|

市場調査レポート

商品コード

1741029

可変周波数ドライブ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Variable Frequency Drives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 可変周波数ドライブ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月24日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

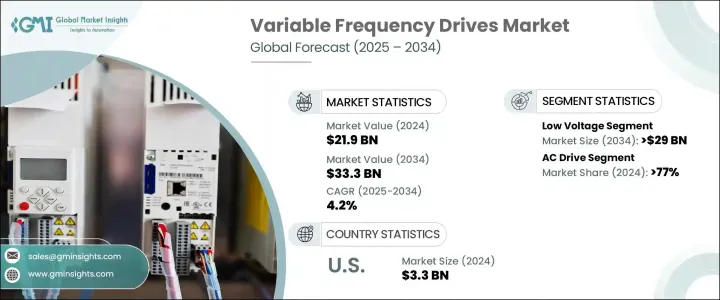

世界の可変周波数ドライブ市場は、2024年には219億米ドルとなり、CAGR 4.2%で成長し、2034年には333億米ドルに達すると推定されています。

この増加傾向は、主に持続可能性と省エネルギーが重視されるようになったことに起因しています。世界中の多くの政府が環境政策を強化し、産業界に最新のエネルギー効率規制への準拠を促しています。こうした規制は、省エネ技術の採用に対するインセンティブと相まって、メーカーや施設に業務の近代化を促しています。その結果、VFDはこのような移行において重要な役割を果たすようになり、エネルギー消費の削減と産業排出の抑制に役立っています。

デジタル化と自動化が進む世界では、IoTと機械学習機能の産業オペレーションへの統合が、VFDの使用方法を再構築する上で重要な役割を果たしています。これらのスマートテクノロジーは、リアルタイムの監視、故障検出、予知保全を可能にし、運転効率を高めてダウンタイムを削減します。産業界は現在、より高いレベルの精度、適応性、信頼性を提供するVFDソリューションを求めています。企業がよりスマートで応答性の高いエネルギー制御システムを求める中、このシフトは市場に新たな成長の道を開いています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 219億米ドル |

| 予測金額 | 333億米ドル |

| CAGR | 4.2% |

過去のデータでは、前年比成長率は一貫しており、VFDの世界市場規模は2022年に207億米ドル、2023年に211億米ドル、2024年に219億米ドルとなりました。電圧に基づく市場セグメンテーションでは、低電圧ドライブと中電圧ドライブの2つの主要カテゴリーが明らかになりました。このうち、低電圧VFDは予測期間中も優位を保つとみられ、収益は2034年までに290億米ドルを超えると予測されます。このセグメントが引き続き主導権を握っている背景には、オートメーション技術の普及、省エネルギーへの関心の高まり、費用対効果の高い性能強化への業界全体のシフトがあります。コンパクトで効率的、かつ統合が容易なシステムを好む傾向が強まっていることから、低電圧ドライブはさまざまな分野に理想的に適合しています。

市場は、ACドライブ、DCドライブ、サーボドライブなどのドライブタイプによってさらに分類されます。現在、ACドライブが最大のシェアを占めており、2024年の世界市場の77%以上を占めています。ACドライブの人気は引き続き高く、2034年には260億米ドルまで成長すると予測されています。ACドライブの持続的な需要は、スマート機能を組み込んだ継続的な技術改善によって全体的な性能が向上し、幅広い用途でその魅力が増していることに起因しています。これらのドライブは優れたエネルギー制御を提供するため、効率性と自動化が最優先される現代の産業環境に適しています。

地域別では、米国が依然として世界市場の収益に大きく貢献しています。米国のVFD市場は、2022年と2023年の両方で32億米ドルであり、2024年には33億米ドルに達しました。着実な上昇は、製造、産業オートメーション、空調制御システムなどの分野でエネルギー効率の高いソリューションが広く導入されていることが背景にあります。これらの分野の企業は、環境コンプライアンス目標を達成しながら運用コストを削減する技術に多額の投資を行っており、先進的なVFDシステムの需要をさらに高めています。

市場の競争力学は激化の一途をたどっており、大手企業は市場全体の30%以上のシェアを占めています。有力企業には、ロックウェル・オートメーション、ダンフォス、ABB、シーメンス、三菱電機などがあります。業界をリードするこれらの企業は、革新的な製品ラインの導入や戦略的提携を通じて市場の拡大に注力しています。ブランドの存在感を高め、より多くの顧客層を獲得することを目的とした合弁事業、パートナーシップ、技術提携などの取り組みが行われています。

製品の革新、運転効率、エネルギーの最適化は、VFDメーカーにとって依然として中心的な注力分野です。拡大する市場ニーズに対応するため、多くの企業が生産能力を拡大し、デジタルエコシステムにシームレスに統合する次世代製品を投入しています。各国政府が引き続き厳しい環境政策を実施する中、二酸化炭素排出量の削減と持続可能性の向上におけるVFDの役割はますます強くなり、業界の長期的な発展の舞台が整うことになるでしょう。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 市場規模・予測:電圧別、2021-2034

- 主要動向

- 低

- 中

第5章 市場規模・予測:車で、2021-2034

- 主要動向

- 交流

- DC

- サーボ

第6章 市場規模・予測:用途別、2021-2034

- 主要動向

- ポンプ

- ファン

- コンベア

- コンプレッサー

- 押出機

- その他

第7章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 石油・ガス

- 発電

- 鉱業および金属

- パルプ・紙

- 海洋

- その他

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- デンマーク

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- ABB

- Beckhoff Automation

- Bosch Rexroth

- Danfoss

- Eaton

- Emerson Electric

- Fuji Electric

- GE Vernova

- Hiconics Eco-energy Technology

- Hitachi Industrial Equipment Systems

- Honeywell International

- Invertek Drives

- Johnson Controls

- Mitsubishi Electric

- Nidec Motor

- Rockwell Automation

- Schneider Electric

- Siemens

- WEG

- Yaskawa Electric

The Global Variable Frequency Drives Market was valued at USD 21.9 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 33.3 billion by 2034. This upward trend is primarily attributed to the growing importance placed on sustainability and energy conservation. Many governments around the world are reinforcing environmental policies, prompting industries to comply with updated energy efficiency regulations. These regulations, combined with incentives for adopting energy-saving technologies, are pushing manufacturers and facilities to modernize their operations. As a result, VFDs have become a critical part of these transitions, helping reduce energy consumption and curb industrial emissions.

In an increasingly digital and automated world, the integration of IoT and machine learning capabilities into industrial operations is playing a key role in reshaping how VFDs are used. These smart technologies enable real-time monitoring, fault detection, and predictive maintenance, which enhance operational efficiency and reduce downtime. Industries are now demanding VFD solutions that offer higher levels of precision, adaptability, and reliability. This shift is opening up new growth avenues for the market as enterprises look for smarter and more responsive energy control systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.9 Billion |

| Forecast Value | $33.3 Billion |

| CAGR | 4.2% |

Historical data highlights consistent year-over-year growth, with the global VFD market valued at USD 20.7 billion in 2022, USD 21.1 billion in 2023, and USD 21.9 billion in 2024. Market segmentation based on voltage reveals two main categories: low voltage and medium voltage drives. Among these, low voltage VFDs are expected to remain dominant through the forecast period, with revenue projected to surpass USD 29 billion by 2034. This segment's continued leadership is driven by the widespread adoption of automation technologies, a growing focus on energy savings, and an industry-wide shift toward cost-effective performance enhancements. The increasing preference for compact, efficient, and easy-to-integrate systems makes low voltage drives an ideal fit across multiple sectors.

The market is further divided based on drive types, which include AC drives, DC drives, and servo drives. AC drives currently account for the largest share, contributing over 77% of the global market in 2024. Their popularity is expected to remain strong, with projections indicating growth to USD 26 billion by 2034. The sustained demand for AC drives stems from ongoing technological improvements that incorporate smart functionality, which has enhanced their overall performance and increased their appeal across a broad range of applications. These drives offer superior energy control, which makes them well-suited for modern industrial environments where efficiency and automation are paramount.

Regionally, the United States remains a significant contributor to global market revenue. The U.S. VFD market stood at USD 3.2 billion in both 2022 and 2023, and reached USD 3.3 billion in 2024. The steady rise is driven by widespread implementation of energy-efficient solutions across sectors such as manufacturing, industrial automation, and climate control systems. Businesses in these areas are investing heavily in technologies that help lower operational costs while meeting environmental compliance goals, further bolstering demand for advanced VFD systems.

Competitive dynamics in the market continue to intensify, with leading players collectively holding more than 30% of the total market share. Prominent companies include Rockwell Automation, Danfoss, ABB, Siemens, and Mitsubishi Electric Corporation. These industry leaders are focusing on expanding their market reach through the introduction of innovative product lines and strategic alliances. Efforts include joint ventures, partnerships, and technology collaborations aimed at strengthening brand presence and capturing a larger customer base.

Product innovation, operational efficiency, and energy optimization remain the core focus areas for VFD manufacturers. To address growing market needs, many companies are scaling up production capabilities and introducing next-generation products that integrate seamlessly into digital ecosystems. As governments continue enforcing stringent environmental policies, the role of VFDs in reducing carbon footprints and enhancing sustainability will only grow stronger, setting the stage for long-term industry advancement.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Market Size and Forecast, By Voltage, 2021 - 2034, ('000 Units & USD Million)

- 4.1 Key trends

- 4.2 Low

- 4.3 Medium

Chapter 5 Market Size and Forecast, By Drive, 2021 - 2034, ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 AC

- 5.3 DC

- 5.4 Servo

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034, ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Pump

- 6.3 Fan

- 6.4 Conveyor

- 6.5 Compressor

- 6.6 Extruder

- 6.7 Others

Chapter 7 Market Size and Forecast, By End Use, 2021 - 2034, ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 Oil & gas

- 7.3 Power generation

- 7.4 Mining & metals

- 7.5 Pulp & paper

- 7.6 Marine

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034, ('000 Units & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Denmark

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Beckhoff Automation

- 9.3 Bosch Rexroth

- 9.4 Danfoss

- 9.5 Eaton

- 9.6 Emerson Electric

- 9.7 Fuji Electric

- 9.8 GE Vernova

- 9.9 Hiconics Eco-energy Technology

- 9.10 Hitachi Industrial Equipment Systems

- 9.11 Honeywell International

- 9.12 Invertek Drives

- 9.13 Johnson Controls

- 9.14 Mitsubishi Electric

- 9.15 Nidec Motor

- 9.16 Rockwell Automation

- 9.17 Schneider Electric

- 9.18 Siemens

- 9.19 WEG

- 9.20 Yaskawa Electric