住宅保険の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Home Insurance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755386

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

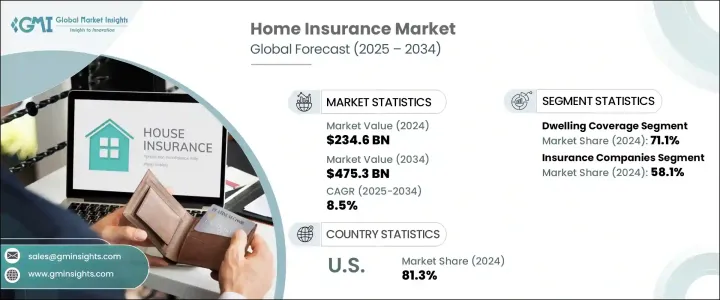

住宅保険の世界市場は、2024年には2,346億米ドルとなり、住宅所有率の増加や不動産価値の上昇を背景に、CAGR8.5%で成長し、2034年までには4,753億米ドルに達すると予測されています。

世界の住宅市場が引き続き高い需要と投資に見舞われる中、住宅保険の必要性はより重要になっています。住宅所有者は現在、住宅の構造だけでなく、ライフスタイルや住宅に関連する負債を確保することに重点を置くようになっています。この変化により、保険会社は個々のリスクプロファイルや特定の地域の危険に合わせたより柔軟な保険を提供するようになりました。住宅が貴重で感傷的な資産となりつつある現在、保険はもはや単なる必要条件ではなく、富を保全し、責任ある住宅所有権を確保するための戦略的優先事項となっています。

住宅保険市場の進化を促す重要な要因は、特に若い世代で初めて住宅を購入する人が増えていることです。これらの新しい住宅所有者は、デジタルファーストのやり取り、リアルタイムの契約管理、迅速な顧客サービスを好み、異なる期待を持っています。住宅財産の価値が上昇し続ける中、保険会社は高度な分析、衛星画像、IoTデータなどの新技術に投資し、個別化された補償とより良いリスク評価を提供しています。この動向により、住宅保険プロバイダーは、単に物理的資産を保護するだけでなく、住宅所有者の旅における信頼できるパートナーへと変貌を遂げます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 2,346億米ドル |

| 予測金額 | 4,753億米ドル |

| CAGR | 8.5% |

2024年時点で、住居補償分野は71.1%のシェアを占め、2025年から2034年のCAGRは9%で成長すると予測されます。住宅補償は、火災、盗難、破壊行為、自然災害による構造的損害を補償するため、住宅所有者にとって極めて重要です。この補償は、都市部のアパートから郊外の住宅まで、あらゆるタイプの物件に不可欠であり、保険会社はより強固な保護を確保するため、インフレ調整後の再建築費用や地域別リスクモデルなどの改善を進めています。

2024年には保険会社セグメントが58.1%のシェアで市場をリードし、2034年までのCAGRは9.3%で成長すると予想されています。これらの保険会社は住宅保険業界の中心的存在であり、包括的な保険引受、リスク評価、保険金請求管理を提供しています。大規模なリスクと柔軟な補償プランを管理する能力により、先進国および新興国市場で圧倒的なシェアを誇っています。その規模と保険数理に関する専門知識により、住宅所有者の多様なニーズに効果的に応えています。

米国の住宅保険市場は、堅調な賃貸住宅部門、強力な規制枠組み、住宅所有者のリスク管理の重要性に対する意識の高まりが牽引し、2024年には81.3%のシェアを占め、730億米ドルの収益を生み出しました。賃貸住宅市場の拡大と不動産投資の増加により、家主向けに特化した保険商品の需要が高まっています。米国の大手保険業者は、テクノロジー主導のソリューション、個別化された補償、効率的なデジタル保険金請求処理に重点を置き、市場におけるイノベーションの先駆者となっています。

世界の住宅保険市場の主要企業には、Chubb、Allianz、Liberty Mutual、Nationwide Mutual、Progressive Insuranceなどが含まれます。住宅保険市場における地位を強化するため、各社はテクノロジーの活用と顧客体験の向上に注力しています。保険契約管理や保険金請求処理にデジタルプラットフォームを採用する企業も多く、顧客は保険会社とリアルタイムで、自分の都合に合わせてやり取りできるようになっています。パーソナライズされた保険商品の人気が高まっており、保険会社はデータ分析や高度なリスクモデルを用いて、住宅所有者一人ひとりのニーズに合わせて保険をカスタマイズしています。保険会社はAIを活用したクレーム管理ツールに投資することで、プロセスを迅速化し、正確性を高め、顧客満足度を向上させています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 住宅所有者/保険契約者

- 保険会社

- 保険代理店・ブローカー

- サードパーティのサービスプロバイダー

- 最終用途

- 利益率分析

- 気候リスク曝露分析

- 山火事発生地域と保険への影響

- 洪水が発生しやすい地域とカバー範囲のギャップ

- 熱波、嵐、そして構造的レジリエンス

- テクノロジーとイノベーションの情勢

- 特許分析

- ユースケース

- 住宅保険統計

- 平均保険料

- 請求データ

- 地域による違い

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 成長促進要因

- 住宅所有率の上昇

- 不動産価値の上昇

- リスク保護に対する意識の高まり

- 気候変動と自然災害

- 業界の潜在的リスク・課題

- 高額な保険料

- 複雑なポリシー条件と透明性の欠如

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:範囲別、2021年~2034年

- 主要動向

- 住居保険

- 火と煙

- 自然災害

- 破壊行為と盗難

- 建設上の欠陥

- コンテンツ範囲

- 高価値商品

- 家具と衣類

- 一時的な移転

- 賠償責任保険

- 個人責任

- 他人への医療費の支払い

- アンブレラ責任

第6章 市場推計・予測:プロバイダ別、2021年~2034年

- 主要動向

- 保険会社

- 保険代理店/ブローカー

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 家主

- 不動産所有者

- テナント

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第9章 企業プロファイル

- ADMIRAL

- ALLIANZ

- Allstate Insurance Company

- American Family Insurance

- American International Group

- Assicurazioni Generali

- AXA Group

- Chubb

- Covea Group

- Erie Insurance

- Farmers Insurance

- FM Global

- Hartford Financial Services Group

- Liberty Mutual Insurance Company

- Nationwide Mutual Insurance Company

- Progressive Insurance

- State Farm Mutual Automobile Insurance Company

- Tokio Marine Holdings

- Travelers Insurance

- USAA Investment Services Company

目次

The Global Home Insurance Market was valued at USD 234.6 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 475.3 billion by 2034, driven by the increasing rates of homeownership and rising property values. As housing markets worldwide continue to experience high demand and investment, the need for home insurance has become more crucial. Homeowners are now more focused on securing not just the structure of their homes, but also the lifestyle and liabilities associated with them. This shift has led insurers to offer more flexible policies tailored to individual risk profiles and specific regional hazards. With homes becoming valuable and sentimental assets, insurance is no longer just a requirement; it is now a strategic priority to preserve wealth and ensure responsible homeownership.

A key factor driving the evolution of the home insurance market is the increasing number of first-time homebuyers, especially among younger generations. These new homeowners have different expectations, favoring digital-first interactions, real-time policy management, and responsive customer service. As the value of residential properties continues to rise, insurers are investing in new technologies, such as advanced analytics, satellite imagery, and IoT data, to offer personalized coverage and better risk assessment. This trend transforms home insurance providers into trusted partners in the homeowner's journey, beyond just protecting physical assets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $234.6 Billion |

| Forecast Value | $475.3 Billion |

| CAGR | 8.5% |

In 2024, the dwelling coverage segment held a 71.1% share and is expected to grow at a CAGR of 9% during 2025-2034. Dwelling coverage is crucial for homeowners as it protects against structural damage caused by fire, theft, vandalism, and natural disasters. This coverage is essential for all types of properties, from urban apartments to suburban homes, and insurers are making improvements such as inflation-adjusted rebuilding costs and region-specific risk models to ensure more robust protection.

The insurance companies segment led the market in 2024, with a 58.1% share, and is expected to grow at a CAGR of 9.3% through 2034. These companies are central to the home insurance industry, offering comprehensive underwriting, risk assessment, and claims management. Their ability to manage large-scale risks and flexible coverage plans has helped them dominate the market in developed and emerging regions. Their scale and actuarial expertise allow them to meet the diverse needs of homeowners effectively.

U.S. Home Insurance Market held 81.3% share and generated USD 73 billion in 2024 driven by a robust rental property sector, strong regulatory frameworks, and increasing awareness of the importance of risk management among homeowners. The expanding rental housing market and rising property investments have led to a growing demand for specialized insurance products for landlords. Leading insurance providers in the U.S. are pioneering innovations in the market, focusing on technology-driven solutions, personalized coverage, and efficient digital claims processing.

Key players in the Global Home Insurance Market include Chubb, Allianz, Liberty Mutual, Nationwide Mutual, and Progressive Insurance, among others. To strengthen their position in the home insurance market, companies are focusing on leveraging technology and enhancing customer experience. Many are adopting digital platforms for policy management and claims processing, allowing customers to interact with insurers in real time and on their terms. Personalized insurance products are becoming increasingly popular, with insurers using data analytics and advanced risk models to tailor policies to individual homeowners' needs. Insurers invest in AI-driven claims management tools to speed up processes, increase accuracy, and improve customer satisfaction.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Homeowners / Policyholders

- 3.2.2 Insurance providers / Carriers

- 3.2.3 Insurance agents & brokers

- 3.2.4 Third-party service providers

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Climate risk exposure analysis

- 3.4.1 Wildfire zones and insurance implications

- 3.4.2 Flood-prone regions and coverage gaps

- 3.4.3 Heatwaves, storms, and structural resilience

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Use cases

- 3.8 Home insurance statistics

- 3.8.1 Average premiums

- 3.8.2 Claims data

- 3.8.3 Regional variations

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Increasing home ownership rates

- 3.11.1.2 Rising property values

- 3.11.1.3 Growing awareness of risk protection

- 3.11.1.4 Climate change and natural disasters

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High premium costs

- 3.11.2.2 Complex policy terms and lack of transparency

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Coverage, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Dwelling Coverage

- 5.2.1 Fire & smoke

- 5.2.2 Natural disasters

- 5.2.3 Vandalism & theft

- 5.2.4 Construction defects

- 5.3 Content Coverage

- 5.3.1 High-value items

- 5.3.2 Furniture and clothing

- 5.3.3 Temporary relocation

- 5.4 Liability Coverage

- 5.4.1 Personal liability

- 5.4.2 Medical payments to others

- 5.4.3 Umbrella liability

Chapter 6 Market Estimates & Forecast, By Provider, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Insurance companies

- 6.3 Insurance agents/brokers

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Landlords

- 7.3 Property owners

- 7.4 Tenant

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 ADMIRAL

- 9.2 ALLIANZ

- 9.3 Allstate Insurance Company

- 9.4 American Family Insurance

- 9.5 American International Group

- 9.6 Assicurazioni Generali

- 9.7 AXA Group

- 9.8 Chubb

- 9.9 Covea Group

- 9.10 Erie Insurance

- 9.11 Farmers Insurance

- 9.12 FM Global

- 9.13 Hartford Financial Services Group

- 9.14 Liberty Mutual Insurance Company

- 9.15 Nationwide Mutual Insurance Company

- 9.16 Progressive Insurance

- 9.17 State Farm Mutual Automobile Insurance Company

- 9.18 Tokio Marine Holdings

- 9.19 Travelers Insurance

- 9.20 USAA Investment Services Company

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日