|

市場調査レポート

商品コード

1667129

原動機レシプロ発電エンジン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Prime Power Reciprocating Power Generating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 原動機レシプロ発電エンジン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年12月03日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

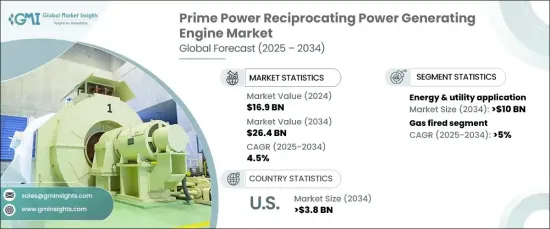

原動機レシプロ発電エンジンの世界市場規模は、2024年に169億米ドルとなり、2025年から2034年にかけてCAGR 4.5%で成長すると予測されています。

この成長の主な要因は、産業、ヘルスケア、データセンター、非電化拠点など、さまざまな分野で信頼性の高い一定電力に対するニーズが高まっていることです。これらのエンジンは、その効率性、寿命、大きな電力負荷を処理する能力が高く評価され、発電用途で好まれています。

エネルギーおよび公益事業部門が市場を独占し、2034年までに100億米ドルの売上が見込まれています。これらのエンジンは、シングルサイクルで50%、コンバインドサイクルでは最大70%という驚異的な電気効率を達成できるため、原動機として支持を集めています。インフラへの投資が拡大し、政府主導の電動化構想が拡大し続ける中、これらのエンジンに対する需要は増加し、市場の拡大をさらに後押しすることになると思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 169億米ドル |

| 予測金額 | 264億米ドル |

| CAGR | 4.5% |

市場のガス動力セグメントは、2034年までCAGR 5%で成長すると予測されます。これは、エンジン性能と効率を向上させる技術の進歩に加え、厳しい環境規制を遵守する必要性が高まっているためです。再生可能エネルギー源を重視する世界の高まりも、ガス焚きエンジンの需要促進に大きな役割を果たしています。ガス焚きエンジンは、高い変換効率、最適化された要素、効率的な燃焼、低メンテナンスといった利点を提供します。これらの特性は、様々な産業でこれらのエンジンが広く採用される一因となっています。

米国の原動機レシプロ発電エンジン市場は、2034年までに38億米ドルを創出すると予測されています。この成長の要因には、無停電電力へのニーズの高まりや、異常気象による電力途絶の頻度の増加があります。電力需要の増加と相まって既存の電力網に負担がかかっていることから、信頼性の高いバックアップ電力ソリューションを提供するこれらのエンジンの重要性が浮き彫りになっています。さらに、データセンターなどの重要施設におけるバックアップ電源の需要の高まりが、これらのエンジンの採用を促進しています。信頼できる電源の必要性に対する意識の高まりが、市場の成長見通しをさらに後押ししています。

産業界と政府がエネルギー効率と持続可能性の確保に重点を置く中、原動機レシプロ発電エンジンの需要は上昇基調を続けると予想され、増大する世界のエネルギー需要を満たす上で重要な役割を果たしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:燃料タイプ別、2021年~2034年

- 主要動向

- ガス焚き

- ディーゼル火力

- デュアル燃料

- その他

第6章 市場規模・予測:定格出力別、2021年~2034年

- 主要動向

- 0.5 MW-1 MW

- 1 MW-2 MW 以上

- 2 MW-3.5 MW 以上

- 3.5MW-5MW 以上

- 5MW-7.5MW 以上

- 7.5MW 以上

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 産業用

- CHP

- エネルギー・公益事業

- 埋立地・バイオガス

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- スペイン

- オランダ

- デンマーク

- ノルウェー

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- タイ

- シンガポール

- インドネシア

- マレーシア

- 中東・アフリカ

- UAE

- サウジアラビア

- カタール

- オマーン

- クウェート

- イラン

- エジプト

- トルコ

- ヨルダン

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- ペルー

第9章 企業プロファイル

- AB Volvo Penta

- Caterpillar

- Cummins

- Deere &Company

- DEUTZ AG

- Kirloskar

- KUBOTA Corporation

- MITSUBISHI HEAVY INDUSTRIES

- Perkins Engines Company

- Rehlko

- Rolls-Royce

- Sulzer

- Wartsila

- YANMAR HOLDINGS

- Yuchai International

The Global Prime Power Reciprocating Power Generating Engines Market was valued at USD 16.9 billion in 2024 and is projected to grow at a CAGR of 4.5% during 2025-2034. This growth is primarily driven by the increasing need for reliable, constant power across several sectors, including industries, healthcare, data centers, and off-grid locations. These engines are highly regarded for their efficiency, longevity, and capacity to handle substantial power loads, making them a favored choice in power generation applications.

The energy and utility sector is expected to dominate the market, with revenues generating USD 10 billion by 2034. These engines are gaining traction as prime movers due to their ability to achieve impressive electrical efficiencies-over 50% in a single cycle and up to 70% in combined cycles. As investments in infrastructure grow and government-led electrification initiatives continue to expand, the demand for these engines is set to rise, further supporting the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.9 Billion |

| Forecast Value | $26.4 Billion |

| CAGR | 4.5% |

The gas-powered segment of the market is forecast to grow at a CAGR of 5% through 2034. This is attributed to technological advancements that enhance engine performance and efficiency, as well as the increasing need to adhere to stringent environmental regulations. The growing global emphasis on renewable energy sources has also played a significant role in driving the demand for gas-fired engines, which offer benefits such as high translation, optimized elements, efficient combustion, and low maintenance. These attributes contribute to the broader adoption of these engines across various industries.

U.S. prime power reciprocating power generating engine market is anticipated to generate USD 3.8 billion by 2034. Factors contributing to this growth include the increasing need for uninterrupted power and the growing frequency of power disruptions due to extreme weather events. The strain on existing electrical grids, coupled with the rising electricity demand, has underscored the importance of these engines in providing a reliable backup power solution. Additionally, the growing demand for backup power in critical facilities, such as data centers, is driving the adoption of these engines. Increased awareness of the need for reliable power sources further boosts the market's growth prospects.

As industries and governments focus on ensuring energy efficiency and sustainability, the demand for prime power reciprocating power generating engines is expected to continue its upward trajectory, playing a crucial role in meeting the growing global energy demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel Type, 2021 – 2034 (Units, MW & USD Million)

- 5.1 Key trends

- 5.2 Gas-fired

- 5.3 Diesel-fired

- 5.4 Dual fuel

- 5.5 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2021 – 2034 (Units, MW & USD Million)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (Units, MW & USD Million)

- 7.1 Key trends

- 7.2 Industrial

- 7.3 CHP

- 7.4 Energy & utility

- 7.5 Landfill & biogas

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (Units, MW & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Denmark

- 8.3.9 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Thailand

- 8.4.7 Singapore

- 8.4.8 Indonesia

- 8.4.9 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Qatar

- 8.5.4 Oman

- 8.5.5 Kuwait

- 8.5.6 Iran

- 8.5.7 Egypt

- 8.5.8 Turkey

- 8.5.9 Jordan

- 8.5.10 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 AB Volvo Penta

- 9.2 Caterpillar

- 9.3 Cummins

- 9.4 Deere & Company

- 9.5 DEUTZ AG

- 9.6 Kirloskar

- 9.7 KUBOTA Corporation

- 9.8 MITSUBISHI HEAVY INDUSTRIES

- 9.9 Perkins Engines Company

- 9.10 Rehlko

- 9.11 Rolls-Royce

- 9.12 Sulzer

- 9.13 Wartsila

- 9.14 YANMAR HOLDINGS

- 9.15 Yuchai International