有機種子品種市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Organic Seed Varieties Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773392

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

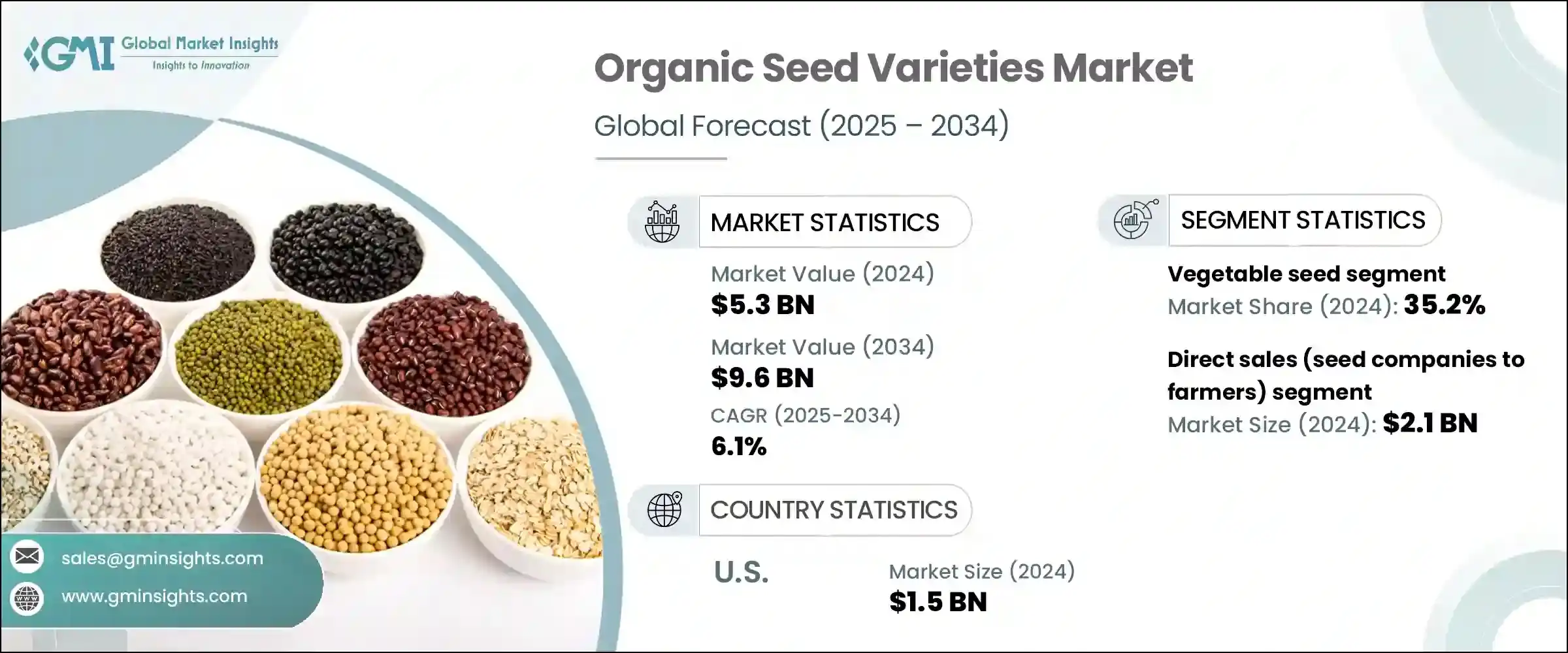

世界の有機種子品種市場は、2024年には53億米ドルとなり、CAGR 6.1%で成長し、2034年には96億米ドルに達すると推定されています。

この成長の原動力となっているのは、健康、持続可能性、食糧安全保障をめぐる消費者の意識の高まりです。より健康的なライフスタイルや環境に配慮した選択にシフトする人が増えるにつれて、有機種子に対する需要は増加の一途をたどっています。有機農業は、生物多様性を保全し、化学物質の使用を削減し、弾力性のある農法を推進するための重要な戦略として勢いを増しています。オーガニック種子は、一般的に家宝品種や特定の気候に適した品種であり、農家の厳しい環境下での作物栽培能力を高めることで、食糧安全保障に貢献しています。また、種子主権の維持にも役立ち、農業における遺伝的多様性の維持にも不可欠です。気候変動は、予測不可能な天候に耐えうるレジリエントな作物の重要性を浮き彫りにし、市場をさらに押し上げています。

さらに、持続可能性と食糧安全保障に対する懸念が高まり続けるなか、世界各国の政府は有機農業への支援を強化しています。これには、有機種子生産を促進し、環境に優しい農法への移行を促進するための資金援助、助成金、政策イニシアチブの増加が含まれます。こうした政府の支援は、有機種子産業の成長を促進し、大規模生産者と零細農家の双方に有機農法への移行を促す上で重要な役割を果たしています。こうした取り組みは、農業の長期的な持続可能性の確保に役立つだけでなく、生物多様性の保全や農業における化学物質の使用量削減といった、より広範な目標にも貢献します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 53億米ドル |

| 予測金額 | 96億米ドル |

| CAGR | 6.1% |

野菜種子(種子会社から農家へ)セグメントは、2024年に35.2%のシェアを占めました。この分野は、有機栽培や地元産の農産物に対する消費者の嗜好の高まりを反映して、今後10年間にCAGR 6.4%で堅調に拡大すると予測されます。健康志向が高まり、無農薬野菜を求める個人が増えるにつれて、家庭菜園家も商業農家も有機野菜の種子品種に目を向けるようになっています。この動向は、より良い栄養と健康的な食習慣を促進するために不可欠と考えられている野菜種子への需要を促進しています。

直接販売セグメントは2024年に21億米ドルと評価され、2034年までCAGR 6.3%で成長すると予想されています。このモデルは、種子生産者が個々の農家独自のニーズに対応したオーダーメイドのソリューションを提供できる、個別サービスの点で支持されています。仲介業者を排除することで、直販は顧客がタイムリーに製品を受け取れるようにし、より強固な関係と高い顧客満足度を育みます。また、専門家によるアドバイス、ロジスティック・サポート、カスタマイズされた配送オプションを提供できることも、直販の成功に貢献しており、大規模な農業経営者にも、小規模な独立農家にも好まれるチャネルとなっています。

米国有機種子品種2024年の市場規模は15億米ドル。有機農産物への需要は、政府の有利な政策や強力な有機サプライチェーンと相まって、この成長を支えています。有機農業の基準が厳しくなるにつれて、多くの農家が規制を遵守するために有機種子生産を採用するようになり、一方、種子会社は製品提供の革新と拡大を続けています。大規模な農業経営と有機農場の増加により、米国市場は継続的に拡大する態勢を整えています。

世界有機種子品種市場の主要企業は、Farm Direct Organic Seeds、Baker Creek Heirloom Seeds、Fedco Seeds、High Mowing Organic Seeds、Johnny's Selected Seedsなどです。有機種子品種市場の各社は、その地位を強化するため、特定の環境条件や消費者の嗜好に対応した、高品質で現地に適合した種子品種の提供に注力しています。種子の保存における革新と、弾力性のある新品種の開発は、各社の戦略の中心となっています。さらに、種子の収量や耐病性を向上させるための研究開発への投資も活発化しています。また、多くの企業が直接販売を通じて農家との関係を強化し、農家のニーズを確実に満たすための個別サービスを提供しています。環境の持続可能性と地域経済の支援は、環境意識の高い消費者と持続可能なソリューションを求める農家の両方にアピールするため、企業にとって重要なセールスポイントとなっています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 北米:オーガニック消費者が主流に

- 欧州:持続可能な食料生産慣行が有機種子の需要を押し上げる

- アジア太平洋:有機農業への変革

- 業界の潜在的リスク&課題

- 有機栽培品種の入手が限られている

- 価格プレミアムと認証負担

- 市場機会

- 作物の多様化とニッチ市場の成長

- 地域繁殖と気候適応

- デジタル化と消費者直販チャネル

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 作物タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- バリューチェーン分析

- 種子の育種と生産

- 認証とテスト

- 流通と小売

- 最終用途セグメント(商業栽培者、小規模農家、家庭菜園家)

- 持続可能性と生物多様性

- 農業生態学と食料安全保障における有機種子の役割

- 生物多様性保全の取り組み

- 種子主権と地域種子システム

- 認証と規制

- USDA NOP認証オーガニック種子

- EU有機認証種子

- その他の国および地域の認定

- 非遺伝子組み換え認証種子

- 種子処理およびコーティング(オーガニック準拠)

- コンプライアンスコストと市場への影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:作物別、2021年~2034年

- 主な傾向

- 野菜の種子

- レタス

- トマト

- ほうれん草

- ニンジン

- キュウリ

- ピーマン

- 穀物の種子

- 小麦

- トウモロコシ

- 米

- 大麦

- オート麦

- キビ

- キノア

- 果物の種子

- メロン

- スイカ

- いちご

- ベリーの品種

- ハーブと花の種子

- バジル

- コリアンダー

- パセリ

- ひまわり

- ジニア

- マリーゴールド

- 油糧種子および代替穀物

- 大豆

- 亜麻

- そば

- アマランサス

- ゴマ

第6章 市場推計・予測:流通チャネル別、2021年~2034年

- 主な傾向

- 直接販売(種子会社から農家へ)

- 小売チャネル(園芸センター、農業用品店)

- オンライン販売およびeコマースプラットフォーム

- 協同組合と購買クラブ

- 卸売業者および機関投資家

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第8章 企業プロファイル

- Adaptive Seeds

- Baker Creek Heirloom Seeds

- Eden Seeds

- Farm Direct Organic Seeds

- Fedco Seeds

- High Mowing Organic Seeds

- Johnny's Selected Seeds

- Kusa Seed Society

- Quality Organic

- Resilient Seeds

- Seed Savers Exchange

- Southern Exposure Seed Exchange

- Victory Seeds

- Vitalis Organic Seeds

目次

The Global Organic Seed Varieties Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 9.6 billion by 2034. This growth is being driven by increasing consumer awareness surrounding health, sustainability, and food security. As more people shift toward healthier lifestyles and environmentally conscious choices, the demand for organic seeds continues to rise. Organic farming is gaining momentum as a key strategy to preserve biodiversity, reduce chemical use, and promote resilient agricultural practices. Organic seeds, typically heirloom varieties or those well-suited to specific climates, contribute to food security by enhancing farmers' ability to grow crops in challenging environments. They also help to maintain seed sovereignty and are vital in maintaining genetic diversity in agriculture. Climate change has highlighted the importance of resilient crops that can endure unpredictable weather, further boosting the market.

Moreover, as concerns about sustainability and food security continue to rise, governments globally are intensifying their support for organic farming. This includes increased funding, grants, and policy initiatives designed to promote organic seed production and facilitate the transition toward eco-friendly agricultural practices. Such government backing plays a critical role in fostering the growth of the organic seed industry, encouraging both large-scale producers and smallholder farmers to shift towards organic farming methods. These efforts not only help ensure the long-term sustainability of agriculture but also support the broader goals of biodiversity conservation and reduced chemical usage in farming.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 6.1% |

The vegetable seed (seed companies to farmers) segment held a 35.2% share in 2024. This segment is projected to expand at a solid CAGR of 6.4% over the next decade, reflecting growing consumer preferences for organic, locally grown produce. As more individuals become health-conscious and seek chemical-free vegetables, both home gardeners and commercial farmers are increasingly turning to organic vegetable seed varieties. This trend is driving demand for vegetable seeds, which are considered essential for promoting better nutrition and healthier eating habits.

The direct sales segment was valued at USD 2.1 billion in 2024 and is expected to grow at a CAGR of 6.3% through 2034. This model is favored for its personalized service, allowing seed producers to offer tailored solutions that address the unique needs of individual farmers. By eliminating intermediaries, direct sales help ensure that customers receive products in a timely manner, fostering stronger relationships and higher levels of customer satisfaction. The ability to offer expert advice, logistical support, and customized delivery options also contributes to the success of direct sales, making it a preferred channel for both large-scale agricultural operations and smaller, independent farmers.

U.S. Organic Seed Varieties Market was valued at USD 1.5 billion in 2024. The demand for organic produce, coupled with favorable government policies and a strong organic supply chain, supports this growth. As organic farming standards become more stringent, many farmers are adopting organic seed production to comply with regulations, while seed companies continue to innovate and expand their product offerings. With large-scale agricultural operations and a growing number of organic farms, the U.S. market is poised for continued expansion.

The top players in the Global Organic Seed Varieties Market include Farm Direct Organic Seeds, Baker Creek Heirloom Seeds, Fedco Seeds, High Mowing Organic Seeds, and Johnny's Selected Seeds. To strengthen their position, companies in the organic seed varieties market are focusing on offering high-quality, locally adapted seed varieties that cater to specific environmental conditions and consumer preferences. Innovations in seed preservation and the development of new, resilient varieties are central to their strategies. Furthermore, companies are increasingly investing in research and development to improve seed yield and disease resistance. Many are also building stronger relationships with farmers through direct sales and providing personalized services to ensure farmers' needs are met. Environmental sustainability and supporting local economies have become key selling points for companies, as they appeal to both eco-conscious consumers and farmers looking for sustainable solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Crop type

- 2.2.3 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 North America: organic consumers are increasingly mainstream

- 3.2.1.2 Europe: sustainable food production practices to boost the demand of organic seeds

- 3.2.1.3 Asia pacific: transformation towards organic agriculture practices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited organic variety availability

- 3.2.2.2 Price premiums and certification burden

- 3.2.3 Market opportunities

- 3.2.3.1 Crop diversification and niche market growth

- 3.2.3.2 Regional breeding and climate adaptation

- 3.2.3.3 Digitalization and direct-to-consumer channels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By crop type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Value chain analysis

- 3.13.1 Seed breeding and production

- 3.13.2 Certification and testing

- 3.13.3 Distribution and retail

- 3.13.4 End use segments (commercial growers, smallholders, home gardeners)

- 3.14 Sustainability and biodiversity

- 3.14.1 Role of organic seed in agroecology and food security

- 3.14.2 Biodiversity conservation initiatives

- 3.14.3 Seed sovereignty and local seed systems

- 3.15 Certification and regulation

- 3.15.1 USDA NOP certified organic seeds

- 3.15.2 EU organic certified seeds

- 3.15.3 Other national and regional certifications

- 3.15.4 Non-GMO verified seeds

- 3.15.5 Seed treatment and coating (Organic-Compliant)

- 3.15.6 Compliance costs and market impact

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Crop Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trend

- 5.2 Vegetable seeds

- 5.2.1 Lettuce

- 5.2.2 Tomato

- 5.2.3 Spinach

- 5.2.4 Carrot

- 5.2.5 Cucumber

- 5.2.6 Bell pepper

- 5.3 Grain seeds

- 5.3.1 Wheat

- 5.3.2 Corn

- 5.3.3 Rice

- 5.3.4 Barley

- 5.3.5 Oats

- 5.3.6 Millet

- 5.3.7 Quinoa

- 5.4 Fruit seeds

- 5.4.1 Melon

- 5.4.2 Watermelon

- 5.4.3 Strawberry

- 5.4.4 Berry varieties

- 5.5 Herb and flower seeds

- 5.5.1 Basil

- 5.5.2 Cilantro

- 5.5.3 Parsley

- 5.5.4 Sunflower

- 5.5.5 Zinnia

- 5.5.6 Marigold

- 5.6 Oilseed and alternative grains

- 5.6.1 Soybean

- 5.6.2 Flax

- 5.6.3 Buckwheat

- 5.6.4 Amaranth

- 5.6.5 Sesame

Chapter 6 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Litres)

- 6.1 Key trend

- 6.2 Direct sales (seed companies to farmers)

- 6.3 Retail channels (garden centres, farm supply stores)

- 6.4 Online sales and e-commerce platforms

- 6.5 Cooperatives and buying clubs

- 6.6 Wholesale and institutional buyers

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Litres)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East & Africa

Chapter 8 Company Profiles

- 8.1 Adaptive Seeds

- 8.2 Baker Creek Heirloom Seeds

- 8.3 Eden Seeds

- 8.4 Farm Direct Organic Seeds

- 8.5 Fedco Seeds

- 8.6 High Mowing Organic Seeds

- 8.7 Johnny's Selected Seeds

- 8.8 Kusa Seed Society

- 8.9 Quality Organic

- 8.10 Resilient Seeds

- 8.11 Seed Savers Exchange

- 8.12 Southern Exposure Seed Exchange

- 8.13 Victory Seeds

- 8.14 Vitalis Organic Seeds

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日