ソースおよび調味料市場の機会、成長要因、業界動向分析、ならびに2025年から2034年までの予測

Sauces and Condiments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1871310

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

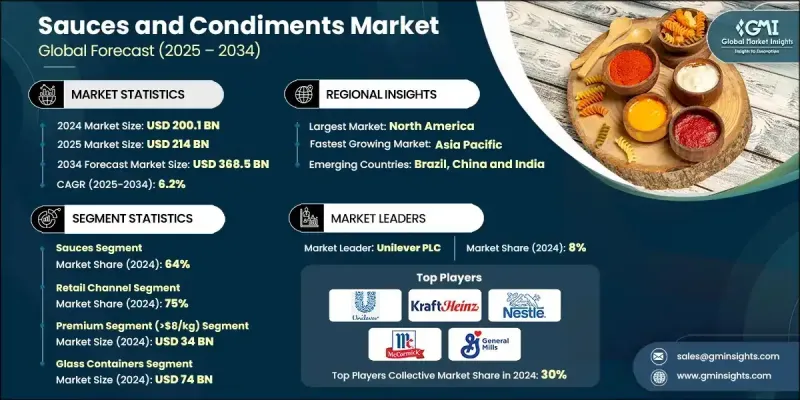

世界のソース・調味料市場は、2024年に2,001億米ドルと評価され、2034年までにCAGR6.2%で成長し、3,685億米ドルに達すると予測されております。

この成長は、消費者の利便性への嗜好の高まりと、より豊かな食体験を求める傾向によって牽引されています。多忙なライフスタイルと世界的な味覚の多様化に伴い、多くの消費者が手軽に食事を豊かにする即席ソースや調味料を好むようになりました。家庭料理や食事の準備の増加動向がさらに需要を後押ししており、メーカーはより良い味と健康効果のためのレシピの再構築、新素材の探求、進化する消費者のニーズに合わせた包装の改善といった革新を促されています。これらの要因が市場を前進させています。しかしながら、新興ブランドや老舗企業からの競合激化により、積極的な価格設定、斬新な製品、強力なマーケティング戦略で市場に参入するプレイヤーが増えるにつれ、利益率に圧力がかかっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025-2034 |

| 開始時価値 | 2,001億米ドル |

| 予測金額 | 3,685億米ドル |

| CAGR | 6.2% |

さらに、プライベートブランド製品の普及により、低価格オプションを求める予算重視の消費者層が拡大しており、ブランドソースメーカーは市場シェアと収益性の維持に課題を抱えています。これらのプライベートブランドは価格競争だけでなく、品質・味・包装の改善に注力し、確立されたブランドとの差を縮めつつあります。小売業者は自社製品ラインに多くの棚スペースと可視性を提供し、プロモーションやロイヤルティインセンティブを通じて顧客の店舗ブランド調味料への選好を促進しています。その結果、既存企業は製品の差別化、製品ラインの革新、そして風味プロファイルの向上、よりクリーンな原材料表示、持続可能な包装を通じてプレミアム価格設定の正当化を迫られています。プライベートブランドの存在感の高まりは競合情勢を変えつつあり、伝統的なブランドは変化し続ける価格に敏感な市場において、自らのポジショニング戦略を見直すことを余儀なくされています。

ソースセグメントは2024年に64%のシェアを占め、2034年までCAGR 5.4%で成長すると予測されています。ソース・調味料市場は引き続き強い勢いを維持しており、現在では主に「ソース」と「調味料」の二大カテゴリーに分類されます。ソースセグメントでは、多様で大胆な味体験を求める消費者の需要の高まりを背景に、多くのイノベーションが生まれています。利便性も主要な促進要因であり、より多くの家庭や外食産業関係者が、調理を簡素化する世界各国の味を再現した即席ソースを選択しています。マリネやグレービーソースからパスタソース、炒め物用ソースに至るまで、これらの製品は、最小限の手間で国際的な料理を探求しつつ日常の食事を格上げしたいと考える現代の消費者にとって、必須の食品庫の定番品となっています。

小売チャネルは2024年に75%のシェアを獲得し、2025年から2034年にかけてCAGR 6.9%での成長が見込まれています。世界的に、ソース・調味料業界は小売と外食産業のチャネルに区分され、いずれも市場の全体的な方向性を形作る上で重要な役割を果たしています。消費者が利便性、品揃え、プレミアム商品の選択肢をますます求める中、小売は依然として主要な購買経路です。スーパーマーケット、ハイパーマーケット、オンラインプラットフォームは、多様な食の嗜好や食事ニーズに応える幅広いソース・調味料への主要なアクセスポイントとなっています。電子商取引やオンライン食料品購入の台頭は、ブランドがリーチを拡大し、商品提供をパーソナライズし、ターゲットを絞ったデジタルマーケティング戦略を通じて顧客と関わることを可能にすることで、小売売上を大幅に強化しました。

北米のソースおよび調味料市場は、2024年に26%のシェアを占めました。多文化の人口、世界的な旅行やメディア消費の普及により、国際的な味の人気が高まっています。この傾向は、さまざまなスパイシーで大胆な調味料の消費の増加に反映されています。ソーシャルメディアが料理のトレンドに与える影響力の急増により、アメリカの消費者にとって国際的なソースがより入手しやすくなり、人気が高まり、新しくエキゾチックな味への需要が加速しています。

世界のソースおよび調味料市場をリードする主要企業には、Conagra Brands、Nestle、McCormick &Company、The Kraft Heinz Company、Mars, Incorporated、Berner Foods、Kikkoman Corporation、Unilever、Bay Valley、Casa Fiesta、Fuchs Gewurze GmbH、Lee Kum Kee、Hormel Foods Corporation、Huy Fong Foodsなどがあります。ソースおよび調味料業界の企業は、市場での存在感を強化するために、いくつかの戦略的アプローチを採用しています。製品革新は最優先事項であり、各社は、変化する消費者の嗜好に応えるため、より健康的で、すべて天然の、特殊なソースを絶えず開発しています。また、環境目標に沿い、環境意識の高い購入者にアピールするため、持続可能で環境に優しい包装ソリューションにも多額の投資を行っています。従来の小売チャネルとEコマースチャネルの両方を通じて流通ネットワークを拡大することで、より広範な市場へのリーチとアクセスが可能になります。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 健康とウェルネスの変革

- プレミアム化と職人技の潮流

- アジア太平洋地域の経済発展

- 業界の潜在的リスク&課題

- 原材料コストの変動性

- プライベートブランド競合の激化

- 市場機会

- 電子商取引チャネルの開発

- 業界再編とM&Aによる価値創造

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントへの配慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協力関係

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- ソース類

- テーブルソース

- ケチャップ・トマトソース

- 醤油及びアジアのソース類

- ホットソース・チリソース

- 特製テーブルソース

- 調理用ソース

- パスタソース

- 炒め物・アジア料理用ソース

- カレー&インド風ソース

- その他の調理用ソース

- プレミアム/職人技のソース

- テーブルソース

- 調味料

- スプレッド&ドレッシング

- マヨネーズ及びマヨネーズベース製品

- マスタード

- サラダドレッシング

- 漬物類

- ピクルス・レリッシュ

- オリーブとケイパー

- 酢類・特殊調味料

- スプレッド&ドレッシング

第6章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 小売チャネル

- 近代小売

- ハイパーマーケット・スーパーマーケット

- コンビニエンスストア

- ホールセールクラブ

- 伝統的な流通形態

- 独立系食料品店

- 専門食品店

- 電子商取引

- 純粋な電子商取引

- 小売業者オンラインプラットフォーム

- 近代小売

- 外食産業向け流通チャネル

- クイックサービスレストラン(QSR)

- フルサービスレストラン

- 機関向け(学校、病院、企業向け)

- 食品加工・製造

第7章 市場推計・予測:価格帯別、2021-2034

- 主要動向

- プレミアムセグメント(8米ドル/kg超)

- 職人技/クラフトブランド

- オーガニック/ナチュラル

- グルメ/スペシャリティ

- メインストリームセグメント(3~8ドル/kg)

- ナショナルブランド

- 地域ブランド

- バリューセグメント(3ドル未満/kg)

- プライベートブランド

- 低価格ブランド

第8章 市場推計・予測:包装タイプ別、2021-2034

- 主要動向

- ガラス容器

- プラスチック容器

- 金属/アルミニウム(缶、チューブ)

- フレキシブル包装(パウチ、サシェ)

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Unilever PLC

- Kraft Heinz Company

- Nestle S.A.

- McCormick &Company

- General Mills

- Kikkoman Corporation

- Lee Kum Kee

- Conagra Brands

- Campbell Soup Company

- Mizkan Holdings

- Barilla Group

- Orkla ASA

- Develey Senf &Feinkost

- Premier Foods

- Foshan Haitian Flavouring &Food

- Ajinomoto Co., Inc.

- Grupo Herdez

- La Costena

- Borges International Group

- Yeo Hiap Seng

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日