|

市場調査レポート

商品コード

1773350

医療・法律・規制レビューソフトウェアの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Medical, Legal, and Regulatory Review Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 医療・法律・規制レビューソフトウェアの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月27日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

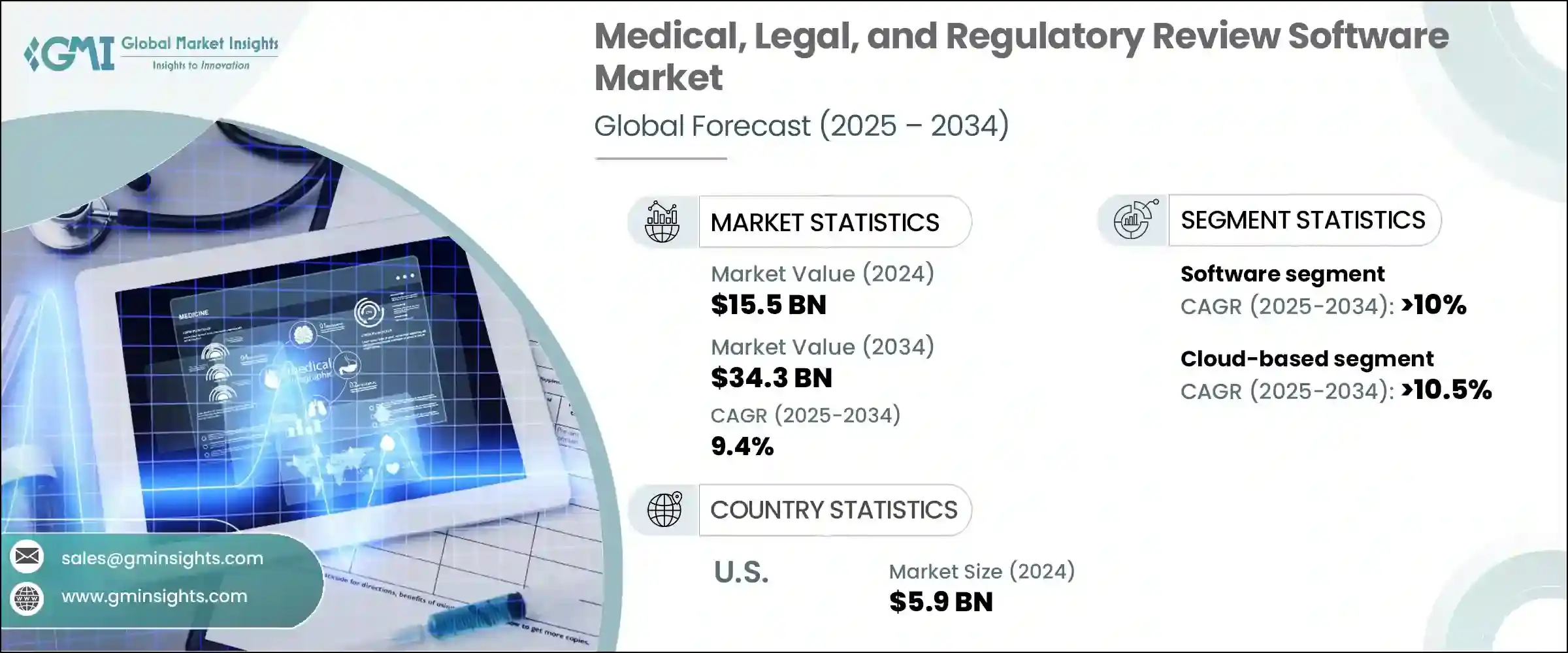

医療・法律・規制レビューソフトウェアの世界市場規模は、2024年に155億米ドルとなり、CAGR9.4%で成長し、2034年までには343億米ドルに達すると予測されています。

この着実な成長軌道は、製薬・ライフサイエンス分野におけるコンプライアンス、協調性、文脈を考慮したコンテンツレビュープロセスに対するニーズの高まりに後押しされています。企業がデジタル戦略を加速させ、複雑な規制の枠組みをナビゲートするにつれて、レビューワークフローを合理化する統合MLRプラットフォームに対する需要が大幅に高まっています。従来、多くのライフサイエンス企業は、手作業、紙ベース、電子メールによるMLRレビュープロセスに依存していました。しかし、このような時代遅れのシステムは、リアルタイムのコラボレーション、AIベースのコンプライアンス検証、自動化された監査証跡を提供するインテリジェントなソフトウェアツールに急速に取って代わられつつあります。これらの機能により、MLRチームは業務効率を高め、法的リスクを低減し、より迅速かつ自信を持って製品を市場に投入できるようになっています。

デジタルマーケティングやマルチチャネルマーケティングがますます推進される中、ライフサイエンス企業は、地域の規制要件に沿いながら、多様なコンテンツ形式を迅速に審査・承認する必要に迫られています。ウェブサイト、電子メール、ソーシャルメディアプラットフォームのコンテンツに関わらず、あらゆるプロモーションや科学的資産が徹底的なコンプライアンスレビューを受けることが重視されるようになっています。MLRソフトウェアシステムは、この複雑性を管理するための集中型プラットフォームとして機能し、コンテンツがパブリックドメインに到達する前に、正確性、合法性、規制遵守を確保します。このようなシステムへの移行は、単なる自動化ではなく、エラーの余地を与えない、速いペースでデジタル接続されたエコシステムの期待に応えることなのです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 155億米ドル |

| 予測金額 | 343億米ドル |

| CAGR | 9.4% |

コンポーネント別では、ソフトウェア分野が2024年の市場セグメンテーションソフトウェア世界市場をリードし、市場総額の約68%を占めました。この分野は2034年までCAGR10%以上で成長すると予測されます。バージョン管理、統合監査機能、共同コンテンツレビュー機能を提供するエンドツーエンドのデジタルツールの採用拡大が、この動向を後押ししています。企業は、世界チーム全体で拡張でき、手作業によるレビューエラーを減らし、リアルタイムのフィードバックループを可能にするクラウドベースのプラットフォームへの投資を増やしています。デジタルトランスフォーメーションを志向する企業は、断片的なシステムから、複数の利害関係者やチームにまたがる大量のコンテンツをサポートする統一されたソフトウェアエコシステムへの移行をさらに促しています。

展開の観点からは、クラウドベースのソリューションが2024年の市場を独占し、総シェアの約64%を占めました。このセグメントのCAGRは、予測期間を通じて10.5%を超えると予測されています。クラウドインフラへの移行が広まったことで、製薬・バイオ企業はコンテンツ管理を一元化し、規制ワークフローを合理化し、社内のITメンテナンスコストを大幅に削減できるようになりました。クラウドプラットフォームは、部署や地域を超えた一貫性のある安全なアクセスを提供し、利害関係者が常に最新の規制ガイダンスに沿った状態を維持できるようにします。企業が新たな市場に進出する際、クラウドベースのMLRツールは、多様で進化するコンプライアンスランドスケープの中で運用するために必要な適応性と応答性を提供します。

機能面では、2024年に規制当局による審査が主要セグメントとして浮上しました。主に科学的信頼性や知的財産の保護に重点を置く法的評価や医学的評価と比較して、規制当局による審査は、地域固有のマーケティング、プロモーション、申請規則との完全な整合性を確保することに主眼が置かれています。こうした規制当局の期待に応えるため、バージョン追跡、コンテンツタグ付け、監査文書化、規制情報システム統合などの自動化機能を備えたソフトウェアソリューションに注目する企業が増えています。これらの機能は、審査サイクルの正確性とスピードを向上させるだけでなく、すべての資料が徹底的に文書化され、容易に検索できるようにすることで、規制当局による監査に備えることもできます。

地域別では、米国が2024年の市場を席巻し、約59億米ドルの売上高を計上しました。この優位性は、連邦政府機関が課す厳しい規制要件に起因しており、コンテンツは一般に普及する前に厳格な検証を受ける必要があります。製薬会社や医療機器メーカーが、法的リスクやコンプライアンス上のリスクを最小限に抑えながら、大量のマーケティング資料や科学的資料を管理しようとしているため、高度なMLRソフトウェアツールへの依存度が高まっています。洗練されたクラウドベースのシステムとAIを統合したプラットフォームが利用可能になったことで、この変革が大きく後押しされています。

MLRレビューソフトウェアの主要ベンダーは、戦略的パートナーシップ、買収、製品イノベーションを積極的に推進し、その機能と市場フットプリントを拡大しています。規制の複雑さが増す中、各社は自動化、トレーサビリティ、リアルタイムのコラボレーションを強化するスマートなプラットフォームを構築するため、研究開発を倍増しています。主な投資分野には、AIを活用したコンプライアンスチェック、モジュール化されたコンテンツワークフロー、世界的な規制のニュアンスに対応できるクラウドネイティブアーキテクチャなどがあります。ベンダーは、世界的な一貫性を維持しながら、管轄地域特有のガイドラインに対応する設定可能なプラットフォームの構築に注力しており、ライフサイエンス企業がリスクを最小限に抑え、承認を迅速化し、地域間の監査に対応できるよう支援しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- デジタル・マルチチャネルマーケティングへの移行

- クラウドベースのプラットフォームの採用増加

- レビュープロセスにおけるAIと自動化

- 中小企業におけるコンプライアンス意識の高まり

- 業界の潜在的リスク・課題

- 複雑な規制状況

- データプライバシーとコンプライアンスリスク

- 市場機会

- 急増する医薬品・バイオテクノロジーのパイプライン

- リモート・分散型コラボレーションの拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- コスト内訳分析

- ソフトウェア開発およびライセンシング費用

- 導入と統合のコスト

- 保守・サポート費用

- サイバーセキュリティとコンプライアンスのコスト

- トレーニングと変更管理コスト

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソフトウェア

- サービス

- プロフェッショナル

- マネージド

第6章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

第7章 市場推計・予測:機能別、2021年~2034年

- 主要動向

- 医学レビュー

- 法務レビュー

- 規制レビュー

第8章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 製薬会社

- バイオテクノロジー企業

- 医療機器メーカー

- 契約調査機関(CRO)

- 規制コンサルティング会社

- ヘルスケアマーケティング代理店

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 3M Health Information Systems

- Allscripts

- Change Healthcare

- Epic Systems

- Experian Health

- GE Healthcare

- Health Catalyst

- IBM Watson Health

- Inovalon Holdings

- LexisNexis Risk Solutions

- McKesson Corporation

- Medtronic

- Nuance Communications

- Optum

- Oracle Health

- Philips Healthcare

- Siemens Healthineers

- Thomson Reuters

- Verisk Analytics

- Wolters Kluwer

The Global Medical, Legal, and Regulatory Review Software Market was valued at USD 15.5 billion in 2024 and is estimated to grow at a CAGR of 9.4% to reach USD 34.3 billion by 2034. This steady growth trajectory is fueled by the rising need for compliant, collaborative, and context-aware content review processes within the pharmaceutical and life sciences sectors. As companies accelerate their digital strategies and navigate complex regulatory frameworks, the demand for integrated MLR platforms that streamline review workflows has grown significantly. Traditionally, many life sciences organizations relied on manual, paper-based, or email-driven MLR review processes. However, those outdated systems are rapidly being replaced by intelligent software tools offering real-time collaboration, AI-based compliance verification, and automated audit trails. These capabilities are helping MLR teams boost operational efficiency, reduce legal exposure, and bring products to market more swiftly and confidently.

With the increasing push for digital and multichannel marketing, life sciences companies are under pressure to rapidly review and approve diverse content formats while staying aligned with regional regulatory requirements. Whether it's content for websites, emails, or social media platforms, there is a growing emphasis on ensuring every promotional or scientific asset undergoes a thorough compliance review. MLR software systems serve as a centralized platform to manage this complexity, ensuring accuracy, legality, and regulatory adherence before any content reaches the public domain. The shift toward these systems is not just about automation; it's about meeting the expectations of a fast-paced, digitally connected ecosystem that leaves no room for error.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.5 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 9.4% |

In terms of components, the software segment led the global MLR review software market in 2024, accounting for nearly 68% of the total market value. This segment is anticipated to grow at a CAGR of over 10% through 2034. The expanding adoption of end-to-end digital tools that offer version control, integrated audit functionality, and collaborative content review features is driving this trend. Enterprises are increasingly investing in cloud-based platforms that can scale across global teams, reduce manual review errors, and enable real-time feedback loops. The preference for digital transformation has further encouraged organizations to move away from fragmented systems toward unified software ecosystems that support higher volumes of content across multiple stakeholders and teams.

From a deployment perspective, cloud-based solutions dominated the market in 2024, capturing approximately 64% of the total share. This segment is projected to register a CAGR exceeding 10.5% throughout the forecast period. The widespread shift to cloud infrastructure is allowing pharmaceutical and biotech companies to centralize content management, streamline regulatory workflows, and significantly reduce internal IT maintenance costs. Cloud platforms provide consistent, secure access across departments and geographies, ensuring that stakeholders remain aligned with current regulatory guidance at all times. As companies expand into new markets, cloud-based MLR tools provide the adaptability and responsiveness needed to operate within diverse and evolving compliance landscapes.

Functionality-wise, regulatory review emerged as the leading segment in 2024. Compared to legal or medical assessments, which primarily focus on scientific credibility or intellectual property protection, regulatory review is centered on ensuring full alignment with region-specific marketing, promotion, and submission rules. To meet these regulatory expectations, more organizations are turning to software solutions equipped with automation capabilities such as version tracking, content tagging, audit documentation, and regulatory information system integration. These features not only improve the accuracy and speed of the review cycle but also prepare organizations for possible regulatory audits by ensuring that all materials are thoroughly documented and easily retrievable.

Geographically, the United States dominated the market in 2024, contributing around USD 5.9 billion in revenue, which translates to a commanding 88.3% share of the North American region. This dominance can be attributed to the stringent regulatory requirements imposed by federal agencies, which demand that content undergo rigorous validation before public dissemination. The reliance on advanced MLR software tools is growing as pharmaceutical and medical device companies seek to manage high volumes of marketing and scientific materials while minimizing legal and compliance risks. The availability of sophisticated cloud-based systems and AI-integrated platforms has significantly supported this transformation.

Leading vendors in the MLR review software landscape are actively pursuing strategic partnerships, acquisitions, and product innovation to expand their capabilities and market footprint. With increasing regulatory complexity, companies are doubling down on R&D to build smarter platforms that support greater automation, traceability, and real-time collaboration. Key areas of investment include AI-powered compliance checks, modular content workflows, and cloud-native architectures that allow companies to adapt to global regulatory nuances. Vendors are focusing on creating configurable platforms that accommodate jurisdiction-specific guidelines while maintaining global consistency, helping life sciences organizations minimize risk, speed up approvals, and stay audit-ready across regions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Functionality

- 2.2.5 Enterprise Size

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift towards digital and multichannel marketing

- 3.2.1.2 Rising adoption of cloud-based platforms

- 3.2.1.3 AI and automation in review processes

- 3.2.1.4 Growing compliance awareness among SMEs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex regulatory landscape

- 3.2.2.2 Data privacy and compliance risks

- 3.2.3 Market opportunities

- 3.2.3.1 Surging pharma and biotech pipelines

- 3.2.3.2 Growing remote and decentralized collaboration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.3.1 Professional

- 5.3.2 Managed

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Functionality, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Medical review

- 7.3 Legal review

- 7.4 Regulatory review

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Pharmaceutical companies

- 9.3 Biotechnology companies

- 9.4 Medical device manufacturers

- 9.5 Contract Research Organizations (CROs)

- 9.6 Regulatory consulting firms

- 9.7 Healthcare marketing agencies

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M Health Information Systems

- 11.2 Allscripts

- 11.3 Change Healthcare

- 11.4 Epic Systems

- 11.5 Experian Health

- 11.6 GE Healthcare

- 11.7 Health Catalyst

- 11.8 IBM Watson Health

- 11.9 Inovalon Holdings

- 11.10 LexisNexis Risk Solutions

- 11.11 McKesson Corporation

- 11.12 Medtronic

- 11.13 Nuance Communications

- 11.14 Optum

- 11.15 Oracle Health

- 11.16 Philips Healthcare

- 11.17 Siemens Healthineers

- 11.18 Thomson Reuters

- 11.19 Verisk Analytics

- 11.20 Wolters Kluwer