|

市場調査レポート

商品コード

1693952

北米の衛星打ち上げロケット:市場シェア分析、産業動向、成長予測(2025~2030年)North America Satellite Launch Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の衛星打ち上げロケット:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 153 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

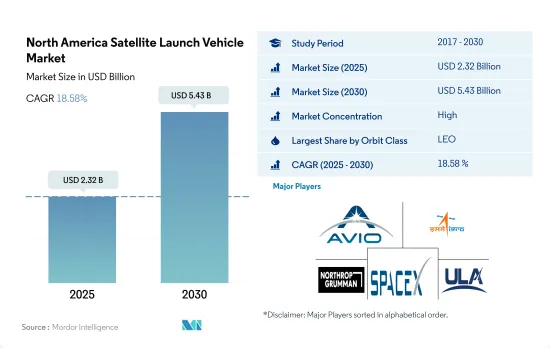

北米の衛星打上げロケット市場規模は2025年に23億2,000万米ドルと推定・予測され、2030年には54億3,000万米ドルに達し、予測期間(2025~2030年)のCAGRは18.58%で成長すると予測されています。

北米地域における軌道打上げシステムの需要増加が成長を補う

- 打ち上げ時、衛星や宇宙船は通常、地球を周回する多くの特別な軌道の1つに配置されます。衛星は、その設計や主要目的によって、さまざまな距離で地球を周回します。それぞれの距離には、カバー範囲の拡大やエネルギー効率の低下など、利点と課題があります。地球中周回軌道にある衛星には、特定の地域をモニタリングするために設計された航法衛星や特殊衛星が含まれます。NASAの地球観測システムチームを含むほとんどの科学衛星は、地球低軌道にあります。

- この領域で製造・打ち上げられる衛星は、それぞれ用途が異なります。例えば、2017~2022年にかけて、MEO軌道で打ち上げられた7機の衛星のうち、ほとんどがナビゲーション/全地球測位目的で製造されました。同様に、GEO軌道の32機の衛星のうち、ほとんどが通信と地球観測の目的で配備されました。打ち上げられた約3,000機のLEO衛星は、北米の組織が所有していました。

- 電子情報、地球科学/気象学、レーザー画像、電子情報、光学画像、気象学などのセグメントで衛星の利用が拡大していることから、北米の衛星打上げロケット市場の需要は拡大し、LEO衛星が大きなシェアを占めると予想されています。2023~2029年にかけて、同市場は213%の急増が見込まれます。

低コスト打上げシステムへの需要の高まりが市場を牽引

- 重い衛星を年に数回、高高度軌道に送ることができる低コストの打上げシステムに対する需要が、北米の政府や商業組織の間で高まっています。中型・大型ロケットによるライドヘイリングサービスを含む小型衛星の打上げ数の増加や小型打上げ能力の拡大により、打上げ価格は前年同期比で低下しています。

- 加えて、衛星製造産業は、軍事モニタリング、通信、ナビゲーションから地球観測に至るまで、様々な用途の衛星の需要に牽引されています。その結果、民間/政府、商業、軍事産業からの衛星需要が増加しています。過去の期間に、この地域では合計4,351機の衛星が打ち上げられました。2021~2022年に打ち上げられた衛星数の伸びは61%で、2021~2020年の伸びは40%でした。

- 宇宙機関や非公開会社はここ数年、衛星打ち上げシステムのコスト削減に努めてきました。多くの市場関係者は、一部または全部の構成段を回収する再使用可能な打上げシステムの開発に投資してきました。市場は、その膨大な製品提供により、少数の参入企業によって支配されています。SpaceXやBlue Originなどの非公開会社が宇宙技術に投資し、産業のイノベーションを推進しています。NASAのような宇宙機関は、この地域での衛星の製造と打ち上げのためにSpaceXのような民間企業と提携しています。同市場は予測期間中に219%急増する見込みで、国別では米国が最大の市場になると予想されています。

北米の衛星打上げロケット市場動向

北米ロケット市場における需要の拡大と競合

- 北米におけるロケットの需要は、主に政府機関、商業衛星事業者、様々なミッションを実施するために宇宙へのアクセスを必要とする科学研究者の要求によってもたらされています。商業的な宇宙探査や観光への関心が高まっており、ロケットプロバイダにとって新たな市場が形成されています。さらに、宇宙探査の非公開化が進む中、再利用可能なロケットや3Dプリンティングなど、企業が宇宙で新技術を開発・展開できるような、費用対効果が高く信頼性の高い打上げサービスへの需要が高まっています。北米にはロケットを所有し、運用している企業がいくつかあります。

- その中でも、打ち上げロケットを所有する大手のスペースXは、先進的なロケットや宇宙船の設計、製造、打ち上げを行う非公開の航空宇宙会社です。同社は現在、北米における打上げサービスのリーディングプロバイダであり、民間と政府顧客のために数多くのミッションを成功させてきました。同社のロケットには、ファルコン9、ファルコンヘビー、スターシップなどがあります。これに続くのがユナイテッド・ローンチ・アライアンスで、政府・民間顧客向けに信頼性が高く、費用対効果の高い宇宙へのアクセスを開発しています。ユナイテッド・ローンチ・アライアンスはアトラスVとデルタIVロケットを運用しています。ブルーオリジンもまた、ニュー・シェパード準軌道ロケットやニュー・グレン軌道ロケットなど、様々な打ち上げロケットを開発しています。ノースロップ・グラマンは世界の航空宇宙・防衛技術企業で、国際宇宙ステーションへの補給ミッションに使用されるアンタレスロケットを運用しています。ロケットラボは小型衛星の打ち上げを専門としています。小型ペイロードの宇宙への頻繁かつ手頃なアクセスを提供するために設計されたエレクトロンロケットを運用しています。

北米の衛星打上げロケット市場における投資機会

- 調査と投資の助成は、北米の衛星打上げロケット市場の革新と成長の主要な推進力となっています。これは、衛星打上げコストを大幅に削減できる可能性のある再使用型ロケットなどの新技術開発に資金を提供するのに役立っています。研究助成金や投資助成金の面では、この地域の政府と民間部門は、宇宙産業における研究と技術革新のために専用の資金を提供しています。北米では、宇宙計画のための政府支出が2022年に約248億米ドルと過去最高を記録しました。例えば、2023年2月まで、NASAは研究助成金として3億3,300万米ドルを分配しました。2022年、米国政府は宇宙プログラムに約620億米ドルを支出し、宇宙産業で世界最高の支出国となりました。

- カナダ宇宙庁(CSA)の予算は控えめで、2022~23年の予算支出見込み額は3億2,900万米ドルでした。2022年4月、アストロサットが収集したデータを使用して星がどのように形成されるかを理解するプロジェクトを支援するため、カナダの大学に総額1億3,283万米ドルの3つの助成金が授与されました。ロケット開発に割り当てられた資金に関しては、2023年度大統領予算要求概要(2022年度~2027年度)において、NASAは138億米ドルを受け取る見込みでした。また、同期間中にSLSプログラムの統合とサポートに5億米ドルを受領する予定でした。これらの投資は、NASAが深宇宙へクルーと大量の貨物を輸送するための大型ロケットの開発を継続するために行われるものです。スペース・ローンチシステム(SLS)プログラムは、人類をかつてないほど遠くまで宇宙へ運ぶ準備を進めています。

北米の衛星打ち上げロケット産業概要

北米の衛星打ち上げロケット市場はかなり統合されており、上位5社で97.58%を占めています。この市場の主要企業は、Avio、Indian Space Research Organisation(ISRO)、Northrop Grumman Corporation、Space Exploration Technologies Corp.、United Launch Alliance, LLC.です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 衛星の小型化

- ロケットの所有者

- 宇宙開発への支出

- 規制の枠組み

- カナダ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 軌道クラス

- GEO

- LEO

- MEO

- ロケット

- 大型

- 小型

- 中型

- 打上げ国

- 米国

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Ariane Group

- Avio

- Indian Space Research Organisation(ISRO)

- Mitsubishi Heavy Industries

- Northrop Grumman Corporation

- Rocket Lab USA, Inc.

- Space Exploration Technologies Corp.

- The Boeing Company

- United Launch Alliance, LLC.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The North America Satellite Launch Vehicle Market size is estimated at 2.32 billion USD in 2025, and is expected to reach 5.43 billion USD by 2030, growing at a CAGR of 18.58% during the forecast period (2025-2030).

Rising demand for orbital launch systems in the North American region has supplemented the growth

- At launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. Satellites orbit the Earth at varying distances depending on their design and primary purpose. Each distance has its own benefits and challenges, including increased coverage and decreased energy efficiency. Satellites in the Medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most scientific satellites, including NASA's Earth Observation System team, are in the low Earth orbit.

- Different satellites manufactured and launched from this region have different applications. For instance, during 2017-2022, out of the seven satellites launched in the MEO orbit, most were built for navigation/global positioning purposes. Similarly, out of the 32 satellites in the GEO orbit, most were deployed for communication and earth observation purposes. Around 3,000 LEO satellites launched were owned by North American organizations.

- The growing use of satellites in areas such as electronic intelligence, Earth science/meteorology, laser imaging, electronic intelligence, optical imaging, and meteorology is expected to drive demand for the North American satellite launch vehicle market, with LEO satellites expected to account for a major share. Between 2023 and 2029, the market is expected to surge by 213%.

Rising demand for low-cost launch systems driving the market

- The demand for low-cost launch systems capable of sending heavy satellites into high-altitude orbits several times a year is growing among governments and commercial organizations in North America. Due to the growing number of small satellite launches, including ride-hailing services on medium and heavy-duty launchers, as well as the growth of small launch capacities, launch prices have decreased Y-o-Y.

- In addition, the satellite manufacturing industry is driven by the demand for satellites for applications ranging from military surveillance, communications, and navigation to earth observation. As a result, the demand for satellites from the civilian/government, commercial, and military industries is increasing. During the historical period, a total of 4,351 satellites were launched in the region. The growth in the number of satellites launched from 2021 to 2022 was 61%, while the growth from 2021 to 2020 was 40%.

- Space agencies and private companies have been trying to reduce the costs of satellite launching systems over the past few years. Many market players have invested in the development of reusable launch systems to recover some or all the component stages. The market is dominated by only a few players due to their huge product offerings. Private companies such as SpaceX and Blue Origin are investing in space technology and driving innovation in the industry. Space organizations such as NASA have partnered with private players like SpaceX for the production and launch of satellites in this region. The market is expected to surge by 219% in the forecast period, and the United States is expected to be the largest country-wise market.

North America Satellite Launch Vehicle Market Trends

Growing demand and competition in the North American launch vehicle market

- The demand for launch vehicles in North America is primarily driven by the requirements of government agencies, commercial satellite operators, and scientific researchers who require access to space to conduct a variety of missions. There is growing interest in commercial space exploration and tourism, which has created a new market for launch providers. Additionally, with the increasing privatization of space exploration, there is a growing demand for cost-effective and reliable launch services that enable companies to develop and deploy new technologies in space, such as reusable rockets and 3D printing. There are several companies that own and operate launch vehicles in North America.

- Among them, a major owner of launch vehicles, SpaceX, is a private aerospace company that designs, manufactures, and launches advanced rockets and spacecraft. It is currently the leading provider of launch services in North America and has conducted numerous successful missions for both commercial and government customers. The company's launch vehicles include Falcon-9, Falcon Heavy, and Starship. It is followed by United Launch Alliance, which develops reliable, cost-effective access to space for government and commercial customers. It operates the Atlas V and Delta IV rockets. Blue Origin is also developing a variety of launch vehicles, including the New Shepard suborbital vehicle and the New Glenn orbital rocket. Northrop Grumman is a global aerospace and defense technology company that operates the Antares rocket, which is used for resupply missions to the International Space Station. Rocket Lab specializes in small satellite launches. It operates the Electron rocket, which is designed to provide frequent and affordable access to space for small payloads.

Investment opportunities in the North American satellite launch vehicle market

- The grant of research and investments has been a major driver of innovations and growth in the satellite launch vehicle market in North America. It has helped fund the development of new technologies, such as reusable launch vehicles, which have the potential to significantly reduce the cost of satellite launches. In terms of research and investment grants, the region's governments and the private sector have dedicated funds for research and innovation in the space industry. In North America, government expenditure for space programs hit a record of approximately USD 24.8 billion in 2022. For instance, till February 2023, NASA distributed USD 333 million as research grants. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender in the space industry in the world.

- The Canadian Space Agency's (CSA) budget was modest, and its estimated budgetary spending for 2022-23 was USD 329 million. In April 2022, three grants totaling USD1 32,831 were awarded to Canadian universities to support projects that use data collected by AstroSat to understand how stars are formed. In terms of funds allocated for launch vehicle development, under the FY 2023 President'S Budget Request Summary from FY 2022-FY 2027, NASA was expected to receive USD 13.8 billion. NASA was also expected to receive USD 500 million for the SLS Program Integration and Support during the same period. These investments are being made as NASA continues the development of a heavy-lift launch vehicle to deliver crew and large volumes of cargo to deep space. The Space Launch System (SLS) program is preparing to carry humans farther into deep space than ever before.

North America Satellite Launch Vehicle Industry Overview

The North America Satellite Launch Vehicle Market is fairly consolidated, with the top five companies occupying 97.58%. The major players in this market are Avio, Indian Space Research Organisation (ISRO), Northrop Grumman Corporation, Space Exploration Technologies Corp. and United Launch Alliance, LLC. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Owner Of Launch Vehicle

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 Canada

- 4.4.2 United States

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Orbit Class

- 5.1.1 GEO

- 5.1.2 LEO

- 5.1.3 MEO

- 5.2 Launch Vehicle Mtow

- 5.2.1 Heavy

- 5.2.2 Light

- 5.2.3 Medium

- 5.3 Country

- 5.3.1 United States

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ariane Group

- 6.4.2 Avio

- 6.4.3 Indian Space Research Organisation (ISRO)

- 6.4.4 Mitsubishi Heavy Industries

- 6.4.5 Northrop Grumman Corporation

- 6.4.6 Rocket Lab USA, Inc.

- 6.4.7 Space Exploration Technologies Corp.

- 6.4.8 The Boeing Company

- 6.4.9 United Launch Alliance, LLC.

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms