化学と石油化学の電気集塵装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Chemicals and Petrochemicals Electrostatic Precipitator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 121 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773219

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

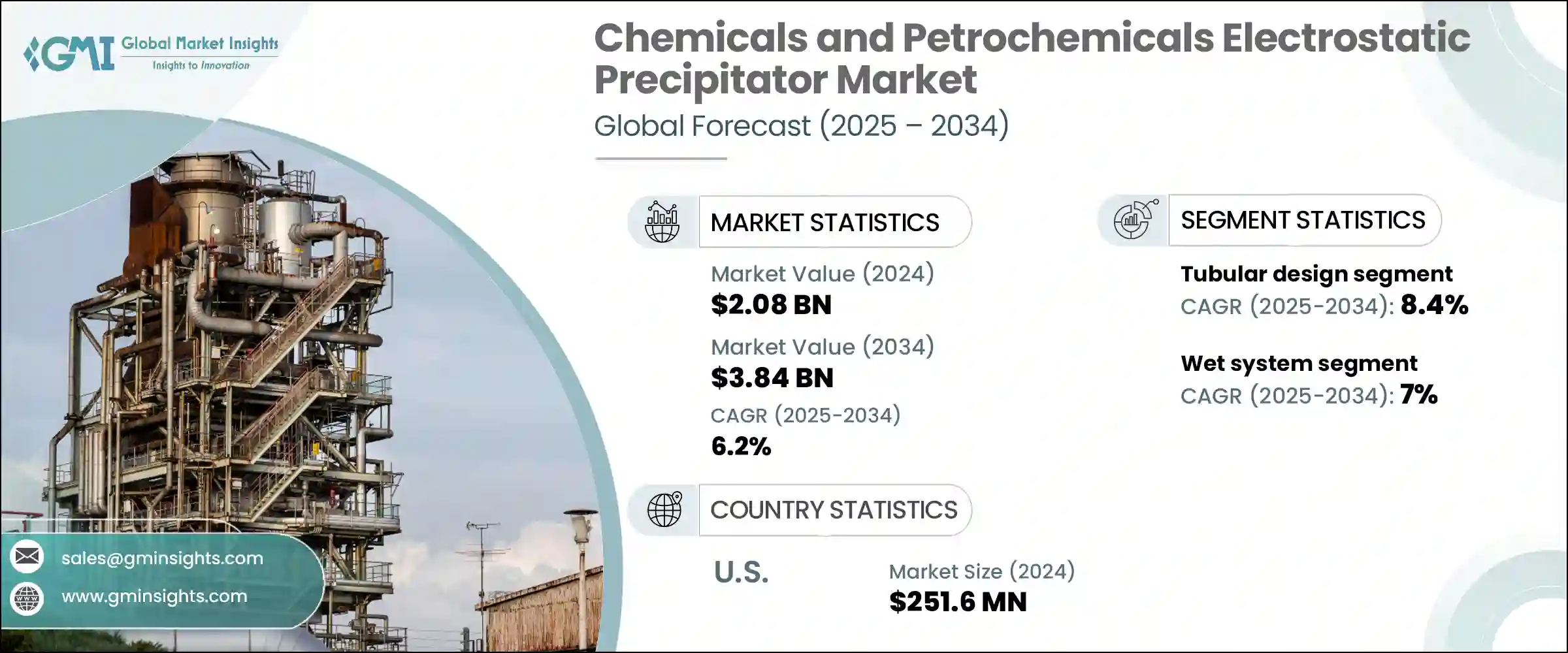

世界の化学と石油化学の電気集塵装置市場は、2024年に20億8,000万米ドルと評価され、CAGR 6.2%で成長し、2034年には38億4,000万米ドルに達すると推定されています。

需要が加速しているのは、粒子状物質を捕捉すると同時に貴重な製品別を回収できるシステムの利用が拡大しているためです。これらの製品別は生産サイクルに再統合することができ、全体的なプロセス効率とリサイクル努力を高める。既存の製油所操業に石油化学処理能力が加わることで、電気集塵装置の導入拡大が続いています。特に高排出ガス工業地帯における大気の質に対する意識の高まりは、職場の安全への懸念とともに、プラント事業者に高度な排出ガス制御システムへの投資を促しています。合成化学物質の生産量の増加と持続可能な操業方法の推進は、大容量装置への電気集塵装置の統合をさらに促進しています。

特に化学セクター全体で環境コンプライアンス規制が強化されていることも、成熟経済諸国と新興経済諸国の両方で製品採用を加速しています。特に有害汚染物質に関する規制が厳しさを増す中、よりクリーンな生産技術の使用は、世界各地の施設で最優先事項であり続けると思われます。産業界のオペレーターは、環境コンプライアンスを満たすだけでなく、エネルギー効率と業務生産性を高める排出削減ソリューションをますます優先するようになっています。脱硫、粒子状物質除去、リアルタイム・エミッション・モニタリングなど、複数の機能を組み合わせた統合型大気汚染防止システムへの移行が、このような関心の高まりに後押しされています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 20億8,000万米ドル |

| 予測金額 | 38億4,000万米ドル |

| CAGR | 6.2% |

プレート式電気集塵装置は、その高い除去効率と大規模処理プラントの乾燥ガス流の処理に適していることから、2034年までに32億米ドルに達すると予想されます。これらのシステムは、連続運転に適合し、高スループットの産業環境でのメンテナンスが容易であることから好まれています。さまざまな化学製造現場での排ガス処理システムの継続的なアップグレードにより、プレート型電気集塵装置の設置が引き続き推進されます。

乾式電気集塵システムセグメントは2024年に86.6%を占めました。この優位性は、費用効果の高い設計、50℃~450℃の範囲の排ガス温度を管理する能力、強力な捕集効率に起因しています。産業界がよりクリーンな排出ガスを優先させる中、乾式電気集塵装置は、メンテナンスの必要性が低く、運転の信頼性が高いため、依然として好まれるソリューションです。これらのシステムでは、デジタル制御とリアルタイムのモニタリング技術の利用が拡大しており、大規模な産業展開への魅力が高まっています。

アジア太平洋化学と石油化学の電気集塵装置市場は、2034年までに18億米ドルに達すると予想されています。成長を促進する要因としては、急速な産業発展、大気汚染に対する社会的関心の高まり、主要国における排出基準の厳格化などが挙げられます。環境コンプライアンスへの投資が増加するにつれて、この地域の国々は、既存の化学・石油化学施設と新設の化学・石油化学施設の両方において、高度なESP技術の設置を優先しています。

化学と石油化学の電気集塵装置市場の競合情勢に貢献している主な企業は、HIMENVIRO、Wood、Enviropol Engineers、Valmet、ELEX、Babcock &Wilcox、ANDRITZ GROUP、GEA Group、Alstom、FLSmidth、KC Cottrell India、PPC Austria Holding、Isgec Heavy Engineering、Thermax Groupなどです。化学と石油化学の電気集塵装置市場の主要企業は、捕捉効率の向上、エネルギーの最適化、メンテナンスコストの削減に重点を置いた研究開発に投資することで存在感を高めています。多くの企業が石油化学メーカーや化学メーカーと戦略的提携を結び、長期契約を結んでいます。また、現地生産とサービス・サポートを通じて、アジア太平洋のような急成長地域でも事業を拡大しています。さらに、デジタル監視システムとAI駆動の診断を集塵ユニットに統合することで、企業は予知保全ソリューションを提供し、中断のない性能を確保することができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:デザイン別、2021年~2034年

- 主要動向

- プレート

- チューブ状

第6章 市場規模・予測:システム別、2021年~2034年

- 主要動向

- ドライ

- ウェット

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- インドネシア

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- アンゴラ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- ペルー

第8章 企業プロファイル

- ANDRITZ GROUP

- Alstom

- Babcock &Wilcox

- Enviropol Engineers

- ELEX

- FLSmidth

- GEA Group

- HIMENVIRO

- Isgec Heavy Engineering

- KC Cottrell India

- PPC Austria Holding

- Thermax Group

- Valmet

- Wood

目次

The Global Chemicals and Petrochemicals Electrostatic Precipitator Market was valued at USD 2.08 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 3.84 billion by 2034. Demand is accelerating due to the growing use of systems capable of capturing particulate matter while simultaneously recovering valuable by-products. These by-products can be reintegrated into the production cycle, boosting overall process efficiency and recycling efforts. The addition of petrochemical processing capacity alongside existing refinery operations continues to support the expansion of electrostatic precipitator deployments. Greater awareness of air quality, especially in high-emission industrial zones, along with workplace safety concerns, is pushing plant operators to invest in advanced emissions control systems. Increasing synthetic chemical output and the push for sustainable operational practices are further fueling the integration of electrostatic precipitators in large-capacity units.

Tighter environmental compliance rules, particularly across the chemicals sector, are also accelerating product adoption in both mature and developing economies. With regulations becoming more rigorous, particularly for hazardous pollutants, the use of cleaner production technologies will remain a top priority across global facilities. Industrial operators are increasingly prioritizing emission-reduction solutions that not only meet environmental compliance but also enhance energy efficiency and operational productivity. This growing emphasis is prompting a widespread shift toward integrated air pollution control systems that combine multiple functions such as desulfurization, particulate removal, and real-time emissions monitoring.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.08 Billion |

| Forecast Value | $3.84 Billion |

| CAGR | 6.2% |

The plate-type electrostatic precipitator segment is expected to reach USD 3.2 billion by 2034, driven by its high removal efficiency and suitability for handling dry gas streams in large processing plants. These systems are favored for their compatibility with continuous operations and ease of maintenance in high-throughput industrial environments. Ongoing upgrades to flue gas treatment systems across various chemical manufacturing sites will continue to drive the installation of plate-type ESPs.

Dry electrostatic precipitator systems segment accounted for 86.6% in 2024. This dominance is attributed to their cost-effective design, ability to manage flue gas temperatures ranging between 50°C and 450°C, and strong collection efficiency. As industries prioritize cleaner emissions, dry ESPs remain the preferred solution due to low maintenance needs and operational reliability. The growing use of digital controls and real-time monitoring technology in these systems is enhancing their appeal for large-scale industrial deployment.

Asia Pacific Chemicals and Petrochemicals Electrostatic Precipitator Market is expected to reach USD 1.8 billion by 2034. Factors driving growth include rapid industrial development, heightened public concern over air pollution, and stricter enforcement of emission standards across key countries. As investments in environmental compliance increase, countries across the region are prioritizing the installation of advanced ESP technologies in both existing and newly built chemical and petrochemical facilities.

Key players contributing to the competitive landscape of the Chemicals and Petrochemicals Electrostatic Precipitator Market include HIMENVIRO, Wood, Enviropol Engineers, Valmet, ELEX, Babcock & Wilcox, ANDRITZ GROUP, GEA Group, Alstom, FLSmidth, KC Cottrell India, PPC Austria Holding, Isgec Heavy Engineering, Thermax Group, and the Thermax Group. Leading companies in the chemicals and petrochemicals electrostatic precipitator market are strengthening their presence by investing in R&D focused on improving capture efficiency, energy optimization, and reducing maintenance costs. Many firms are forming strategic alliances with petrochemical and chemical manufacturers to secure long-term contracts. Businesses are also expanding their footprints in fast-growing regions like Asia Pacific through localized manufacturing and service support. Additionally, integrating digital monitoring systems and AI-driven diagnostics into precipitator units allows companies to offer predictive maintenance solutions, ensuring uninterrupted performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Design, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Plate

- 5.3 Tubular

Chapter 6 Market Size and Forecast, By System, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Dry

- 6.3 Wet

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Indonesia

- 7.4.6 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.5.4 Nigeria

- 7.5.5 Angola

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

- 7.6.4 Peru

Chapter 8 Company Profiles

- 8.1 ANDRITZ GROUP

- 8.2 Alstom

- 8.3 Babcock & Wilcox

- 8.4 Enviropol Engineers

- 8.5 ELEX

- 8.6 FLSmidth

- 8.7 GEA Group

- 8.8 HIMENVIRO

- 8.9 Isgec Heavy Engineering

- 8.10 KC Cottrell India

- 8.11 PPC Austria Holding

- 8.12 Thermax Group

- 8.13 Valmet

- 8.14 Wood

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 121 Pages

- 納期

- 2~3営業日