|

市場調査レポート

商品コード

1773330

アイウェア包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Eyewear Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| アイウェア包装の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月19日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

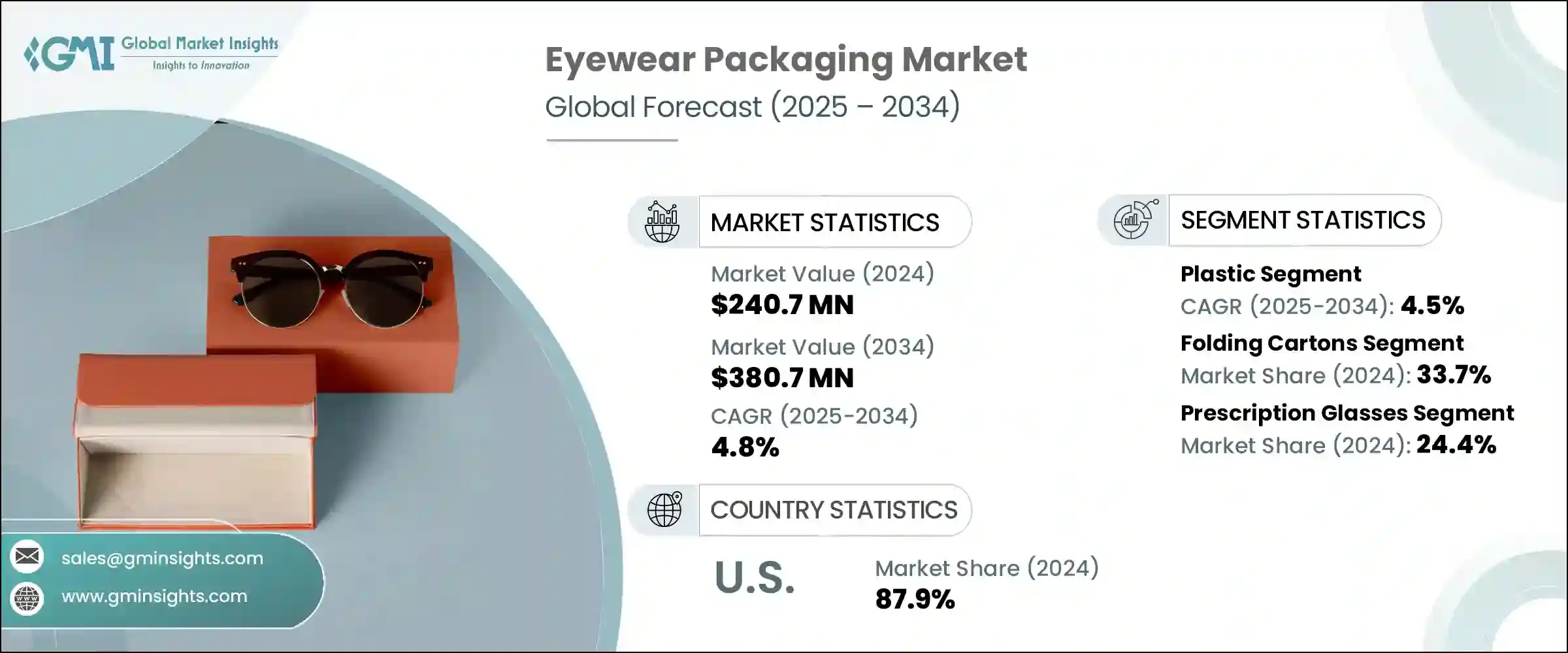

アイウェア包装の世界市場は、2024年には2億4,070万米ドルとなり、CAGR4.8%で成長し、2034年までには3億8,070万米ドルに達すると予測されています。

この成長を後押ししているのは、ファッション用と処方箋入りのアイウエアの両方の需要が増加していることと、販売チャネルとしてeコマースが急速に台頭していることです。スクリーンの使用頻度の増加、視力矯正の必要性、ファッション性の高いアクセサリーとしてのアイウェアの進化などの要因により、アイウェアに依存する層が拡大しています。その結果、ブランドアイデンティティを反映し、プレゼンテーションを高め、高級品を保護する高品質パッケージのニーズが著しく高まっています。ブランドは、このような期待の変化に対応し、競合市場情勢の中で顧客ロイヤルティを強化するために、視覚的な魅力と構造的な完全性を融合させたパッケージに注目しています。

オンライン小売の優位性の高まりは、アイウェア製品の販売方法を再構築し、耐久性があり、視覚に訴えるパッケージへの需要を高めています。製品の破損を減らし、消費者直販チャネルでの開封体験を向上させるためには、ブランドを重視した保護的なデザインが不可欠となっています。また、環境に配慮したソリューションへの選好も高まっており、リサイクル可能で持続可能な素材を使用したパッケージへのシフトが進んでいます。ミニマリストの美学と責任を持って調達された素材の統合は、世界の選好の変化とコンプライアンス要件を反映しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 2億4,070万米ドル |

| 予測金額 | 3億8,070万米ドル |

| CAGR | 4.8% |

紙・板紙分野は、2034年までに1億430万米ドルに達すると予想されています。リサイクル可能性、軽量性、持続可能な調達が優先事項となる中、紙ベースのパッケージングが人気を集めています。これらの素材は、外装パッケージや店内ディスプレイに広く使用されており、環境意識の高まる消費者層とブランドの調和に役立っています。FSC認証ボードやクリーンなデザインを取り入れる企業が増えており、製品の見た目を美しく保ちながら環境への責任を高めています。

アイウェア包装市場の折りたたみ紙器部門は、2024年には33.7%のシェアを占めました。費用対効果と汎用性で知られる折りたたみ式カートンは、小売店でもオンラインショップでも、二次包装の選択肢として好まれています。これらのカートンはブランディングのための大きなスペースを提供し、カスタマイズが容易で、折りたたみ可能で軽量であるため持続可能な物流をサポートします。このカートンの使用は、出荷と棚陳列の効率化により、大量販売において特に顕著です。

米国のアイウェア包装市場は2024年に87.9%のシェアを獲得しました。米国の市場動向は、高級包装、持続可能性、オンラインショッピング体験の向上に対する消費者の選好によって形成されています。eコマースが繁栄を続ける中、機能的でスタイリッシュなパッケージへのニーズは、配送中の保護を確保すると同時に、魅力的な顧客とのインタラクションを提供することで着実に高まっています。パッケージングイノベーションは、成熟した要求の厳しいマーケットプレースにおける差別化のツールになりつつあります。

アイウェア包装市場で活躍する主要企業には、Giorgio Fedon and Figli、Kling、King Home Printing、Ibex Packaging、Box Muse、Gatto Astucci、Classic Packagingなどがあります。アイウェア包装業界で競争力を確保するため、大手企業は持続可能性、カスタマイズ、高度なデザイン技術に投資しています。多くの企業は、環境規制や消費者の期待に応えるため、生分解性やリサイクル可能な包装材へとシフトしています。ブランドの差別化は、製品のアイデンティティを反映した、パーソナライズされた高級感あふれるパッケージングによって達成されます。特にオンライン注文の場合、輸送中の耐久性を確保するため、企業は構造設計能力を強化しています。眼鏡メーカーや消費者直販ブランドとの提携は、顧客基盤の強化に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 持続可能で環境に優しい包装の需要の高まり

- ファッションと処方箋の分野でアイウェアの売上が増加

- eコマースの流通チャネルの拡大

- 高級ブランドとデザイナーブランドのカスタマイズ動向アイウェア包装

- プレミアム化とブランド差別化への重点化

- 業界の潜在的リスク・課題

- 持続可能なカスタムパッケージソリューションの高コスト

- 複数の市場にわたる規制遵守の課題

- 市場機会

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 過去の価格分析(2021年~2024年)

- 価格動向の要因

- 地域による価格差

- 価格予測(2025年~2034年)

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 持続可能な材料の評価

- カーボンフットプリント分析

- 循環型経済の実現

- 持続可能性の認証と基準

- 持続可能性ROI分析

- 世界の消費者感情分析

- 特許分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 市場集中分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展、2021年~2024年

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- プラスチック

- 紙と板紙

- 金属

- レザー

- その他

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 折りたたみカートン

- 硬質箱/ケース

- ポーチ

- その他

第7章 市場推計・予測:アイウェア別、2021年~2034年

- 主要動向

- 処方眼鏡

- サングラス

- スポーツアイウェア

- 安全/産業用メガネ

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Box Muse

- Classic Packaging

- Gatto Astucci

- Giorgio Fedon and Figli

- Ibex Packaging

- King Home Printing

- Kling

- Lsuny Company

- Marber

- Packman Packaging

- Packtek

- Processo Plast Enterprise

- Rongyu Packing

- Salazar Packaging

The Global Eyewear Packaging Market was valued at USD 240.7 million in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 380.7 million by 2034. This growth is being propelled by increasing demand for both fashion and prescription eyewear, alongside the rapid rise of e-commerce as a dominant sales channel. A wider demographic now relies on eyewear due to factors like increased screen usage, vision correction needs, and the evolution of eyewear into a fashion-forward accessory. As a result, the need for high-quality packaging that reflects brand identity, elevates presentation, and protects premium products has grown significantly. Brands are focusing on packaging that merges visual appeal with structural integrity to meet these shifting expectations and reinforce customer loyalty in a competitive market landscape.

The growing dominance of online retail has reshaped how eyewear products are sold, increasing the demand for durable and visually appealing packaging. Protective, brand-focused designs are now essential to reduce product damage and boost unboxing experiences in direct-to-consumer channels. There is also a rising preference for eco-conscious solutions, which is driving a shift toward recyclable and sustainable materials in packaging. The integration of minimalist aesthetics and responsibly sourced materials reflects changing global preferences and compliance requirements.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $240.7 Million |

| Forecast Value | $380.7 Million |

| CAGR | 4.8% |

The paper and paperboard segment is expected to reach USD 104.3 million by 2034. With recyclability, lightweight, and sustainable sourcing becoming priorities, paper-based packaging is gaining popularity. These materials are used widely for exterior packaging and in-store displays, helping brands align with the growing eco-conscious consumer segment. Companies are increasingly incorporating FSC-certified boards and clean designs to enhance environmental responsibility while keeping their products visually appealing.

The folding cartons segment in the eyewear packaging market held a 33.7% share in 2024. Known for their cost-effectiveness and versatility, folding cartons remain a preferred secondary packaging choice in both retail and online settings. These cartons offer substantial space for branding, are easy to customize, and support sustainable logistics due to their collapsible and lightweight nature. Their use is particularly prominent in high-volume sales due to the efficiency they bring in shipping and shelf display.

United States Eyewear Packaging Market captured an 87.9% share in 2024. Market trends in the U.S. are being shaped by consumer preferences for premium packaging, sustainability, and enhanced online shopping experiences. As e-commerce continues to thrive, the need for functional and stylish packaging ensures protection during delivery, while offering an engaging customer interaction is growing steadily. Packaging innovation is becoming a tool for differentiation in a mature and demanding marketplace.

Key companies active in the Eyewear Packaging Market include Giorgio Fedon and Figli, Kling, King Home Printing, Ibex Packaging, Box Muse, Gatto Astucci, and Classic Packaging. To secure a competitive position in the eyewear packaging industry, leading players are investing in sustainability, customization, and advanced design technologies. Many companies are shifting toward biodegradable and recyclable packaging materials to meet environmental regulations and consumer expectations. Brand differentiation is achieved through personalized and luxury-inspired packaging that reflects the product's identity. Firms are enhancing structural design capabilities to ensure durability during shipping, especially for online orders. Partnerships with eyewear manufacturers and direct-to-consumer brands help strengthen their client base.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Product Type trends

- 2.2.3 Eyewear trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable and eco-friendly packaging

- 3.2.1.2 Growth in eyewear sales across fashion and prescription segments

- 3.2.1.3 Expansion of e-commerce distribution channels

- 3.2.1.4 Customization trends in luxury and designer eyewear packaging

- 3.2.1.5 Increasing focus on premiumization and brand differentiation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of sustainable and custom packaging solutions

- 3.2.2.2 Regulatory compliance challenges across multiple markets

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability roi analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&d

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Material,2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Paper & paperboard

- 5.4 Metal

- 5.5 Leather

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Folding cartons

- 6.3 Rigid boxes/cases

- 6.4 Pouches

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Eyewear, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Prescription glasses

- 7.3 Sunglasses

- 7.4 Sports eyewear

- 7.5 Safety/industrial glasses

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Box Muse

- 9.2 Classic Packaging

- 9.3 Gatto Astucci

- 9.4 Giorgio Fedon and Figli

- 9.5 Ibex Packaging

- 9.6 King Home Printing

- 9.7 Kling

- 9.8 Lsuny Company

- 9.9 Marber

- 9.10 Packman Packaging

- 9.11 Packtek

- 9.12 Processo Plast Enterprise

- 9.13 Rongyu Packing

- 9.14 Salazar Packaging