|

|

市場調査レポート

商品コード

1740963

HVACの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年HVAC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| HVACの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

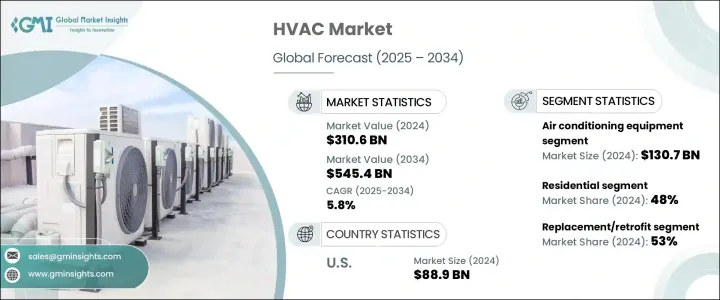

HVACの世界市場規模は、2024年に3,106億米ドルとなり、CAGR 5.8%で成長し、2034年には5,454億米ドルに達すると予測されています。

この成長を支える主な要因の1つは、先進国と発展途上国の両方でエネルギー効率が高く環境に優しい冷却技術に対する需要が高まっていることです。持続可能性と環境保護に対する世界の関心が高まるにつれ、メーカー各社はエネルギー消費量と排出量の少ない先進的なHVACシステムの革新と開発に取り組んでいます。規制機関は、そのようなシステムの使用を促進する様々なエネルギー効率化プログラムを実施しており、企業と消費者の両方が、エネルギーを意識したHVACソリューションを選択するよう促しています。このような嗜好の変化は、より優れた性能と運転コストの削減を提供するスマート空調システムや可変速空調システムの採用を加速させています。特に空調システムにおいて消費電力を削減する必要性が高まっているため、エネルギー効率の高いHVAC技術は、住宅、商業施設、産業用アプリケーションにおいてますます魅力的なものとなっています。さらに、気候変動と世界の気温の上昇により、より多くの地域で一貫した冷却システムの使用が推進され、高性能HVACユニットへのニーズがさらに高まっています。

新興市場における急速な都市化は、集合住宅、商業スペース、産業インフラの建設増加と相まって、市場にも拍車をかけています。最新の建物は、最新のエネルギー基準に準拠したスマートシステムと統合されたHVAC技術で設計されています。世界各国の政府は、新しい開発においてエネルギー効率の高い空調制御ソリューションの使用を義務付ける建築基準を施行しつつあります。よりスマートでコネクテッドなビルを目指す動きは、自動温度制御、スマートセンサー、IoT接続などの機能を備えたHVACシステムの需要に大きく貢献しています。さらに、特に古い建物では、最新の規制基準や持続可能性の目標を満たすためのアップグレードが必要であるため、後付け設置の人気が高まっています。2024年のHVAC市場全体に占める後付け/交換セグメントの割合は53%で、レガシーシステムがまだ使用されている市場で強い勢いを示しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 3,106億米ドル |

| 予測金額 | 5,454億米ドル |

| CAGR | 5.8% |

製品タイプ別に見ると、HVAC市場には空調機器、暖房機器、換気システム、冷凍機、冷却塔が含まれます。2024年には、空調機器が1,307億米ドルの売上を生み出し、支配的なカテゴリーとなりました。その継続的な成長は、特に空気の質と気温の上昇が懸念される都市部において、エネルギー効率の高い冷却ソリューションに対する意識が高まっていることが大きな要因となっています。一方、暖房機器分野は、費用対効果の高い低排出ガス暖房システムへの需要の高まりに支えられ、2025年から2034年にかけて約5.7%のCAGRで成長する見通しです。

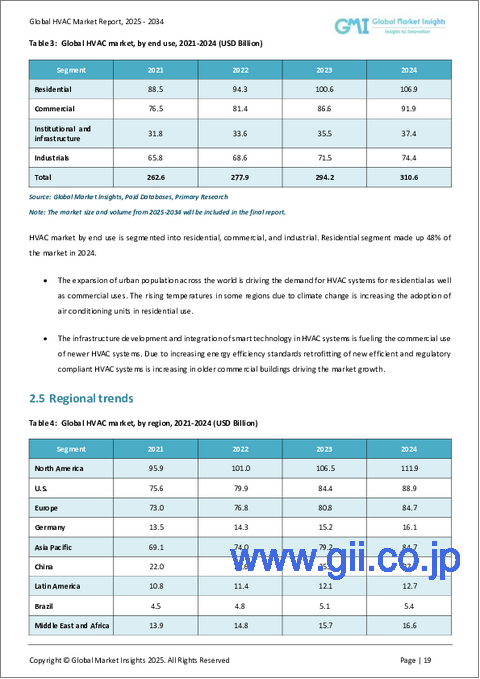

市場の最終用途セグメンテーションには、住宅、商業、工業部門が含まれます。住宅部門は2024年に市場の48%を占め、急速な都市拡大と、個人的な快適さのために空調・気候制御システムへの投資を増やしている中流階級の人口増加を背景としています。オフィスビル、小売店、ホスピタリティ施設などの商業スペースでも、高度なHVACシステムに対する需要が高まっています。これらの施設は、空気の質、快適性、業務効率を優先しており、スマートでコネクテッドなHVAC技術の導入を促進しています。商業施設では、インフラのアップグレードや、より厳しい環境基準への対応により、ビルオーナーが古いシステムを最新のエネルギー効率の高いソリューションに改修する動きが加速しています。

地域的には、米国がHVAC市場の主要な貢献者であり続け、北米のシェアの約79%を占め、2024年には889億米ドルの収益を生み出します。米国の市場成長は、冷暖房システムのエネルギー効率を促進する連邦政府の義務付けやインセンティブによって後押しされています。古いユニットを最新のエネルギー効率の高い代替品と交換する際に税額控除を提供するプログラムは、住宅と商業ビルの両方でシステムのアップグレードを加速させています。その結果、高度な接続性、エネルギー管理の改善、環境負荷の低減を特徴とするHVACシステムへの需要が急増しています。

いくつかの著名な企業が、製品の革新や戦略的パートナーシップを通じて、HVACの展望を積極的に形成しています。主な業界プレーヤーは、Carrier、Bosch、Daikin Industries、GREE Electric Appliances、Danfoss、Haier、Johnson Controls、Hisense HVAC Equipment、Lennox International、Midea、LG Electronics、Mitsubishi Electric、Rheem Manufacturing Company、Panasonic、Trane Technologiesなどです。これらの企業は、進化する消費者の期待や規制要件に対応するため、継続的に研究開発に投資しており、よりスマートで環境に優しく、効率的なHVACソリューションに向けて市場を牽引しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- インフラ開発の拡大

- さまざまな業界での利用が増加

- 技術的進歩

- 業界の潜在的リスク&課題

- 高い投資コスト

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:製品タイプ別、2021年~2034年

- 主要動向

- 暖房設備

- 炉

- ボイラー

- ヒートポンプ

- 換気設備

- 空調設備

- ダクト

- ファン

- 空調設備

- チラー

- 冷却塔

第6章 市場推定・予測:最終用途別、2021年~2034年

- 主要動向

- 住宅

- 商業

- 工業

第7章 市場推定・予測:設置別、2021年~2034年

- 主要動向

- 新設

- 交換/レトロフィット

第8章 市場推定・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第9章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Bosch

- Carrier

- Daikin Industries

- Danfoss

- GREE Electric Appliances

- Haier

- Hisense HVAC equipment

- Johnson Controls

- Lennox International

- LG Electronics

- Midea

- Mitsubishi Electric

- Panasonic

- Rheem Manufacturing Company

- Trane Technologies

The Global HVAC Market was valued at USD 310.6 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 545.4 billion by 2034. One of the major factors supporting this growth is the rising demand for energy-efficient and eco-friendly cooling technologies across both developed and developing countries. As global focus intensifies on sustainability and environmental protection, manufacturers are being encouraged to innovate and develop advanced HVAC systems that consume less energy and produce fewer emissions. Regulatory bodies are implementing various energy efficiency programs that promote the use of such systems, which is prompting both businesses and consumers to opt for energy-conscious HVAC solutions. This shift in preference is accelerating the adoption of smart and variable-speed air conditioning systems, which offer better performance and lower operational costs. The growing need to reduce power consumption, particularly in climate control systems, has made energy-efficient HVAC technologies increasingly attractive across residential, commercial, and industrial applications. Additionally, climate change and rising global temperatures are pushing more regions toward consistent use of cooling systems, further amplifying the need for high-performance HVAC units.

Rapid urbanization in emerging markets, combined with increased construction of residential complexes, commercial spaces, and industrial infrastructure, is also fueling the market. Modern buildings are being designed with smart systems and integrated HVAC technologies that comply with the latest energy standards. Governments around the world are enforcing building codes that mandate the use of energy-efficient climate control solutions in new developments. The push for smarter, more connected buildings has significantly contributed to the demand for HVAC systems equipped with features like automated temperature control, smart sensors, and IoT connectivity. In addition, retrofit installations are gaining traction, especially in older buildings that require upgrades to meet updated regulatory standards and sustainability goals. The retrofit/replacement segment accounted for 53% of the total HVAC market in 2024, showing strong momentum in markets where legacy systems are still in use.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $310.6 Billion |

| Forecast Value | $545.4 Billion |

| CAGR | 5.8% |

When broken down by product type, the HVAC market includes air conditioning equipment, heating equipment, ventilation systems, chillers, and cooling towers. In 2024, air conditioning equipment was the dominant category, generating revenue of USD 130.7 billion. Its continued growth is largely driven by increased awareness of energy-efficient cooling solutions, particularly in urban areas where air quality and rising temperatures are a growing concern. On the other hand, the heating equipment segment is poised to grow at a CAGR of approximately 5.7% from 2025 to 2034, supported by growing demand for cost-effective and low-emission heating systems.

End-use segmentation of the market includes residential, commercial, and industrial sectors. The residential segment comprised 48% of the market in 2024, backed by rapid urban expansion and a growing middle-class population that is increasingly investing in air conditioning and climate control systems for personal comfort. Commercial spaces, such as office buildings, retail outlets, and hospitality venues, are also witnessing heightened demand for advanced HVAC systems. These facilities prioritize air quality, comfort, and operational efficiency, driving the installation of smart and connected HVAC technologies. The commercial segment is further benefitting from infrastructure upgrades and compliance with stricter environmental standards, which are pushing building owners to retrofit older systems with modern, energy-efficient solutions.

Geographically, the United States remained a leading contributor to the HVAC market, accounting for approximately 79% of the North American share and generating revenue of USD 88.9 billion in 2024. The market growth in the US is being fueled by federal mandates and incentives that promote energy efficiency in heating and cooling systems. Programs offering tax credits for replacing older HVAC units with modern, energy-efficient alternatives are supporting the acceleration of system upgrades in both residential and commercial buildings. As a result, there has been a strong uptick in demand for HVAC systems that feature advanced connectivity, improved energy management, and reduced environmental impact.

Several prominent companies are actively shaping the HVAC landscape through product innovation and strategic partnerships. Key industry players include Carrier, Bosch, Daikin Industries, GREE Electric Appliances, Danfoss, Haier, Johnson Controls, Hisense HVAC Equipment, Lennox International, Midea, LG Electronics, Mitsubishi Electric, Rheem Manufacturing Company, Panasonic, and Trane Technologies. These companies are continually investing in R&D to meet evolving consumer expectations and regulatory requirements, helping to drive the market toward smarter, greener, and more efficient HVAC solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing infrastructure development

- 3.6.1.2 Growing uses in various industries

- 3.6.1.3 Technological advancements

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs of investments

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Heating equipment

- 5.2.1 Furnaces

- 5.2.2 Boiler

- 5.2.3 Heat pumps

- 5.3 Ventilation equipment

- 5.3.1 Air handlers

- 5.3.2 Ductwork

- 5.3.3 Fans

- 5.4 Air conditioning equipment

- 5.5 Chillers

- 5.6 Cooling towers

Chapter 6 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrials

Chapter 7 Market Estimates & Forecast, By Installation, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 New construction

- 7.3 Replacement/Retrofit

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Bosch

- 10.2 Carrier

- 10.3 Daikin Industries

- 10.4 Danfoss

- 10.5 GREE Electric Appliances

- 10.6 Haier

- 10.7 Hisense HVAC equipment

- 10.8 Johnson Controls

- 10.9 Lennox International

- 10.10 LG Electronics

- 10.11 Midea

- 10.12 Mitsubishi Electric

- 10.13 Panasonic

- 10.14 Rheem Manufacturing Company

- 10.15 Trane Technologies