小型ロケットの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Small Launch Vehicle (SLV) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797781

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

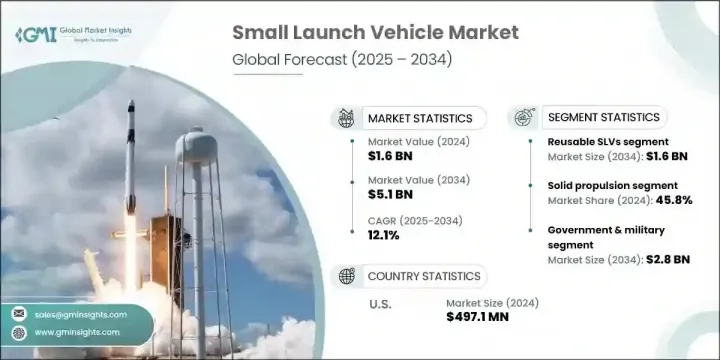

世界の小型ロケット市場は、2024年に16億米ドルと評価され、CAGR12.1%で成長し、2034年には51億米ドルに達すると推定されています。

この市場の拡大は、宇宙の商業化が進み、より低コストで機敏な打上げソリューションへのシフトが大きな原動力となっています。民間企業が衛星配備、分析、宇宙ベースのサービスへの関与を深めるにつれ、業界は技術革新、手頃な価格、サービスのカスタマイズにおいて急速な変化を目の当たりにしています。このように進化する商業宇宙情勢は、通信、地球画像、IoT対応システムなど、より特化したビジネスモデルを生み出し、SLVの需要をさらに促進しています。打ち上げペイロードの共有から、オーダーメイドのスケジュールやカスタマイズされた軌道配信へのシフトは、応答性が高くミッションに特化した機体設計の必要性を押し上げています。

より迅速な展開サイクルと打ち上げ頻度を求める需要の高まりにより、事業者は、迅速なターンアラウンドとミッション制御の強化をサポートする、低コストで適応性の高いシステムを構築する必要に迫られています。民間や政府の宇宙ミッションが、軌道へのオンデマンド・アクセスをますます優先するようになるにつれ、スケーラブルでモジュール化された打上げソリューションの必要性が極めて重要になってきています。事業者は、開発期間を短縮し、統合を合理化するために、リーン生産方式、付加製造方式、および簡素化された設計アーキテクチャにシフトしています。これらの機敏なシステムは、地球観測、防衛通信、災害対応などの一刻を争う用途に不可欠な軌道パラメータの土壇場での調整を可能にしながら、多種多様なペイロードに対応できるように構築されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 16億米ドル |

| 予測金額 | 51億米ドル |

| CAGR | 12.1% |

2024年の市場は、固体推進分野が45.8%のシェアで牽引。固体推進システムは、その信頼性、統合の容易さ、貯蔵の利点から、迅速な対応、軌道下、防衛関連のミッションに依然として好ましい選択肢です。新規参入企業は、設計の複雑さを最小限に抑え、打ち上げ準備を合理化するために、固体ベースのSLVに傾倒しています。プロバイダーは、シンプルさと信頼性が最優先される戦略的な使用事例に固体燃料ロケットを位置づけています。

再使用可能な打上げシステムは、1回あたりの打上げ費用を削減し、所要時間を増加させるために採用されつつあります。再使用型SLV分野は2034年までに16億米ドルに達すると予測されています。多くの企業が、回収、改修、再打ち上げのためのスケーラブルなハードウェアを開発することで、再利用性を重視しています。これらの技術は、廃棄物の削減、運用コストの低減、頻繁な軌道アクセスのための長期的な環境的・経済的持続可能性のサポートに不可欠であることが証明されつつあります。

北米小型ロケット(SLV)市場は2024年に34.6%のシェアを占め、2034年まで11.1%のCAGRで成長すると予測されています。強力な財政支援、官民協力の増加、小型衛星メーカーとオペレーターの強固なエコシステムにより、この地域は世界のSLV産業の最前線にあります。国家安全保障と商業的需要に対応するため、より迅速で柔軟な打上げオプションへのシフトが顕著です。

世界のSLV市場を形成する主要企業には、C6 Launch社、Astra Space社、Agnikul Cosmos社、Interstellar Technologies社、Galactic Energy社、Firefly Aerospace社、CAS Space社、ABL Space Systems社、HyImpulse社、Dawn Aerospace社などがあります。小型ロケット市場で活躍する企業は、技術革新、再利用性、ミッションに特化した構成を中心に取り組みを強化しています。その多くは、モジュール式打ち上げシステムや再利用可能なステージ開発に投資し、費用対効果が高く、頻繁な展開サイクルを提供しています。衛星メーカーや宇宙機関との戦略的提携は、顧客範囲の拡大と信頼性の強化に役立っています。また、コンポーネントの製造から打上げ後のデータサービスまで、すべての工程を管理する垂直統合に注力する企業も増えており、品質の確保、コストの削減、市場投入までの時間の短縮を実現しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 小型衛星と衛星群の需要増加

- 宇宙の商業化の進展

- 費用対効果の高い専用打ち上げサービスの需要

- 防衛および国家安全保障アプリケーションの成長

- 低コスト打ち上げインフラの拡大

- 業界の潜在的リスク&課題

- 新規参入者にとって開発および発売コストが高め

- SLVの積載容量の制限

- 市場機会

- コンステレーションベースの衛星展開に対する需要の急増

- 新興宇宙国におけるSLVの導入拡大

- 再利用可能な技術を統合してコスト効率を高める

- オンデマンドおよび迅速打ち上げサービスの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 国防予算分析

- 世界の防衛費の動向

- 地域防衛予算配分

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 主要な防衛近代化プログラム

- 予算予測(2025-2034)

- 業界の成長への影響

- 国別防衛予算

- サプライチェーンのレジリエンス

- 地政学的分析

- 人材分析

- デジタル変革

- 合併、買収、戦略的提携の情勢

- リスク評価と管理

- 主要契約の締結(2021-2024)

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダーたち

- 課題者たち

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:推進方式別、2021-2034

- 主要動向

- 固体推進

- 液体推進

- ハイブリッド推進

第6章 市場推計・予測:容量別、2021-2034

- 主要動向

- 100kgまで

- 100~500kg

- 500~1000kg

- 1000~2000kg

第7章 市場推計・予測:再利用性別、2021-2034

- 主要動向

- 再利用可能なSLV

- 再利用できないSLV

第8章 市場推計・予測:打ち上げプラットフォーム別、2021-2034

- 主要動向

- 陸上ベース

- 海上ベース

- 空中ベース

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 政府と軍隊

- 防衛機関

- 民間宇宙機関

- 国家安全保障組織

- 公的調査機関および大学

- その他

- 商業用

- 衛星通信事業者

- 宇宙スタートアップ企業と技術実証企業

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界の主要企業

- Rocket Lab

- Virgin

- Relativity Space

- Firefly Aerospace

- Isar Aerospace

- 地域の主要企業

- 北米

- ABL Space Systems

- Astra Space

- X-Bow Systems

- 欧州

- Rocket Factory Augsburg

- Orbex

- Skyrora Limited

- HyImpulse

- PLD Space

- アジア太平洋地域

- Agnikul Cosmos

- Skyroot Aerospace

- CAS Space

- Interstellar Technologies

- 北米

- ニッチプレーヤー/ディスラプター

- Dawn Aerospace

- Galactic Energy

目次

The Global Small Launch Vehicle Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 12.1% to reach USD 5.1 billion by 2034. Expansion in this market is largely driven by the increasing commercialization of space and a shift toward lower-cost and more agile launch solutions. As private entities deepen their involvement in satellite deployment, analytics, and space-based services, the industry is witnessing rapid shifts in innovation, affordability, and service customization. This evolving commercial space landscape is giving rise to more specialized business models across telecommunications, Earth imaging, and IoT-enabled systems, further fueling SLV demand. The shift from shared launch payloads to tailored schedules and customized orbital delivery is pushing the need for responsive and mission-specific vehicle design.

Growing demand for faster deployment cycles and greater launch frequency is compelling operators to create low-cost, adaptable systems that support rapid turnaround and increased mission control. As commercial and governmental space missions increasingly prioritize on-demand access to orbit, the need for scalable, modular launch solutions has become critical. Operators are shifting toward lean manufacturing, additive production methods, and simplified design architectures to reduce development timelines and streamline integration. These agile systems are built to accommodate a wide variety of payloads while enabling last-minute adjustments to orbital parameters, which is essential for time-sensitive applications such as Earth observation, defense communication, and disaster response.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 12.1% |

The solid propulsion segment led the market in 2024 with a 45.8% share. Solid propulsion systems remain a preferred choice for rapid-response, suborbital, and defense-related missions due to their reliability, ease of integration, and storage benefits. New entrants are leaning on solid-based SLVs to minimize design complexity and streamline launch readiness. Providers are positioning solid-fueled vehicles for strategic use cases where simplicity and dependability are top priorities.

The reusable launch systems are increasingly being adopted to cut per-launch expenses and increase turnaround times. The reusable SLV segment is projected to reach USD 1.6 billion by 2034. Many players are focusing on reusability by developing scalable hardware for recovery, refurbishment, and relaunch. These technologies are proving essential in reducing waste, lowering operational costs, and supporting long-term environmental and economic sustainability for frequent orbital access.

North America Small Launch Vehicle (SLV) Market held 34.6% share in 2024 and is projected to grow at a CAGR of 11.1% through 2034. With strong financial backing, increasing government-private sector collaboration, and a robust ecosystem of small satellite manufacturers and operators, the region is at the forefront of the global SLV industry. There's a marked shift toward faster, more flexible launch options catering to national security and commercial demands alike.

Key players shaping the Global Small Launch Vehicle (SLV) Market include C6 Launch, Astra Space, Agnikul Cosmos, Interstellar Technologies, Galactic Energy, Firefly Aerospace, CAS Space, ABL Space Systems, HyImpulse, and Dawn Aerospace. Companies active in the small launch vehicle market are intensifying their efforts around innovation, reusability, and mission-specific configurations. Many are investing in modular launch systems and reusable stage development to offer cost-effective and frequent deployment cycles. Strategic collaborations with satellite manufacturers and space agencies help extend their client reach and bolster credibility. A growing number of firms are also focusing on vertical integration, controlling every step from component fabrication to post-launch data services, ensuring quality, reducing costs, and speeding up time-to-market.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Propulsion type trends

- 2.2.2 Capacity trends

- 2.2.3 Reusability trends

- 2.2.4 Launch platform trends

- 2.2.5 End use trends

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for small satellites and satellite constellations

- 3.2.1.2 Increasing commercialization of space

- 3.2.1.3 Demand for cost-effective and dedicated launch services

- 3.2.1.4 Growth in defense and national security applications

- 3.2.1.5 Expansion of low-cost launch infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and launch costs for new entrants

- 3.2.2.2 Payload capacity limitations of SLVs

- 3.2.3 Market opportunities

- 3.2.3.1 Surge in demand for constellation-based satellite deployments

- 3.2.3.2 Growing adoption of SLVs in emerging space nations

- 3.2.3.3 Integration of reusable technologies to enhance cost efficiency

- 3.2.3.4 Expansion of on-demand and rapid launch services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Propulsion Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Solid propulsion

- 5.3 Liquid propulsion

- 5.4 Hybrid propulsion

Chapter 6 Market Estimates and Forecast, By Capacity, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Upto 100 kg

- 6.3 100-500 kg

- 6.4 500-1000 kg

- 6.5 1000 -2000 kg

Chapter 7 Market Estimates and Forecast, By Reusability, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Reusable SLVs

- 7.3 Non-reusable SLVs

Chapter 8 Market Estimates and Forecast, By Launch Platform, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Land-based

- 8.3 Sea-based

- 8.4 Air-based

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.1.1 Government & Military

- 9.1.2 Defense agencies

- 9.1.3 Civil space agencies

- 9.1.4 National security organizations

- 9.1.5 Public research institutions & universities

- 9.1.6 Others

- 9.2 Commercial

- 9.2.1 Satellite operators

- 9.2.2 Space startups & technology demonstrators

- 9.2.3 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Rocket Lab

- 11.1.2 Virgin

- 11.1.3 Relativity Space

- 11.1.4 Firefly Aerospace

- 11.1.5 Isar Aerospace

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 ABL Space Systems

- 11.2.1.2 Astra Space

- 11.2.1.3 X-Bow Systems

- 11.2.2 Europe

- 11.2.2.1 Rocket Factory Augsburg

- 11.2.2.2 Orbex

- 11.2.2.3 Skyrora Limited

- 11.2.2.4 HyImpulse

- 11.2.2.5 PLD Space

- 11.2.3 APAC

- 11.2.3.1 Agnikul Cosmos

- 11.2.3.2 Skyroot Aerospace

- 11.2.3.3 CAS Space

- 11.2.3.4 Interstellar Technologies

- 11.2.1 North America

- 11.3 Niche Players / Disruptors

- 11.3.1 Dawn Aerospace

- 11.3.2 Galactic Energy

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日