植物由来のタンパク質加工機器の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Plant-Based Protein Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766270

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

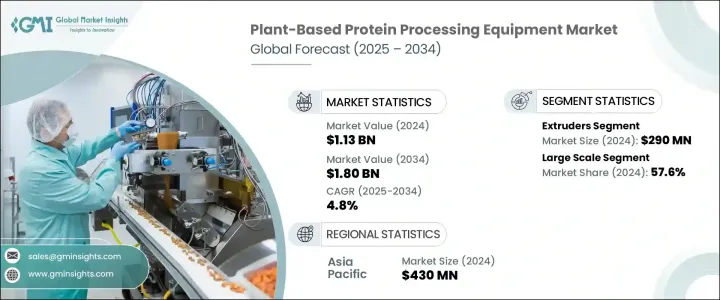

世界の植物由来のタンパク質加工機器市場は、2024年には11億3,000万米ドルと評価され、CAGR 4.8%で成長し、2034年には18億米ドルに達すると推定されています。

植物を前面に押し出した食生活、健康志向の生活、持続可能性への消費者行動の変化が植物性食品への需要を煽り、豆類や穀物から機能性タンパク質を抽出する技術への投資を促進しています。食品製造業者は事業の規模を拡大するにつれて、効率性、製品の一貫性、および栄養の完全性を実現できる装置を求めています。こうした動向は、多様なタンパク源の進化する処理要件を満たす特殊システムの採用をメーカーに促しています。

代替食肉に対する消費者の関心の高まりも、特に世界市場における製造能力の拡大に影響を与えています。しかし、潜在的な可能性が高まっているにもかかわらず、この業界は、商業規模の工場を設立・維持するために必要な多額の資本投資による課題に直面し続けています。押出、乾燥、発酵、テクスチャライズなどの工程では、厳しい衛生・安全基準に準拠した精密工学に基づく機械が必要となります。中小企業にとって、こうした機器の購入、設置、アップグレードに伴うコストは、しばしば大きなハードルとなります。開発途上地域では、金融支援や規制インフラへのアクセスが限られているため、新規参入企業や新興企業にとっての課題がさらに強まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 11億3,000万米ドル |

| 予測金額 | 18億米ドル |

| CAGR | 4.8% |

2024年の売上高は2億9,000万米ドルで、押出システム部門が最大のシェアを占めています。これらのシステムは、様々な食品用途に使用されるテクスチャーのある植物性タンパク質や類似品を成形するのに不可欠です。大豆、小麦、エンドウ豆のタンパク質を加工して、動物性食品の食感や口当たりを再現した製品にします。高水分と低水分の両方の押出方法に対応できるエクストルーダーは、スナック、パテ、タンパク質強化製品など、幅広い植物性食品用途に適応します。その多用途性と生産効率により、エクストルーダーは最新の加工ラインの中核となっています。

2024年には、大規模セグメントが57.6%のシェアを占める。この成長は、植物由来タンパク質に対する消費者需要の増加と、その結果生じる、工業的生産量で安定した生産量を提供する生産者へのプレッシャーを反映しています。主要メーカーは、大容量の乾燥機、ホモジナイザー、セパレーター、エクストルーダーなどの先進設備で施設をアップグレードしています。こうした投資は、スループットの向上、手作業の削減、生産バッチ全体の均一性の確保に役立っています。高出力のシステムは、プロテインをベースとする幅広い製品の信頼性の高いサプライチェーンを必要とする大手ブランドや小売業者をサポートする上で不可欠です。

アジア太平洋植物由来のタンパク質加工機器2024年に4億3,000万米ドルを生み出し、38%のシェアを占める。この地域は、植物性タンパク質の文化的普及と旺盛な農業生産の両方から恩恵を受けています。アジア太平洋諸国では、大豆やマメ科の植物をベースにした製品を取り入れる食生活が長く続いており、植物ベースのイノベーションを採用するための強固な基盤が形成されています。急速な産業化が、人口主導の食糧需要と持続可能性への関心の高まりと相まって、この地域全体の加工機器の成長を支えています。政府の好意的な支援と、食品イノベーションとタンパク質調達の自給自足を目指した新たな取り組みが、この地域の市場開拓をさらに加速させています。

植物由来のタンパク質加工機器業界の主要企業には、Equinom、Clextral SAS、Hosokawa Micron B.V、Alfa Laval、Netzsch-Feinmahltechnik GmbH、Flottweg SE、Bepex International LLC、SPX FLOW Inc、Lyco Manufacturing、Koch Separation Solutions、ANDRITZ AG、Glatt Group、Coperion GmbH、GEA Group、Buhler Groupなどがあります。市場でのプレゼンスを拡大するため、この分野の企業は研究開発と高度なオートメーション技術への戦略的投資を優先しています。その多くは、食品メーカーや新興企業とパートナーシップを結び、新製品のイノベーションに合わせてカスタマイズされた加工ソリューションを共同開発しています。グローバルメーカーはまた、地域化された生産拠点やサービスネットワークを通じて新興経済圏での足跡を増やしています。需要の拡張性を満たすため、大手企業は、さまざまな植物性タンパク質の処理に柔軟性を提供する、モジュール式でエネルギー効率の高いシステムを発売しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 植物由来食品の需要の高まり

- さまざまな食品における植物性タンパク質の採用

- 代替タンパク質に特化したスタートアップの成長

- 業界の潜在的リスク&課題

- 初期資本投資額が高め

- 生産規模の拡大における複雑さ

- 機会

- サプライチェーンの最適化

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 用途別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- デカンターと遠心分離機

- グラインダーと粉砕機

- 乾燥機

- 押出機

- ろ過システム

- 包装システム

- その他

第6章 市場推計・予測:生産能力別、2021年~2034年

- 主要動向

- 中小規模

- 大規模

第7章 市場推計・予測:タンパク質の種類別、2021年~2034年

- 主要動向

- 大豆タンパク質

- エンドウ豆タンパク質

- 小麦タンパク質

- ひよこ豆タンパク質

- その他

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 粉末

- 分離株

- 濃縮物

- テクスチャ加工製品

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Alfa Laval

- ANDRITZ AG

- Bepex International LLC

- Buhler Group

- Clextral SAS

- Coperion GmbH

- Equinom

- Flottweg SE

- GEA Group

- Glatt Group

- Hosokawa Micron B.V

- Koch Separation Solutions

- Lyco Manufacturing

- Netzsch-Feinmahltechnik GmbH

- SPX FLOW Inc

目次

The Global Plant-Based Protein Processing Equipment Market was valued at USD 1.13 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 1.8 billion by 2034. Shifts in consumer behavior toward plant-forward diets, health-conscious living, and sustainability are fueling demand for plant-based foods, driving investment in technologies that extract functional proteins from legumes and grains. As food producers scale up their operations, they're seeking equipment capable of delivering efficiency, product consistency, and nutritional integrity. These trends are encouraging manufacturers to adopt specialized systems that meet the evolving processing requirements of diverse protein sources.

Increased consumer interest in meat alternatives is also influencing the expansion of manufacturing capabilities, particularly across global markets. However, despite the growing potential, the industry continues to face challenges due to the substantial capital investment needed to establish and maintain commercial-scale plants. Processes like extrusion, drying, fermentation, and texturization demand precision-engineered machinery that complies with strict hygiene and safety standards. For smaller companies, the costs associated with purchasing, installing, and upgrading this equipment often become a major hurdle. In developing regions, limited access to financial support and regulatory infrastructure further intensifies the challenge for new entrants and emerging firms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.13 Billion |

| Forecast Value | $1.8 Billion |

| CAGR | 4.8% |

Extrusion systems segment accounted for the largest share in 2024, with revenue of USD 290 million. These systems are essential in shaping textured plant proteins and analogs used in a variety of food applications. They process soy, wheat, and pea proteins into products that replicate the texture and mouthfeel of animal-based foods. With the ability to handle both high- and low-moisture extrusion methods, extruders provide adaptability for a wide array of plant-based food applications including snacks, patties, and protein-enriched products. Their versatility and production efficiency make them a core part of modern processing lines.

In 2024, the large-scale segment held 57.6% share. This growth reflects increased consumer demand for plant-derived proteins and the resulting pressure on producers to deliver consistent output at industrial volumes. Major manufacturers are upgrading their facilities with advanced equipment such as high-capacity dryers, homogenizers, separators, and extruders. These investments help enhance throughput, reduce manual labor, and ensure uniformity across production batches. High-output systems are vital in supporting large brands and retailers that require reliable supply chains for a wide range of protein-based products.

Asia Pacific Plant-Based Protein Processing Equipment Industry generated USD 430 million and held 38% share in 2024. The region benefits from both the cultural prevalence of plant proteins and strong agricultural output. Countries across Asia Pacific have long-standing dietary habits that incorporate soy and legume-based products, creating a solid base for the adoption of plant-based innovations. Rapid industrialization, combined with population-driven food demand and growing concerns about sustainability, are supporting the growth of processing equipment across this region. Favorable government support and new initiatives aimed at food innovation and self-sufficiency in protein sourcing are further accelerating market development in this region.

Major players in the Plant-Based Protein Processing Equipment Industry include Equinom, Clextral SAS, Hosokawa Micron B.V, Alfa Laval, Netzsch-Feinmahltechnik GmbH, Flottweg SE, Bepex International LLC, SPX FLOW Inc, Lyco Manufacturing, Koch Separation Solutions, ANDRITZ AG, Glatt Group, Coperion GmbH, GEA Group, and Buhler Group. To expand their market presence, companies in this space are prioritizing strategic investments in R&D and advanced automation technologies. Many are forming partnerships with food producers and startups to co-develop customized processing solutions that align with new product innovations. Global manufacturers are also increasing their footprint in emerging economies through localized production hubs and service networks. To meet demand scalability, leading firms are launching modular, energy-efficient systems that offer flexibility in handling various plant proteins.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for plant-based foods

- 3.2.1.2 Adoption of plant-based protein in various food products

- 3.2.1.3 Growth of startups focused on alternative proteins

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Complexity in scaling production

- 3.2.3 Opportunities

- 3.2.4 Supply chain optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By application

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Bn) (Thousand Units)

- 5.1 Key trends

- 5.2 Decanter and centrifuges

- 5.3 Grinders and crushers

- 5.4 Dryers

- 5.5 Extruders

- 5.6 Filtration systems

- 5.7 Packaging systems

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Production Capacity, 2021 – 2034 (USD Bn) (Thousand Units)

- 6.1 Key trends

- 6.2 Small and medium scale

- 6.3 Large scale

Chapter 7 Market Estimates and Forecast, By Protein Type, 2021 – 2034 (USD Bn) (Thousand Units)

- 7.1 Key trends

- 7.2 Soy protein

- 7.3 Pea protein

- 7.4 Wheat protein

- 7.5 Chickpea protein

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Bn) (Thousand Units)

- 8.1 Key trends

- 8.2 Powder

- 8.3 Isolates

- 8.4 Concentrates

- 8.5 Texturized products

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Bn) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alfa Laval

- 11.2 ANDRITZ AG

- 11.3 Bepex International LLC

- 11.4 Buhler Group

- 11.5 Clextral SAS

- 11.6 Coperion GmbH

- 11.7 Equinom

- 11.8 Flottweg SE

- 11.9 GEA Group

- 11.10 Glatt Group

- 11.11 Hosokawa Micron B.V

- 11.12 Koch Separation Solutions

- 11.13 Lyco Manufacturing

- 11.14 Netzsch-Feinmahltechnik GmbH

- 11.15 SPX FLOW Inc

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日