|

市場調査レポート

商品コード

1939601

南米の飼料添加物:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)South America Feed Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の飼料添加物:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

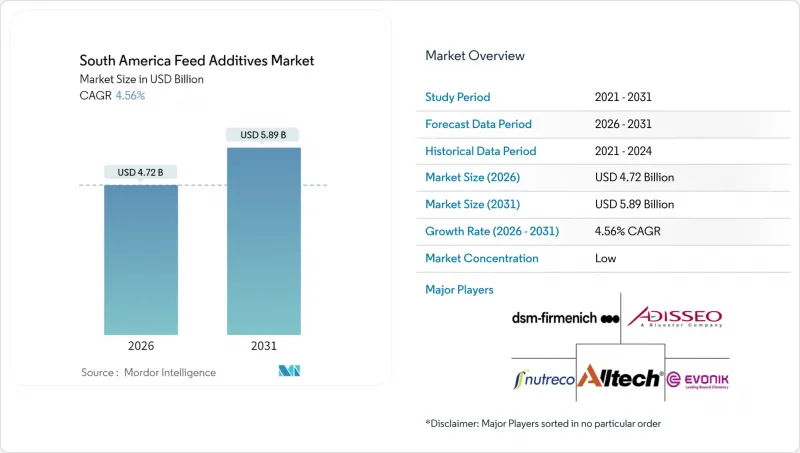

南米の飼料添加物市場は、2025年に45億1,000万米ドルと評価され、2026年の47億2,000万米ドルから2031年までに58億9,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは4.56%と見込まれます。

この成長は、畜産および水産養殖システム全体における栄養・機能性成分への堅調な需要を反映しています。同地域は、特にブラジルとアルゼンチンにおけるトウモロコシと大豆の豊作に支えられた、安定した原料供給の恩恵を受けています。家禽およびサケの生産増加に伴い、生産性向上添加物の使用が拡大しています。OECDによれば、アルゼンチンの家禽肉消費量は2022年の213万トンから2024年には232万トンへ増加しました。FAOSTATデータでは、羊肉生産量が2022年の25万8,961トンから2023年には33万5,764トンへ増加しています。ブラジルとアルゼンチンにおける規制の改善により、製品承認サイクルが短縮され、イノベーションと市場参入の迅速化が促進されています。さらに、大豆原料からのリジンおよびメチオニンの現地生産は、地域のバイヤーを通貨変動から保護し、コスト安定性を確保するのに役立っています。これらの複合的な要因により、通貨変動や飼料工場の生産能力の分散化が短期的な利益率に課題をもたらしているにもかかわらず、南米は先進的な飼料ソリューションの競争力ある供給地としての地位を確立しています。

南米飼料添加物市場の動向と洞察

産業用家禽・豚生産の堅調な成長

南米全域で工業的養鶏・養豚生産が拡大を続けており、飼料効率を向上させるアミノ酸や酵素の需要を牽引しています。大規模飼料工場と統合システムは、高品質添加剤の高い配合率を支えています。輸出志向型モデルは枝肉品質基準を引き上げ、栄養強化剤の使用を促進します。豚飼料の需要も着実に増加しており、飼料要求率を改善する付加価値の高い配合の必要性を高めています。飼料コストが総生産費の大部分を占める中、栄養利用率を高める添加剤は、競合の激しい畜産拠点において収益性を維持するための必須ツールとなっています。

飼料効率への費用対効果重視の高まり

変動する商品価格と為替変動が生産者の利益率を圧迫する中、飼料効率を改善する添加剤への関心が高まっています。酵素やバランスの取れたアミノ酸プロファイルは、標準的なトウモロコシ・大豆飼料からエネルギーを効率的に引き出すのに役立ちます。精密給餌プラットフォームはリアルタイムでの配合調整を可能にし、収益性の向上と廃棄物の削減を実現します。エネルギーコストが高い地域では、動物の耐性を高め、電力消費量の多いシステムへの依存を減らす配合が注目を集めています。炭水化物分解酵素やフィターゼはより多くの消化可能な栄養素を抽出します。一方、データ駆動型分析は添加剤の使用と測定可能な財務成果を結びつけ、費用対効果の高い畜産管理における添加剤の役割を強化しています。

通貨変動が輸入添加物価格を押し上げる

南米全域における為替レートの変動により、輸入飼料添加物、特にビタミンや微量ミネラルのコストが増加しています。現地通貨はドルに対して弱含みとなることが多く、購買力が低下し、予算に負担がかかります。エネルギー料金の上昇はさらに運営コストを圧迫し、飼料メーカーは低コストの代替品を探すか、高価な添加剤の試験導入を遅らせることを余儀なくされています。デュアルソーシング、先物契約、国内アミノ酸生産への依存度向上などの戦略が、これらの課題の緩和に役立っています。財政的な逆風にもかかわらず、生産者は測定可能な効率性と回復力のメリットをもたらす添加剤を引き続き優先しています。

セグメント分析

2025年、アミノ酸は南米飼料添加物市場シェアの20.55%を占めました。これは、トウモロコシ・大豆配合飼料におけるリジンとメチオニンのバランス調整に注力する統合生産者によるものです。現地の粉砕工場や発酵施設は、多国籍企業および国内生産者にとってコスト優位性を提供しています。安定した供給網は為替リスクを最小限に抑え、家禽・豚生産者が粗タンパク質レベルを削減しつつ成長性能を維持するためにアミノ酸を利用する信頼性を高めています。需要が最も高いのは、高純度粉末および液体メチオニンを効率的に調達できるブラジルの家禽産地とアルゼンチンの豚生産地域です。特に低タンパク質配合飼料を中心とした採卵用飼料の採用拡大が、アミノ酸の使用を後押ししています。

抗酸化剤は、主に集約的な水産養殖システムからの需要増加により、2026年から2031年にかけてCAGR5.21%で成長すると予測されています。チリのサーモン加工業者は、フィレの色調保持と保存期間延長のため、天然トコフェロールとポリフェノール抽出物の組み合わせを好んで採用しています。ブラジルのエビ生産者は、オメガ3脂肪酸の強化とストレス軽減効果を併せ持つ微細藻由来の抗酸化剤を導入しています。これらの添加剤は、ケージ養殖、池養殖、循環式養殖システムにおいて免疫機能を強化し、合成保存料の使用量を削減します。

南米飼料添加物市場レポートは、添加物別(酸性化剤、アミノ酸、抗生物質、抗酸化剤など)、動物別(水産養殖、家禽、反芻動物、豚など)、地域別(アルゼンチン、ブラジル、チリなど)に分類されています。市場予測は金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 エグゼクティブサマリーおよび主要な調査結果

第2章 レポート提供

第3章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第4章 主要な業界動向

- 家畜頭数

- 家禽

- 反芻動物

- 豚

- 飼料生産

- 水産養殖

- 家禽

- 反芻動物

- 豚

- 規制の枠組み

- アルゼンチン

- ブラジル

- チリ

- バリューチェーン及び流通チャネル分析

- 市場促進要因

- 産業用家禽・豚生産の堅調な成長

- 飼料効率性に対する費用対効果重視の高まり

- 競争力のある価格の大豆由来アミノ酸の供給状況

- 水産養殖生産量の増加が特殊添加剤需要を牽引

- キアラヤサポニンの現地調達による植物性原料コストの削減

- AIを活用した精密給餌の導入

- 市場抑制要因

- 通貨変動による輸入添加剤価格の高騰

- 飼料工場基盤の分散化が付加価値製品の導入を制限

- ビタミン供給網における短期的な供給過剰が利益率を圧迫

- 新規微生物株の規制承認が遅延

第5章 市場規模と成長予測(数量および金額)

- 添加物別

- 酸性化剤

- フマル酸

- 乳酸

- プロピオン酸

- その他の酸性化剤

- アミノ酸

- リジン

- メチオニン

- スレオニン

- トリプトファン

- その他のアミノ酸

- 抗生物質

- バシトラシン

- ペニシリン類

- テトラサイクリン系

- タイロシン

- その他の抗生物質

- 抗酸化剤

- ブチル化ヒドロキシアニソール(BHA)

- ブチル化ヒドロキシトルエン(BHT)

- クエン酸

- エトキシキン

- プロピルガレート

- トコフェロール

- その他の抗酸化剤

- 結合剤

- 天然結合剤

- 合成結合剤

- 酵素

- 炭水化物分解酵素

- フィターゼ

- その他の酵素

- 香料・甘味料

- フレーバー

- 甘味料

- ミネラル

- 主要ミネラル

- 微量ミネラル

- マイコトキシン解毒剤

- 結合剤

- バイオトランスフォーマー

- 植物性原料

- 精油

- ハーブ&スパイス

- その他の植物性原料

- 色素

- カロテノイド

- クルクミン&スピルリナ

- プレバイオティクス

- フルクトオリゴ糖

- ガラクトオリゴ糖

- イヌリン

- ラクツロース

- マンナンオリゴ糖

- キシロオリゴ糖

- その他のプレバイオティクス

- プロバイオティクス

- ビフィズス菌

- エンテロコッカス

- 乳酸菌

- ペディオコッカス

- ストレプトコッカス

- その他のプロバイオティクス

- ビタミン

- ビタミンA

- ビタミンB

- ビタミンC

- ビタミンE

- その他のビタミン

- 酵母

- 生酵母

- セレン酵母

- 使用済み酵母

- トルラ乾燥酵母

- ホエイ酵母

- 酵母派生品

- 酸性化剤

- 動物別

- 養殖

- 魚類

- エビ

- その他の養殖種

- 家禽

- ブロイラー

- 採卵鶏

- その他の家禽類

- 反芻動物

- 肉用牛

- 乳用牛

- その他の反芻動物

- 豚

- その他の動物

- 養殖

- 地域別

- アルゼンチン

- ブラジル

- チリ

- その他南米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Adisseo France SAS(China National BlueStar Co. Ltd.)

- Alltech Inc.

- Archer-Daniels-Midland Company

- Cargill Incorporated

- DSM-Firmenich AG

- Evonik Industries AG

- IFF Danisco Animal Nutrition and Health

- Kemin Industries Inc.

- Novus International, Inc.(Mitsui & Co., Ltd.)

- Nutreco N.V.(SHV Holdings N.V.)

- BASF SE

- BioMar A/S(Schouw & Co.)

- CJ CheilJedang Corp.(CJ Corporation)

- Elanco Animal Health Incorporated

- Phibro Animal Health Corporation