精製乳糖の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Refined Lactose Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755198

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

精製乳糖の世界市場は、2024年には9億9,080万米ドルとなり、飲食品、医薬品、動物飼料など様々な産業での需要増加を背景に、CAGR 5.1%で成長し、2034年には16億米ドルに達すると予測されています。

食品分野では、精製乳糖はベーカリー製品、菓子類、乳製品の甘味料や充填剤として利用されています。消費者の天然素材や加工度の低い素材への嗜好が、精製乳糖を合成甘味料に代わる健康的な甘味料として位置づけ、精製乳糖の需要をさらに促進しています。医薬品では、精製乳糖は圧縮性と溶解性に優れているため、錠剤やカプセル剤の賦形剤として使用され、市場の拡大に貢献しています。

さらに、精製乳糖を動物用飼料(特に子豚や子牛などの幼若な家畜用)に配合することで、消化器系の健康を促進し、初期のエネルギー代謝をサポートする高い効果が証明されています。この機能的な利点は、家畜の健康と急速な成長が経済的な存続に不可欠な畜産・酪農分野での採用の原動力となっています。生産者が飼料効率の改善と合成添加物の最小化を目指す中、乳糖は天然で嗜好性が高く、栄養豊富な成分です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 9億9,080万米ドル |

| 予測金額 | 16億米ドル |

| CAGR | 5.1% |

食品グレード分野は、加工食品におけるクリーンラベルの天然由来原料に対する消費者需要の増加に後押しされ、CAGR 5.2%で成長し、2034年までに7億7,980万米ドルに達すると予測されます。食品用乳糖は、そのマイルドな甘味と食感特性だけでなく、消化性と乳児栄養における重要な役割のために広く使用されています。ベーカリー、菓子類、乳製品における使用量の増加は、製剤化と機能性食品開発の革新と相まって、予測期間を通じてこのセグメントの持続的な勢いを促進すると予想されます。

精製乳糖の様々な形態の中で、粉末形態は2024年に59.8%を占めて最大の市場シェアを占め、2025年から2034年にかけてCAGR 6.8%で成長すると予測されています。粉末形態は汎用性が高く取り扱いが容易なため、医薬品、飲食品、乳児栄養など様々な用途に適しています。しかし、原料価格の変動や一貫した品質基準の要求といった課題は、成長に影響を与える可能性があります。純度と性能を高める加工技術の革新が、精製乳糖市場の継続的な拡大を促進すると予想されます。

北米の精製乳糖市場は2024年に34.7%のシェアを占めたが、これは同地域の酪農セクターが発展しており、医薬品用途で乳糖のニーズが高まっているためです。米国は、高度な生産能力と乳糖精製のための研究開発への高い投資により、この地域の市場シェアに大きく貢献しています。さらに、医薬品製剤における乳糖ベースの賦形剤の使用が増加していることも、この地域の市場成長を後押ししています。

世界の精製乳糖市場の主要企業は、Arla Foods Ingredients Group P/S、Fonterra Co-operative Group Limited、Lactalis Ingredients、FrieslandCampina Ingredients、Agropur Cooperative、Hilmar Cheese Company, Inc.などです。これらの企業は、製品ポートフォリオの拡大、生産能力の強化、研究開発への投資に注力し、様々な用途における精製乳糖の需要増に対応しています。市場での存在感を高めるため、世界の精製乳糖業界の企業はいくつかの重要な戦略を採用しています。これには、需要の増加に対応するための生産能力の拡大、製品品質の革新と向上のための研究開発への投資、流通網と市場リーチを強化するための戦略的パートナーシップや協力関係の構築などが含まれます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 主要メーカー

- 販売代理店

- 業界全体の利益率

- サプライチェーンと流通分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021年~2024年

- 主要輸出国、2021年~2024年

注:上記の貿易統計は主要国のみに提供されます

- 影響要因

- 促進要因

- 食品・飲料業界の需要増加

- 健康とウェルネスの動向

- 製薬業界の需要

- 動物飼料産業の拡大

- 業界の潜在的リスク&課題

- 乳糖不耐症の増加

- 原材料価格の変動

- 市場機会

- 市場の課題

- 市場機会

- 促進要因

- 原材料の情勢

- 製造業の動向

- 技術の進化

- 価格分析とコスト構造

- 価格動向(米ドル/トン)

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東アフリカ

- 価格要因(原材料、エネルギー、労働力)

- 地域による価格差

- コスト構造の内訳

- 収益性分析

- 価格動向(米ドル/トン)

- 規制の枠組みと基準

- 食品安全規制

- 医薬品品質基準

- 乳児用調製粉乳規制

- ラベル要件

- 輸出入規制

- ポーター分析

- PESTEL分析

- 製造プロセス分析

- ホエイ加工

- 結晶化技術

- 精製方法

- 乾燥と粉砕

- 品質管理手順

- 原材料分析と調達戦略

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業ヒートマップ分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- Expansion

- Mergers &acquisition

- Collaborations

- New product launches

- Research &development

- 主要企業による最近の動向と影響分析

- 企業分類

- 参加者の概要

- 財務実績

- 製品ベンチマーク

第5章 市場推計・予測:グレード別、2021年~2034年

- 主要動向

- 食品グレード

- 標準食品グレード

- 高純度食品グレード

- その他の食品グレード

- 医薬品グレード

- USP/EP/JPグレード

- 無水乳糖

- スプレー乾燥乳糖

- 一水和乳糖

- その他の医薬品グレード

- テクニカルグレード

- その他のグレード

第6章 市場推計・予測:形態別、2021年~2034年

- 主要動向

- 粉末

- 微粉末

- 粗粉

- 顆粒

- 粉砕顆粒

- 凝集顆粒

- クリスタル

- その他の形態

第7章 市場推計・予測:製造方法別、2021年~2034年

- 主要動向

- ホエイ由来乳糖

- スイートホエイ由来

- 酸性ホエイ由来

- 牛乳由来の乳糖

- その他の製造方法

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 食品・飲料

- 菓子類

- ベーカリー製品

- 乳製品

- 加工食品

- 飲料

- その他の食品用途

- 医薬品

- 錠剤製剤(賦形剤)

- カプセル製剤

- 吸入製品

- 注射剤

- その他の医薬品用途

- 乳児用調製粉乳

- 標準的な乳児用調製粉乳

- フォローアップフォーミュラ

- 特別な処方

- その他の乳児栄養製品

- 動物飼料

- 化粧品・パーソナルケア

- その他の用途

第9章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 食品・飲料業界

- 大手食品メーカー

- 中型・小型フードプロセッサー

- 職人による食品生産者

- 製薬業界

- 大手製薬会社

- ジェネリック医薬品メーカー

- 契約製造組織

- 乳児用調製粉乳メーカー

- 動物飼料産業

- 化粧品・パーソナルケア業界

- その他の最終用途産業

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直販/B2B

- 販売代理店および卸売業者

- オンラインチャネル

- その他の流通チャネル

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第12章 企業プロファイル

- Arla Foods Ingredients Group P/S

- Fonterra Co-operative Group Limited

- Lactalis Ingredients

- FrieslandCampina Ingredients

- Agropur Cooperative

- Hilmar Cheese Company, Inc.

- Leprino Foods Company

- Meggle Group GmbH

- DFE Pharma

- Kerry Group plc

- Milei GmbH(Hochdorf Group)

- Molkerei MEGGLE Wasserburg GmbH &Co. KG

- Actus Nutrition

目次

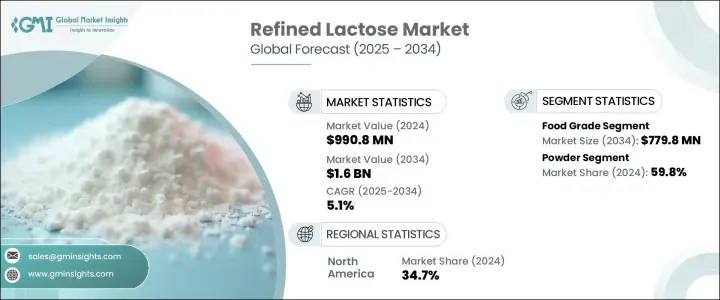

The Global Refined Lactose Market was valued at USD 990.8 million in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 1.6 billion by 2034, driven by increasing demand across various industries, including food and beverage, pharmaceuticals, and animal feed. In the food sector, refined lactose is utilized as a sweetener and filler in bakery items, confectioneries, and dairy products. Consumers' preference for natural and minimally processed ingredients has further fueled the demand for refined lactose, positioning it as a healthier alternative to synthetic sweeteners. In pharmaceuticals, refined lactose serves as an excipient in tablet and capsule formulations due to its excellent compressibility and solubility, contributing to the expansion of the market.

Additionally, incorporating refined lactose into animal feed formulations-especially for young livestock such as piglets and calves-has proven highly effective in promoting digestive health and supporting early-stage energy metabolism. This functional benefit drives its adoption in the livestock and dairy farming sectors, where animal health and rapid growth are critical for economic viability. As producers aim to improve feed efficiency and minimize synthetic additives, lactose is a natural, palatable, and nutrient-rich component.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $990.8 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 5.1% |

The food-grade segment is projected to reach USD 779.8 million by 2034, growing at a CAGR of 5.2% fueled by increasing consumer demand for clean-label, naturally derived ingredients in processed foods. Food-grade lactose is widely used not only for its mild sweetness and textural properties but also due to its digestibility and essential role in infant nutrition. Its rising usage in bakery, confectionery, and dairy products-coupled with innovation in formulation and functional food development-is expected to drive sustained momentum in this segment throughout the forecast period.

Among the various forms of refined lactose, the powder form held the largest market share, accounting for 59.8% in 2024, and is projected to grow at a CAGR of 6.8% from 2025 to 2034. The powder form's versatility and ease of handling make it suitable for various applications in pharmaceuticals, food and beverage industries, and infant nutrition. However, challenges such as fluctuating raw material prices and the requirement for consistent quality standards may impact growth. Innovations in processing techniques to enhance purity and performance are expected to drive the continued expansion of the refined lactose market.

North America Refined Lactose Market held a 34.7% share in 2024 due to the region's developed dairy sector and the growing need for lactose in pharmaceutical applications. The United States significantly contributes to this region's market share, owing to its sophisticated production capabilities and high investment in research and development for refining lactose. Additionally, the increasing use of lactose-based excipients in drug formulations continues to bolster market growth in this region.

Key players in the Global Refined Lactose Market include Arla Foods Ingredients Group P/S, Fonterra Co-operative Group Limited, Lactalis Ingredients, FrieslandCampina Ingredients, Agropur Cooperative, and Hilmar Cheese Company, Inc. These companies are focusing on expanding their product portfolios, enhancing production capacities, and investing in research and development to meet the rising demand for refined lactose across various applications. To strengthen their market presence, companies in the Global Refined Lactose Industry are adopting several key strategies. These include expanding production capacities to meet the growing demand, investing in research and development to innovate and improve product quality, and forming strategic partnerships and collaborations to enhance distribution networks and market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.1.4 Supply chain and distribution analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major exporting countries, 2021-2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only

- 3.4 Impact forces

- 3.4.1 Growth drivers

- 3.4.1.1 Rising demand in food & beverage industry

- 3.4.1.2 Health & wellness trends

- 3.4.1.3 Pharmaceutical industry demand

- 3.4.1.4 Expansion in animal feed industry

- 3.4.2 Industry pitfalls & challenges

- 3.4.2.1 Increasing lactose intolerance

- 3.4.2.2 Raw material price fluctuations

- 3.4.3 Market opportunities

- 3.4.4 Market challenges

- 3.4.5 Market opportunity

- 3.4.1 Growth drivers

- 3.5 Raw material landscape

- 3.5.1 Manufacturing trends

- 3.5.2 Technology evolution

- 3.6 Pricing analysis and cost structure

- 3.6.1 Pricing trends (USD/Ton)

- 3.6.1.1 North America

- 3.6.1.2 Europe

- 3.6.1.3 Asia Pacific

- 3.6.1.4 Latin America

- 3.6.1.5 Middle East Africa

- 3.6.2 Pricing factors (raw materials, energy, labor)

- 3.6.3 Regional price variations

- 3.6.4 Cost structure breakdown

- 3.6.5 Profitability analysis

- 3.6.1 Pricing trends (USD/Ton)

- 3.7 Regulatory framework and standards

- 3.7.1 Food safety regulations

- 3.7.2 Pharmaceutical quality standards

- 3.7.3 Infant formula regulations

- 3.7.4 Labeling requirements

- 3.7.5 Import/Export regulations

- 3.8 Porter's analysis

- 3.9 Pestel analysis

- 3.10 Manufacturing process analysis

- 3.10.1 Whey processing

- 3.10.2 Crystallization techniques

- 3.10.3 Purification methods

- 3.10.4 Drying & milling

- 3.10.5 Quality control procedures

- 3.11 Raw material analysis & procurement strategies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.6.1 Expansion

- 4.6.2 Mergers & acquisition

- 4.6.3 Collaborations

- 4.6.4 New product launches

- 4.6.5 Research & development

- 4.7 Recent developments & impact analysis by key players

- 4.7.1 Company categorization

- 4.7.2 Participant’s overview

- 4.7.3 Financial performance

- 4.8 Product benchmarking

Chapter 5 Market Estimates & Forecast, By Grade, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Food grade

- 5.2.1 Standard food grade

- 5.2.2 High purity food grade

- 5.2.3 Other food grades

- 5.3 Pharmaceutical Grade

- 5.3.1 USP/EP/JP grade

- 5.3.2 Anhydrous lactose

- 5.3.3 Spray-dried lactose

- 5.3.4 Monohydrate lactose

- 5.3.5 Other pharmaceutical grades

- 5.4 Technical grade

- 5.5 Other grades

Chapter 6 Market Estimates & Forecast, By Form, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.2.1 Fine powder

- 6.2.2 Coarse powder

- 6.3 Granules

- 6.3.1 Milled granules

- 6.3.2 Agglomerated granules

- 6.4 Crystals

- 6.5 Other forms

Chapter 7 Market Estimates & Forecast, By Production Method, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Whey-derived lactose

- 7.2.1 Sweet whey-derived

- 7.2.2 Acid whey-derived

- 7.3 Milk-derived lactose

- 7.4 Other production methods

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.2.1 Confectionery

- 8.2.2 Bakery products

- 8.2.3 Dairy products

- 8.2.4 Processed foods

- 8.2.5 Beverages

- 8.2.6 Other food applications

- 8.3 Pharmaceuticals

- 8.3.1 Tablet formulations (excipient)

- 8.3.2 Capsule formulations

- 8.3.3 Inhalation products

- 8.3.4 Injectable formulations

- 8.3.5 Other pharmaceutical applications

- 8.4 Infant formula

- 8.4.1 Standard infant formula

- 8.4.2 Follow-on formula

- 8.4.3 Specialty formula

- 8.4.4 Other infant nutrition products

- 8.5 Animal feed

- 8.6 Cosmetics & personal care

- 8.7 Other applications

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Food & beverage industry

- 9.2.1 Large food manufacturers

- 9.2.2 Medium & small food processors

- 9.2.3 Artisanal food producers

- 9.3 Pharmaceutical industry

- 9.3.1 Large pharmaceutical companies

- 9.3.2 Generic drug manufacturers

- 9.3.3 Contract manufacturing organizations

- 9.4 Infant formula manufacturers

- 9.4.1 Animal feed industry

- 9.4.2 Cosmetics & personal care industry

- 9.4.3 Other end-use industries

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct sales/B2B

- 10.3 Distributors & wholesalers

- 10.4 Online channels

- 10.5 Other distribution channels

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Arla Foods Ingredients Group P/S

- 12.2 Fonterra Co-operative Group Limited

- 12.3 Lactalis Ingredients

- 12.4 FrieslandCampina Ingredients

- 12.5 Agropur Cooperative

- 12.6 Hilmar Cheese Company, Inc.

- 12.7 Leprino Foods Company

- 12.8 Meggle Group GmbH

- 12.9 DFE Pharma

- 12.10 Kerry Group plc

- 12.11 Milei GmbH (Hochdorf Group)

- 12.12 Molkerei MEGGLE Wasserburg GmbH & Co. KG

- 12.13 Actus Nutrition

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日