|

|

市場調査レポート

商品コード

1699245

自動車用レーダー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Automotive Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 自動車用レーダー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月17日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

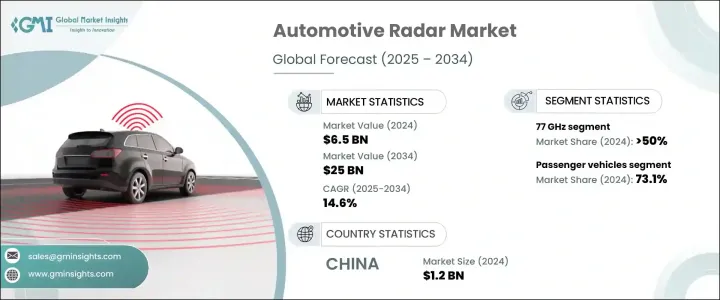

世界の自動車用レーダー市場は、2024年に65億米ドルの評価額に達し、2025年から2034年にかけてCAGR 14.6%で拡大すると予測されています。

この成長は、4Dイメージングレーダー、デジタルビームフォーミング、AI搭載レーダー処理などの技術革新を含む、レーダー技術の継続的な進歩によってもたらされます。こうした機能強化により、レーダーは探知距離、分解能、干渉抑制が向上し、ADAS(先進運転支援システム)や自律走行に効果的なシステムとなっています。

OTA(Over-the-Air)ソフトウェアアップデートにより、車両はレーダー機能のアップグレードを受けられるようになり、普及がさらに加速しています。電気自動車やコネクテッドカーの台頭も需要を後押ししています。レーダー技術は、死角監視、アダプティブ・クルーズ・コントロール、自動駐車などの安全機能で重要な役割を果たしているからです。コネクテッドカーの増加に伴い、業界は単体のレーダーセンサーから、他の自動車、インフラ、クラウドベースのシステムとのリアルタイム通信を容易にする統合車両ネットワークへと移行しつつあります。主要地域の厳しい安全規制は、自動車メーカーがレーダーベースのソリューションを車種に標準装備することをさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 65億米ドル |

| 予測金額 | 250億米ドル |

| CAGR | 14.6% |

周波数別では、24GHz、77GHz、79GHzレーダーに分類されます。77 GHzセグメントは2024年に50%以上の最大市場シェアを占める。77GHzレーダーが広く採用されている背景には、優れた解像度と長い検出距離があります。これらは、車線維持支援や自動緊急ブレーキといった重要な安全機能に不可欠です。欧州と北米の規制と政策により、77GHzレーダーが新たな業界標準として確立され、中国ではすべての新車に高周波レーダー・システムの搭載を義務付ける最近の政策変更により、アジア太平洋地域での採用が加速しています。

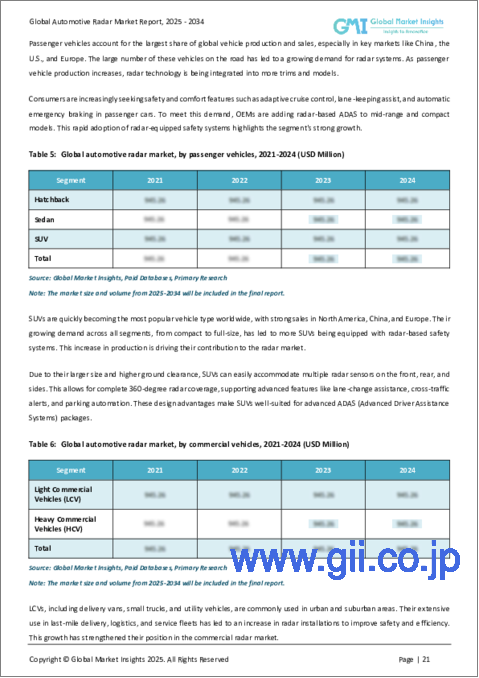

市場は乗用車と商用車に区分され、2024年のシェアは乗用車が73.1%を占める。強化された安全機能に対する消費者の嗜好の高まりが、レーダーベースの運転支援システムの幅広い統合につながっています。死角検出やアダプティブ・クルーズ・コントロールなどの技術は、規制の枠組みや安全性評価システムの更新に後押しされ、個人所有の自動車に標準装備されつつあります。世界中の政府がより厳格なガイドラインを施行し、衝突回避と乗員保護の基準に準拠するために高周波レーダーが必要不可欠となっています。自動車メーカーはレーダー技術を活用して自動運転機能を強化しており、特にレベル2およびレベル3の自律走行車では、ハイウェイ・パイロットや自動車線変更などの機能が高精度レーダー・センサーに依存しています。

範囲は、中距離レーダー(MRR)、短距離レーダー(SRR)、長距離レーダー(LRR)に分けられ、2024年はMRRが優位を占める。その重要性は、自動駐車や衝突回避のために360度の状況認識が必要とされる都市型モビリティで高まっています。都市がスマート交通システムを拡大するにつれて、ライドヘイリング・フリート、電気自動車、ラストマイル・デリバリー・サービスでは、交通量の多い環境での安全なナビゲーションのためにMRRを統合するケースが増えています。レーダーセンサーはリアルタイムの交通監視、予測分析、事故防止に重要な役割を果たすため、高度道路交通システム(ITS)の台頭が採用をさらに促進しています。

また、市場は販売チャネル別にOEMとアフターマーケットに分類されます。2024年には、自動車メーカーがレーダーシステムを新車モデルに直接組み込み続けているため、OEMセグメントが圧倒的なシェアを占めています。大手メーカーはレーダー技術プロバイダーと提携し、高級車と中級車の両方でADAS機能の大規模展開を可能にしています。自動車の安全性に対する消費者の意識が高まるにつれて、自動車メーカーはレーダーベースのソリューションをオプションではなく標準装備とする傾向が強まっています。

アジア太平洋地域は世界の自動車用レーダー市場をリードしており、2024年には中国だけで12億米ドルを占める。自律走行、AI搭載センサー、車両電動化への投資が成長を牽引しており、スマート交通とインテリジェント・ハイウェイ・システムを推進する政府のイニシアティブが強力に支援しています。新エネルギー車(NEV)へのレーダー採用を奨励する好意的な政策により、この地域は自動車レーダー技術革新の最前線に位置付けられています。

目次

第1章 調査手法と調査範囲

- 調査デザイン

- 調査アプローチ

- データ収集方法

- 基本推定と計算

- 基準年の算出

- 市場推計の主要動向

- 予測モデル

- 1次調査と検証

- 市場定義

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- サプライヤーの状況

- チップセットメーカー

- レーダーセンサーメーカー

- ティア1自動車サプライヤー

- AI&ソフトウェア・プロバイダ

- 利益率分析

- テクノロジー&イノベーション情勢

- 特許分析

- 使用事例

- 価格動向

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- ADASと自律走行車に対する需要の高まり

- レーダーシステムの技術的進歩

- 車両の電動化とコネクティビティの増加

- 交通安全に対する消費者の意識の高まり

- 業界の潜在的リスク&課題

- 高コストと複雑な統合

- 干渉と標準化の問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:周波数別、2021年~2034年

- 主要動向

- 24GHzレーダー

- 77GHzレーダー

- 79GHzレーダー

第6章 市場推計・予測:距離別、2021年~2034年

- 主要動向

- 短距離レーダー(SRR)

- 中距離レーダー(MRR)

- 長距離レーダー(LRR)

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV車

- 商用車

- 小型商用車(LCV)

- 大型商用車(HCV)

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- アダプティブ・クルーズ・コントロール(ACC)

- ブラインドスポットディテクション(BSD)

- 前方衝突警報(FCW)

- 車線逸脱警報システム(LDWS)

- 自動緊急ブレーキ(AEB)

- 駐車支援(PA)

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Analog Devices

- Aptiv

- Arbe Robotics

- Bosch

- Continental

- Denso

- Echodyne

- Fujitsu Ten

- Hella

- Hitachi Astemo

- Infineon Technologies

- Mitsubishi Electric

- NXP Semiconductors

- Oculii

- Smart Radar System

- Texas Instruments

- Uhnder

- Valeo

- Veoneer

- ZF Friedrichshafen

The Global Automotive Radar Market reached a valuation of USD 6.5 billion in 2024 and is projected to expand at a CAGR of 14.6% from 2025 to 2034. This growth is driven by the continuous advancement of radar technology, including innovations such as 4D imaging radar, digital beamforming, and AI-powered radar processing. These enhancements are improving range, resolution, and interference suppression, making radar systems more effective for advanced driver assistance systems (ADAS) and autonomous driving.

Over-the-air (OTA) software updates are allowing vehicles to receive radar capability upgrades, further accelerating adoption. The rise of electric and connected vehicles is also fueling demand, as radar technology plays a crucial role in safety features like blind spot monitoring, adaptive cruise control, and automated parking. With the increasing number of connected vehicles, the industry is transitioning from standalone radar sensors to integrated vehicle networks that facilitate real-time communication with other cars, infrastructure, and cloud-based systems. Strict safety regulations across key regions are further pushing automakers to implement radar-based solutions as standard features in their models.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $25 Billion |

| CAGR | 14.6% |

By frequency, the market is categorized into 24 GHz, 77 GHz, and 79 GHz radar. The 77 GHz segment held the largest market share of over 50% in 2024. Its widespread adoption is driven by its superior resolution and longer detection range, which are essential for critical safety features like lane-keeping assistance and automated emergency braking. Regulations in Europe and North America have established 77 GHz radar as the new industry standard, and recent policy changes in China mandating high-frequency radar systems in all new cars are accelerating adoption in the Asia Pacific region.

The market is segmented into passenger and commercial vehicles, with passenger cars holding a 73.1% share in 2024. Growing consumer preference for enhanced safety features has led to the widespread integration of radar-based driver assistance systems. Technologies such as blind spot detection and adaptive cruise control are becoming standard in personal vehicles, driven by regulatory frameworks and updated safety rating systems. Governments worldwide are enforcing stricter guidelines, making high-frequency radar a necessity for compliance with crash avoidance and occupant protection standards. Automakers are leveraging radar technology to enhance self-driving capabilities, particularly in Level 2 and Level 3 autonomous vehicles, where features like highway pilot and automated lane changes rely on high-precision radar sensors.

In terms of range, the market is divided into medium-range radar (MRR), short-range radar (SRR), and long-range radar (LRR), with MRR dominating in 2024. Its importance is growing in urban mobility, where self-parking and collision avoidance require 360-degree situational awareness. As cities expand smart transportation systems, ride-hailing fleets, electric vehicles, and last-mile delivery services are increasingly integrating MRR for safe navigation in high-traffic environments. The rise of intelligent transportation systems (ITS) is further driving adoption, as radar sensors play a key role in real-time traffic monitoring, predictive analytics, and accident prevention.

The market is also classified by sales channel into OEMs and aftermarket. In 2024, the OEM segment held the dominant share as automakers continued integrating radar systems directly into new vehicle models. Leading manufacturers are collaborating with radar technology providers to enable large-scale deployment of ADAS features in both luxury and mid-range vehicles. As consumer awareness of vehicle safety grows, automakers are increasingly including radar-based solutions as standard rather than optional features.

The Asia Pacific region leads the global automotive radar market, with China alone accounting for USD 1.2 billion in 2024. Investments in autonomous driving, AI-powered sensors, and vehicle electrification are driving growth, with strong support from government initiatives promoting smart transportation and intelligent highway systems. Favorable policies encouraging radar adoption in new energy vehicles (NEVs) are positioning the region at the forefront of innovation in automotive radar technology.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Chipset providers

- 3.2.2 Radar sensor producers

- 3.2.3 Tier-1 auto suppliers

- 3.2.4 AI & software providers

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Use cases

- 3.7 Price trend

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for ADAS and autonomous vehicles

- 3.10.1.2 Technological advancements in radar systems

- 3.10.1.3 Increasing vehicle electrification and connectivity

- 3.10.1.4 Growing consumer awareness of road safety

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High costs and complex integration

- 3.10.2.2 Interference and standardization issues

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Frequency, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 24 GHz radar

- 5.3 77 GHz radar

- 5.4 79 GHz radar

Chapter 6 Market Estimates & Forecast, By Range, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Short-Range radar(SRR)

- 6.3 Medium-Range radar(MRR)

- 6.4 Long-Range radar(LRR)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Adaptive Cruise Control (ACC)

- 9.3 Blind Spot Detection (BSD)

- 9.4 Forward Collision Warning (FCW)

- 9.5 Lane Departure Warning System (LDWS)

- 9.6 Automatic Emergency Braking (AEB)

- 9.7 Parking Assistance (PA)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Analog Devices

- 11.2 Aptiv

- 11.3 Arbe Robotics

- 11.4 Bosch

- 11.5 Continental

- 11.6 Denso

- 11.7 Echodyne

- 11.8 Fujitsu Ten

- 11.9 Hella

- 11.10 Hitachi Astemo

- 11.11 Infineon Technologies

- 11.12 Mitsubishi Electric

- 11.13 NXP Semiconductors

- 11.14 Oculii

- 11.15 Smart Radar System

- 11.16 Texas Instruments

- 11.17 Uhnder

- 11.18 Valeo

- 11.19 Veoneer

- 11.20 ZF Friedrichshafen