|

市場調査レポート

商品コード

1766174

培養肉バイオリアクターの市場機会と促進要因、産業動向分析、2025年~2034年予測Cultured Meat Bioreactors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 培養肉バイオリアクターの市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月05日

発行: Global Market Insights Inc.

ページ情報: 英文 380 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

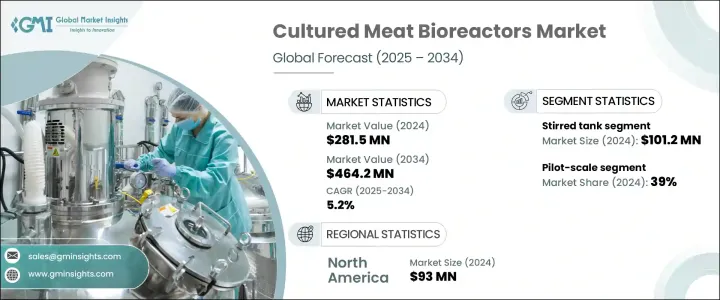

世界の培養肉バイオリアクター市場は、2024年には2億8,150万米ドルとなり、CAGR 5.2%で成長し、2034年には4億6,420万米ドルに達すると予測されています。

この市場は、洗練されたバイオリアクターシステムを通じてラボ栽培肉の大規模生産を可能にすることで、栽培肉セグメントで重要な役割を果たしています。これらのバイオリアクターは、動物細胞培養のための注意深く制御された環境を作り出し、動物の処理を必要としない食肉生産を可能にします。攪拌タンク型、灌流型、エアリフト型、中空糸型など、さまざまなタイプのバイオリアクターがあり、それぞれ、拡大性、栄養供給、せん断力の管理などの点で明確な利点があります。バイオリアクターの設計、細胞培養培地、スケーリング方法の革新により、培養食肉生産のコスト効率は向上しています。

技術の進歩に伴い、生産コストは低下し、培養肉はより手頃で入手しやすくなると予想されます。食感、風味、品質の向上も、消費者に受け入れられ市場成長を促進する重要な要因です。持続可能性は依然として主要な動機であり、培養肉は従来型食肉生産に代わる、環境にやさしく、より倫理的な選択肢を記載しています。代替食肉に対する消費者の関心の高まりが、この技術に対する需要をさらに後押ししているが、特に新興企業にとっては、初期資本コストと運営コストが依然として大きな障壁となっています。生産を確立するには、産業規模での細胞増殖をサポートできる特殊なバイオリアクターが必要です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 2億8,150万米ドル |

| 予測金額 | 4億6,420万米ドル |

| CAGR | 5.2% |

攪拌タンクバイオリアクターセグメントが2024年の市場をリードし、1億120万米ドルを生み出しました。攪拌タンクバイオリアクターは、その信頼性と拡大性から高い支持を得ており、商業規模の細胞培養に理想的です。バイオ医薬品や発酵用途で高い実績があり、培養肉生産者にとって技術的リスクが低いです。これらのシステムは、1~10リットルの小さな実験室サイズから1万リットルを超える産業用容量まで拡大可能で、研究開発から本格的な製造まで、重要な柔軟性を記載しています。この拡大性は、競合価格で培養肉の商品化を目指す企業にとって不可欠です。

パイロット規模の2024年のシェアは39%です。培養肉産業は研究から商業生産へと移行しつつあるため、パイロット規模バイオリアクターは重要な橋渡し役を果たしています。商業化の前段階にある多くの企業は、パイロット規模システムを使用して、細胞株の改良、組織工学プロセスの最適化、大規模生産シミュレーションを行っています。こうしたバイオリアクターは資本投資が少なくて済むため、新興企業や、規制当局の承認やビジネスモデルの開発に取り組んでいる企業にとって利用しやすいものとなっています。

北米の培養肉バイオリアクター2024年の市場規模は9,300万米ドル。米国は、明確な規制によって培養肉に関わる投資家や企業を支援する環境を育んできました。2023年に政府が培養鶏の販売を承認したのに続き、米国は商業培養肉販売の世界的リーダーとなり、バイオリアクター技術とインフラへの投資を後押ししています。この地域には、バイオリアクターの開発とプロセスの革新を専門とする最先端のバイオテクノロジー企業や食品技術企業があり、主要研究機関がそれを支えています。さらに、北米の消費者、特にミレニアル世代とZ世代は、倫理的に生産されたエコフレンドリー食品を強く嗜好しており、これが培養肉の需要を促進し、企業によるバイオリアクターシステムの生産規模拡大と技術革新を促しています。

世界の培養肉バイオリアクター産業で事業を展開している主要企業には、Merck KGaA、ABEC、Alfa Laval、Bioengineering AG、Esco Lifesciences Group、Sartorius AG、GEA、Infors HT、Eppendorf AG、INNOVA Bio-meditech、KBIoTech GmBH、OLLITAL Technology、Pall Corporation、Solaris BIoTech、Vogtlin Instruments GmbHなどがあります。市場リーダーが採用する主要戦略は、市場でのポジショニングを高めるために技術革新とコラボレーションに重点を置いています。

企業は、バイオリアクターの設計を改善し、細胞培養培地を最適化し、費用対効果の高い生産のためのスケーラビリティを高めるために、研究開発に幅広く投資しています。培養肉生産者と戦略的パートナーシップを結ぶことで、技術の統合とプロセスの改良が可能になります。企業はまた、需要の増加に対応するため、生産能力の拡大と新興市場への参入を優先しています。マーケティングキャンペーンで持続可能性と倫理的食品生産を強調することは、環境意識の高い消費者を惹きつけるのに役立ちます。さらに企業は、イノベーションを保護するために、規制の遵守と知的財産の確保に重点を置きます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 産業への影響要因

- 促進要因

- サステイナブルタンパク質への需要の高まり

- バイオリアクター設計における技術的進歩

- 培養肉スタートアップへの投資増加

- 産業の潜在的リスク・課題

- 高い資本コストと運用コスト

- 生産規模の拡大における複雑さ

- 機会

- サプライチェーンの最適化

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- 中空繊維

- エアリフトリアクター

- 攪拌タンク

- その他

第6章 市場推定・予測:規模別、2021~2034年

- 主要動向

- 実験室規模

- パイロット規模

- 商業規模

第7章 市場推定・予測:動作モード別、2021~2034年

- 主要動向

- バッチ

- フェドバッチ

- 常用

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 牛肉

- 家禽

- 豚肉

- その他

第9章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 培養肉メーカー

- 契約製造組織

- 研究開発機関/ラボ

第10章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- ABEC

- Alfa Laval

- Bioengineering AG

- Eppendorf AG

- Esco Lifesciences Group

- GEA

- Infors HT

- INNOVA Bio-meditech

- KBIoTech GmBH

- Merck KGaA

- OLLITAL Technology

- Pall Corporation

- Sartorius AG

- Solaris BIoTech

- Vogtlin Instruments GmbH

The Global Cultured Meat Bioreactors Market was valued at USD 281.5 million in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 464.2 million by 2034. This market plays a critical role in the cultivated meat sector by enabling large-scale production of lab-grown meat through sophisticated bioreactor systems. These bioreactors create carefully controlled environments for animal cell cultures, allowing meat production without the need for animal slaughter. Various bioreactor types, including stirred-tank, perfusion, airlift, and hollow-fiber systems, each provide distinct advantages in terms of scalability, nutrient delivery, and management of shear forces. Innovations in bioreactor design, cell culture media, and scaling methods have enhanced the cost-efficiency of cultured meat production.

As technology advances, production costs are expected to decline, making cultivated meat more affordable and accessible. Improved texture, flavor, and quality are also key factors that will boost consumer acceptance and drive market growth. Sustainability remains a major motivator, with cultured meat offering an eco-friendly and more ethical alternative to traditional meat production. Rising consumer interest in meat alternatives further fuels demand for this technology, though high initial capital and operating costs remain significant barriers, especially for startups. Establishing production requires specialized bioreactors capable of supporting cell growth at industrial scales.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $281.5 Million |

| Forecast Value | $464.2 Million |

| CAGR | 5.2% |

The stirred-tank bioreactor segment led the market in 2024, generating USD 101.2 million. Stirred-tank bioreactors are highly favored for their reliability and scalability, making them ideal for commercial-scale cell cultivation. With a strong track record in biopharmaceutical and fermentation applications, they present low technical risks to cultivated meat producers. These systems can scale from small laboratory sizes of 1-10 liters to industrial capacities exceeding 10,000 liters, offering vital flexibility for research, development, and full-scale manufacturing. This scalability is essential for companies aiming to commercialize cultured meat at competitive prices.

The pilot-scale segment held a 39% share in 2024. Since the cultured meat industry is transitioning from research to commercial production, pilot-scale bioreactors serve as a critical bridge. Many companies at the pre-commercial stage use pilot-scale systems to refine cell lines, optimize tissue engineering processes, and simulate large-scale production without the high costs associated with full-scale facilities. These bioreactors require lower capital investment, making them accessible to startups and firms working on regulatory approvals or business model development.

North America Cultured Meat Bioreactors Market accounted for USD 93 million in 2024. The United States has fostered a supportive environment for investors and companies involved in cultivated meat through clear regulations. Following government approval for marketing cultured chicken in 2023, the U.S. has become a global leader in commercial cultured meat sales, boosting investments in bioreactor technology and infrastructure. The region hosts some of the most advanced biotech and food tech companies specializing in bioreactor development and process innovation, supported by leading research institutions. Moreover, North American consumers, particularly millennials and Gen Z, show strong preferences for ethically produced, environmentally friendly food products, driving demand for cultured meat and encouraging companies to scale production and innovate bioreactor systems.

Leading companies operating in the Global Cultured Meat Bioreactors Industry include Merck KGaA, ABEC, Alfa Laval, Bioengineering AG, Esco Lifesciences Group, Sartorius AG, GEA, Infors HT, Eppendorf AG, INNOVA Bio-meditech, KBiotech GmBH, OLLITAL Technology, Pall Corporation, Solaris Biotech, and Vogtlin Instruments GmbH. Key strategies adopted by market leaders focus heavily on innovation and collaboration to boost their market positioning.

Companies invest extensively in research and development to improve bioreactor designs, optimize cell culture media, and enhance scalability for cost-effective production. Forming strategic partnerships with cultivated meat producers enables technology integration and process refinement. Firms also prioritize expanding production capacities and entering emerging markets to capitalize on rising demand. Emphasizing sustainability and ethical food production in marketing campaigns helps attract eco-conscious consumers. Additionally, players focus on regulatory compliance and securing intellectual property to safeguard innovations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Scale

- 2.2.4 Mode of Operation

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable protein

- 3.2.1.2 Technological advancements in bioreactor design

- 3.2.1.3 Growing investments in cultured meat startups

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High capital and operating costs

- 3.2.2.2 Complexity in scaling up production

- 3.2.3 Opportunities

- 3.2.4 Supply chain optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Million) (Units)

- 5.1 Key trends

- 5.2 Hollow fiber

- 5.3 Airlift reactor

- 5.4 Stirred tank

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Scale, 2021 – 2034 (USD Million) (Units)

- 6.1 Key trends

- 6.2 Lab-scale

- 6.3 Pilot-scale

- 6.4 Commercial-scale

Chapter 7 Market Estimates and Forecast, By Mode of Operation, 2021 – 2034 (USD Million) (Units)

- 7.1 Key trends

- 7.2 Batch

- 7.3 Fed-batch

- 7.4 Continuous

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million) (Units)

- 8.1 Key trends

- 8.2 Beef

- 8.3 Poultry

- 8.4 Pork

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Million) (Units)

- 9.1 Key trends

- 9.2 Cultured meat manufacturers

- 9.3 Contract manufacturing organizations

- 9.4 R&D organizations/Institutes

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABEC

- 11.2 Alfa Laval

- 11.3 Bioengineering AG

- 11.4 Eppendorf AG

- 11.5 Esco Lifesciences Group

- 11.6 GEA

- 11.7 Infors HT

- 11.8 INNOVA Bio-meditech

- 11.9 KBiotech GmBH

- 11.10 Merck KGaA

- 11.11 OLLITAL Technology

- 11.12 Pall Corporation

- 11.13 Sartorius AG

- 11.14 Solaris Biotech

- 11.15 Vogtlin Instruments GmbH