調味料の市場機会、成長促進要因、業界動向分析、2025年~2034年予測

Seasoning Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755335

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

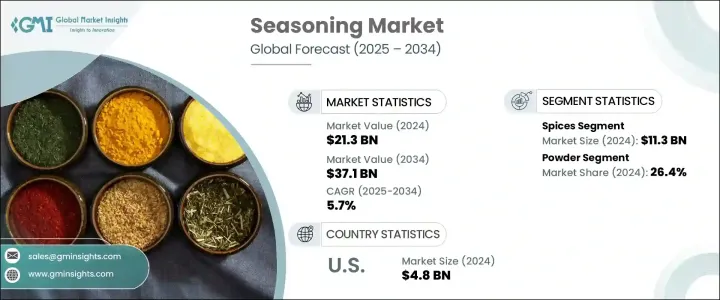

調味料の世界市場は、2024年には213億米ドルとなり、食生活の変化、便利な食品の人気の高まり、食品の風味を高めることへの関心の高まりなどを背景に、CAGR5.7%で成長し、2034年までには371億米ドルに達すると予測されています。

世界経済の変動にもかかわらず、調味料の需要は、先進経済諸国および新興経済諸国の家庭の台所や業務用食品産業において不可欠な役割を担っているため、引き続き堅調です。調味料は、単に風味をつけるためだけでなく、世界各国の料理において信憑性を保つためにも不可欠なものとなっています。

技術の向上と世界化の進展により、多様なハーブやスパイスの入手可能性が世界的に広がり、より複雑で独自のスパイスブレンドが生み出されるようになりました。こうした開発により、包装食品や調理済み食品に調味料をシームレスに組み込むことが可能になりました。都市化が進み、世界各国の料理に接する機会が増えるにつれ、市場は活況を呈しています。消費者はクリーンラベル、ナチュラル、非遺伝子組み換えの製品を明確に好む傾向を示しており、これが各企業に成分の透明性と持続可能性の革新を促しています。料理用途に加え、機能性食品に対する需要の高まりが、健康上の利点を強化した調味料製品の使用をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 213億米ドル |

| 予測金額 | 371億米ドル |

| CAGR | 5.7% |

スパイスに基づく調味料分野の2024年の市場規模は113億米ドルで、2034年までのCAGRは5.6%と予測されます。スパイスは、味と栄養価の両方を高める役割を果たすため、食品調理に欠かせない存在であり続けています。伝統的な料理から現代的なレシピまで幅広く使用されているのは、健康志向の高まりと地域特有の味に対する世界の評価が背景にあります。消費者がターメリック、チリ、クミン、パプリカなどのスパイスを求め続けるのは、味だけでなくその健康効果もあるからです。ホール、粉砕、抽出物など、さまざまな形態でスパイスを使用できる柔軟性も、スパイスの持続的な魅力を高めています。さらに、eコマースや小売店の増加により、スパイスはより身近なものとなっています。

粉末調味料分野は2024年に181億米ドルを生み出し、26.4%のシェアを占め、2025年から2034年にかけてCAGR5.5%で成長するとみられています。安定したテクスチャーと保存のしやすさは、特に均一な味と保存期間の長さが鍵となる加工・包装食品において、粉末調味料に大きな優位性を与えています。消費者やメーカーは、ルビー、スープ、ソース、スナック、ミールキットなどの用途に粉末タイプを好みます。さらに、これらの調味料は輸送や保存にコスト効率がよく、人気の高まりに貢献しています。

米国の調味料市場は2024年に48億米ドルを生み出し、2025年から2034年にかけてCAGR6%で成長すると予想されています。同市場は、高い国内消費、強力な食品加工能力、有機・天然素材への広範なシフトから恩恵を受けています。多文化料理、特にアジア、地中海、ラテンアメリカの料理の人気が高まっているため、ブレンドされたエスニックなスパイスの組み合わせに対する需要が高まっています。同時に、家庭料理、ソーシャルメディアの影響力、グルメ料理への関心が急上昇しています。減塩やアレルゲンフリーのブレンドスパイスなど、健康志向のイノベーションが重要なセールスポイントになりつつあります。このような力関係により、米国は世界の調味料業界のリーダーとなっています。

世界の調味料市場で活躍する企業は、Givaudan SA、Olam International、McCormick & Company, Inc.、Kerry Group plc、Ajinomoto Co., Incです。調味料業界の企業は、市場フットプリントを確保・拡大するため、的を絞った戦略を実施しています。その多くは、文化的に多様なブレンドや、クリーンラベルの需要に応えるより健康的な代替品を導入しています。製品の革新が中心で、各ブランドは減塩や保存料不使用など、風味と健康のバランスをとったスパイスの処方を展開しています。eコマースへの進出は、カスタマイズ可能なパッケージや定期購入ベースのスパイスキットを提供しながら、より幅広い消費者層へのリーチを可能にしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

- TAM分析、2025年~2034年

- CXOの視点:戦略的必須事項

- 経営上の意思決定ポイント

- 重要な成功要因

- 将来の見通しと戦略的提言

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 成長促進要因

- エスニック料理やエキゾチック料理の需要増加

- グルメ料理への消費者の関心の高まり

- クリーンラベル製品への選好の高まり

- 外食産業の成長

- 業界の潜在的リスク・課題

- 原材料価格の変動

- 食品添加物に関する厳しい規制

- 市場機会

- 成長促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ハーブ

- バジル

- オレガノ

- タイム

- ローズマリー

- パセリ

- その他

- スパイス

- ペッパー

- シナモン

- クミン

- ターメリック

- カルダモン

- クローブ

- その他

- 塩と塩の代替品

- 食塩

- 海塩

- ヒマラヤ塩

- 低ナトリウム塩

- その他

- 調味料ブレンド

- イタリアン調味料

- ケイジャン調味料

- カレー粉

- タコス調味料

- ガラムマサラ

- その他

- その他

第6章 市場推計・予測:形態別、2021年~2034年

- 主要動向

- 粉末

- 全体/インタクト

- 粉砕/挽いて細かくした

- 液体

- ペースト

- その他

第7章 市場推計・予測:性質別、2021年~2034年

- 主要動向

- 従来型

- オーガニック

- 非遺伝子組み換え

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 肉類・鶏肉

- スナック・コンビニエンスフード

- スープ、ソース、ドレッシング

- ベーカリー・菓子類

- シーフード

- 冷凍食品

- 飲料

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 食品加工業界

- 外食産業

- レストラン

- ホテル

- カフェ

- ファーストフードチェーン

- その他

- 小売/家庭用

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- B2B

- B2C

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- 専門店

- オンライン小売

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Ajinomoto Co., Inc.

- Ariake Japan Co., Ltd.

- Baria Pepper

- British Pepper &Spice Co Ltd

- Dohler GmbH

- DS Group

- Everest Spices

- Firmenich SA

- Frontier Co-op

- Fuchs Gewurze GmbH

- Givaudan SA

- Kerry Group plc

- McCormick &Company, Inc.

- MDH Spices

- Nestle S.A.

- Olam International

- Sensient Technologies Corporation

- Symrise AG

- The Kraft Heinz Company

- Unilever PLC

目次

The Global Seasoning Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 37.1 billion by 2034, fueled by changing dietary habits, the rising popularity of convenient food products, and a heightened interest in enhancing food flavor. Despite fluctuations in the global economy, the demand for seasoning remains strong due to its indispensable role in household kitchens and the commercial food industry across developed and emerging economies. Seasonings have become integral not just for flavor but also for preserving authenticity in global cuisines.

Technological improvements and increasing globalization have broadened the availability of diverse herbs and spices worldwide, giving rise to more complex and tailored spice blends. These developments have enabled the seamless incorporation of seasonings into packaged and ready-to-eat food segments. As urbanization and exposure to international cuisines rise, the market thrives. Consumers are showing a clear preference for clean-label, natural, and non-GMO products, which is encouraging companies to innovate in ingredient transparency and sustainability. In addition to culinary uses, the increasing demand for functional foods further boosts the use of seasoning products enriched with health benefits.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $37.1 Billion |

| CAGR | 5.7% |

The seasoning segment based on spices was valued at USD 11.3 billion in 2024 and is projected to grow at a CAGR of 5.6% through 2034. Spices remain vital in food preparation thanks to their role in enhancing both taste and nutritional value. Their widespread use in traditional dishes and contemporary recipes alike is driven by rising health consciousness and the global appreciation for regional flavors. Consumers continue to demand spices like turmeric, chili, cumin, and paprika not only for taste but for their wellness properties. The flexibility of using spices in different formats-whether whole, ground or as extracts-adds to their sustained appeal. Moreover, growing e-commerce and retail availability have made spices more accessible.

The powdered seasoning segment generated USD 18.1 billion in 2024, holding a 26.4% share, and is set to grow at a CAGR of 5.5% from 2025 to 2034 driven by the convenience and compatibility with a wide range of recipes. The consistent texture and ease of storage give powdered seasonings a significant edge, particularly in processed and packaged foods where uniform taste and longer shelf life are key. Consumers and manufacturers prefer powdered formats for applications in rubs, soups, sauces, snacks, and meal kits. Additionally, these seasonings are cost-effective to transport and store, contributing to their growing popularity.

U.S. Seasoning Market generated USD 4.8 billion in 2024 and is expected to grow at a CAGR of 6% from 2025 to 2034. The market benefits from high domestic consumption, strong food processing capabilities, and a widespread shift toward organic and natural ingredients. The growing popularity of multicultural cuisines-particularly those from Asia, the Mediterranean, and Latin America-has sparked increased demand for blended and ethnic spice combinations. Simultaneously, home cooking, social media influence, and interest in gourmet meal preparation have surged. Health-focused innovations, such as low-sodium and allergen-free spice blends, are becoming key selling points. These dynamics position the U.S. as a leader in the global seasoning industry.

Companies active in the Global Seasoning Market include: Givaudan SA, Olam International, McCormick & Company, Inc., Kerry Group plc, and Ajinomoto Co., Inc. To secure and expand their market footprint, companies in the seasoning industry are implementing targeted strategies. Many are introducing culturally diverse blends and healthier alternatives that cater to clean-label demands. Product innovation is central-brands are rolling out spice formulations that balance flavor and health, such as low-sodium and preservative-free options. Expansion into e-commerce has enabled companies to reach broader consumer segments while offering customizable packaging and subscription-based spice kits.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Product type

- 2.2.1.3 Form

- 2.2.1.4 Nature

- 2.2.1.5 Application

- 2.2.1.6 End use

- 2.2.1.7 Distribution channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for ethnic and exotic cuisines

- 3.2.1.2 Rising consumer interest in gourmet cooking

- 3.2.1.3 Increasing preference for clean label products

- 3.2.1.4 Growth in the food service industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Stringent regulations on food additives

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Herbs

- 5.2.1 Basil

- 5.2.2 Oregano

- 5.2.3 Thyme

- 5.2.4 Rosemary

- 5.2.5 Parsley

- 5.2.6 Others

- 5.3 Spices

- 5.3.1 Pepper

- 5.3.2 Cinnamon

- 5.3.3 Cumin

- 5.3.4 Turmeric

- 5.3.5 Cardamom

- 5.3.6 Cloves

- 5.3.7 Others

- 5.4 Salt & salt substitutes

- 5.4.1 Table salt

- 5.4.2 Sea salt

- 5.4.3 Himalayan salt

- 5.4.4 Low-sodium salt

- 5.4.5 Others

- 5.5 Seasoning blends

- 5.5.1 Italian seasoning

- 5.5.2 Cajun seasoning

- 5.5.3 Curry powder

- 5.5.4 Taco seasoning

- 5.5.5 Garam masala

- 5.5.6 Others

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Whole/intact

- 6.4 Crushed/ground

- 6.5 Liquid

- 6.6 Paste

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Nature, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Conventional

- 7.3 Organic

- 7.4 Non-GMO

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Meat & Poultry

- 8.3 Snacks & convenience food

- 8.4 Soups, sauces & dressings

- 8.5 Bakery & confectionery

- 8.6 Seafood

- 8.7 Frozen foods

- 8.8 Beverages

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Food processing industry

- 9.3 Food service industry

- 9.3.1 Restaurants

- 9.3.2 Hotels

- 9.3.3 Cafes

- 9.3.4 Fast food chains

- 9.3.5 Others

- 9.4 Retail/household

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 B2B

- 10.3 B2C

- 10.3.1 Supermarkets/hypermarkets

- 10.3.2 Convenience stores

- 10.3.3 Specialty stores

- 10.3.4 Online retail

- 10.3.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Ajinomoto Co., Inc.

- 12.2 Ariake Japan Co., Ltd.

- 12.3 Baria Pepper

- 12.4 British Pepper & Spice Co Ltd

- 12.5 Dohler GmbH

- 12.6 DS Group

- 12.7 Everest Spices

- 12.8 Firmenich SA

- 12.9 Frontier Co-op

- 12.10 Fuchs Gewurze GmbH

- 12.11 Givaudan SA

- 12.12 Kerry Group plc

- 12.13 McCormick & Company, Inc.

- 12.14 MDH Spices

- 12.15 Nestle S.A.

- 12.16 Olam International

- 12.17 Sensient Technologies Corporation

- 12.18 Symrise AG

- 12.19 The Kraft Heinz Company

- 12.20 Unilever PLC

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日