|

市場調査レポート

商品コード

1740935

自動車用超音波技術の市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Ultrasonic Technologies Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用超音波技術の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月14日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

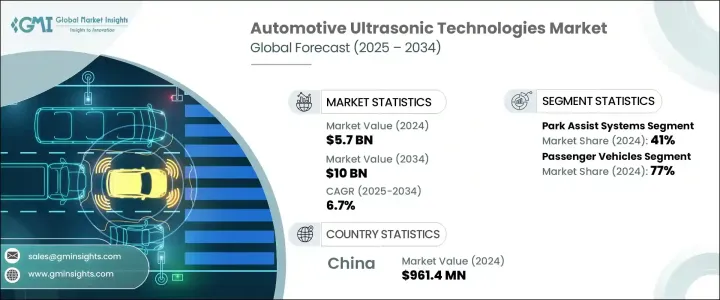

自動車用超音波技術の世界市場規模は2024年に57億米ドルとなり、ADAS(先進運転支援システム)のような自動車の先進安全機能に対する需要の高まりを背景に、CAGR 6.7%で成長し、2034年には100億米ドルに達すると予測されています。

自動車の安全性が引き続き重視される中、超音波技術の統合が次世代モビリティの重要な実現要素として浮上しています。自動車メーカーは、より安全で、よりスマートで、よりコネクテッドな自動車を求める消費者の期待に応える必要に迫られています。このシフトはプレミアム・ブランドに限ったことではなく、中級車や普及価格帯の自動車セグメントも、安全意識の高い消費者によってますます形成される市場で競争力を維持するために、超音波センサー・システムを急速に取り入れています。

自動車の安全基準の継続的な進化、技術の進歩、自律走行機能の推進により、超音波技術が単なるオプションではなく必須となる環境が生まれつつあります。自動車メーカー、サプライヤー、技術イノベーターは、スケーラブルで費用対効果の高い超音波ソリューションを市場に投入するために緊密に協力しており、エントリーレベルの自動車でさえ最先端の安全システムを装備できるようにしています。業界では、センサーの精度、耐久性、価格の向上に重点を置いた研究開発投資が加速しており、大量市場導入の余地が広がっています。世界各国の政府が厳格な自動車安全の枠組みを導入し、スマートモビリティの革新を奨励しているため、自動車用超音波技術市場は成熟経済圏と新興経済圏の両方で持続的な成長を遂げることになります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 57億米ドル |

| 予測金額 | 100億米ドル |

| CAGR | 6.7% |

パーキングセンサー、衝突回避、死角検出などの技術は、安全基準が強化されるにつれてますます普及しています。各地域の政府は、自動車安全規制を積極的に更新し、先進運転支援技術の採用を重視する新たなコンプライアンス枠組みを導入しています。UNECE、NHTSA、その他の世界的組織のような規制機関は、障害物検知、歩行者警告システム、自動ブレーキ、強化された駐車サポートなどの機能を義務付けることで中心的な役割を果たしており、これらはすべて超音波センシング機能に大きく依存しています。安全規制が基本的なコンプライアンスから積極的な事故防止へとシフトする中、超音波技術は自動車の安全革新において極めて重要な役割を担っています。自動車メーカーは現在、こうした世界の安全基準を満たし、安全を重視する消費者のロイヤリティを獲得するため、プレミアム・モデルだけでなく、中級車やエントリー・レベルの自動車にも超音波センサーを組み込んでいます。

さまざまなアプリケーションの中で、駐車支援システムが最大のシェアを占め、2024年には41%を占める。これらのシステムは、特に小型車や中級車において、低速での操縦や駐車をより簡単かつ安全にします。他の先進安全システムと比べて価格が手ごろでシンプルなため、さまざまな車両カテゴリーで消費者に選ばれています。

市場は車種別にもセグメント化されており、2024年のシェアは乗用車が77%を占めています。小型車や中型車に超音波を利用した安全機能を搭載する自動車メーカーが増えるにつれて、需要は増加の一途をたどっています。エコノミークラスでも安全性強化を求める規制圧力がこの動向をさらに後押ししています。

中国は、自動車産業が堅調であることと、自動車の安全性とスマートモビリティを推進する政府の取り組みが後押しして、2024年の世界市場で38%の圧倒的シェアを占めました。電気自動車、ハイブリッド車、コネクテッドカー、自律走行車に対する需要の高まりが、超音波の採用をさらに加速させています。

世界自動車用超音波技術市場の主要企業には、現代モービス、ボッシュ、コンチネンタル、マグナ・インターナショナル、NXPセミコンダクターズ、ロックウェル・オートメーション、三菱電機、STマイクロエレクトロニクス、TEコネクティビティ、テキサス・インスツルメンツなどがあります。これらの企業は、戦略的パートナーシップ、継続的な研究開発、製品革新に注力し、統合を推進し、性能を向上させ、高度な自動車安全機能に対する需要の高まりに対応しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品メーカー

- モジュールおよびシステムインテグレーター

- 自動車OEMメーカー

- アフターマーケットサプライヤーおよび設置業者

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーン再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 車両の安全機能とADASの需要の増加

- 自動運転車と半自動運転車の成長

- 政府の規制と安全基準

- 超音波センサーの技術的進歩

- スマートパーキングソリューションに対する消費者の嗜好の高まり

- 業界の潜在的リスク&課題

- 悪条件下でのパフォーマンスの限界

- 範囲と視野が限られている

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:用途別、2021-2034

- 主要動向

- パーキングアシストシステム

- 死角検知

- 衝突回避

- セルフパーキングシステム

- その他

第6章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:技術別、2021-2034

- 主要動向

- 近接検知センサー

- 距離測定センサー

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Autoliv

- Balluff

- Baumer Holding

- Bosch

- Continental

- Elmos Semiconductor

- Garmin

- Honeywell International

- Hyundai Mobis

- Keyence Corporation

- Magna International

- Mitsubishi Electric

- NXP Semiconductors

- Omron Corporation

- Pepperl+Fuchs

- Rockwell Automation

- STMicroelectronics

- TDK Corporation

- TE Connectivity

- Texas Instruments

The Global Automotive Ultrasonic Technologies Market was valued at USD 5.7 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 10 billion by 2034, driven by rising demand for advanced automotive safety features and driver assistance systems like ADAS. As vehicle safety continues to take center stage, the integration of ultrasonic technologies has emerged as a critical enabler of next-generation mobility. Automakers are under growing pressure to meet consumer expectations for safer, smarter, and more connected vehicles. This shift is not limited to premium brands; mid-range and budget-friendly car segments are also rapidly incorporating ultrasonic sensor systems to stay competitive in a market increasingly shaped by safety-conscious consumers.

The continuous evolution of vehicle safety norms, technological advancements, and a push for autonomous capabilities are creating an environment where ultrasonic technologies are not just optional but essential. Automakers, suppliers, and tech innovators are collaborating intensively to bring scalable, cost-effective ultrasonic solutions to the market, ensuring that even entry-level vehicles are equipped with cutting-edge safety systems. The industry is witnessing accelerated R&D investments focused on enhancing sensor accuracy, durability, and affordability, thus widening the scope for mass-market adoption. As governments worldwide introduce stringent vehicle safety frameworks and encourage smart mobility innovations, the automotive ultrasonic technologies market is set to experience sustained growth across both mature and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.7 Billion |

| Forecast Value | $10 Billion |

| CAGR | 6.7% |

Technologies such as parking sensors, collision avoidance, and blind-spot detection are becoming increasingly popular as safety standards tighten. Governments across various regions are actively updating vehicle safety regulations and introducing new compliance frameworks that emphasize the adoption of advanced driver assistance technologies. Regulatory bodies like UNECE, NHTSA, and other global organizations are playing a central role by mandating features such as obstacle detection, pedestrian alert systems, automated braking, and enhanced parking support, all of which rely heavily on ultrasonic sensing capabilities. As safety regulations shift from basic compliance to proactive accident prevention, ultrasonic technologies are securing a pivotal role in automotive safety innovation. Automakers are now embedding ultrasonic sensors not only in premium models but also across mid-range and entry-level vehicles to meet these global safety norms and capture the loyalty of safety-focused consumers.

Among different applications, parking assist systems hold the largest share, accounting for 41% in 2024. These systems make low-speed maneuvering and parking much easier and safer, especially for compact and mid-range vehicles. Their affordability and simplicity compared to other advanced safety systems have made them a go-to choice for consumers across various vehicle categories.

The market is also segmented by vehicle type, with passenger vehicles dominating a 77% share in 2024. Demand continues to climb as more automakers equip compact and mid-sized cars with ultrasonic-enabled safety features. Regulatory pressures requiring enhanced safety even in economy-class models further fuel this trend.

China held a dominant 38% share of the global market in 2024, driven by its robust automotive industry and government initiatives promoting vehicle safety and smart mobility. Growing demand for electric, hybrid, connected, and autonomous vehicles is further accelerating ultrasonic adoption.

Key players in the Global Automotive Ultrasonic Technologies Market include Hyundai Mobis, Bosch, Continental, Magna International, NXP Semiconductors, Rockwell Automation, Mitsubishi Electric, STMicroelectronics, TE Connectivity, and Texas Instruments. These companies are focusing on strategic partnerships, continuous R&D, and product innovation to drive integration, improve performance, and cater to the rising demand for advanced automotive safety features.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Module and system integrators

- 3.2.4 Automotive original equipment manufacturers

- 3.2.5 Aftermarket suppliers and installers

- 3.3 Profit margin analysis

- 3.4 Trump Administration Tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the industry

- 3.4.2.1 Supply-side impact (Raw Materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply Chain Restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (Selling Price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (Raw Materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing demand for vehicle safety features and ADAS

- 3.9.1.2 Growth of autonomous and semi-autonomous vehicles

- 3.9.1.3 Government regulations and safety standards

- 3.9.1.4 Technological advancements in ultrasonic sensors

- 3.9.1.5 Increasing consumer preference for smart parking solutions

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Performance limitations in adverse conditions

- 3.9.2.2 Limited range and field of view

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Park assist system

- 5.3 Blind spot detection

- 5.4 Collision avoidance

- 5.5 Self-parking system

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Proximity detection sensors

- 7.3 Range measurement sensors

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Autoliv

- 10.2 Balluff

- 10.3 Baumer Holding

- 10.4 Bosch

- 10.5 Continental

- 10.6 Elmos Semiconductor

- 10.7 Garmin

- 10.8 Honeywell International

- 10.9 Hyundai Mobis

- 10.10 Keyence Corporation

- 10.11 Magna International

- 10.12 Mitsubishi Electric

- 10.13 NXP Semiconductors

- 10.14 Omron Corporation

- 10.15 Pepperl+Fuchs

- 10.16 Rockwell Automation

- 10.17 STMicroelectronics

- 10.18 TDK Corporation

- 10.19 TE Connectivity

- 10.20 Texas Instruments