ディーゼルパワーエンジン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Diesel Power Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 200 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687308

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

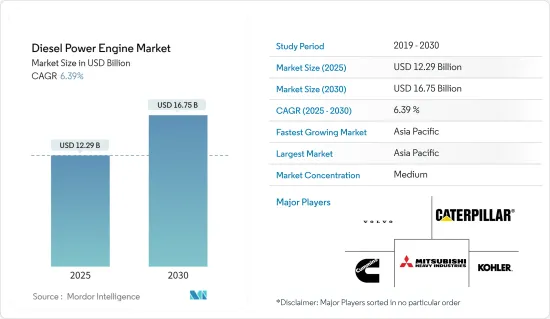

ディーゼルパワーエンジン市場規模は2025年に122億9,000万米ドルと予測され、予測期間(2025-2030年)のCAGRは6.39%で、2030年には167億5,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、産業部門からの需要の増加や停電の増加といった要因がディーゼル発電機の需要を増加させ、ディーゼルパワーエンジン市場を牽引しています。

- 一方、天然ガスが豊富で環境に優しいことから、様々なエンドユーザー産業でディーゼルエンジンの代替として天然ガスエンジンへの移行が進んでおり、予測期間中はディーゼルエンジン市場の成長を抑制すると予想されます。

- とはいえ、ハイブリッド・パワー・ディーゼル発電機の人気が高まっていることから、ディーゼルパワーエンジン市場のプレーヤーにとっては、今後数年間で計り知れない機会がもたらされることになります。

- アジア太平洋は最大かつ最も急成長している市場になると予想され、需要の大部分はインドや中国のような国々からもたらされます。

ディーゼルパワーエンジン市場動向

市場を独占する産業用セグメント

- *ディーゼル発電は、産業部門にとって最も適切なスタンバイ電源です。一般的に、産業部門は事業運営のために多くの電力を消費します。ディーゼルパワーエンジンは信頼性が高く、電力供給の質を高める。

- *電力需要は世界中で高まっています。急速な産業拡大と商業インフラ開発により、ディーゼルパワーエンジンの利用が増加しています。ディーゼルエンジンから発電される電力に大きく依存している重要な産業は、建設部門、製造業、医療、石油・ガス、通信、データセンターなどです。

- ディーゼル発電機には、電流を監視する高度な技術が搭載されており、電力に歪みや障害が発生すると自動的に始動し、電力が回復するとスイッチオフ・モードに戻ります。

- ディーゼルエンジンは揮発率が低いため、鉱業分野では最適な選択肢となります。特に鉱業分野では、重作業には完璧な電源とバックアップが必要です。そのため、鉱業は耐久性に優れたディーゼルエンジンに依存しています。ヘルスケア分野では、酸素吸入器、輸液ポンプ、心電図装置、除細動器などの精密機器を患者の治療に使用しています。中断を避けるため、質の高い電力供給が必要です。ディーゼルパワーエンジンは、病院にとって最も信頼できるバックアップ電源であり、中断のない電力を供給することができます。

- 建設分野では、停電が原因でプロジェクトが停滞することがよくあります。停電が続くとプロジェクトの遂行が遅れ、経済的な損失につながります。建設現場の安全性と電力供給を向上させるために、ディーゼルパワーエンジンが必要とされています。

- 製造業における停電は、少量生産につながり、低水準の製品を提供することになります。製造部門で停電が発生すると、一般的にすべての工程に影響が及ぶ。そのため、生産部門はこのような障害を回避するため、最適な電源として機能するディーゼルパワーエンジンに頼っています。

- また、鉄鋼業界では、電力需要や電力停止時のバックアップ電源としてディーゼルパワーエンジンを使用しています。世界鉄鋼協会によると、2022年12月現在、粗鋼生産量では中国が世界首位で、前年比10%減の7,790万トンを生産しました。インド、日本、米国、ロシアは大きく後れを取っています。

- したがって、上記の要因から、予測期間中、ディーゼルパワーエンジン市場は産業部門が支配すると予想されます。

アジア太平洋が市場を独占する

- 平均エネルギー消費率とGDP成長率の大幅な増加とともに、アジア太平洋地域におけるインフラ開拓と電力需要の増加が、ディーゼルパワーエンジン市場を促進すると予想されます。

- 中国は、インフラ・プロジェクトの増加、電力需給ギャップの拡大、全国的な製造施設の拡大、商業オフィスの増加により、アジア太平洋のディーゼル発電機市場をリードしています。

- 世界最大級の中国の建設業界は、過去数十年にわたって著しい成長を遂げてきました。中国の急速な工業化は、住宅、商業、インフラ建設を含む建設活動の急増につながりました。新たなプロジェクトが推進されるにつれ、中国経済はCOVID-19パンデミックの影響から回復し始めています。

- 2023年4月、中国政府は、地域経済がパンデミックから回復するのを支援するため、大規模建設およびインフラ・プロジェクトに対する支出を前年比1兆8,000億米ドル増額すると発表しました。建設活動の拡大にはディーゼルエンジンを搭載した機械が必要であり、これが市場の成長を促進すると予想されます。

- インド政府は、開放的なFDI基準、スマートシティミッション、インフラ部門への多額の予算配分など、重点的な政策を通じてインフラと建設サービスの開発に注力しています。2023年1月、政府と建設産業開発評議会(CIDC)は、国内に21のグリーンフィールド空港の開発を承認しました。建設部門の成長により、バックアップ用のディーゼル発電機が必要となり、市場開拓の道が開かれることになります。

- スマートシティミッションの下、2022年11月現在、PMAY-Uミッションの下で1,200万戸以上の住宅が認可され、そのうち640万戸以上が完成しました。残りは様々な建設・建設段階にあります。2024年現在、AMRUT 2.0ミッションの下、水域の若返り、上水道、下水道、公園・緑地開発など、8億5,512万米ドル相当の1億7,742件のプロジェクトが進行中です。インドの多くの住宅には、停電時に電気を供給するためのディーゼル発電機(DG)が設置されています。そのため、予測期間中にディーゼルエンジンの需要が増加することが予想されます。

- さらに、急成長する製造業によるエネルギー需要の増加は、アジア太平洋地域の発電機事業に大きな推進力を与えると予想されます。その結果、予測期間中、アジア太平洋地域が世界のディーゼルパワーエンジン市場で最も速い成長を遂げると予想されます。

ディーゼルパワーエンジン産業の概要

ディーゼルパワーエンジン市場は半断片化されています。この市場の主要企業(順不同)には、Caterpillar Inc.、Cummins Inc.、Kohler Co.、Volvo AB、三菱重工業株式会社などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 産業部門からの需要増加

- 停電の増加によるディーゼル発電機需要の増加

- 抑制要因

- よりクリーンなエネルギー資源へのシフトの増加

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- エンドユーザー別

- 産業

- 商業

- 住宅

- 用途別

- スタンバイ

- プライム

- ピークカット

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- 英国

- フランス

- ドイツ

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- ASEAN諸国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- ナイジェリア

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Caterpillar Inc.

- Cummins Inc.

- Kohler Co

- Volvo AB

- Mitsubishi Heavy Industries Ltd

- Wartsila Oyj Abp

- Hyundai Heavy Industries Co. Ltd

- Man SE

- Rolls-Royce Holding PLC

- YANMAR HOLDINGS Co. Ltd

- Market Ranking/Share(%)Analysis

第7章 市場機会と今後の動向

- ハイブリッド式ディーゼル発電機の人気の高まり

目次

Product Code: 61049

The Diesel Power Engine Market size is estimated at USD 12.29 billion in 2025, and is expected to reach USD 16.75 billion by 2030, at a CAGR of 6.39% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, factors such as the increasing demand from the industrial sector and rising power outages have increased the demand for diesel generators, thereby driving the diesel power engine market.

- On the other hand, the abundance of natural gas, coupled with its environmental soundness, has led to an increasing shift toward natural gas engines as an alternative to diesel engines in various end-user industries and is expected to restrain the growth of the diesel engine market during the forecast period.

- Nevertheless, the increasing popularity of hybrid power diesel generators presents immense opportunities for the diesel power engine market players in the coming years.

- Asia-Pacific is expected to be the largest and fastest-growing market, with the majority of the demand coming from countries like India and China.

Diesel Power Engine Market Trends

The Industrial Segment to Dominate the Market

- * Diesel power generation is the most appropriate standby source for the industrial sector. Generally, the industrial sector consumes more power for its business operations. A diesel power engine offers better reliability and enhances the quality of the power supply.

- * The demand for electricity is growing worldwide. Rapid industrial expansions and commercial infrastructure development are increasing the utilization of diesel power engines. Significant industries that rely heavily on the power generated from diesel engines are the construction sector, manufacturing, health care, oil and gas, telecommunication and data centers, etc.

- Diesel generators are equipped with advanced technologies for monitoring electric current, which help automatically start when there are power distortions and failures and revert to switch-off mode when the power comes back.

- The diesel engine's low volatility rate makes it the finest option in mining fields. Especially in mining fields, heavy-duty activities need a perfect power source and backup. Hence, mining industries rely on diesel-powered engines for better durability. The healthcare segment uses sensitive equipment such as oxygen ventilators, infusion pumps, ECG machines, and defibrillators to treat patients. There is a need for a quality power supply to avoid interruptions. Diesel power engines are hospitals' most reliable backup power sources for uninterrupted power.

- In the construction sector, projects often stall due to power failures. Constant power interruptions result in delayed project execution, which leads to financial loss. There is a need for a diesel power engine to ensure safety and better power supply on construction sites.

- Disruptions of power in the manufacturing industry lead to low-volume production and result in the offering of low-standard products. When a blackout occurs in manufacturing divisions, it generally affects all the processes. Hence, the production units rely on the diesel power engine to avoid such failures, which acts as the best power source.

- The iron and steel industry also uses diesel power engines as backup power in case of power requirements or power shutdown. According to the World Steel Association, as of December 2022, China was the world leader in crude steel production, with 77.9 million metric tonnes produced, a 10% decrease from the previous year. India, Japan, the United States, and Russia trailed far behind.

- Therefore, based on the abovementioned factors, the industrial segment is expected to dominate the diesel power engine market during the forecast period.

Asia-Pacific to Dominate the Market

- The increasing infrastructural developments and electricity demand in Asia-Pacific, with the huge increase in average energy consumption rate and GDP growth rate, are expected to promulgate the diesel power engine market.

- China is the leading diesel generator market in Asia-Pacific owing to increasing infrastructure projects, widening power demand-supply gap, expanding manufacturing facilities across the nation, and rising commercial office spaces.

- The construction industry in China, one of the largest in the world, has experienced significant growth over the last few decades. Rapid industrialization in China has led to a surge in construction activities, including residential, commercial, and infrastructure construction. The Chinese economy is beginning to recover from the effects of the COVID-19 pandemic as new projects are pushed forward.

- In April 2023, the Chinese government announced that it was set to increase its spending on large construction and infrastructure projects by USD 1.8 trillion Y-o-Y to help regional economies recover from the pandemic. The growing construction activities require machinery fitted with diesel engines; this is expected to promote the growth of the market.

- The Indian government has been focusing on developing infrastructure and construction services through focused policies such as open FDI norms, smart city missions, and large budget allocation to the infrastructure sector. In January 2023, the government and the Construction Industry Development Council (CIDC) approved the development of 21 greenfield airports in the country. The growth in the construction sector will, in turn, need diesel generators to power backup, which will create avenues for the development of the market.

- Under the Smart City Mission, as of November 2022, more than 12.0 million houses were sanctioned under the PMAY-U Mission, out of which more than 6.4 million were completed. The rest are in various stages of construction/grounding. As of 2024, 1174 projects worth USD 855.12 million of Water Body Rejuvenation, Water Supply, Sewage & Sewage Management, and Parks & Green Space Development are ongoing under the AMRUT 2.0 mission. Many of the residential societies in India are equipped with diesel generator (DG) sets to supply electricity during power outages. Thus, such commitments are expected to increase the demand for diesel engines during the forecast period.

- Moreover, the growing energy demands of the burgeoning manufacturing industry are expected to provide a huge impetus to the generator business in Asia-Pacific. As a result, Asia-Pacific is expected to witness the fastest growth in the global diesel power engine market during the forecast period.

Diesel Power Engine Industry Overview

The diesel power engine market is semi fragmented. Some of the key players in this market (in no particular order) include Caterpillar Inc., Cummins Inc., Kohler Co., Volvo AB, and Mitsubishi Heavy Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand From Industrial Sector

- 4.5.1.2 Rising Power Outages To Increase The Demand For Diesel Generators

- 4.5.2 Restraints

- 4.5.2.1 Increasing Shift Toward Cleaner Energy Resources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Industrial

- 5.1.2 Commercial

- 5.1.3 Residential

- 5.2 By Application

- 5.2.1 Standby

- 5.2.2 Prime

- 5.2.3 Peak Shaving

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 ASEAN Countries

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Cummins Inc.

- 6.3.3 Kohler Co

- 6.3.4 Volvo AB

- 6.3.5 Mitsubishi Heavy Industries Ltd

- 6.3.6 Wartsila Oyj Abp

- 6.3.7 Hyundai Heavy Industries Co. Ltd

- 6.3.8 Man SE

- 6.3.9 Rolls-Royce Holding PLC

- 6.3.10 YANMAR HOLDINGS Co. Ltd

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Popularity Of Hybrid Power Diesel Generators

ディーゼルパワーエンジン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 200 Pages

- 納期

- 2~3営業日