強化ミルクの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Fortified Milk Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 245 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773346

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

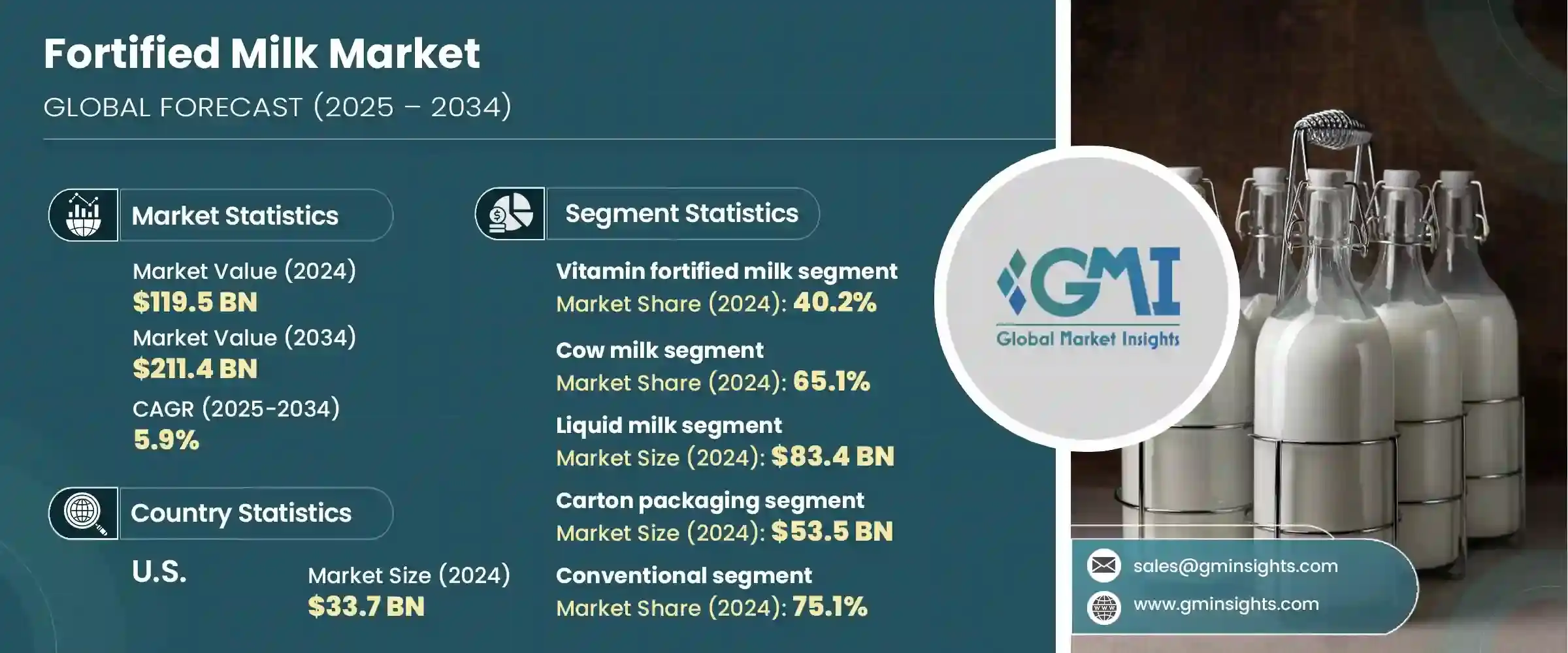

世界の強化ミルク市場は、2024年には1,195億米ドルとなり、CAGR 5.9%で成長し、2034年には2,114億米ドルに達すると推定されています。

この着実な成長の原動力となっているのは、栄養不足に対する意識の高まりと機能性乳製品に対する需要の高まりです。消費者の健康意識が高まるにつれ、ビタミンD、ビタミンA、カルシウム、亜鉛、鉄などの必須微量栄養素を強化した乳製品への志向が高まっています。こうした強化製品は、骨の健康、免疫機能、認知機能の開発をサポートします。パンデミック後の優先順位は免疫力を高める栄養へと大きくシフトし、メーカー各社は幼児から高齢者まであらゆるライフステージに対応する強化ミルクオプションを発売するようになりました。

都市化の進展、可処分所得の増加、公衆衛生イニシアティブが推進する食品強化の取り組みも、特にアフリカとアジアの新興経済諸国を中心に市場を前進させています。強化ミルクは、貧血、骨粗しょう症、ビタミン欠乏症といった広範な栄養問題に対処する上で極めて重要な役割を果たしており、多様な食生活へのアクセスが限られている地域において実用的な解決策を提供しています。また、多くの地域では、学童や妊産婦の健康増進を目的とした大規模な栄養プログラムの主要な構成要素となっており、主流の健康食品としての関連性をさらに高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 1,195億米ドル |

| 予測金額 | 2,114億米ドル |

| CAGR | 5.9% |

ビタミン強化ミルク分野は2024年に40.2%のシェアを占め、2034年までのCAGRは6.1%と予測されます。人気の高まりは、毎日の栄養補給に便利なものを好む消費者の嗜好によるところが大きいです。A、D、B複合体などの必須ビタミンを豊富に含む強化ミルクは、成長期の子供、健康志向の大人、より良い食事バランスを求める妊婦など、健康を重視するターゲットグループに特に魅力的です。こうした栄養素の添加は、牛乳の機能的価値を大幅に高め、より幅広い層にアピールします。

強化ミルク市場の牛乳セグメントは2024年に65.1%のシェアを占め、2034年までのCAGRは5.9%と予測されています。牛乳が広く使用されているのは、その栄養的プロファイルと、世界的に最も親しまれ受け入れられている牛乳の種類としての地位の両方によるものです。牛乳は信頼性の高いタンパク質、カルシウム、ビタミンの供給源であり、栄養強化のための自然な選択肢となっています。オメガ3脂肪酸やミネラルなど、さまざまな栄養添加物との相性の良さは、便利で栄養豊富なベースとしての成長を支えています。

米国強化ミルク2024年の市場規模は337億米ドルで、2034年までのCAGRは6.1%と予想されています。米国は乳製品産業が発達しており、栄養面での健康を重視する人口が多いため、北米の中でも際立っています。同国の消費者は機能性食品を積極的に求めており、強化ミルクは広範な流通チャネルを通じて広く入手可能です。ウェルネス、予防栄養、毎日の健康最適化に対する国民の関心の高まりが、消費者の需要を強化し、製品イノベーションを加速させています。全国的な広告キャンペーンや強化乳製品の利点に関する教育が、採用をさらに後押ししています。

世界の強化ミルク市場を形成している主要企業には、Arla Foods amba、Nestle S.A.、The Coca-Cola Company(Fairlife)、Fonterra Co-operative Group Limited、Danone S.A.などがあります。強化ミルクの主要企業は、市場でのリーダーシップを確固たるものにするため、技術革新、戦略的拡大、ターゲットを絞った健康マーケティングの組み合わせを採用しています。各社は、免疫力、骨強度、総合的な健康を目的とした栄養素に特化した製剤を開発するための研究に投資しています。

多くの企業は、異なる消費者層にアピールするため、年齢をターゲットにした製品ラインを立ち上げています。世界的な流通網、特に新興市場での流通網を拡大することで、これらの企業は未開拓の需要を取り込むことができます。さらに、公衆衛生機関との提携や栄養アウトリーチ・プログラムへの参加は、信頼の構築とブランドのプレゼンス強化に役立っています。環境にやさしいパッケージやクリーンラベルへの取り組みも、進化する消費者の期待に応えるための戦略の一環です。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- 栄養分析と健康効果

- 強化ミルクの栄養成分

- 主要栄養素

- 微量栄養素

- 生理活性化合物

- 対象消費者別の健康効果

- 乳幼児

- 子どもと青少年

- 大人

- お年寄り

- 妊娠中および授乳中の女性

- アスリートとフィットネス愛好家

- 栄養不足への対処

- ビタミンD欠乏症

- カルシウム欠乏症

- 鉄欠乏症

- その他の栄養不足

- 臨床研究と調査結果

- 骨の健康

- 免疫機能

- 認知開発

- その他の健康分野

- 比較分析

- 強化ミルクvs.普通の牛乳

- 強化ミルクvs.植物由来代替品

- 強化ミルクvs.栄養補助食品

- 強化ミルクの栄養成分

- 消費者行動分析

- 消費者の人口統計

- 年齢層分析

- 所得水準分析

- 地理的分布

- 学歴

- 購入決定要因

- 栄養上の利点

- 価格感度

- ブランドロイヤルティ

- パッケージの好み

- 味と風味

- 消費パターン

- 消費頻度

- 機会に基づいた消費

- 季節の変化

- 消費者の認知と認識

- 強化の利点に関する知識

- ラベルの読み取り行動

- 健康に関する主張への信頼

- 消費者セグメンテーション

- 健康志向の消費者

- 価値追求者

- プレミアム購入者

- 利便性を重視する消費者

- 消費者の人口統計

- マーケティングと価格戦略

- ブランドポジショニング

- プレミアムポジショニング

- 価値ポジショニング

- 健康重視のポジショニング

- ターゲット固有のポジショニング

- マーケティングチャネル

- 従来のメディア

- デジタルマーケティング

- ソーシャルメディア戦略

- インフルエンサーマーケティング

- ブランドポジショニング

- 生産・加工分析

- 原材料調達

- 牛乳の調達

- 強化原料の調達

- 品質管理措置

- 強化プロセス

- 直接加算

- マイクロカプセル化

- リポソーム送達

- その他の強化方法

- 加工技術

- 殺菌

- 超高温(UHT)処理

- スプレー乾燥

- その他の加工技術

- 品質保証とテスト

- 栄養安定性試験

- 微生物学的検査

- 官能評価

- 保存期間試験

- 包装技術

- 無菌包装

- ガス置換包装

- アクティブパッケージング

- 持続可能な包装ソリューション

- 原材料調達

- 将来の見通しと戦略的提言

- 市場進化シナリオ

- 楽観的シナリオ

- 現実的なシナリオ

- 悲観的なシナリオ

- 新たな動向

- パーソナライズされた栄養

- クリーンラベル強化

- 新しい送達システム

- デジタル統合

- イノベーションの機会

- 新しい強化成分

- パッケージングの革新

- 加工技術

- 製品の配合

- 戦略的提言

- メーカー向け

- 小売業者向け

- 投資家向け

- 規制当局向け

- 市場進化シナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:強化の種類別、2021~2034年

- 主な傾向

- ビタミン強化ミルク

- ビタミンA

- ビタミンD

- ビタミンB複合体

- ビタミンE

- その他のビタミン

- ミネラル強化ミルク

- カルシウム

- 鉄

- 亜鉛

- その他のミネラル

- タンパク質強化ミルク

- オメガ3強化ミルク

- プロバイオティクス強化ミルク

- マルチ栄養素強化ミルク

- その他の強化の種類

第6章 市場推計・予測:牛乳の種類別、2021~2034年

- 主な傾向

- 牛乳

- 全乳

- 低脂肪牛乳

- スキムミルク

- 水牛のミルク

- ヤギミルク

- A2ミルク

- その他の牛乳の種類

第7章 市場推計・予測:形態別、2021~2034年

- 主な傾向

- 液体ミルク

- 生鮮液体ミルク

- UHTミルク

- フレーバーミルク

- 粉乳

- 全乳粉乳

- 脱脂粉乳

- フレーバーミルクパウダー

- 練乳

- エバミルク

第8章 市場推計・予測:包装形態別、2021~2034年

- 主な傾向

- カートン包装

- テトラパック

- ゲーブルトップ

- その他のカートンの種類

- プラスチックボトル

- ペットボトル

- HDPEボトル

- その他のプラスチックの種類

- ガラス瓶

- ポーチ

- 缶

- その他の梱包タイプ

第9章 市場推計・予測:ターゲット消費者別、2021~2034年

- 主な傾向

- 乳幼児(0~3歳)

- 子供(4~12歳)

- 青少年(13~18歳)

- 成人(19~50歳)

- 高齢者(50歳以上)

- 妊娠中および授乳中の女性

- アスリートとフィットネス愛好家

第10章 市場推計・予測:流通チャネル別、2021~2034年

- 主な傾向

- スーパーマーケットとハイパーマーケット

- コンビニエンスストア

- オンライン小売

- eコマースプラットフォーム

- 消費者直販ウェブサイト

- 専門店

- 薬局・ドラッグストア

- フードサービス

- HoReCa(ホテル・レストラン・カフェ)

- 機関

- その他

第11章 市場推計・予測:性質別、2021~2034年

- 主な傾向

- 従来型

- オーガニック

- ラクトースフリー

第12章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第13章 企業プロファイル

- Alaska Milk Corporation

- Almarai Company

- Arla Foods amba

- Dairy Farmers of America

- Danone S.A.

- Dean Foods Company

- Fonterra Co-operative Group Limited

- Groupe Lactalis

- Gujarat Cooperative Milk Marketing Federation(Amul)

- Inner Mongolia Yili Industrial Group Co., Ltd.

- Meiji Holdings Co., Ltd.

- Mother Dairy Fruit &Vegetable Pvt Ltd

- Nestle S.A

- Parmalat S.p.A.

- Saputo Inc.

- The Coca-Cola Company(Fairlife)

- Vinamilk

目次

The Global Fortified Milk Market was valued at USD 119.5 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 211.4 billion by 2034. This steady growth is being fueled by a heightened awareness of nutritional deficiencies and a rising demand for functional dairy products. As consumer health consciousness broadens, there is a growing inclination toward dairy options enhanced with essential micronutrients like vitamin D, vitamin A, calcium, zinc, and iron. These enriched products support bone health, immune function, and cognitive development. Post-pandemic priorities have shifted significantly toward immune-boosting nutrition, driving manufacturers to launch fortified milk options that cater to every life stage, from young children to the elderly.

Increased urbanization, higher disposable incomes, and food fortification efforts promoted by public health initiatives are also propelling the market forward, particularly across developing economies in Africa and Asia. Fortified milk is playing a pivotal role in addressing widespread nutritional concerns, such as anemia, osteoporosis, and vitamin deficiencies, offering a practical solution in regions with limited access to diverse diets. In many areas, it is also a key component of large-scale nutritional programs designed to improve the well-being of school children and expectant mothers, further reinforcing its relevance as a mainstream health product.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $119.5 Billion |

| Forecast Value | $211.4 Billion |

| CAGR | 5.9% |

Vitamin-enriched milk segment held a 40.2% share in 2024 and is forecasted to grow at a CAGR of 6.1% through 2034. Its rising popularity is largely attributed to consumer preference for convenient sources of daily nutrition. Fortified milk rich in essential vitamins such as A, D, and B-complex is especially appealing to target groups focused on health, including growing children, wellness-minded adults, and expectant mothers seeking better dietary balance. These nutrient additions significantly boost milk's functional value and expand its appeal to broader demographics.

The cow milk segment in the fortified milk market held 65.1% share in 2024 and is projected to grow at a CAGR of 5.9% through 2034. Its widespread use stems from both its nutritional profile and its position as the most familiar and accepted milk type globally. Cow milk offers a reliable source of protein, calcium, and vitamins, making it a natural choice for fortification. Its compatibility with a range of nutritional additives, including omega-3 fatty acids and minerals, supports its continued growth as a convenient and nutrient-rich base.

United States Fortified Milk Market generated USD 33.7 billion in 2024 and is anticipated to grow at a CAGR of 6.1% through 2034. The US market stands out within North America due to its well-developed dairy industry and a population that places a high value on nutritional health. Consumers across the country actively seek functional foods, and fortified milk is widely accessible through extensive distribution channels. Growing public interest in wellness, preventive nutrition, and daily health optimization is reinforcing consumer demand and accelerating product innovation. National advertising campaigns and education on the benefits of fortified dairy have further driven adoption.

Key players shaping the Global Fortified Milk Market include Arla Foods amba, Nestle S.A., The Coca-Cola Company (Fairlife), Fonterra Co-operative Group Limited, and Danone S.A. To solidify their market leadership, top fortified milk companies are employing a combination of innovation, strategic expansion, and targeted health marketing. They are investing in research to develop nutrient-specific formulations aimed at immunity, bone strength, and overall wellness.

Many are launching age-targeted product lines to appeal to different consumer segments. Expanding global distribution networks, especially in emerging markets, allows these companies to capture untapped demand. Additionally, partnerships with public health agencies and participation in nutrition outreach programs help build trust and strengthen brand presence. Eco-friendly packaging and clean-label initiatives are also part of their strategy to meet evolving consumer expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fortification type

- 2.2.3 Milk type

- 2.2.4 Target customer

- 2.2.5 Form

- 2.2.6 Packaging type

- 2.2.7 Distribution channel

- 2.2.8 Nature

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Nutritional analysis & health benefits

- 3.13.1 Nutritional profile of fortified milk

- 3.13.1.1 Macronutrients

- 3.13.1.2 Micronutrients

- 3.13.1.3 Bioactive compounds

- 3.13.2 Health benefits by target consumer

- 3.13.2.1 Infants & toddlers

- 3.13.2.2 Children & adolescents

- 3.13.2.3 Adults

- 3.13.2.4 Elderly

- 3.13.2.5 Pregnant & lactating women

- 3.13.2.6 Athletes & fitness enthusiasts

- 3.13.3 Addressing nutritional deficiencies

- 3.13.3.1 Vitamin d deficiency

- 3.13.3.2 Calcium deficiency

- 3.13.3.3 Iron deficiency

- 3.13.3.4 Other nutritional deficiencies

- 3.13.4 Clinical studies & research findings

- 3.13.4.1 Bone health

- 3.13.4.2 Immune function

- 3.13.4.3 Cognitive development

- 3.13.4.4 Other health areas

- 3.13.5 Comparative analysis

- 3.13.5.1 Fortified milk vs. Regular milk

- 3.13.5.2 Fortified milk vs. Plant-based alternatives

- 3.13.5.3 Fortified milk vs. Dietary supplements

- 3.13.1 Nutritional profile of fortified milk

- 3.14 Consumer behavior analysis

- 3.14.1 Consumer demographics

- 3.14.1.1 Age group analysis

- 3.14.1.2 Income level analysis

- 3.14.1.3 Geographic distribution

- 3.14.1.4 Educational background

- 3.14.2 Purchase decision factors

- 3.14.2.1 Nutritional benefits

- 3.14.2.2 Price sensitivity

- 3.14.2.3 Brand loyalty

- 3.14.2.4 Packaging preferences

- 3.14.2.5 Taste & flavor

- 3.14.3 Consumption patterns

- 3.14.3.1 Frequency of consumption

- 3.14.3.2 Occasion-based consumption

- 3.14.3.3 Seasonal variations

- 3.14.4 Consumer awareness & perception

- 3.14.4.1 Knowledge of fortification benefits

- 3.14.4.2 Label reading behavior

- 3.14.4.3 Trust in health claims

- 3.14.5 Consumer segmentation

- 3.14.5.1 Health-conscious consumers

- 3.14.5.2 Value seekers

- 3.14.5.3 Premium buyers

- 3.14.5.4 Convenience-oriented consumers

- 3.14.1 Consumer demographics

- 3.15 Marketing & pricing strategies

- 3.15.1 Brand positioning

- 3.15.1.1 Premium positioning

- 3.15.1.2 Value positioning

- 3.15.1.3 Health-focused positioning

- 3.15.1.4 Target-specific positioning

- 3.15.2 Marketing channels

- 3.15.2.1 Traditional media

- 3.15.2.2 Digital marketing

- 3.15.2.3 Social media strategies

- 3.15.2.4 Influencer marketing

- 3.15.1 Brand positioning

- 3.16 Production & processing analysis

- 3.16.1 Raw material sourcing

- 3.16.1.1 Milk sourcing

- 3.16.1.2 Fortification ingredients sourcing

- 3.16.1.3 Quality control measures

- 3.16.2 Fortification process

- 3.16.2.1 Direct addition

- 3.16.2.2 Microencapsulation

- 3.16.2.3 Liposomal delivery

- 3.16.2.4 Other fortification methods

- 3.16.3 Processing technologies

- 3.16.3.1 Pasteurization

- 3.16.3.2 Ultra-High Temperature (UHT) processing

- 3.16.3.3 Spray drying

- 3.16.3.4 Other processing technologies

- 3.16.4 Quality assurance & testing

- 3.16.4.1 Nutrient stability testing

- 3.16.4.2 Microbiological testing

- 3.16.4.3 Sensory evaluation

- 3.16.4.4 Shelf-life testing

- 3.16.5 Packaging technologies

- 3.16.5.1 Aseptic packaging

- 3.16.5.2 Modified atmosphere packaging

- 3.16.5.3 Active packaging

- 3.16.5.4 Sustainable packaging solutions

- 3.16.1 Raw material sourcing

- 3.17 Future outlook & strategic recommendations

- 3.17.1 Market evolution scenario

- 3.17.1.1 Optimistic scenario

- 3.17.1.2 Realistic scenario

- 3.17.1.3 Pessimistic scenario

- 3.17.2 Emerging trends

- 3.17.2.1 Personalized nutrition

- 3.17.2.2 Clean label fortification

- 3.17.2.3 Novel delivery systems

- 3.17.2.4 Digital integration

- 3.17.3 Innovation opportunities

- 3.17.3.1 New fortification ingredients

- 3.17.3.2 Packaging innovations

- 3.17.3.3 Processing technologies

- 3.17.3.4 Product formulations

- 3.17.4 Strategic recommendations

- 3.17.4.1 For manufacturers

- 3.17.4.2 For retailers

- 3.17.4.3 For investors

- 3.17.4.4 For regulatory bodies

- 3.17.1 Market evolution scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Fortification Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trend

- 5.2 Vitamin fortified milk

- 5.2.1 Vitamin A

- 5.2.2 Vitamin D

- 5.2.3 Vitamin B Complex

- 5.2.4 Vitamin E

- 5.2.5 Other vitamins

- 5.3 Mineral fortified milk

- 5.3.1 Calcium

- 5.3.2 Iron

- 5.3.3 Zinc

- 5.3.4 Other minerals

- 5.4 Protein fortified milk

- 5.5 Omega-3 fortified milk

- 5.6 Probiotic fortified milk

- 5.7 Multi-nutrient fortified milk

- 5.8 Other fortification types

Chapter 6 Market Estimates & Forecast, By Milk Type, 2021-2034 (USD Billion) (Thousand Litres)

- 6.1 Key trend

- 6.2 Cow milk

- 6.2.1 Whole milk

- 6.2.2 Semi-skimmed milk

- 6.2.3 Skimmed milk

- 6.3 Buffalo milk

- 6.4 Goat milk

- 6.5 A2 milk

- 6.6 Other milk types

Chapter 7 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Thousand Litres)

- 7.1 Key trend

- 7.2 Liquid milk

- 7.2.1 Fresh liquid milk

- 7.2.2 UHT milk

- 7.2.3 Flavored milk

- 7.3 Powdered milk

- 7.3.1 Whole milk powder

- 7.3.2 Skimmed milk powder

- 7.3.3 Flavored milk powder

- 7.4 Condensed milk

- 7.5 Evaporated milk

Chapter 8 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion) (Thousand Litres)

- 8.1 Key trend

- 8.2 Carton packaging

- 8.2.1 Tetra pak

- 8.2.2 Gable top

- 8.2.3 Other carton types

- 8.3 Plastic bottles

- 8.3.1 Pet bottles

- 8.3.2 HDPE bottles

- 8.3.3 Other plastic types

- 8.4 Glass bottles

- 8.5 Pouches

- 8.6 Cans

- 8.7 Other packaging types

Chapter 9 Market Estimates & Forecast, By Target Consumer, 2021-2034 (USD Billion) (Thousand Litres)

- 9.1 Key trend

- 9.2 Infants & toddlers (0-3 years)

- 9.3 Children (4-12 years)

- 9.4 Adolescents (13-18 years)

- 9.5 Adults (19-50 years)

- 9.6 Elderly (above 50 years)

- 9.7 Pregnant & lactating women

- 9.8 Athletes & fitness enthusiasts

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Litres)

- 10.1 Key trend

- 10.2 Supermarkets & hypermarkets

- 10.3 Convenience stores

- 10.4 Online retail

- 10.4.1 E-commerce platforms

- 10.4.2 Direct-to-consumer websites

- 10.5 Specialty stores

- 10.6 Pharmacies & drug stores

- 10.7 Foodservice

- 10.7.1 HoReCa (Hotels, Restaurants, Cafes)

- 10.7.2 Institutional

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Nature, 2021-2034 (USD Billion) (Thousand Litres)

- 11.1 Key trend

- 11.2 Conventional

- 11.3 Organic

- 11.4 Lactose-free

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Litres)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Rest of Europe

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Rest of Asia Pacific

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Rest of Latin America

- 12.6 Middle East & Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

- 12.6.4 Rest of Middle East & Africa

Chapter 13 Company Profiles

- 13.1 Alaska Milk Corporation

- 13.2 Almarai Company

- 13.3 Arla Foods amba

- 13.4 Dairy Farmers of America

- 13.5 Danone S.A.

- 13.6 Dean Foods Company

- 13.7 Fonterra Co-operative Group Limited

- 13.8 Groupe Lactalis

- 13.9 Gujarat Cooperative Milk Marketing Federation (Amul)

- 13.10 Inner Mongolia Yili Industrial Group Co., Ltd.

- 13.11 Meiji Holdings Co., Ltd.

- 13.12 Mother Dairy Fruit & Vegetable Pvt Ltd

- 13.13 Nestle S.A

- 13.14 Parmalat S.p.A.

- 13.15 Saputo Inc.

- 13.16 The Coca-Cola Company (Fairlife)

- 13.17 Vinamilk

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 245 Pages

- 納期

- 2~3営業日