食品用乳化剤の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Food Emulsifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750581

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

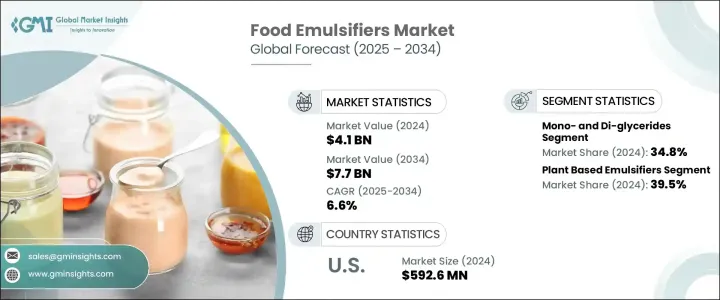

食品用乳化剤の世界市場は、2024年には41億米ドルと評価され、コンビニエンス食品、植物由来原料、クリーンラベル製品への需要の増加に牽引され、CAGR6.6%で成長し、2034年までには77億米ドルに達すると推定されます。

乳化剤は、食品の構造、安定性、保存性を向上させる上で重要な役割を果たしています。乳化剤は、ベーカリー、乳製品、冷菓、飲料、加工肉、調理済み食品、幼児栄養など、さまざまな食品分野で使用されています。クリーンラベルやビーガンフレンドリーな選択肢へのシフトが進む中、レシチン、ヒマワリ、大豆などの天然・植物由来の乳化剤が人気を集めています。さらに、モノグリセリドとジグリセリドの需要は、その多用途性、費用対効果、機能性食品とコンビニエンスフードにおける幅広い用途により、引き続き優位を占めています。

地域別の成長という点では、食生活の選好の変化と都市化の進展により、アジア太平洋市場が急速に拡大しています。欧州と北米は成熟市場ですが、天然で持続可能なクリーンラベル原料に対する強い需要を維持し続けています。食品の安全性とラベルの透明性に対する規制当局の支援の高まりも、乳化剤ブレンドの技術革新を促進し、近代的な食品製造プロセスにおける乳化剤の存在感を高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 41億米ドル |

| 予測金額 | 77億米ドル |

| CAGR | 6.6% |

モノグリセリド・ジグリセリド分野は34.8%のシェアを占め、2034年までにCAGR6.4%で成長すると予測されています。これらの乳化剤は、その汎用性、費用対効果、ベーカリー、乳製品、菓子類、加工食品など複数の分野にわたる幅広い用途で高く評価されています。安定剤、乳化剤、テクスチャライザーとして機能するその能力は、長い保存期間と一貫性と相まって、食品業界で最も使用される乳化剤のひとつとしての地位を確固たるものにしています。このように広く使用されていることと、多機能性が相まって、モノグリセリド・ジグリセリドは食品製造において支配的な選択肢であり続けています。

植物由来の乳化剤セグメントは2024年に39.5%のシェアを占め、2034年までCAGR6.2%で成長すると予想されます。これは、より持続可能で健康志向のライフスタイルに合致した天然植物由来成分への消費者の選好の顕著なシフトが原動力となっています。環境に優しくクリーンラベルの製品を求める消費者が増えるにつれ、大豆、ヒマワリ、カノーラ由来の乳化剤の需要が伸びています。これらの植物性乳化剤は、栄養価の高さ、クリーンラベル、持続可能な調達により人気を集めており、これらはすべて、より健康的で環境に配慮した食品を求める消費者の需要の高まりと一致しています。

米国の食品用乳化剤強力な食品加工産業とコンビニエンスフードの高い消費により、2024年の市場規模は5億9,260万米ドルとなりました。同国の堅調なベーカリー、乳製品、冷菓部門が乳化剤の需要をさらに支えています。さらに、米国の消費者の間で健康とウェルネスの傾向が高まっていることが、植物由来や天然の代替品など、より革新的な乳化剤の必要性を高めています。米国の確立されたサプライチェーンとマーケティングシステムは、国内外からの原料調達における競争優位性に貢献しています。

Cargill, Inc.、Corbion N.V.、Archer Daniels Midland Company(ADM)、Kerry Group plc、Croda International Plcなど、食品用乳化剤世界市場の主要企業は、製品ポートフォリオの多様化と市場でのプレゼンス拡大に注力しています。これらの企業は、持続可能な製品に対する消費者の需要の高まりに対応した、よりクリーンな植物由来の乳化剤を開発するため、研究開発に多額の投資を行っています。また、効率向上とコスト削減のため、生産プロセスの強化も進めています。パートナーシップ、合併、買収は、これらの企業が市場での足跡を拡大し、世界の食品乳化剤セクターにおける競争力を高めるために用いる主要な戦略です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

注:上記の貿易統計は主要国についてのみ提供されます

- 消費者の動向と選好

- クリーンラベル運動

- 乳化剤に対する消費者の認識

- 天然と合成の好み

- 製品処方への影響

- 健康とウェルネスの動向

- 栄養に関する懸念

- アレルギーに関する考慮事項

- 食事制限の影響

- 持続可能性と倫理的配慮

- 環境影響認識

- 持続可能な調達の優先

- パッケージングに関する考慮事項

- 植物由来のビーガン動向

- 植物由来乳化剤の需要

- ビーガン認証の影響

- 透明性とトレーサビリティの要求

- 地域による消費者の選好の違い

- クリーンラベル運動

- 消費者行動分析

- 購入決定要因

- 価格感度分析

- ブランドロイヤルティパターン

- ソーシャルメディアとデジタルが消費者の認識に与える影響

- サプライチェーンと原材料分析

- 原材料調達分析

- 主要原材料

- 調達地域

- 調達における持続可能性

- 生産プロセス分析

- 製造技術

- 品質管理措置

- コスト構造分析

- 流通チャネル分析

- 直接チャネルと間接チャネル

- eコマースの影響

- 流通の課題

- サプライチェーンの課題

- 原材料価格の変動

- サプライチェーンの混乱

- 物流の課題

- サプライチェーン最適化戦略

- 持続可能なサプライチェーンの実践

- サプライチェーンにおける技術統合

- 原材料調達分析

- 価格分析とコスト構造

- 価格分析:製品タイプ別

- 価格動向分析、2021年~2025年

- 価格予測、2025年~2034年

- 価格に影響を与える要因

- 原材料費

- 生産コスト

- 規制遵守コスト

- 市場競争

- 地域による価格差

- 主要企業の価格戦略

- コスト構造分析

- 原材料費

- 製造コスト

- 流通コスト

- マーケティング・販売コスト

- 収益性分析:製品セグメント別

- 技術の進歩と革新

- 最近の技術開発

- 乳化剤製造における新技術

- 酵素修飾

- マイクロカプセル化

- ナノテクノロジーの応用

- クリーンラベルのイノベーション

- 天然乳化剤の代替品

- 酵素ベースのソリューション

- 植物由来のイノベーション

- 持続可能な生産技術

- 機能改善

- 安定性の向上

- テクスチャ特性の改善

- 保存期間延長ソリューション

- 生産と品質管理におけるデジタル技術

- 特許分析と研究開発動向

- 将来の技術ロードマップ

- 持続可能性と環境への影響

- 乳化剤の環境フットプリント

- カーボンフットプリント分析

- 水使用量の評価

- 廃棄物の発生と管理

- 持続可能な調達慣行

- パーム油の持続可能性問題

- 大豆調達の課題

- 代替の持続可能な資源

- 生分解性と生態毒性評価

- 循環型経済のアプローチ

- 業界の持続可能性への取り組み

- 持続可能性に対する規制圧力

- 持続可能な製品に対する消費者の需要

- 持続可能な慣行の費用便益分析

- 乳化剤の環境フットプリント

- 市場の課題と機会

- 主な市場の課題

- 健康への懸念と否定的な認識

- 規制上のハードル

- 原材料価格の変動

- クリーンラベル処方の課題

- 市場機会

- 植物由来乳化剤の開発

- 新興市場の拡大

- 機能性食品の応用

- 持続可能な乳化剤ソリューション

- マクロ経済要因の影響

- 技術的機会の評価

- 戦略的機会マッピング

- 主な市場の課題

- 将来の市場見通しと予測

- 市場予測:製品タイプ別、2025年~2030年

- 市場予測:用途別、2025年~2030年

- 市場予測:地域別、2025年~2030年

- 新興市場の動向

- 将来の促進要因

- 市場進化シナリオ

- 楽観的シナリオ

- 現実的シナリオ

- 悲観的シナリオ

- 投資機会の評価

- 将来の競合情勢予測

- 戦略的提言

- 市場参入戦略

- 製品開発の推奨事項

- 地域拡大の機会

- 競争的ポジショニング戦略

- 持続可能性の実装ロードマップ

- デジタル変革戦略

- 規制コンプライアンス戦略

- マーケティングとブランディングの推奨事項

- リスク軽減戦略

- 投資優先順位付けフレームワーク

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 成長促進要因

- 飲料業界の成長が製品需要を押し上げる可能性

- 加工食品の消費量の増加が業界の成長を促進

- 乳製品の消費量の増加は食品乳化剤業界の成長を促進する可能性が高め

- 業界の潜在的リスク・課題

- 高まる健康への懸念

- 製品のクリーンラベル要件

- 成長促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場規模・予測:タイプ別、2021年~2034年

- 主要動向

- モノグリセリド・ジグリセリド

- レシチン

- ソルビタンエステル

- ステアロイル乳酸

- ポリグリセロールエステル

- ポリソルベート

- その他(DATEM、CSLなど)

第6章 市場規模・予測:ソース別、2021年~2034年

- 主要動向

- 植物由来乳化剤

- 大豆由来

- ヒマワリ由来

- パーム由来

- その他の植物源

- 動物由来乳化剤

- 合成乳化剤

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- パン・菓子類

- パン・ロールパン

- ケーキ・ペストリー

- ビスケット・クッキー

- チョコレート・菓子類

- 乳製品・冷凍デザート

- アイスクリーム・冷凍デザート

- 牛乳・クリーム製品

- チーズ製品

- ヨーグルト・発酵乳製品

- 加工肉・魚介類

- ソーセージ・加工肉

- シーフード製品

- インスタント食品・調理済み食品

- スープ・ソース

- ドレッシング・マヨネーズ

- すぐに食べられる食事

- 飲料

- 炭酸飲料

- フルーツジュース・ネクター

- アルコール飲料

- 植物由来飲料

- 乳児の栄養と離乳食

- 乳児用調製粉乳

- ベビーフード

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Archer Daniels Midland Company(ADM)

- Cargill、Inc.

- Croda International Plc

- Kerry Group plc

- Corbion N.V.

- Ingredion Incorporated

- Lasenor Emul、S.L.

- Palsgaard A/S

- Lonza

- Riken Vitamin

目次

The Global Food Emulsifiers Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 7.7 billion by 2034, driven by the increasing demand for convenience foods, plant-based ingredients, and clean-label products. Emulsifiers play a vital role in improving the structure, stability, and shelf life of food products. They are used across various food sectors such as bakery, dairy, frozen desserts, beverages, processed meats, ready-to-eat meals, and infant nutrition. With an increasing shift toward clean label and vegan-friendly options, natural and plant-based emulsifiers such as lecithin, sunflower, and soy are gaining traction. Moreover, the demand for mono- and diglycerides continues to dominate due to their versatility, cost-effectiveness, and wide application in functional and convenience foods.

In terms of regional growth, the Asia Pacific market is expanding rapidly due to changing dietary preferences and rising urbanization. Europe and North America, while mature markets, continue to maintain strong demand for natural, sustainable, and clean-label ingredients. The growing regulatory support for food safety and label transparency is also driving the innovation of emulsifier blends, strengthening their presence in modern food production processes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $7.7 Billion |

| CAGR | 6.6% |

The mono- and diglycerides segment holds 34.8% share and is forecasted to grow at a CAGR of 6.4% by 2034. These emulsifiers are highly regarded for their versatility, cost-effectiveness, and wide application across multiple sectors, including bakery, dairy, confectionery, and processed foods. Their ability to act as stabilizers, emulsifiers, and texturizers, combined with their long shelf life and consistency, has cemented their position as one of the most used emulsifiers in the food industry. This widespread usage, coupled with their multifunctionality, ensures that mono and diglycerides remain a dominant choice in food manufacturing.

The plant-based emulsifiers segment held 39.5% share in 2024 and is expected to grow at a CAGR of 6.2% through 2034, driven by a noticeable shift in consumer preferences toward natural, plant-derived ingredients that align with a more sustainable and health-conscious lifestyle. As more consumers seek eco-friendly and clean-label products, the demand for emulsifiers derived from soy, sunflower, and canola is growing. These plant-based emulsifiers are gaining popularity due to their nutritional benefits, clean labeling, and sustainable sourcing, all of which align with the rising consumer demand for healthier and environmentally responsible food options.

U.S. Food Emulsifiers Market was valued at USD 592.6 million in 2024 due to its strong food processing industry and high consumption of convenience foods. The country's robust bakery, dairy, and frozen dessert sectors further support the demand for emulsifiers. Additionally, the growing health and wellness trends among U.S. consumers are driving the need for more innovative emulsifiers, including plant-based and natural alternatives. The well-established supply chains and marketing systems in the U.S. contribute to its competitive advantage in obtaining raw materials from both local and international sources.

Leading players in the Global Food Emulsifiers Market, such as Cargill, Inc., Corbion N.V., Archer Daniels Midland Company (ADM), Kerry Group plc, and Croda International Plc, are focusing on diversifying their product portfolios and expanding their market presence. These companies are investing heavily in research and development to create cleaner, plant-based emulsifiers that meet the growing consumer demand for sustainable products. They are also enhancing their production processes to improve efficiency and reduce costs. Partnerships, mergers, and acquisitions are key strategies used by these companies to expand their market footprint and improve their competitive positioning in the global food emulsifier sector.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021 - 2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021 - 2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only.

- 3.4 Consumer trends and preferences

- 3.4.1 Clean label movement

- 3.4.1.1 Consumer perception of emulsifiers

- 3.4.1.2 Natural vs. synthetic preferences

- 3.4.1.3 Impact on product formulation

- 3.4.2 Health and wellness trends

- 3.4.2.1 Nutritional concerns

- 3.4.2.2 Allergen considerations

- 3.4.2.3 Dietary restrictions impact

- 3.4.3 Sustainability and ethical considerations

- 3.4.3.1 Environmental impact awareness

- 3.4.3.2 Sustainable sourcing preferences

- 3.4.3.3 Packaging considerations

- 3.4.4 Plant-based vegan trends

- 3.4.4.1 Demand for plant-derived emulsifiers

- 3.4.4.2 Vegan certification impact

- 3.4.5 Transparency and traceability demands

- 3.4.6 Regional consumer preference variations

- 3.4.1 Clean label movement

- 3.5 Consumer behavior analysis

- 3.5.1 Purchase decision factors

- 3.5.2 Price sensitivity analysis

- 3.5.3 Brand loyalty patterns

- 3.6 Social media and digital influence on consumer perception

- 3.7 Supply chain and raw material analysis

- 3.7.1 Raw material sourcing analysis

- 3.7.1.1 Key raw materials

- 3.7.1.2 Sourcing regions

- 3.7.1.3 Sustainability in sourcing

- 3.7.2 Production process analysis

- 3.7.2.1 Manufacturing technologies

- 3.7.2.2 Quality control measures

- 3.7.2.3 Cost structure analysis

- 3.7.3 Distribution channel analysis

- 3.7.3.1 Direct vs. indirect channels

- 3.7.3.2 E-commerce impact

- 3.7.3.3 Distribution challenges

- 3.7.4 Supply chain challenges

- 3.7.4.1 Raw material price volatility

- 3.7.4.2 Supply chain disruptions

- 3.7.4.3 Logistics challenges

- 3.7.5 Supply chain optimization strategies

- 3.7.6 Sustainable supply chain practices

- 3.7.7 Technology integration in supply chain

- 3.7.1 Raw material sourcing analysis

- 3.8 Pricing analysis and cost structure

- 3.8.1 Price point analysis by product type

- 3.8.2 Price trend analysis 2021–2025

- 3.8.3 Price forecast 2025–2034

- 3.8.4 Factors affecting pricing

- 3.8.4.1 Raw material costs

- 3.8.4.2 Production costs

- 3.8.4.3 Regulatory compliance costs

- 3.8.4.4 Market competition

- 3.8.4.5 Regional price variations

- 3.8.4.6 Pricing strategies of key players

- 3.8.4.7 Cost structure analysis

- 3.8.4.8 Raw material costs

- 3.8.4.9 Manufacturing costs

- 3.8.4.10 Distribution costs

- 3.8.4.11 Marketing and sales costs

- 3.8.5 Profitability analysis by product segment

- 3.9 Technological advancements and innovations

- 3.9.1 Recent technological developments

- 3.9.2 Emerging technologies in emulsifier production

- 3.9.2.1 Enzymatic modification

- 3.9.2.2 Microencapsulation

- 3.9.2.3 Nanotechnology applications

- 3.9.3 Clean label innovations

- 3.9.3.1 Natural emulsifier alternatives

- 3.9.3.2 Enzyme-based solutions

- 3.9.3.3 Plant-based innovations

- 3.9.4 Sustainable production technologies

- 3.9.5 Functional improvements

- 3.9.5.1 Enhanced stability

- 3.9.5.2 Improved texture properties

- 3.9.5.3 Extended shelf life solutions

- 3.9.6 Digital technologies in production and quality control

- 3.9.7 Patent analysis and r&d trends

- 3.9.8 Future technology roadmap

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental footprint of emulsifiers

- 3.10.1.1 Carbon footprint analysis

- 3.10.1.2 Water usage assessment

- 3.10.1.3 Waste generation and management

- 3.10.2 Sustainable sourcing practices

- 3.10.2.1 Palm oil sustainability issues

- 3.10.2.2 Soy sourcing challenges

- 3.10.2.3 Alternative sustainable sources

- 3.10.3 Biodegradability and eco-toxicity assessment

- 3.10.4 Circular economy approaches

- 3.10.5 Industry sustainability initiatives

- 3.10.6 Regulatory pressures for sustainability

- 3.10.7 Consumer demand for sustainable products

- 3.10.8 Cost-benefit analysis of sustainable practices

- 3.10.1 Environmental footprint of emulsifiers

- 3.11 Market challenges and opportunities

- 3.11.1 Key market challenges

- 3.11.1.1 Health concerns and negative perception

- 3.11.1.2 Regulatory hurdles

- 3.11.1.3 Raw material price volatility

- 3.11.1.4 Clean label formulation challenges

- 3.11.2 Market opportunities

- 3.11.2.1 Plant-based emulsifier development

- 3.11.2.2 Emerging markets expansion

- 3.11.2.3 Functional food applications

- 3.11.2.4 Sustainable emulsifier solutions

- 3.11.3 Impact of macro-economic factors

- 3.11.4 Technological opportunity assessment

- 3.11.5 Strategic opportunity mapping

- 3.11.1 Key market challenges

- 3.12 Future market outlook and forecast

- 3.12.1 Market forecast by product type 2025–2030

- 3.12.2 Market forecast by application 2025–2030

- 3.12.3 Market forecast by region 2025–2030

- 3.12.4 Emerging market trends

- 3.12.5 Future growth drivers

- 3.12.6 Market evolution scenarios

- 3.12.6.1 Optimistic scenario

- 3.12.6.2 Realistic scenario

- 3.12.6.3 Pessimistic scenario

- 3.12.7 Investment opportunities assessment

- 3.12.8 Future competitive landscape projection

- 3.13 Strategic recommendations

- 3.13.1 Market entry strategies

- 3.13.2 Product development recommendations

- 3.13.3 Regional expansion opportunities

- 3.13.4 Competitive positioning strategies

- 3.13.5 Sustainability implementation roadmap

- 3.13.6 Digital transformation strategies

- 3.13.7 Regulatory compliance strategies

- 3.13.8 Marketing and branding recommendations

- 3.13.9 Risk mitigation strategies

- 3.13.10 Investment prioritization framework

- 3.14 Supplier landscape

- 3.15 Profit margin analysis

- 3.16 Key news & initiatives

- 3.17 Regulatory landscape

- 3.18 Impact forces

- 3.18.1 Growth drivers

- 3.18.1.1 Growing beverage industry may fuel product demand

- 3.18.1.2 Increasing consumption of processed foods will foster industry growth

- 3.18.1.3 Growth in consumption of dairy products is likely to favor food emulsifier industry growth

- 3.18.2 Industry pitfalls & challenges

- 3.18.2.1 Growing health concerns

- 3.18.2.2 Clean label requirements for the product

- 3.18.1 Growth drivers

- 3.19 Growth potential analysis

- 3.20 Porter’s analysis

- 3.21 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Type 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Mono- and Di-glycerides

- 5.3 Lecithin

- 5.4 Sorbitan esters

- 5.5 Stearoyl lactylates

- 5.6 Polyglycerol esters

- 5.7 Polysorbates

- 5.8 Others (DATEM, CSL, etc.)

Chapter 6 Market Size and Forecast, By Source, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Plant-based emulsifiers

- 6.3 Soy-derived

- 6.4 Sunflower-derived

- 6.5 Palm-derived

- 6.6 Other plant sources

- 6.7 Animal-based emulsifiers

- 6.8 Synthetic emulsifiers

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery and confectionery

- 7.2.1 Bread and rolls

- 7.2.2 Cakes and pastries

- 7.2.3 Biscuits and cookies

- 7.2.4 Chocolate and confectionery

- 7.3 Dairy and frozen desserts

- 7.3.1 Ice cream and frozen desserts

- 7.3.2 Milk and cream products

- 7.3.3 Cheese products

- 7.3.4 Yogurt and fermented dairy

- 7.4 Processed meat and seafood

- 7.4.1 Sausages and processed meats

- 7.4.2 Seafood products

- 7.5 Convenience foods and ready meals

- 7.5.1 Soup and sauces

- 7.5.2 Dressings and mayonnaise

- 7.5.3 Ready-to-eat meals

- 7.6 Beverages

- 7.6.1 Carbonated drinks

- 7.6.2 Fruit juices and nectars

- 7.6.3 Alcoholic beverages

- 7.6.4 Plant-based beverage

- 7.7 Infant nutrition and baby food

- 7.7.1 Infant formula

- 7.7.2 Baby food products

- 7.8 Other

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland Company (ADM)

- 9.2 Cargill, Inc.

- 9.3 Croda International Plc

- 9.4 Kerry Group plc

- 9.5 Corbion N.V.

- 9.6 Ingredion Incorporated

- 9.7 Lasenor Emul, S.L.

- 9.8 Palsgaard A/S

- 9.9 Lonza

- 9.10 Riken Vitamin

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日