乾式電気集塵装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Dry Electrostatic Precipitator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 124 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766307

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

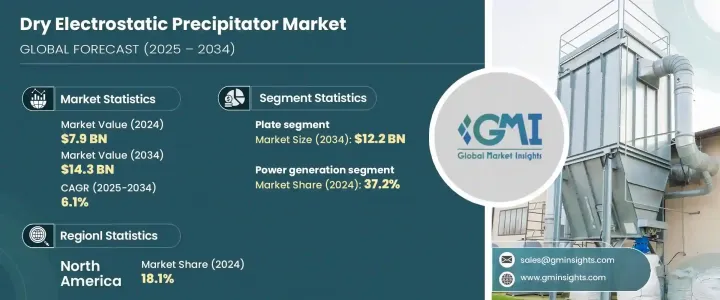

世界の乾式電気集塵装置市場は、2024年には79億米ドルと評価され、CAGR 6.1%で成長し、2034年には143億米ドルに達すると推定されています。

これらのシステムの採用は、大気汚染の削減と産業発生源からの粒子状物質の排出の制御を目的とした、世界の環境規制の厳格化の影響を強く受けています。さらに、特にアジア太平洋などの新興市場における急速な工業化と都市化が、効果的な大気汚染防止ソリューションの需要を促進しており、これが乾式電気集塵装置の採用を後押ししています。

市場の成長は、電気集塵システムの性能と効率を高める先端技術への多額の投資によっても後押しされています。電極設計、先端材料、高度な制御システムの革新により、これらのシステムの捕集効率と信頼性が向上しています。乾式電気集塵装置のコンパクトな性質は、同じガス量に対して垂直方向のスペースが最大2~3倍少なくて済むため、スペースが限られた設備に最適です。これらのシステムは、PM2.5のような微粒子に対して99%以上の捕集効率を達成できるため、発電、セメント、冶金などの産業における大容量の排ガスアプリケーションに適しています。さらに、その連続運転能力は、最小限のメンテナンスで高負荷のダストを処理する能力とともに、産業界にとって経済的に実行可能な長期的ソリューションとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 79億米ドル |

| 予測金額 | 143億米ドル |

| CAGR | 6.1% |

乾式電気集塵装置市場のプレート式セグメントは、微小粒子状物質を捕捉する優れた能力により、2034年までに122億米ドルに達する見込みです。これらのシステムは、特に微小粒子に対して高い捕集効率を示し、大気汚染の抑制に非常に効果的です。小規模な産業オペレーションから大規模な発電所まで、幅広いアプリケーションに対応できる汎用性が、普及に拍車をかけています。プレート式電気集塵装置の需要の増加は、多様な環境におけるその適応性と効率性によるものであり、よりクリーンな排出と大気質の改善を保証します。そのため、高度な大気汚染防止ソリューションを必要とする産業、特に大量の排気ガスを扱う産業にとって好ましい選択肢となっています。

製造業セクターは堅調な成長率が見込まれており、2025~2034年のCAGRは6.7%と予測されています。この成長の原動力となっているのは、産業近代化の重視の高まり、職場の大気質規制の厳格化、呼吸器系の健康リスクに対する意識の高まりなど、いくつかの要因です。よりクリーンで持続可能な生産プロセスへの需要も、乾式電気集塵装置の普及を後押ししています。企業は浮遊粒子状物質を軽減するために自動粉塵制御システムを採用しており、こうした技術の必要性をさらに高めています。産業界が環境フットプリントを改善し、より厳しい規制要件に準拠するよう努めているため、乾式電気集塵装置のような効果的な汚染制御技術に対する需要は製造セクターで大幅に増加すると予想されます。

アジア太平洋の乾式電気集塵装置市場は、2034年までに67億米ドルに達すると予測されています。この地域では、石炭ベースの発電の拡大が続いており、これが市場成長の大きな要因となっています。多くの国で石炭が依然として一次エネルギー源であるため、汚染を緩和するための排出ガス制御システムの需要が高まっています。さらに、セメントや金属産業における高度な大気汚染防止技術の設置が、乾式電気集塵装置の採用をさらに後押ししています。大気汚染削減を目的とした規制措置が、産業界にクリーン技術への投資を促しています。また、この地域ではさまざまな産業部門への投資が増加しており、最先端の微粒子制御ソリューションの採用が加速し、乾式電気集塵装置の市場を強化しています。

世界の乾式電気集塵装置業界では、GEAGroup Aktiengesellschaft, Babcock and Wilcox Enterprises, Siemens Energy, Mitsubishi Heavy Industries, ANDRITZ GROUP, Duconenv, Thermax, PPC Industries, Sumitomo Heavy Industries, Wood, Enviropol Engineers, DURR Group, TAPC, KC Cottrell India, and WEIXIAN.などが著名な企業です。乾式電気集塵装置市場におけるプレゼンスを強化するため、各社は継続的なイノベーションと戦略的パートナーシップに注力しています。厳しい環境基準を満たすより効率的なシステムの開発に投資することで、高度な公害防止技術に対する需要の高まりに対応することを目指しています。企業はまた、特に産業の成長と環境規制が機会を生み出している新興市場において、世界の足跡の拡大にも注力しています。また、多くの企業が、発電から製造まで、さまざまな業界に合わせたソリューションを提供するため、製品の多様化を進めており、市場での地位をさらに強固なものにしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:デザイン別、2021年~2034年

- 主要動向

- プレート式

- チューブ状

第6章 市場規模・予測:排出産業別、2021年~2034年

- 主要動向

- 発電

- 化学製品・石油化学製品

- セメント

- 金属加工・鉱業

- 製造業

- 海洋

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- インドネシア

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- アンゴラ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- ペルー

第8章 企業プロファイル

- ANDRITZ GROUP

- Babcock and Wilcox Enterprises

- Duconenv

- DURR Group

- Enviropol Engineers

- GEA Group Aktiengesellschaft

- KC Cottrell India

- Mitsubishi Heavy Industries

- PPC Industries

- Siemens Energy

- Sumitomo Heavy Industries

- Thermax

- TAPC

- Wood

目次

The Global Dry Electrostatic Precipitator Market was valued at USD 7.9 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 14.3 billion by 2034. The adoption of these systems is being strongly influenced by stricter environmental regulations worldwide aimed at reducing air pollution and controlling emissions of particulate matter from industrial sources. Additionally, rapid industrialization and urbanization, especially in emerging markets like the Asia Pacific, are driving the demand for effective air pollution control solutions, which is propelling the adoption of dry electrostatic precipitators.

The growth of the market is also being fueled by significant investments in advanced technologies that enhance the performance and efficiency of electrostatic precipitator systems. Innovations in electrode designs, advanced materials, and sophisticated control systems are improving the collection efficiency and reliability of these systems. The compact nature of dry ESPs, requiring up to two or three times less vertical space for the same gas volume, makes them ideal for installations with limited space. These systems can achieve collection efficiencies of more than 99% for fine particles like PM2.5, making them suitable for high-capacity flue gas applications in industries such as power generation, cement, and metallurgy. Moreover, their continuous operation capabilities, along with their ability to handle heavy dust loads with minimal maintenance, make them an economically viable long-term solution for industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.9 Billion |

| Forecast Value | $14.3 Billion |

| CAGR | 6.1% |

The plate-based segment of the dry electrostatic precipitator market is poised to reach USD 12.2 billion by 2034, owing to their superior ability to capture fine particulate matter. These systems have demonstrated high collection efficiency, particularly for smaller particles, making them highly effective in controlling air pollution. Their versatility across a wide range of applications, from small-scale industrial operations to large power plants, has fueled their widespread adoption. The increased demand for plate ESPs is attributed to their adaptability and efficiency in diverse settings, ensuring cleaner emissions and improved air quality. This makes them a preferred choice for industries that require advanced air pollution control solutions, especially those dealing with high volumes of exhaust gases.

The manufacturing sector is expected to experience a robust growth rate, with a projected CAGR of 6.7% between 2025 and 2034. Several factors are driving this growth, such as the increasing emphasis on industrial modernization, stricter workplace air quality regulations, and growing awareness of respiratory health risks. The demand for cleaner, more sustainable production processes is also encouraging the widespread adoption of dry electrostatic precipitators. Companies are adopting automated dust control systems to mitigate airborne particulate matter, further boosting the need for these technologies. As industries strive to improve their environmental footprint and comply with stricter regulatory requirements, the demand for effective pollution control technologies like dry ESPs is expected to grow significantly in the manufacturing sector.

Asia Pacific Dry Electrostatic Precipitator Market is anticipated to reach USD 6.7 billion by 2034. The ongoing expansion of coal-based power generation in the region is a significant contributor to the market growth. As coal remains a primary energy source in many countries, the demand for emission control systems to mitigate pollution is rising. Additionally, the installation of advanced air pollution control technologies in cement and metal industries is further propelling the adoption of dry electrostatic precipitators. Regulatory measures aimed at reducing air pollution are encouraging industries to invest in cleaner technologies. The region is also experiencing increased investments in various industrial sectors, which will accelerate the adoption of cutting-edge particulate control solutions, bolstering the dry ESP market.

Prominent players in the Global Dry Electrostatic Precipitator Industry include GEAGroup Aktiengesellschaft, Babcock and Wilcox Enterprises, Siemens Energy, Mitsubishi Heavy Industries, ANDRITZ GROUP, Duconenv, Thermax, PPC Industries, Sumitomo Heavy Industries, Wood, Enviropol Engineers, DURR Group, TAPC, KC Cottrell India, and WEIXIAN. To strengthen their presence in the dry electrostatic precipitator market, companies are focusing on continuous innovation and strategic partnerships. By investing in the development of more efficient systems that meet stringent environmental standards, they aim to cater to the growing demand for advanced pollution control technologies. Companies are also focusing on expanding their global footprint, particularly in emerging markets, where industrial growth and environmental regulations are creating opportunities. Many companies are also diversifying their product offerings to provide tailored solutions for different industries, from power generation to manufacturing, further cementing their market positions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Design, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Plate

- 5.3 Tubular

Chapter 6 Market Size and Forecast, By Emitting Industry, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Power generation

- 6.3 Chemicals and petrochemicals

- 6.4 Cement

- 6.5 Metal processing & mining

- 6.6 Manufacturing

- 6.7 Marine

- 6.8 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Indonesia

- 7.4.6 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.5.4 Nigeria

- 7.5.5 Angola

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

- 7.6.4 Peru

Chapter 8 Company Profiles

- 8.1 ANDRITZ GROUP

- 8.2 Babcock and Wilcox Enterprises

- 8.3 Duconenv

- 8.4 DURR Group

- 8.5 Enviropol Engineers

- 8.6 GEA Group Aktiengesellschaft

- 8.7 KC Cottrell India

- 8.8 Mitsubishi Heavy Industries

- 8.9 PPC Industries

- 8.10 Siemens Energy

- 8.11 Sumitomo Heavy Industries

- 8.12 Thermax

- 8.13 TAPC

- 8.14 Wood

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 124 Pages

- 納期

- 2~3営業日