自動ボイドフィルディスペンサーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Automated Void Fill Dispensers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766198

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

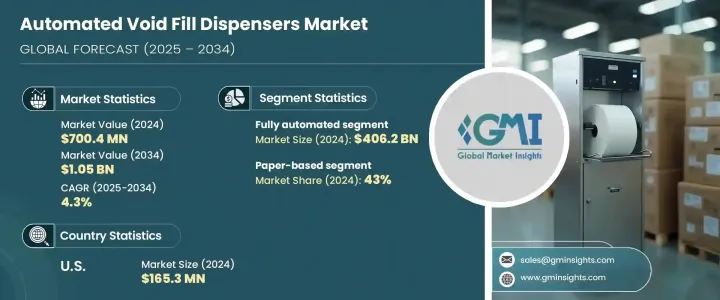

自動ボイドフィルディスペンサーの世界市場は、2024年には7億40万米ドルと評価され、CAGR 4.3%で成長し、2034年には10億5,000万米ドルに達すると推定されています。

この成長は主にeコマースセクタの急速な拡大が牽引しており、効率的でサステイナブル包装ソリューションへの需要が高まっています。自動ボイドフィルディスペンサーは、紙、発泡スチロール、エアベース製品などの緩衝材を包装の空いたスペースに充填し、配送中の商品を保護するという重要な役割を担っています。これらのディスペンサーは、メーカーが材料の使用量を最適化し、包装効率を向上させながらコストを削減するのに役立ちます。さらに、エコフレンドリー包装が重視されるようになったことで、廃棄物を最小限に抑え、世界の環境規制への準拠をサポートする正確な分注が可能になり、これらの機械の導入が加速しています。

AIやIoTの統合などの技術的進歩は、リアルタイムのデータモニタリング、予知保全、生産ライン全体のシームレスな接続を可能にすることで、機械の性能に革命をもたらしています。これらのスマート機能は、効率と精度を高めるだけでなく、ダウンタイムと運用コストを削減します。その結果、これらのインテリジェントシステムは、スピード、精度、適応性が増大し続ける需要に対応し、競合優位性を維持するために不可欠な、最新の自動包装設備に不可欠なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 7億40万米ドル |

| 予測金額 | 10億5,000万米ドル |

| CAGR | 4.3% |

2024年には、完全自動セグメントが市場を席巻し、4億620万米ドルの収益を上げ、2034年までCAGR 4.7%で成長すると予測されます。このセグメントの拡大には、大量生産に対応できる省力的で効率的な包装ソリューションを求める産業が拍車をかけています。完全に自動化されたディスペンサーは、材料のアウトプットを正確に制御し、廃棄物を削減し、サステイナブル取り組みを後押しします。スマート倉庫や製造工場での採用が増加しているのは、AIやIoTのような先進的自動化技術の統合によって推進されており、全体的な生産性と業務効率を向上させています。

紙ベースのセグメントは2024年に43%のシェアを占め、大きな収益を生み出し、2025~2034年のCAGRは4.5%で成長すると予測されています。紙ベースのボイドフィルディスペンサーは、リサイクル可能で、ますます厳しくなる環境基準に適合しているため、支持されています。規制が強化されるにつれて、eコマースや包装産業の各企業は、エコフレンドリー代替品を求めてリサイクル不可能で有害な材料を段階的に排除しており、紙ベースのシステムが好ましい選択肢となっています。

米国の自動ボイドフィルディスペンサー市場は79%のシェアを占め、2024年には1億6,530万米ドルを創出します。同国は持続可能性とエコフレンドリー製造業に重点を置いており、紙ベースの空隙充填ソリューションへの需要が高まっています。さらに、スマート工場と自動化へのシフトが、包装作業の効率と処理能力を高めるために、AIを搭載したビジョンシステムやIoT接続などのスマート機能を備えた完全自動ディスペンサーの普及を支えています。

世界の自動ボイドフィルディスペンサー市場で競合する主要企業は、EcoEnclose、Ranpak、IPG、Papier Sprick、Storopack Hans Reichenecker、Crawford Packaging、HexcelPack、The Packaging Club、Pregis、Kite Packaging、Ashtonne Packaging、Omni Group、Fromm Packaging Systems、Zepak、Sealed Airなどです。市場での存在感を高めるため、主要企業は機械の精度、スピード、エネルギー効率を高める研究開発に多額の投資を行っています。また、リアルタイムのモニタリング、予知保全、他の包装システムとのシームレスな接続を可能にするため、最先端のAIとIoT技術の統合に注力しています。包装メーカーやeコマース企業との戦略的パートナーシップは、これらの参入企業が特定の顧客のニーズに合わせてソリューションをカスタマイズするのに役立っています。さらに、持続可能でリサイクル可能な空隙充填材を含む製品ポートフォリオを拡大することで、環境コンプライアンスへの取り組みを支援しています。また、トレーニング、アフターセールスサポート、柔軟な資金調達オプションを提供することで、企業は長期的な顧客関係を築き、新興市場での足跡を拡大することができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 産業への影響要因

- 促進要因

- eコマース産業の拡大

- 持続可能性と環境コンプライアンス

- スマート倉庫とインダストリー4.0との統合

- 産業の潜在的リスク・課題

- 初期資本投資額が高め

- 既存の倉庫システムとの統合の課題

- 持続可能性と過剰包装への懸念

- 機会

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- 半自動

- 完全自動

第6章 市場推定・予測:包装材タイプ別、2021~2034年

- 主要動向

- 紙ベース

- フォームベース

- その他

第7章 市場推定・予測:操作別、2021~2034年

- 主要動向

- 統合型

- スタンドアロン

第8章 市場推定・予測:出力容量別、2021~2034年

- 主要動向

- 最大100m/分

- 100~200m/分

- 200m/分以上

第9章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- 包装

- eコマース

- エレクトロニクス

- 医薬品

- 消費財

- 自動車

- その他(家具・家庭用品、化粧品・パーソナルケア用品など)

第10章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接販売

- 間接販売

第11章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Ashtonne Packaging

- Crawford Packaging

- EcoEnclose

- Fromm Packaging Systems

- HexcelPack

- IPG

- Kite Packaging

- Omni Group

- Papier Sprick

- Pregis

- Ranpak

- Sealed Air

- Storopack Hans Reichenecker

- The Packaging Club

- Zepak

目次

The Global Automated Void Fill Dispensers Market was valued at USD 700.4 million in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 1.05 billion by 2034. This growth is primarily driven by the rapid expansion of the e-commerce sector, which has heightened the demand for efficient and sustainable packaging solutions. Automated void fill dispensers play a crucial role by filling empty spaces in packages with cushioning materials such as paper, foam, or air-based products to protect items during shipping. These dispensers help manufacturers optimize material usage, reducing costs while improving packaging efficiency. Furthermore, the growing emphasis on eco-friendly packaging has accelerated the adoption of these machines, as they allow for precise dispensing that minimizes waste and supports compliance with environmental regulations globally

Technological advancements, such as the integration of AI and IoT, are revolutionizing machine performance by enabling real-time data monitoring, predictive maintenance, and seamless connectivity across production lines. These smart capabilities not only boost efficiency and accuracy but also reduce downtime and operational costs. As a result, these intelligent systems have become indispensable in modern, automated packaging facilities, where speed, precision, and adaptability are critical to meeting ever-growing demands and maintaining competitive advantage.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $700.4 Million |

| Forecast Value | $1.05 Billion |

| CAGR | 4.3% |

In 2024, the fully automated segment dominated the market, generating USD 406.2 million in revenue and is expected to grow at a CAGR of 4.7% through 2034. This segment's expansion is fueled by industries seeking labor-saving, efficient packaging solutions capable of handling high volumes. Fully automated dispensers precisely control material output, reducing waste and boosting sustainability efforts. Their growing adoption in smart warehouses and manufacturing plants is propelled by the integration of advanced automation technologies like AI and IoT, which improve overall productivity and operational efficiency.

The paper-based segment held a 43% share in 2024, generating significant revenue and is anticipated to grow at a CAGR of 4.5% during 2025-2034. Paper-based void fill dispensers are favored due to their recyclable nature and alignment with increasingly strict environmental standards. As regulations tighten, companies across the e-commerce and packaging industries are phasing out non-recyclable and toxic materials in favor of eco-friendly alternatives, making paper-based systems the preferred choice.

United States Automated Void Fill Dispensers Market held 79% share and generated USD 165.3 million in 2024. The country's focus on sustainability and eco-conscious manufacturing has driven strong demand for paper-based void fill solutions. Additionally, the shift toward smart factories and automation supports the uptake of fully automated dispensers equipped with smart features like AI-powered vision systems and IoT connectivity to boost efficiency and throughput in packaging operations.

Key players competing in the Global Automated Void Fill Dispensers Market include EcoEnclose, Ranpak, IPG, Papier Sprick, Storopack Hans Reichenecker, Crawford Packaging, HexcelPack, The Packaging Club, Pregis, Kite Packaging, Ashtonne Packaging, Omni Group, Fromm Packaging Systems, Zepak, and Sealed Air. To strengthen their market presence, leading companies are investing heavily in R&D to enhance machine accuracy, speed, and energy efficiency. They are focusing on integrating cutting-edge AI and IoT technologies to enable real-time monitoring, predictive maintenance, and seamless connectivity with other packaging systems. Strategic partnerships with packaging manufacturers and e-commerce companies help these players customize solutions for specific client needs. Furthermore, expanding product portfolios to include sustainable and recyclable void fill materials supports their commitment to environmental compliance. Offering training, after-sales support, and flexible financing options also helps companies build long-term client relationships and expand their footprint in emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Packaging material type

- 2.2.4 Operation

- 2.2.5 Output capacity

- 2.2.6 End use industry

- 2.2.7 Distribution channel

- 2.3 CXO prospectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of e-commerce industry

- 3.2.1.2 Sustainability and environmental compliance

- 3.2.1.3 Integration with smart warehousing and industry 4.0

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Integration challenges with existing warehousing systems

- 3.2.2.3 Sustainability and over-packaging concerns

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East and Africa

- 4.2.1.5 Latin America

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Million, Thousand Units)

- 5.1 Key trends

- 5.2 Semi-automated

- 5.3 Fully automated

Chapter 6 Market Estimates & Forecast, By Packaging Material Type, 2021 - 2034 ($Million, Thousand Units)

- 6.1 Key trends

- 6.2 Paper based

- 6.3 Foam based

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Million, Thousand Units)

- 7.1 Key trends

- 7.2 Integrated

- 7.3 Standalone

Chapter 8 Market Estimates & Forecast, By Output Capacity, 2021 - 2034 ($Million, Thousand Units)

- 8.1 Key trends

- 8.2 Up to 100 m/min

- 8.3 100 m/min - 200 m/min

- 8.4 Above 200 m/min

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Million, Thousand Units)

- 9.1 Key trends

- 9.2 Packaging

- 9.3 E-commerce

- 9.4 Electronics

- 9.5 Pharmaceutical

- 9.6 Consumer goods

- 9.7 Automotive

- 9.8 Others(furnishing and home goods, cosmetic and personal care, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Million, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Million, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Ashtonne Packaging

- 12.2 Crawford Packaging

- 12.3 EcoEnclose

- 12.4 Fromm Packaging Systems

- 12.5 HexcelPack

- 12.6 IPG

- 12.7 Kite Packaging

- 12.8 Omni Group

- 12.9 Papier Sprick

- 12.10 Pregis

- 12.11 Ranpak

- 12.12 Sealed Air

- 12.13 Storopack Hans Reichenecker

- 12.14 The Packaging Club

- 12.15 Zepak

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日