乳製品ブレンドの市場機会、成長促進要因、業界動向分析、2025年~2034年予測

Dairy Blends Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 300 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740915

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

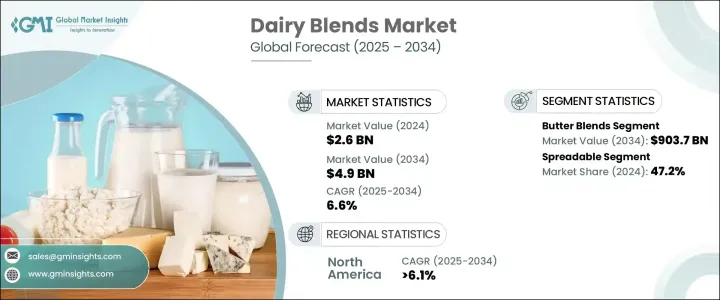

乳製品ブレンドの世界市場規模は、2024年には26億米ドルとなり、現代の消費パターンに対応した多機能食品素材に対する需要の高まりに後押しされ、CAGR 6.6%で成長し、2034年には49億米ドルに達すると予測されています。

今日の消費者は、味、栄養、利便性のバランスが取れた食品をますます求めるようになっており、乳製品ブレンドはそのすべての面で成果を上げています。この変化は、健康への意識の高まり、すぐに使える製品を好む忙しいライフスタイル、持続可能でありながら贅沢な食体験への欲求によってもたらされています。乳製品ブレンドは、その完璧な中間点を突いています。それは、伝統的な乳製品の豊かな感覚的魅力に、機能性と健康上の利点を加えたものです。乳製品ブレンドは、口当たりの良さ、保存期間の長さ、熱安定性、展延性の向上を提供します。これらの特性により、乳製品ブレンドは冷凍食品や焼き菓子からソースやスナックに至るまで、幅広い食品用途に理想的です。世界の食の嗜好の進化に伴い、消費者は毎日の食事に取り入れやすく、栄養プロファイルを調整できるブレンドに注目しています。

乳製品ブレンドは、技術の大きな進歩により急速に進化しています。ホモジナイゼーション、マイクロカプセル化、高精度ブレンドの画期的な進歩により、メーカーは特定の健康目標や食事要件をターゲットにしたブレンドを作ることができるようになりました。脂肪分を低くしたり、ビタミンを強化したり、子どもやアスリート、高齢者向けにブレンドをカスタマイズしたりと、業界は現在、精密な栄養を提供するためのツールを手にしています。ウェルネスへの注目はかつてないほど高まっており、こうしたオーダーメイドのソリューションは、風味や食感を犠牲にすることなく、消費者が個人の健康目標を達成するのに役立っています。世界・サプライチェーンの多様化も促進要因のひとつです。企業は現在、調達と生産においてより機敏になっており、原材料価格の変動、貿易力学、気候関連の課題に迅速に対応できるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 26億米ドル |

| 予測金額 | 49億米ドル |

| CAGR | 6.6% |

市場は、精製クリーム、バター、チーズ、ヨーグルト、その他の特殊ブレンドにタイプ別に区分されます。中でもバターブレンドは強いインパクトを与えており、CAGR 6.5%の成長率で2034年までに9億370万米ドルに達すると予測されます。これらのブレンドは、その安定した食感、風味、製品配合を安定させる能力から、食品加工分野で高く評価されており、特に焼き菓子や包装食品に適しています。

形状に関しては、乳製品ブレンドは粉末、液体、スプレッド製品に分類されます。スプレッド可能なブレンドが47.2%の市場シェアを占め、2034年までに12億米ドルに達し、CAGR 6.9%で成長すると予測されています。その使いやすさ、ペースの速いライフスタイルへの適合性、直接スプレッドからソースやミールキットまであらゆるものへの汎用性により、消費者の人気を集めています。

北米の乳製品ブレンド市場は、2025年から2034年にかけてCAGR 6.1%で成長すると予測されています。大豆、オート麦、アーモンドの要素を取り入れたブレンドは、従来の乳製品に代わるクリーンラベルの機能性食品を求める人々の間で人気を集めています。風味を高め、栄養豊富で保存性の高い食品に対する需要の高まりが、市場の成長をさらに後押ししています。

Cargill、Agropur、Friesland Campina、Kerry Group、Fonterra、Dohler、AFPなどの主要企業は、よりクリーンなラベルとより高い栄養価の提供を目指した研究開発投資で限界に課題しています。戦略的提携や持続可能性に焦点を当てた取り組みを通じて、これらの企業は、責任ある調達や環境負荷の低減に対する消費者の期待に応えながら、世界の足跡を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国のみに提供されます

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 消費者は、脂肪とコレステロール含有量が低い乳製品ブレンドを好みます

- 機能性食品の需要増加

- 乳製品ブレンドは適切な代替案を提案する

- 業界の潜在的リスク&課題

- 厳格な表示および成分に関する法律により、市場の拡大が制限される可能性があります

- 購入者の中には、ブレンドは純粋な乳製品よりも品質が低いと考える人もいます

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 乳製品のクリームブレンド

- バターブレンド

- ヨーグルトブレンド

- チーズブレンド

- その他のブレンド

第6章 市場推計・予測:形態別、2021-2034

- 主要動向

- 塗り広げられる

- 液体

- 粉

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- ベーカリー&菓子類

- 乳製品と冷凍デザート

- 飲み物

- 栄養・機能性食品

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Kerry Group plc

- FrieslandCampina

- Cargill、Incorporated

- Fonterra Co-operative Group Limited

- Dohler GmbH

- Agropur

- AFP advanced food products llc

- Cape Food Ingredients

- Intermix Australia Pty Ltd.

- Spectrum Organics Products、LLC

目次

The Global Dairy Blends Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 4.9 billion by 2034, fueled by the rising demand for multi-functional food ingredients that meet modern consumption patterns. Consumers today are increasingly looking for food options that offer a balance between taste, nutrition, and convenience, and dairy blends deliver on all fronts. This shift is being driven by a growing awareness of health, a busy lifestyle that favors ready-to-use products, and a desire for sustainable yet indulgent eating experiences. Dairy blends strike that perfect middle ground-they combine the rich sensory appeal of traditional dairy with added functionality and health benefits. These products provide improved mouthfeel, longer shelf life, thermal stability, and enhanced spreadability. These attributes make dairy blends ideal for a wide range of food applications, from frozen and baked goods to sauces and snacks. As global food preferences evolve, consumers are turning to blends that are easy to incorporate into their daily meals while offering tailored nutritional profiles.

Dairy blends are evolving quickly, thanks to major advancements in technology. Breakthroughs in homogenization, microencapsulation, and precision blending are allowing manufacturers to create blends that target specific health goals or dietary requirements. Whether it's lowering fat content, enriching with vitamins, or customizing blends for children, athletes, or the elderly, the industry now has the tools to deliver precision nutrition. The focus on wellness is stronger than ever, and these tailored solutions are helping consumers meet personal health targets without giving up flavor or texture. Global supply chain diversification is another driving factor. Companies are now more agile in their sourcing and production, helping them adapt quickly to fluctuations in raw material prices, trade dynamics, and climate-related challenges.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 6.6% |

The market is segmented by type into refined creams, butter, cheese, yogurt, and other specialty blends. Among these, butter blends are making a strong impact and are expected to reach USD 903.7 million by 2034, growing at a CAGR of 6.5%. These blends are highly valued in the food processing sector for their consistent texture, flavor, and ability to stabilize product formulations, particularly in baked and packaged foods.

In terms of form, dairy blends are categorized as powders, liquids, and spreadable products. Spreadable blends dominate with a 47.2% market share and are projected to hit USD 1.2 billion by 2034, growing at a CAGR of 6.9%. Their ease of use, compatibility with fast-paced lifestyles, and versatility in everything from direct spreads to sauces and meal kits make them a consumer favorite.

North America's dairy blends market is forecasted to grow at a CAGR of 6.1% between 2025 and 2034, supported by the region's shift toward health-conscious, plant-forward diets. Blends incorporating soy, oat, or almond elements are gaining traction among those seeking clean-label, functional alternatives to traditional dairy. The rising demand for flavor-enhancing, nutrient-rich, and shelf-stable foods further boosts market growth.

Leading companies such as Cargill, Agropur, Friesland Campina, Kerry Group, Fonterra, Dohler, and AFP are pushing the envelope with R&D investments aimed at delivering cleaner labels and higher nutritional value. Through strategic collaborations and sustainability-focused initiatives, these players are expanding their global footprint while meeting consumer expectations for responsible sourcing and reduced environmental impact.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: The above trade statistics will be provided for key countries only

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Consumers prefer dairy blends for lower fat and cholesterol content.

- 3.8.1.2 Growing demand for functional foods

- 3.8.1.3 Dairy blends offer a suitable alternative

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Strict labeling and composition laws can limit market expansion.

- 3.8.2.2 Some buyers see blends as lower quality than pure dairy.

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dairy cream blends

- 5.3 Butter blends

- 5.4 Yogurt blends

- 5.5 Cheese blends

- 5.6 Other blends

Chapter 6 Market Estimates & Forecast, By Form, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Spreadable

- 6.3 Liquid

- 6.4 Powder

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery & confectionery

- 7.3 Dairy & frozen desserts

- 7.4 Beverages

- 7.5 Nutritional & functional foods

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Kerry Group plc

- 9.2 FrieslandCampina

- 9.3 Cargill, Incorporated

- 9.4 Fonterra Co-operative Group Limited

- 9.5 Dohler GmbH

- 9.6 Agropur

- 9.7 AFP advanced food products llc

- 9.8 Cape Food Ingredients

- 9.9 Intermix Australia Pty Ltd.

- 9.10 Spectrum Organics Products, LLC

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 300 Pages

- 納期

- 2~3営業日