バックアップ用レシプロ発電エンジン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Backup Reciprocating Power Generating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 115 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750587

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

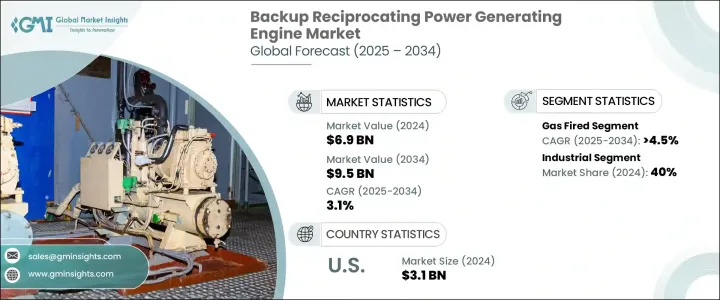

世界のバックアップ用レシプロ発電エンジン市場は、2024年には69億米ドルと評価され、信頼性の高いバックアップ電源システムの需要に牽引され、CAGR 3.1%で成長し、2034年には95億米ドルに達すると推定されます。

特に遠隔地での分散型エネルギー発電へのシフトが、市場をさらに拡大しています。これらのエンジンは、特に孤立した場所や脆弱な場所など、電気が途絶えやすい地域で安定した電力供給を確保するために不可欠です。バックアップ用レシプロエンジンは、非常用電源の提供に加え、電力の信頼性が重要な産業において、事業継続性を維持するためにますます重要になってきています。

新興経済諸国では電力供給が不安定になりつつあり、災害の多い地域ではエネルギーに対するニーズが高まっているため、バックアップ電源システムの採用が加速すると予想されます。さらに、モノのインターネット(IoT)対応エンジンの統合により、システムのインテリジェンスが強化され、予知保全が容易になるため、重要な遠隔アプリケーションの性能が向上します。排出規制の強化や産業部門における待機電力需要の高まりも、市場拡大に寄与しています。輸入部品への関税を含む規制状況の進展は、国際貿易に影響を与え、バックアップ発電エンジンの生産コストを上昇させる可能性があります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 69億米ドル |

| 予測金額 | 95億米ドル |

| CAGR | 3.1% |

ガス焚きバックアップ用レシプロ発電エンジン市場は、2034年まで4.5%のCAGRで堅調に成長すると予測されます。これは、環境規制の厳格化と天然ガスの値ごろ感の増加により、従来の発電方法に代わる実行可能で持続可能な選択肢となっているためです。熱電併給エンジンは、従来の化石燃料を動力とする発電機に比べて効率が高く、排出量が少ないため、信頼性の高い電力供給を維持しながら二酸化炭素排出量を削減したい産業にとって好ましい選択肢となっています。

これに加えて、熱電併給(CHP)システムも顕著な成長が見込まれており、2034年までのCAGRは4.5%と予想されています。エネルギー効率の高いソリューションに対する需要の高まりと、燃料消費量と運転コストの削減を求める企業の動きが、この動向の主な要因となっています。CHPシステムは、発電と廃熱回収を同時に行い、暖房に利用することで、エネルギー効率を向上させ、全体的な運用コストを削減する能力が特に評価されています。

米国のバックアップ用レシプロ発電エンジン2024年の市場規模は31億米ドルで、信頼できる電力に対する需要の増加を反映しています。この急増は、老朽化した送電網インフラの近代化と、停電時に継続的な電力を確保するためのバックアップシステムの必要性が主な原因です。加えて、商業・産業活動の拡大と相まって、様々な分野でエネルギー効率の高い技術の採用が拡大していることも、市場のさらなる成長を促進すると予想されます。

バックアップ用レシプロ発電エンジン世界市場の主要企業は、製品革新と市場拡大に注力し、その地位を強化しています。Rolls-Royce、MAN Energy Solutions、Wartsilaなどの企業は、エンジン性能と燃料効率を向上させるための研究開発への投資を増やしています。戦略的パートナーシップや買収も、新しい地域市場への参入や製品提供の強化に活用されています。さらに、企業は厳しい排ガス基準に適合するエンジンを開発することで、持続可能性に注力しています。こうした戦略は、さまざまな産業で信頼性が高く環境に優しいパワー・ソリューションに対する需要の高まりに対応するために採用されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:燃料タイプ別、2021年~2034年

- 主要動向

- ガス火力

- ディーゼル燃料

- デュアル燃料

- その他

第6章 市場規模・予測:定格出力別、2021年~2034年

- 主要動向

- 0.5MW~1MW

- 1MW~2MW以上

- 2MW~3.5MW以上

- 3.5MW~5MW以上

- 5MW~7.5MW以上

- 7.5MW以上

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 産業

- CHP

- エネルギー・ユーティリティ

- 埋立地とバイオガス

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- スペイン

- オランダ

- デンマーク

- ノルウェー

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- タイ

- シンガポール

- インドネシア

- マレーシア

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- オマーン

- クウェート

- イラン

- エジプト

- トルコ

- ヨルダン

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- ペルー

第9章 企業プロファイル

- AB Volvo Penta

- Atlas Copco

- Caterpillar

- Clarke Energy

- GE Vernova

- HIMOINSA

- Kirloskar

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Motorenfabrik Hatz

- Rehlko

- Rolls-Royce

- Scania

- Wartsila

- Yamaha Motor

- Yuchai International

目次

The Global Backup Reciprocating Power Generating Engine Market was valued at USD 6.9 billion in 2024 and is estimated to grow at a CAGR of 3.1% to reach USD 9.5 billion by 2034, driven by the demand for reliable backup power systems. The shift toward decentralized energy generation, particularly in remote areas, is further expanding the market. These engines are vital for ensuring a consistent power supply in areas prone to electrical disruptions, especially in isolated or vulnerable locations. In addition to providing emergency power, backup reciprocating engines are becoming increasingly important for maintaining operational continuity in industries where power reliability is critical.

The growing volatility of electricity supply in developing economies and the increasing need for energy in disaster-prone regions are expected to fuel the adoption of backup power systems. Furthermore, the integration of Internet of Things (IoT)-enabled engines is enhancing system intelligence and facilitating predictive maintenance, thus improving the performance of critical and remote applications. Stricter emission regulations and the rising demand for standby power in industrial sectors also contribute to market expansion. The evolving regulatory landscape, including tariffs on imported parts, may impact international trade and increase production costs for backup power-generating engines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $9.5 Billion |

| CAGR | 3.1% |

The gas-fired backup reciprocating power generating engine market is projected to grow at a robust CAGR of 4.5% through 2034, driven by stricter environmental regulations and the increasing affordability of natural gas, making it a viable and sustainable alternative to traditional power generation methods. These engines offer a compelling advantage due to their higher efficiency and lower emissions compared to conventional fossil-fuel-powered generators, making them a preferred choice for industries looking to reduce their carbon footprint while maintaining a reliable power supply.

In addition to this, Combined Heat and Power (CHP) systems are expected to see notable growth, with an anticipated CAGR of 4.5% through 2034. The rising demand for energy-efficient solutions and the push for businesses to lower their fuel consumption and operating costs are key factors contributing to this trend. CHP systems are particularly valued for their ability to simultaneously generate electricity and capture waste heat for use in heating, thereby improving energy efficiency and reducing overall operational costs.

United States Backup Reciprocating Power Generating Engine Market was valued at USD 3.1 billion in 2024, reflecting the increasing demand for dependable electricity. This surge is largely attributed to the modernization of the nation's aging grid infrastructure and the need for backup systems to ensure continuous power during outages. Additionally, the growing adoption of energy-efficient technologies across various sectors, coupled with the expansion of commercial and industrial activities, is expected to drive further growth in the market.

Key players in the Global Backup Reciprocating Power Generating Engine Market are focusing on product innovation and market expansion to strengthen their positions. Companies like Rolls-Royce, MAN Energy Solutions, and Wartsila are increasingly investing in research and development to improve engine performance and fuel efficiency. Strategic partnerships and acquisitions are also being utilized to enter new regional markets and enhance product offerings. Additionally, firms are focusing on sustainability by developing engines that comply with stringent emission standards. These strategies are being adopted to meet the growing demand for reliable, environmentally friendly power solutions across various industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel Type, 2021 - 2034 (USD Million, MW & Units)

- 5.1 Key trends

- 5.2 Gas-fired

- 5.3 Diesel-fired

- 5.4 Dual fuel

- 5.5 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2021 - 2034 (USD Million, MW & Units)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, MW & Units)

- 7.1 Key trends

- 7.2 Industrial

- 7.3 CHP

- 7.4 Energy & utility

- 7.5 Landfill & biogas

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, MW & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Denmark

- 8.3.9 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Thailand

- 8.4.7 Singapore

- 8.4.8 Indonesia

- 8.4.9 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Qatar

- 8.5.4 Oman

- 8.5.5 Kuwait

- 8.5.6 Iran

- 8.5.7 Egypt

- 8.5.8 Turkey

- 8.5.9 Jordan

- 8.5.10 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 AB Volvo Penta

- 9.2 Atlas Copco

- 9.3 Caterpillar

- 9.4 Clarke Energy

- 9.5 GE Vernova

- 9.6 HIMOINSA

- 9.7 Kirloskar

- 9.8 MAN Energy Solutions

- 9.9 Mitsubishi Heavy Industries

- 9.10 Motorenfabrik Hatz

- 9.11 Rehlko

- 9.12 Rolls-Royce

- 9.13 Scania

- 9.14 Wartsilä

- 9.15 Yamaha Motor

- 9.16 Yuchai International

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 115 Pages

- 納期

- 2~3営業日