|

市場調査レポート

商品コード

1755370

衛生用紙の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Hygienic Paper Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 衛生用紙の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月29日

発行: Global Market Insights Inc.

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

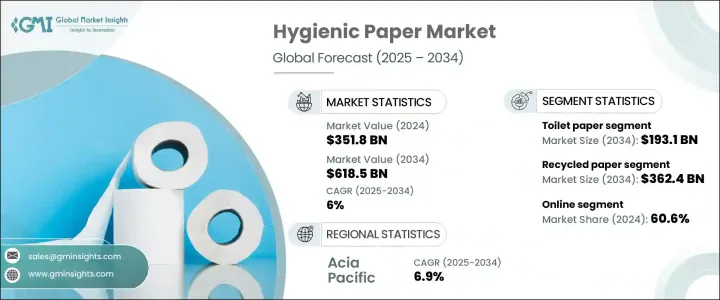

衛生用紙の世界市場規模は、2024年に3,518億米ドルとなり、CAGR6%で成長し、2034年には6,185億米ドルに達すると予測されています。

同市場の力強い成長軌道は、環境に優しい製品に対する消費者の嗜好の高まり、衛生基準の高まり、環境意識の高まりに大きく後押しされています。今日の買い物客は、生態系への影響を意識するようになり、環境に配慮した価値観に沿った持続可能な代替品を積極的に求めるようになっています。このような行動の変化は、特に消費者が安全性と環境保護を重視する中、リサイクル衛生用紙の需要急増に拍車をかけています。また、世界の健康問題に対する社会的関心も、個人と地域社会の衛生習慣が進化し続ける中で、ティッシュ、ウェットティッシュ、その他の衛生関連製品の普及に寄与しています。

このような行動変遷は、環境教育や広範なメディア報道の影響を大きく受けた、持続可能性を目指す広範な文化的動きによって強化されています。企業はこうした価値観を反映させるために製品やサプライチェーンを再設計することで対応し、急速に変化する市場において適切な存在であり続けています。持続可能なイノベーションと企業責任は、今や競合戦略の中心となっています。政府もまた、より厳格な環境政策を制定する一方で、持続可能な製造を奨励するインセンティブを提供することで、その役割を果たしています。こうした規制は、消費者の期待や技術の向上と相まって、環境の完全性を損なうことなく衛生基準を満たす、環境に配慮した製品の開発につながっています。先端材料と持続可能なプロセスの使用により、効果的で環境に配慮した衛生用紙の生産が可能になり、世界市場に長期的な成長の可能性が生まれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 3,518億米ドル |

| 予測金額 | 6,185億米ドル |

| CAGR | 6% |

衛生用紙市場は、タイプ別にトイレットペーパー、フェイシャルティッシュ、ペーパータオル、ナプキン、ウェットティッシュ、その他(キッチンペーパー、薬用ペーパーを含む)に区分されます。このうち、トイレットペーパーは2024年に圧倒的なシェアを占め、1,040億米ドルの収益を上げ、2034年には1,931億米ドルに達すると予測されています。トイレットペーパーは家庭、企業、公衆トイレで広く使用されており、安定した需要を確保しています。他の衛生用紙製品とは異なり、トイレットペーパーは代替不可能であり、人口構成や地域を問わず一貫して消費されます。多くの開発途上国では、都市人口が増加し、近代的な衛生設備が利用できるようになったため、使用量がさらに増加しています。また、まとめ買いの習慣も、衛生用紙分野の定番商品としての信頼性を高めています。

供給源の観点から、市場はバージンパルプと再生紙に分類されます。2024年の市場規模は再生紙が2,031億米ドルで圧倒的であり、2034年には3,624億米ドルに達すると予想されています。この分野は、環境に安全な選択肢を求める消費者と企業の嗜好の高まりにより、引き続きリードしています。リサイクル衛生用紙は、廃棄物を最小限に抑えるだけでなく、コスト面でも有利であるため、メーカーとバイヤーの双方にとって魅力的です。リサイクル工程の改善により、製品の品質は大幅に向上し、性能と持続可能性のギャップを埋めています。対照的に、バージンパルプは、高級製品向けの高級な品質を提供する一方で、資源集約的な採取方法を伴い、環境に悪影響を及ぼします。これらの要因から、持続可能性が世界的に支持される中、再生紙がより現実的な選択肢となっています。

衛生用紙市場の流通チャネルには、オンラインとオフラインのプラットフォームがあります。2024年にはオンライン販売が市場の約60.6%を占め、2034年までのCAGRは6.5%と予想されています。デジタル・プラットフォームは、便利で迅速な非接触型ショッピングを求める消費者の嗜好の変化により、優位性を獲得しています。eコマースは、価格比較を容易にし、幅広い製品群へのアクセスを可能にし、定期購入を可能にします。さらに、多くのメーカーがオンライン体験の強化を通じて消費者直販戦略を強化しており、デジタル・チャネルの魅力をさらに高めています。

地域別では、アジア太平洋が2024年の衛生用紙世界市場で大きなシェアを占めており、予測期間中のCAGRは6.9%と最も高く成長すると予測されています。この地域内では、中国だけが2024年に780億米ドル以上の貢献をしており、2034年には1,587億米ドルに達する勢いです。都市化の進展、生活水準の向上、可処分所得の増加が需要を押し上げる主な要因です。衛生面や環境に優しいことに対する意識が高まる中、この地域の消費者は高品質でブランド力のある紙製品を受け入れています。メーカー各社も、この需要増を支えるため、地域の生産・流通インフラへの投資で対応しています。

競合衛生用紙業界の主要企業は、競争力を維持するために、持続可能性、製品イノベーション、効率的なサプライチェーンマネジメントに注力しています。主要企業は、市場シェアの維持と長期的な成長を達成するために、世界の環境動向と消費者の期待の変化に対応した事業戦略をとっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- サプライヤーの情勢

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- 影響要因

- 促進要因

- 環境に優しい製品に対する消費者の嗜好の高まり

- 衛生基準の向上

- 環境問題への意識の高まりと持続可能な慣行への移行

- 業界の潜在的リスク&課題

- 紙の生産に必要なエネルギー集約型プロセス

- 原材料費とサプライチェーンの問題

- 促進要因

- 成長可能性分析

- 消費者購買行動分析

- 人口動向

- 購入決定に影響を与える要因

- 消費者製品の採用

- 優先流通チャネル

- 希望価格帯

- 規制情勢

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 産業構造と集中

- 競争強度評価

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 製品の位置付け

- 価格性能比ポジショニング

- 地理的プレゼンス

- イノベーション能力

- 戦略的ダッシュボード

- Competitive benchmarking

- Strategic initiatives assessment

- SWOT analysis of key players

- Future competitive outlook

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- トイレットペーパー

- シングルプライ

- 二重層

- その他(三重織など)

- ティッシュペーパー

- ペーパータオル

- ロールタオル

- 折りたたんだタオル

- その他(センタープルタオルなど)

- ナプキン

- ウェットティッシュ

- その他(薬用紙、キッチンペーパーなど)

第6章 市場推計・予測:由来別、2021年~2034年

- 主要動向

- バージンパルプ

- 再生紙

第7章 市場推計・予測:価格別、2021年~2034年

- 主要動向

- 低

- 中

- 高

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 家庭用

- 商業用

- ホレカ

- 企業

- ヘルスケア

- その他(スパ、施設など)

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- オンライン

- eコマース

- 企業ウェブサイト

- オフライン

- スーパーマーケット/ハイパーマーケット

- 専門店

- その他(個人店舗等)

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- APP

- Cascades

- Essity

- Georgia-Pacific

- Hengan

- Kimberly-Clark

- Mondi

- Nine Dragons Paper

- Oji

- Paperlinx

- Procter &Gamble

- Sofidel

- Suzano

- Vinda

- Wausau Paper

The Global Hygienic Paper Market was valued at USD 351.8 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 618.5 billion by 2034. The market's strong growth trajectory is largely driven by rising consumer preference for eco-friendly products, heightened hygiene standards, and growing environmental consciousness. Shoppers today are increasingly aware of their ecological impact and actively seek sustainable alternatives that align with green values. This shift in behavior has fueled a surge in demand for recycled hygienic paper, especially as consumers place a premium on safety and environmental protection. Public concern over global health issues has also contributed to the widespread adoption of tissues, wipes, and other hygiene-related products as both individual and community hygiene practices continue to evolve.

This behavioral transition is being reinforced by a broader cultural movement toward sustainability, heavily influenced by environmental education and widespread media coverage. Businesses are responding by redesigning products and supply chains to reflect these values, ensuring they stay relevant in a rapidly changing market. Sustainable innovation and corporate responsibility are now central to competitive strategies. Governments are also playing a role by enacting stricter environmental policies while offering incentives to encourage sustainable manufacturing. These regulations, coupled with consumer expectations and technological improvements, are leading to the development of eco-conscious products that meet hygiene standards without compromising environmental integrity. The use of advanced materials and sustainable processes has made it feasible to produce hygienic paper that is both effective and environmentally responsible, creating long-term growth potential for the global market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $351.8 Billion |

| Forecast Value | $618.5 Billion |

| CAGR | 6% |

The hygienic paper market is segmented by type into toilet paper, facial tissues, paper towels, napkins, wet wipes, and others, which include kitchen and medicinal paper. Among these, toilet paper held the dominant share in 2024, generating USD 104 billion in revenue, and is projected to reach USD 193.1 billion by 2034. Its widespread usage in homes, businesses, and public restrooms ensures steady demand. Unlike other hygienic paper products, toilet paper is non-substitutable and consumed consistently across demographics and geographies. In many developing nations, growing urban populations and access to modern sanitation have further fueled usage. Bulk purchasing habits also contribute to the product's reliability as a staple in the hygiene paper segment.

In terms of sources, the market is categorized into virgin pulp and recycled paper. In 2024, recycled paper dominated with a market value of USD 203.1 billion and is expected to climb to USD 362.4 billion by 2034. This segment continues to lead due to the increasing consumer and business preference for environmentally safe options. Recycled hygienic paper not only minimizes waste but also offers cost advantages, making it attractive for both manufacturers and buyers. Improvements in recycling processes have significantly enhanced product quality, bridging the gap between performance and sustainability. In contrast, virgin pulp, while offering high-end quality for premium products, involves resource-intensive extraction methods that negatively impact the environment. These factors make recycled paper the more viable option as sustainability gains traction globally.

Distribution channels in the hygienic paper market include online and offline platforms. In 2024, online sales accounted for approximately 60.6% of the market and are expected to grow at a CAGR of 6.5% through 2034. Digital platforms have gained dominance due to shifting consumer preferences for convenient, fast, and contactless shopping. E-commerce enables easy price comparison, access to a wide product range, and subscription-based purchasing, which suits both individuals and corporate buyers. Moreover, many manufacturers are strengthening their direct-to-consumer strategies through enhanced online experiences, making digital channels even more appealing.

Regionally, Asia Pacific captured a significant share of the global hygienic paper market in 2024 and is projected to grow at the highest CAGR of 6.9% during the forecast period. Within this region, China alone contributed over USD 78 billion in 2024 and is on track to reach USD 158.7 billion by 2034. Rising urbanization, improved living standards, and increasing disposable income are key factors boosting demand. With heightened awareness around hygiene and eco-friendly practices, consumers in the region are embracing high-quality and branded paper products. Manufacturers are also responding with investments in regional production and distribution infrastructure to support this growing demand.

Leading companies in the hygienic paper industry are focusing on sustainability, product innovation, and efficient supply chain management to remain competitive. Key players are aligning their business strategies with global environmental trends and evolving consumer expectations to maintain market share and achieve long-term growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Supplier Landscape

- 3.1.3 Profit margin analysis

- 3.1.4 Disruptions

- 3.1.5 Future outlook

- 3.1.6 Manufacturers

- 3.1.7 Distributors

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer preference for eco-friendly products

- 3.2.1.2 Increased Hygiene Standard

- 3.2.1.3 Growing awareness of environmental issues and a shift towards sustainable practices

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Energy-intensive processes required for paper production

- 3.2.2.2 Raw material costs and supply chain issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Consumer buying behavior analysis

- 3.4.1 Demographic trends

- 3.4.2 Factors affecting buying decision

- 3.4.3 Consumer product adoption

- 3.4.4 Preferred distribution channel

- 3.4.5 Preferred price range

- 3.5 Regulatory landscape

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.1.1 Industry structure and concentration

- 4.1.2 Competitive intensity assessment

- 4.1.3 Company market share analysis

- 4.1.4 Competitive positioning matrix

- 4.1.4.1 Product positioning

- 4.1.4.2 Price-performance positioning

- 4.1.4.3 Geographic presence

- 4.1.4.4 Innovation capabilities

- 4.1.5 Strategic dashboard

- 4.1.5.1 Competitive benchmarking

- 4.1.5.1.1 Manufacturing capabilities

- 4.1.5.1.2 Product portfolio strength

- 4.1.5.1.3 Distribution network

- 4.1.5.1.4 R&D investments

- 4.1.5.2 Strategic initiatives assessment

- 4.1.5.3 SWOT analysis of key players

- 4.1.5.4 Future competitive outlook

- 4.1.5.1 Competitive benchmarking

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Toilet paper

- 5.2.1 Single ply

- 5.2.2 Double ply

- 5.2.3 Others (Triple ply, etc.)

- 5.3 Facial tissues

- 5.4 Paper towels

- 5.4.1 Roll towels

- 5.4.2 Folded towels

- 5.4.3 Others (Center-pull towels, etc.)

- 5.5 Napkins

- 5.6 Wet wipes

- 5.7 Others (medicinal paper, kitchen paper, etc.)

Chapter 6 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Virgin pulp

- 6.3 Recycled paper

Chapter 7 Market Estimates & Forecast, By Price, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Household

- 8.3 Commercial

- 8.3.1 HoReCa

- 8.3.2 Corporate

- 8.3.3 Healthcare

- 8.3.4 Others (Spa, Institutional, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Company website

- 9.3 Offline

- 9.3.1 Supermarket/hypermarket

- 9.3.2 Specialty stores

- 9.3.3 Others (Individual stores, etc.)

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 APP

- 11.2 Cascades

- 11.3 Essity

- 11.4 Georgia-Pacific

- 11.5 Hengan

- 11.6 Kimberly-Clark

- 11.7 Mondi

- 11.8 Nine Dragons Paper

- 11.9 Oji

- 11.10 Paperlinx

- 11.11 Procter & Gamble

- 11.12 Sofidel

- 11.13 Suzano

- 11.14 Vinda

- 11.15 Wausau Paper