|

市場調査レポート

商品コード

1907324

欧州の発泡ポリスチレン(EPS):市場シェア分析、業界動向、統計、成長予測(2026年~2031年)Europe Expanded Polystyrene (EPS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の発泡ポリスチレン(EPS):市場シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

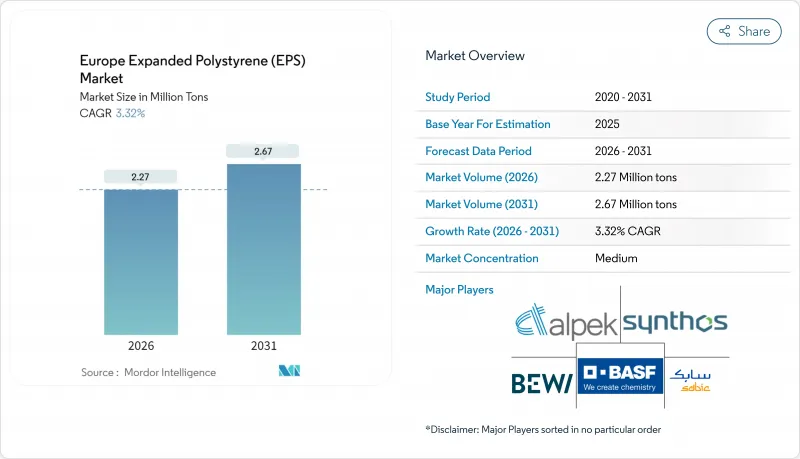

欧州の発泡ポリスチレン(EPS)市場は、2025年に220万トンと評価され、2026年の227万トンから2031年までに267万トンに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは3.32%と見込まれます。

需要は主に建築物の断熱改修および精密機器向け保護包装から生じており、堅調な国内サプライチェーン、リサイクル率の漸増、および技術革新による炭素排出量削減が業界の回復力を強化しています。2025年施行のEU建築物エネルギー性能指令などの規制要因は、新築・改修物件における断熱性能(R値)の向上を義務付け、代替素材のシェア拡大にもかかわらず断熱材需要を安定的に維持します。同時に、mRNAバイオロジクス物流の急増と家電製品の国内回帰により包装需要が持続し、スチレン価格変動によるマージン圧縮から商品セグメントを緩衝する役割を果たしています。しかしながら、欧州発泡ポリスチレン市場は、原料価格変動に伴う顕在リスクの高まり、密集都市部における防火規制、紙・パルプ・菌糸体ベース代替品の顧客試験といった課題に対処する必要があります。

欧州の発泡ポリスチレン(EPS)市場の動向と洞察

建築省エネ基準が断熱性能要件を推進

より厳格な国家およびEU全体のエネルギー基準により、開発者は壁、屋根、床のU値を低減した設計を迫られており、断熱材の厚さ要件が引き上げられ、欧州のEPS市場ソリューションに対する安定した需要を支えています。ドイツの建築物エネルギー法(Gebaudeenergiegesetz)では、外壁のU値を0.20 W/(m2K)前後に規定しており、これには通常12~16cmのEPS断熱材が必要となります。高さに基づく防火制限があるにもかかわらず、ドイツの外壁システムにおいて発泡スチロールが約40%のシェアを維持する要因となっています。フランスや北欧諸国も同様の性能規定を拡大しており、2024年に改正される「建築物のエネルギー性能指令」では、2030年以降の新築建物にネットゼロ義務を課すことで、長期的な断熱材需要が固定化されます。EU改修計画「Renovation Wave」の下では改修需要も増加し、補助金制度により住宅所有者は断熱効率が高く手頃な価格のシステムを選択するよう導かれています。この規制対応の潮流の中で、メーカー各社はネオポールやグラファイト強化製品ラインを拡充し、高価な構造変更を伴わずに優れた断熱性能(R値)を提供しています。

mRNAバイオロジクス向けコールドチェーンの拡大

mRNAワクチンや先進治療薬の急速な商業化には、工場から診療所まで2℃~8℃の温度安定性が求められます。EPS製輸送容器がこの分野で主流となっているのは、その独立気泡構造が長距離輸送やラストマイル配送において、予測可能な断熱性と緩衝性を提供するからです。コールド・チェーン・テクノロジーズ社などのメーカーは、オランダ・ブレダに欧州生産拠点を新設し、EU GDP中核地域の80%を6時間以内の輸送圏に収める医薬品流通網を特に強化しています。欧州薬局方補遺11.7に基づく規制強化により、包装資材サプライヤーは抽出物・溶出物の検証を迫られており、実績あるコンプライアンス記録を持つ既存のEPS配合が有利です。コールドチェーン市場は高収益性を伴い、汎用建築用発泡材におけるスチレン価格変動の影響を一部相殺しています。

原料コストの変動が利益率を圧迫

スチレンはEPSの現金コストの最大70%を占めるため、ベンゼン・ナフサ価格の変動に収益性が敏感です。トリンセオ社が発表した2025年1月契約におけるトン当たり55ユーロの値上げは、生産者がマージン防衛を図っていることを示しています。構造的な逼迫は、ヴェルサリス社が2025年4月にブリンディジのクラッカーを閉鎖することでさらに深刻化し、地域の輸入依存度を高め、運賃および為替リスクを増幅させます。変動する原材料費と固定価格の建設契約との不一致は、コンバーターのキャッシュフローを圧迫し、北西欧全域の小規模プラントに課題をもたらしています。

セグメント分析

欧州のホワイトグレード発泡ポリスチレン市場規模は、全体消費量の70.86%を占めました。ホワイトEPSは、コストが依然として重要な選定基準であり、規格適合に十分な薄板厚で済む中空壁、スラブオングレード床、周縁排水板において継続的に使用されています。しかしながら、黒色および銀色グレードは2031年までに3.74%のCAGRで最速の成長を記録する見込みです。これは、黒色グレードに含有される黒鉛の赤外線反射粒子が熱伝導率(λ値)を約0.030 W/(m・K)まで低減するためです。外断熱複合システムにおいて、黒色EPSは同じ断熱性能(U値)を維持しながら層厚を16cmから12cmに削減可能であり、狭小敷地の都市部におけるファサード改修を実現します。BEWI社のCIRCULUM製品ラインは、性能優位性と再生ビーズ含有率を両立させ、建築家が省エネルギー目標と循環型経済目標を調和させることを支援します。メーカー各社は、機械的特性を損なうことなく再生材の含有率を高めるため、インライン発泡剤回収技術や連続ブロック成形技術への投資を進めており、欧州発泡ポリスチレン市場においてグレーEPSは技術的・環境的価値の向上を可能とする製品として位置付けられています。

欧州発泡ポリスチレン(EPS)市場レポートは、製品タイプ(ホワイトEPS、グレーおよびシルバーEPS)、エンドユーザー産業(建築・建設、電気・電子、包装、その他のエンドユーザー産業)、地域(ドイツ、英国、フランス、イタリア、スペイン、ノルウェー、スウェーデン、デンマーク、フィンランド、その他欧州)別に分類されています。市場予測は数量(トン)単位で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 2025年より高い断熱性能(R値)を義務付ける建築物エネルギー基準

- mRNA系生物製剤向け必須コールドチェーン容量の増強

- 家電製品の国内回帰が国内保護包装需要を押し上げる

- EU「改修波」改修プロジェクトにおけるグレーEPSの採用状況

- 低コストモジュラー住宅プログラム

- 市場抑制要因

- スチレンモノマー価格の変動が原油スプレッドに連動

- 菌糸体および成形パルプ代替品の商業化

- 石油由来ポリマーのスコープ3排出量を膨らませる炭素価格制度

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 輸出入動向

第5章 市場規模と成長予測

- 製品タイプ別

- ホワイトEPS

- グレーおよびシルバーEPS

- エンドユーザー業界別

- 建築・建設

- 電気・電子機器

- 包装

- その他のエンドユーザー産業(農業および自動車産業)

- 地域別

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ノルウェー

- スウェーデン

- デンマーク

- フィンランド

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)**/順位分析

- 企業プロファイル

- Alpek SAB de CV

- Austrotherm

- BASF

- BEWi

- Epsilyte LLC

- Ineos

- Kaneka Corporation

- Ravago

- SABIC

- SIBUR International GmbH

- Sunde Group

- Sunpor

- Synthos

- TotalEnergies

- Versalis S.p.A.