保存の利く牛乳の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Non-Perishable Milk Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750498

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

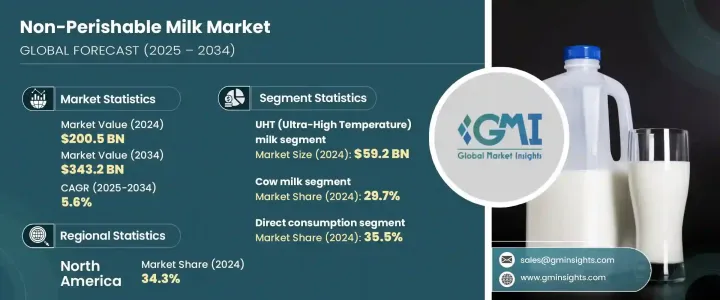

世界の保存の利く牛乳市場は、2024年には2,005億米ドルとなり、CAGR5.6%で成長し、2034年までには3,432億米ドルに達すると推定されています。

この成長の主な要因は、保存期間が長く冷蔵の必要性が少ない乳製品への需要の増加です。保存の利く牛乳は、冷蔵倉庫のない地域での実用的な選択肢から、世界中で主流の選択肢へと進化しています。消費者は、利便性、栄養価、より長い使用期間を提供する選択肢に惹かれています。都市化が進み、食生活の選好が変化する中、業界は多様な消費者層へのリーチを拡大し続けています。

市場は、強化ミルク、オーガニックミルク、無乳糖ミルクへの関心の高まりによって形成されています。こうした選好は、メーカーが変化する健康とライフスタイルの動向に対応するにつれて、製品開発戦略を再構築しています。技術革新、特に加工方法も市場拡大に寄与しています。超高温(UHT)治療や高温短時間(HTST)技術の先進パッケージングと無菌包装の組み合わせにより、保存の利く牛乳の安全性、品質、耐久性が向上しています。これらの要因により、特に冷蔵品へのアクセスが限られている地域において、より広範な流通と消費の拡大が可能になりつつあります。これと並行して、カルシウムの豊富な食生活に対する意識が高まり、牛乳の消費パターンが増加しています。持続可能性と健康に対する消費者の優先順位の進化を反映して、植物由来の代替品も非生鮮セグメントでシェアを拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 2,005億米ドル |

| 予測金額 | 3,432億米ドル |

| CAGR | 5.6% |

市場セグメンテーションでは、UHTミルク、エバミルク、加糖練乳、粉ミルク、その他が含まれます。このうち、UHTミルクは2024年の市場シェア29.5%、592億米ドルでこのカテゴリーをリードしています。UHT牛乳の優位性は、その多用途性と冷蔵なしで長期間新鮮さを保つ能力によるもので、都市部でも農村部でも好まれる選択肢となっています。粉ミルクとエバミルクもまた、特に手頃な価格と長期保存が不可欠な場合によく利用されています。加糖練乳は、健康上の懸念から一部の地域では成長率がやや鈍化しているもの、料理用途ではその関連性を維持しています。

ソース別に評価すると、市場は牛乳、ヤギ乳、水牛乳、植物性乳、その他に区分されます。牛乳は2024年に市場全体の29.7%を占め、2034年までCAGR5.3%で成長すると予想されます。牛乳の継続的な人気は、UHTや粉末の形態で入手できることに支えられており、これらは便利ですぐに使える乳製品の選択肢を求める現在の消費者の需要によく合致しています。ヤギ乳は、乳糖不耐症にやさしい、または消化しやすい代替品を求める消費者の間で着実に支持を集めています。一方、バッファローミルクは脂肪分が高く、地域的選好が強いため、ニッチな魅力を保っています。

保存の利く牛乳の流通チャネルには、スーパーマーケット・ハイパーマーケット、専門店、コンビニエンスストア、オンライン小売、外食店舗、B2B直販、その他が含まれます。スーパーマーケット・ハイパーマーケットが2024年の市場で最大のシェアを占め、31.5%を占めました。スーパーマーケット・ハイパーマーケットの人気は、幅広い品ぞろえの商品を一カ所で提供できることから、日常的に利用する消費者に選ばれていることに起因しています。専門店は、特に健康志向や植物由来のミルクなど、プレミアムな商品を提供することでますます支持されるようになっています。コンビニエンスストアは、シングルサーブやオン・ザ・ゴー形式の需要を満たす上で重要な役割を果たしています。オンライン小売は、戸口配送の利便性とeコマースプラットフォームの拡大により、急速な成長を遂げています。外食チャネルは、安定供給と保存のしやすさから引き続きUHTミルクと粉ミルクに依存しています。企業への直接販売は、特に施設や商業部門で引き続き堅調です。その他の流通方法としては、自動販売機や輸出に特化したチャネルがあり、これらのチャネルはブランドが未開拓の市場を開拓するのに役立っています。

地域別では、北米が2024年の保存の利く牛乳市場で最大のシェアを占め、総売上の34.3%を占めました。この地域市場では、消費者のライフスタイルの進化と保存可能な栄養オプションへの関心の高まりにより、UHT牛乳やその他の長期保存可能な乳製品の採用が増加しています。欧州は、その利便性とコールドチェーンへの依存度の低さから、UHTミルクへの選好が強く、これに追随しています。

Lactalis International、Nestle S.A.、Fonterra Co-operative Group Limited、Danone S.A.、Arla Foodsなどの大手業界企業が市場成長の牽引役となっています。彼らの影響力は、技術革新、加工技術、世界の流通能力において特に顕著です。これらの企業は一貫して製品開発に投資し、保存の利く牛乳製品に対する世界の需要の高まりに対応するため、そのプレゼンスを拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 製造業者

- 販売代理店

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制の枠組みと基準

- 食品安全規制

- ラベル要件

- 品質基準

- 輸出入規制

- オーガニック・クリーンラベル認証

- 影響要因

- 成長促進要因

- 都市化とライフスタイルの進化

- 加工と包装における技術の進歩

- 小売業の拡大と政府の支援

- 業界の潜在的リスク・課題

- サプライチェーンの混乱

- 経済の不確実性

- 市場機会

- 成長促進要因

- 製品概要

- 非腐敗性牛乳加工技術

- 賞味期限延長方法

- 栄養プロファイルの比較

- 感覚特性

- 製造プロセス分析

- UHT処理

- 蒸発と凝縮

- スプレー乾燥

- 無菌包装

- 品質管理プロセス

- 原材料分析と調達戦略

- 価格分析

- 持続可能性と環境影響評価

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 市場シェア分析

- 戦略枠組み

- 合併と買収

- ジョイントベンチャーとコラボレーション

- 新製品開発

- 拡大戦略

- 競合ベンチマーキング

- ベンダー情勢

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

- ブランドポジショニングと消費者認識分析

- 新規参入者の市場参入戦略

- プライベートラベル分析と戦略

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- UHT(超高温)牛乳

- 全乳(UHT)

- 低脂肪UHT牛乳

- 脱脂UHT牛乳

- 風味付きUHTミルク

- エバミルク

- 全乳

- 脱脂練乳

- その他

- 加糖練乳

- 通常の加糖練乳

- 風味付き加糖練乳

- その他

- 加糖練乳

- 通常の加糖練乳

- 風味付き加糖練乳

- その他

- 粉乳

- 全乳粉乳

- 脱脂粉乳

- 脂肪分の多い粉乳

- 乳児用調製粉乳

- その他

- その他

第6章 市場推計・予測:ソース別、2021年~2034年

- 主要動向

- 牛乳

- ヤギミルク

- 水牛のミルク

- 植物由来の代替品

- 豆乳

- アーモンドミルク

- オートミルク

- ココナッツミルク

- その他

- その他

第7章 市場推計・予測:脂肪含有量別、2021年~2034年

- 主要動向

- 全脂肪(脂肪分3.5%以上)

- 低脂肪/低脂肪(脂肪分1.5~1.8%)

- 脱脂/低脂肪(脂肪分0.5%未満)

- 無脂肪(脂肪0%)

- 脂肪含有量の変動

第8章 市場推計・予測:包装形態別、2021年~2034年

- 主要動向

- テトラパック/アセプティックカートン

- レンガ箱

- ゲーブルトップカートン

- その他

- 缶

- スチール缶

- アルミ缶

- ボトル

- ガラス瓶

- ペットボトル

- パウチ

- バッグインボックス

- 缶・小袋(粉ミルク用)

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- スーパーマーケット・ハイパーマーケット

- 専門店

- コンビニエンスストア

- オンライン小売

- 企業のウェブサイト

- eコマースプラットフォーム

- サブスクリプションサービス

- フードサービス

- ホテル&レストラン

- カフェ&ベーカリー

- 施設内ケータリング

- 直接販売(B2B)

- その他

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 直接消費

- 食品加工

- ベーカリー・菓子類

- 乳製品

- 幼児用食品

- 調理済み食品

- その他

- 飲料業界

- コーヒー・紅茶

- スムージー・シェイク

- その他

- 外食産業

- 栄養補助食品

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州地域

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第12章 企業プロファイル

- Nestle S.A.

- Danone S.A.

- Lactalis Group

- Fonterra Co-operative Group Limited

- FrieslandCampina

- Arla Foods amba

- Dean Foods(Dairy Farmers of America)

- Saputo Inc.

- Parmalat S.p.A.(Lactalis)

- Amul(Gujarat Cooperative Milk Marketing Federation)

- China Mengniu Dairy Company Limited

- Inner Mongolia Yili Industrial Group Co.、Ltd.

- Morinaga Milk Industry Co.、Ltd.

- Meiji Holdings Co.、Ltd.

- Savencia Fromage &Dairy

- DMK Deutsches Milchkontor GmbH

- Muller Group

- Dairy Farmers of America、Inc.

- Almarai Company

- Grupo LALA

- Vinamilk(Vietnam Dairy Products JSC)

- Borden Dairy Company

- Dairy Partners Americas(DPA)

- Darigold、Inc.

- California Dairies、Inc.

- Sodiaal

- Glanbia plc

- Schreiber Foods Inc.

- Land O'Lakes、Inc.

- Dairy Crest Group plc(Saputo)

目次

The Global Non-Perishable Milk Market was valued at USD 200.5 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 343.2 billion by 2034. This growth is largely fueled by the increasing demand for milk products with extended shelf life and minimal refrigeration requirements. Non-perishable milk has evolved from being a practical option in regions lacking cold storage to a mainstream choice worldwide. Consumers are gravitating toward options that offer convenience, nutritional value, and longer usability. With rising urbanization and shifting dietary preferences, the industry continues to expand its reach across diverse consumer groups.

The market has been shaped by growing interest in fortified, organic, and lactose-free milk variants. These preferences are reshaping product development strategies as manufacturers respond to changing health and lifestyle trends. Technological innovations, especially in processing methods, are also contributing to market expansion. Advancements in Ultra-High Temperature (UHT) treatment and high-temperature short-time (HTST) techniques, combined with aseptic packaging, have improved the safety, quality, and durability of non-perishable milk. These factors are enabling broader distribution and increased consumption, especially in areas with limited access to refrigerated goods. In parallel, there's a rise in awareness regarding calcium-rich diets, which plays into higher milk consumption patterns. Even plant-based alternatives are gaining space in the non-perishable segment, reflecting evolving consumer priorities toward sustainability and wellness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $200.5 Billion |

| Forecast Value | $343.2 Billion |

| CAGR | 5.6% |

In terms of product segmentation, the non-perishable milk market includes UHT milk, evaporated milk, sweetened condensed milk, powdered milk, and others. Among these, UHT milk led the category in 2024 with a market share of 29.5%, representing USD 59.2 billion. Its dominance is attributed to its versatility and ability to remain fresh without refrigeration for extended periods, making it a preferred option in both urban and rural settings. Powdered and evaporated variants are also well-established, particularly where affordability and long-term storage are essential. Sweetened condensed milk maintains its relevance in culinary applications, though health concerns are slightly dampening its growth rate in some areas.

When evaluated by source, the market is segmented into cow milk, goat milk, buffalo milk, plant-based milk, and others. Cow milk accounted for 29.7% of the total market in 2024 and is expected to grow at a CAGR of 5.3% through 2034. Its continued popularity is supported by its availability in UHT and powdered forms, which align well with current consumer demands for convenient, ready-to-use dairy options. Goat milk is steadily gaining traction among consumers seeking lactose-intolerant-friendly or easily digestible alternatives. Meanwhile, buffalo milk retains niche appeal due to its higher fat content and regional preferences.

Distribution channels for non-perishable milk include supermarkets and hypermarkets, specialty stores, convenience stores, online retail, food service outlets, direct B2B sales, and others. Supermarkets and hypermarkets commanded the largest share of the market in 2024, accounting for 31.5%. Their popularity stems from their ability to offer a wide selection of products in one location, making them a go-to choice for everyday consumers. Specialty stores are increasingly favored for premium offerings, especially for health-centric or plant-based milk variants. Convenience stores play a key role in fulfilling demand for single-serve or on-the-go formats. Online retail is experiencing rapid growth, driven by the convenience of doorstep delivery and the expansion of e-commerce platforms. Food service channels continue to rely on UHT and powdered milk for consistent supply and ease of storage. Direct sales to businesses remain robust, particularly in institutional and commercial sectors. Additional distribution methods include vending and export-focused channels that are helping brands tap into untapped markets.

Regionally, North America held the largest share of the non-perishable milk market in 2024, contributing 34.3% of the total revenue. The regional market has seen increasing adoption of UHT milk and other long-lasting dairy products, thanks to evolving consumer lifestyles and greater interest in shelf-stable nutrition options. Europe follows closely with a strong preference for UHT milk due to its convenience and reduced reliance on cold chains.

Major industry players such as Lactalis International, Nestle S.A., Fonterra Co-operative Group Limited, Danone S.A., and Arla Foods are instrumental in driving market growth. Their influence is particularly evident in innovation, processing technology, and global distribution capabilities. These companies are consistently investing in product development and expanding their presence to meet the growing global demand for non-perishable milk products.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Methodology and scope

- 1.2 Research methodology

- 1.3 Research scope & assumptions

- 1.4 List of data sources

- 1.5 Market estimation technique

- 1.6 Research limitations

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Manufacturers

- 3.1.4 Distributors

- 3.1.5 Impact on trade

- 3.1.6 Trade volume disruptions

- 3.2 Retaliatory measures

- 3.3 Impact on the industry

- 3.3.1 Supply-side impact (Raw Materials)

- 3.3.1.1 Price volatility in key materials

- 3.3.1.2 Supply chain restructuring

- 3.3.1.3 Production cost implications

- 3.3.1 Supply-side impact (Raw Materials)

- 3.4 Demand-side impact (Selling Price)

- 3.4.1 Price transmission to end markets

- 3.4.2 Market share dynamics

- 3.4.3 Consumer response patterns

- 3.5 Key companies impacted

- 3.6 Strategic industry responses

- 3.6.1 Supply chain reconfiguration

- 3.6.2 Pricing and product strategies

- 3.6.3 Policy engagement

- 3.7 Outlook and future considerations

- 3.8 Supplier landscape

- 3.9 Profit margin analysis

- 3.10 Key news & initiatives

- 3.11 Regulatory framework and standards

- 3.11.1 Food safety regulations

- 3.11.2 Labeling requirements

- 3.11.3 Quality standards

- 3.11.4 Import/export regulations

- 3.11.5 Organic & clean label certifications

- 3.12 Impact forces

- 3.12.1 Growth drivers

- 3.12.1.1 Urbanization and evolving lifestyles

- 3.12.1.2 Technological advancements in processing and packaging

- 3.12.1.3 Retail expansion and government support

- 3.12.2 Industry pitfalls & challenges

- 3.12.2.1 Supply chain disruptions

- 3.12.2.2 Economic uncertainty

- 3.12.3 Market opportunities

- 3.12.1 Growth drivers

- 3.13 Product overview

- 3.13.1 Nonperishable milk processing technologies

- 3.13.2 Shelf-life extension methods

- 3.13.3 Nutritional profile comparison

- 3.13.4 Sensory characteristics

- 3.14 Manufacturing process analysis

- 3.14.1 UHT processing

- 3.14.2 Evaporation & Condensation

- 3.14.3 Spray drying

- 3.14.4 Aseptic packaging

- 3.14.5 Quality control processes

- 3.15 Raw material analysis & procurement strategies

- 3.16 Pricing analysis

- 3.17 Sustainability & environmental impact assessment

- 3.18 Growth potential analysis

- 3.19 Porter's analysis

- 3.20 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Market share analysis

- 4.3 Strategic framework

- 4.3.1 Mergers & acquisitions

- 4.3.2 Joint ventures & collaborations

- 4.3.3 New product developments

- 4.3.4 Expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Vendor landscape

- 4.6 Competitive positioning matrix

- 4.7 Strategic dashboard

- 4.8 Brand positioning & consumer perception analysis

- 4.9 Market entry strategies for new players

- 4.10 Private label analysis & strategies

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 UHT (Ultra-High Temperature) milk

- 5.2.1 Whole UHT milk

- 5.2.2 Semi-skimmed UHT milk

- 5.2.3 Skimmed UHT milk

- 5.2.4 Flavored UHT milk

- 5.3 Evaporated milk

- 5.3.1 Whole evaporated milk

- 5.3.2 Skimmed evaporated milk

- 5.3.3 Others

- 5.4 Sweetened condensed milk

- 5.4.1 Regular sweetened condensed milk

- 5.4.2 Flavored sweetened condensed milk

- 5.4.3 Others

- 5.5 Sweetened condensed milk

- 5.5.1 Regular sweetened condensed milk

- 5.5.2 Flavored sweetened condensed milk

- 5.5.3 Others

- 5.6 Powdered milk

- 5.6.1 Whole milk powder

- 5.6.2 Skimmed milk powder

- 5.6.3 Fat-filled milk powder

- 5.6.4 Infant formula

- 5.6.5 Others

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cow milk

- 6.3 Goat milk

- 6.4 Buffalo milk

- 6.5 Plant-based alternatives

- 6.5.1 Soy milk

- 6.5.2 Almond milk

- 6.5.3 Oat milk

- 6.5.4 Coconut milk

- 6.5.5 Others

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Fat Content, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Whole/full fat (≥3.5% Fat)

- 7.3 Semi-skimmed/reduced fat (1.5-1.8% Fat)

- 7.4 Skimmed/low fat (≤0.5% Fat)

- 7.5 Fat-free (0% Fat)

- 7.6 Variable fat content

Chapter 8 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Tetra packs/aseptic cartons

- 8.2.1 Brick cartons

- 8.2.2 Gable top cartons

- 8.2.3 Others

- 8.3 Cans

- 8.3.1 Steel cans

- 8.3.2 Aluminum cans

- 8.4 Bottles

- 8.4.1 Glass bottles

- 8.4.2 Plastic bottles

- 8.5 Pouches

- 8.6 Bag-in-box

- 8.7 Tins & sachets (for Powdered Milk)

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets & hypermarkets

- 9.3 Specialty stores

- 9.4 Convenience stores

- 9.5 Online retail

- 9.5.1 Company websites

- 9.5.2 E-commerce platforms

- 9.5.3 Subscription services

- 9.6 Foodservice

- 9.6.1 Hotels & restaurants

- 9.6.2 Cafes & bakeries

- 9.6.3 Institutional catering

- 9.7 Direct sales (B2B)

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct consumption

- 10.3 Food processing

- 10.3.1 Bakery & confectionery

- 10.3.2 Dairy products

- 10.3.3 Infant food

- 10.3.4 Prepared foods

- 10.3.5 Others

- 10.4 Beverage industry

- 10.4.1 Coffee & tea

- 10.4.2 Smoothies & shakes

- 10.4.3 Others

- 10.5 Food service industry

- 10.6 Nutritional supplements

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.3.7 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 Nestle S.A.

- 12.2 Danone S.A.

- 12.3 Lactalis Group

- 12.4 Fonterra Co-operative Group Limited

- 12.5 FrieslandCampina

- 12.6 Arla Foods amba

- 12.7 Dean Foods (Dairy Farmers of America)

- 12.8 Saputo Inc.

- 12.9 Parmalat S.p.A. (Lactalis)

- 12.10 Amul (Gujarat Cooperative Milk Marketing Federation)

- 12.11 China Mengniu Dairy Company Limited

- 12.12 Inner Mongolia Yili Industrial Group Co., Ltd.

- 12.13 Morinaga Milk Industry Co., Ltd.

- 12.14 Meiji Holdings Co., Ltd.

- 12.15 Savencia Fromage & Dairy

- 12.16 DMK Deutsches Milchkontor GmbH

- 12.17 Muller Group

- 12.18 Dairy Farmers of America, Inc.

- 12.19 Almarai Company

- 12.20 Grupo LALA

- 12.21 Vinamilk (Vietnam Dairy Products JSC)

- 12.22 Borden Dairy Company

- 12.23 Dairy Partners Americas (DPA)

- 12.24 Darigold, Inc.

- 12.25 California Dairies, Inc.

- 12.26 Sodiaal

- 12.27 Glanbia plc

- 12.28 Schreiber Foods Inc.

- 12.29 Land O'Lakes, Inc.

- 12.30 Dairy Crest Group plc (Saputo)

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日