|

市場調査レポート

商品コード

1801803

包装用発泡ポリスチレン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Expanded Polystyrene for Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 包装用発泡ポリスチレン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年08月01日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

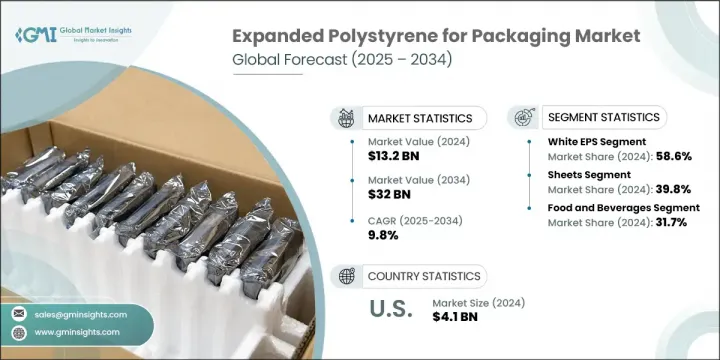

包装用発泡ポリスチレンの世界市場は、2024年には132億米ドルとなり、CAGR 9.8%で成長し、2034年には320億米ドルに達すると推定されています。

この市場成長の原動力となっているのは、軽量で衝撃を吸収し、高い断熱性を持つ包装材料へのニーズです。EPSは、構造的完全性を維持し鮮度を保つことで、長距離輸送中の商品(特に生鮮品)を保護するのに役立ちます。すぐに食べられる食事や便利な食品への嗜好の高まりも、効率的で信頼性の高い包装形態への需要の増加を促しています。

急増するeコマース活動と迅速な宅配サービスは、EPS包装市場の拡大に影響を与え続けています。食料品、電化製品、医薬品などをオンラインで購入する消費者が増えるにつれ、軽量でありながら輸送中の商品を保護するのに十分な弾力性を備えた包装が重視されるようになっています。メーカーやロジスティクス・プロバイダーは、これらの条件を満たし、費用対効果の高い輸送をサポートするEPSをますます好むようになっています。この素材の信頼性、強度対重量比、断熱性能により、EPSは現代の流通・配送ニーズに対応するあらゆる分野で重要な選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 132億米ドル |

| 予測金額 | 320億米ドル |

| CAGR | 9.8% |

白色EPSは、2024年の市場評価額が77億米ドルとなり、引き続きトップの座にあります。白色EPSは、手頃な価格、実証済みの信頼性、多様な包装用途への適合性から広く好まれています。FMCGや農産物から電子機器や家電製品に至るまで、白色EPSが優位を保っています。成形技術や表面技術の進歩により、高速自動包装システムとの適合性が向上しています。単純に見えるが、白色EPSはスピードと機能性を優先する、大量生産でコスト重視の包装環境で広く利用されています。

EPSシート分野は、2024年に52億米ドルを生み出しました。これらのシートは優れた耐衝撃性を持ち、軽量で、非常に経済的であることで知られています。パッケージ化された電子機器、機械、家電製品の構造的保護を強化するために、しばしば型抜きされたり、フォームの裏地とラミネートされたりします。これらの分野では、オーダーメイドの保護包装に対する需要が高まっているため、EPSシートは今後も好まれる材料であり続けると思われます。

米国の包装用発泡ポリスチレン市場規模は2024年に41億米ドルで、2034年までのCAGRは9%です。同国の堅調な飲食品産業は、特にコールドチェーン・ロジスティクスと断熱材用途でEPSの利用を促進し続けています。オンラインショッピングの動向は、EPSベースの保護包装の需要をさらに増大させています。市場関係者は現在、環境問題の高まりに対応するため、バイオベースの代替品や持続可能なリサイクル・オプションを模索しています。米国では、輸送時の排出を減らしコストを下げる軽量包装が重視され、技術革新を促し、新たな成長の道を切り開いています。

世界の包装用発泡ポリスチレン市場を形成する主要企業には、BASF SE、KANEKA CORPORATION、Alpek S.A.B. de C.V.、TotalEnergies、Synthos、Dart Container Corporation、Wuxi Xingda Foam Plastic、Tamai Kasei Corporation、DuPont、Styrotech, Inc.、Versalis S.p.A.、Michigan Foam Products LLC、Engineered Foam Products、Foamcraft USA, LLC、Styropekなどがあります。EPS包装市場の主要企業は、競争力を維持するために、製品の革新、地域拡大、持続可能性への取り組みを組み合わせて実施しています。多くの企業は、世界の環境意識の動向に合わせるため、リサイクル可能なバイオベースのEPSソリューションの開発に投資しています。ロジスティクス企業やFMCG企業との戦略的パートナーシップにより、進化するパッケージング・ニーズに対応することができます。オンライン小売やコールドチェーンサプライチェーンからの大量需要に対応するため、生産の自動化やカスタマイズされたEPS金型が優先されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 食品・飲料業界における需要の増加

- eコマースと宅配サービスの急速な拡大

- 建設業界の成長

- コスト効率と多様な用途

- リサイクル性と技術の進歩

- 業界の潜在的リスク&課題

- 環境問題と規制圧力

- 持続可能な代替包装材への置き換え

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 過去の価格分析(2021-2024)

- 価格動向の要因

- 地域による価格差

- 価格予測(2025-2034)

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 持続可能な材料の評価

- カーボンフットプリント分析

- 循環型経済の実現

- 持続可能性の認証と基準

- 持続可能性ROI分析

- 世界の消費者感情分析

- 特許分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中分析

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 黒

- グレー

- 白

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- シート

- トレイとクラムシェル

- フォームクーラー

- カップとボウル

- バラ緩衝材

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 飲食品

- 黒

- グレー

- 白

- フードサービス

- 黒

- グレー

- 白

- ヘルスケア

- 黒

- グレー

- 白

- 電子機器および電気機器

- 黒

- グレー

- 白

- 建築および建設

- 黒

- グレー

- 白

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Alpek S.A.B. de C.V.

- BASF SE

- Cellofoam

- Dart Container Corporation

- DuPont

- Engineered Foam Products

- Epsilyte LLC

- Flint Hills Resources

- Foam Holdings, Inc.

- Foam Products Corporation

- Foamcraft USA, LLC

- Geofoam International LLC

- Harbor Foam

- K. K. Nag Pvt. Ltd.

- KANEKA CORPORATION

- Michigan Foam Products LLC

- Poliestireno de San Luis S.A. de C.V.

- Storopack

- Styropek

- Styrotech, Inc.

- Synthos

- Tamai Kasei Corporation

- TotalEnergies

- Versalis S.p.A.

- Wuxi Xingda Foam Plastic

The Global Expanded Polystyrene for Packaging Market was valued at USD 13.2 billion in 2024 and is estimated to grow at a CAGR of 9.8% to reach USD 32 billion by 2034. This market growth is being driven by the need for lightweight, shock-absorbing packaging materials that offer high insulation properties. EPS helps protect goods-especially perishables-during long-distance transport by maintaining structural integrity and preserving freshness. The rising preference for ready-to-eat meals and convenient food solutions is also prompting increased demand for efficient and reliable packaging formats.

Surging e-commerce activities and rapid doorstep delivery services continue to influence the expansion of the EPS packaging market. As more consumers shift toward purchasing items like groceries, electronics, and pharmaceuticals online, there is a stronger emphasis on packaging that is lightweight yet resilient enough to protect goods in transit. Manufacturers and logistics providers increasingly favor EPS as it checks these boxes and supports cost-effective shipping. The material's reliability, strength-to-weight ratio, and insulation capabilities make it a key choice across sectors responding to modern distribution and delivery needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.2 Billion |

| Forecast Value | $32 Billion |

| CAGR | 9.8% |

White EPS remained the top-performing segment in 2024 with a market valuation of USD 7.7 billion. This variant is widely preferred for its affordability, proven reliability, and suitability across diverse packaging applications. From FMCG and agricultural produce to electronics and household appliances, white EPS continues to dominate. Advances in molding and surface technology have improved its compatibility with high-speed automated packaging systems. Although it appears simple, white EPS is widely utilized in high-volume, cost-sensitive packaging environments that prioritize speed and functionality.

The EPS sheets segment generated USD 5.2 billion in 2024. These sheets offer excellent impact resistance, are lightweight, and are known for being highly economical. They are often die-cut or laminated with foam backings to enhance structural protection in packaged electronics, machinery, and consumer appliances. The rising demand for tailored and protective packaging in these sectors ensures that EPS sheets will remain a preferred material in the years to come.

United States Expanded Polystyrene for Packaging Market generated USD 4.1 billion in 2024, registering a CAGR of 9% through 2034. The country's robust food and beverage industry continues to drive EPS usage, especially in cold chain logistics and insulation applications. Online shopping trends further amplify demand for EPS-based protective packaging. Market players are now exploring bio-based alternatives and sustainable recycling options to respond to increasing environmental concerns. Emphasis on lighter packaging that reduces shipping emissions and lowers costs is prompting innovations, creating new avenues for growth in the US.

Key players shaping the Global Expanded Polystyrene for Packaging Market include BASF SE, KANEKA CORPORATION, Alpek S.A.B. de C.V., TotalEnergies, Synthos, Dart Container Corporation, Wuxi Xingda Foam Plastic, Tamai Kasei Corporation, DuPont, Styrotech, Inc., Versalis S.p.A., Michigan Foam Products LLC, Engineered Foam Products, Foamcraft USA, LLC, and Styropek. Leading companies in the EPS packaging market are implementing a mix of product innovation, regional expansion, and sustainability initiatives to maintain a competitive edge. Many are investing in the development of recyclable and bio-based EPS solutions to align with global eco-conscious trends. Strategic partnerships with logistics firms and FMCG companies allow them to address evolving packaging needs. Automation in production and customized EPS molds are being prioritized to meet high-volume demand from online retail and cold-chain supply chains.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Packaging type trends

- 2.2.2 Material trends

- 2.2.3 Application trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand in food and beverage industry

- 3.2.1.2 Rapid expansion of e-commerce and home delivery services

- 3.2.1.3 Construction industry growth

- 3.2.1.4 Cost-effectiveness and versatile applications

- 3.2.1.5 Recyclability and technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental concerns and regulatory pressure

- 3.2.2.2 Substitution by sustainable packaging alternatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability roi analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Black

- 5.3 Grey

- 5.4 White

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Sheets

- 6.3 Trays & clamshells

- 6.4 Foam coolers

- 6.5 Cups & bowls

- 6.6 Packaging peanuts

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Food and beverages

- 7.2.1 Black

- 7.2.2 Grey

- 7.2.3 White

- 7.3 Foodservice

- 7.3.1 Black

- 7.3.2 Grey

- 7.3.3 White

- 7.4 Healthcare

- 7.4.1 Black

- 7.4.2 Grey

- 7.4.3 White

- 7.5 Electronics and electrical appliances

- 7.5.1 Black

- 7.5.2 Grey

- 7.5.3 White

- 7.6 Building and constructions

- 7.6.1 Black

- 7.6.2 Grey

- 7.6.3 White

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alpek S.A.B. de C.V.

- 9.2 BASF SE

- 9.3 Cellofoam

- 9.4 Dart Container Corporation

- 9.5 DuPont

- 9.6 Engineered Foam Products

- 9.7 Epsilyte LLC

- 9.8 Flint Hills Resources

- 9.9 Foam Holdings, Inc.

- 9.10 Foam Products Corporation

- 9.11 Foamcraft USA, LLC

- 9.12 Geofoam International LLC

- 9.13 Harbor Foam

- 9.14 K. K. Nag Pvt. Ltd.

- 9.15 KANEKA CORPORATION

- 9.16 Michigan Foam Products LLC

- 9.17 Poliestireno de San Luis S.A. de C.V.

- 9.18 Storopack

- 9.19 Styropek

- 9.20 Styrotech, Inc.

- 9.21 Synthos

- 9.22 Tamai Kasei Corporation

- 9.23 TotalEnergies

- 9.24 Versalis S.p.A.

- 9.25 Wuxi Xingda Foam Plastic