先進セメント・コンクリート

- 集成材

- 構造用断熱パネル

- シーリング材

- その他の材料

- 国別

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- China National Building Material Group Corporatio

- Henkel Balti OU

- China Lesso

- Huitian

- Zamil Steel Buildings India Private Limited

- Kingspan Jindal

- Bondzil

- Ultratech Cement Limited

- Arto Precast Concrete

- Saint-Gobain Group

- BASF SE

- DuPont

- Sika AG

- Shin-Etsu Chemical Co., Ltd*

第7章 市場機会と今後の動向

第8章 付録

The APAC Advanced Building Materials Market size is estimated at USD 32.57 billion in 2025, and is expected to reach USD 48.52 billion by 2030, at a CAGR of 8.3% during the forecast period (2025-2030).

Key Highlights

- The pandemic had impacted building materials manufacturing and disrupted the supply chain, further preventing the market from expanding due to restrictions, border closures, etc. Additionally, the pandemic caused delays in construction projects, further affecting the advanced building materials industry. Later, after easing restrictions, the market recovered when compared to pre-pandemic levels.

- The growing building construction and infrastructure sectors are the major drivers of the advanced building materials industry. These materials are employed in construction projects to achieve structural strength, energy efficiency, decarbonization goals, etc. In addition, to meet net-zero goals set by the country, most of the developers are interested in adopting green building materials in development projects.

- Meanwhile, in April 2023, the Confederation of Real Estate Developers Association of India (Credai) partnered with the Indian Green Building Council (IGBC) to build over 1,000 certified green projects across India in the next two years, and 4,000 projects by 2030, these projects, in turn, bolsters the utilization of advanced building materials.

- Furthermore, the increasing need for construction time reduction and utilization of cost-effective products is driving the demand for advanced construction materials. In addition, the utilization of ready-mix concrete and precast products saves time in the building construction industry.

- For instance, in July 2022, AboitizLand partnered with Sumitomo Mitsui Construction Co. Ltd., SMCC Philippines Inc., to innovate its residential projects with the introduction of Japanese precast concrete technology. Thus, the growing construction projects and increasing investments in the infrastructure sector are expected to drive the demand for the advanced building materials industry in the region.

APAC Advanced Building Materials Market Trends

Infrastructure developments driving the market demand

- The Asia-Pacific region is currently experiencing significant growth in infrastructure development projects, primarily driven by increased investments. This surge in investment is, in turn, bolstering the demand for advanced building materials within these projects. For example, in May 2022, the United States, India, and Australia announced plans to invest over USD 50 billion in infrastructure projects across the Asia-Pacific region.

- Moreover, developing countries such as India, China, and Japan are undergoing numerous infrastructure projects, which are further propelling their respective economies. In April 2023, the Indian government revealed plans for infrastructure projects exceeding USD 740 million. Additionally, through the National Infrastructure Pipeline, the government aims to allocate more than USD 1,300 billion to infrastructure development projects in India.

- Meanwhile, in May 2023, Japan committed to funding India with over USD 860 million for three infrastructure projects, including the Patna Metro Rail Construction Project and the Rajasthan Water Sector Livelihood Improvement Project. Furthermore, Chinese public expenditure in 2022 witnessed a substantial growth of over 5% compared to the previous year. Consequently, these increasing investments in infrastructure development projects across the Asia Pacific region are generating a significant demand for advanced building materials.

China construction sector is driving market growth

- The Chinese construction industry is experiencing significant growth despite the pandemic crisis, fueled by substantial investments in infrastructure as outlined in the 14th Five-Year Plan (spanning from 2021 to 2025). This plan comprises 20 quantitative targets across five categories. The Chinese government has allocated over USD 1.1 trillion for diverse infrastructure projects nationwide by 2023, further boosting the development of advanced building materials manufacturing plants in the country.

- Additionally, in 2022, the Chinese government earmarked more than USD 14 billion for green construction projects aimed at curbing pollution associated with buildings. To achieve net-zero carbon emission goals, the government allocated over USD 780 million specifically to mitigate building-related pollution.

- Furthermore, efforts to preserve cultural heritage involve the construction of numerous museums nationwide. For example, the Beijing Municipal Cultural Heritage Bureau planned to build over 460 museums in the city by February 2023, with more than 215 museums already registered. These continuous investments and expanding projects have driven the country's construction output to grow by over 6% compared to the previous year, thereby generating increased demand for manufacturers of advanced construction materials.

APAC Advanced Building Materials Industry Overview

The report covers prominent players operating in the Asia-Pacific advanced building material market. The market is highly competitive and fragmented, with no players occupying a significant share. To remain competitive, the major players are constantly working to enhance their product offerings, expanding their geographical presence, and constantly being involved in mergers and acquisitions. Some of the major players in the market include Huitian, Bondzil, Saint-Gobain Group, Henkel Balti OU, Shin-Etsu Chemical Co., Ltd, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Insights on Technological Trends

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Spotlight on Government Regulations and Key Initiatives in the Market

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increase in government expenditures for infrastructural development

- 4.5.1.2 Need for reduced construction time and cost-effective products

- 4.5.2 Restraints

- 4.5.2.1 High initial investments

- 4.5.3 Opportunities

- 4.5.1 Drivers

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Building Construction

- 5.1.2 Infrastructure

- 5.2 By Type

- 5.2.1 Green Materials

- 5.2.2 Technically Advanced

- 5.3 By Material

- 5.3.1 Advanced Cement And Concrete

- 5.3.2 Cross-Laminated Timber

- 5.3.3 Structural Insulated Panel

- 5.3.4 Sealants

- 5.3.5 Other Materials

- 5.4 By Country

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia

- 5.4.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 China National Building Material Group Corporatio

- 6.2.2 Henkel Balti OU

- 6.2.3 China Lesso

- 6.2.4 Huitian

- 6.2.5 Zamil Steel Buildings India Private Limited

- 6.2.6 Kingspan Jindal

- 6.2.7 Bondzil

- 6.2.8 Ultratech Cement Limited

- 6.2.9 Arto Precast Concrete

- 6.2.10 Saint-Gobain Group

- 6.2.11 BASF SE

- 6.2.12 DuPont

- 6.2.13 Sika AG

- 6.2.14 Shin-Etsu Chemical Co., Ltd*