|

市場調査レポート

商品コード

1740899

フレキシブル保護包装市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Flexible Protective Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| フレキシブル保護包装市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月22日

発行: Global Market Insights Inc.

ページ情報: 英文 189 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

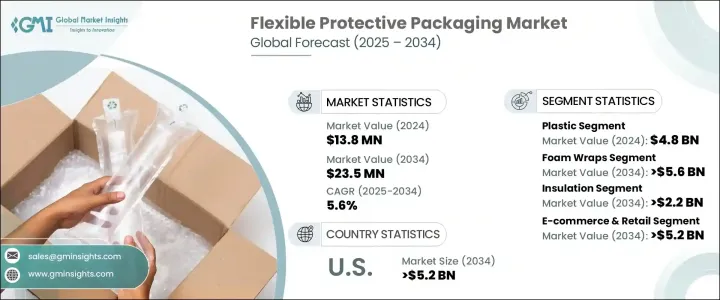

フレキシブル保護包装の世界市場は、2024年には138億米ドルと評価され、eコマース分野の拡大とラストマイル配送ネットワークの進歩により、CAGR 5.6%で成長し、2034年には235億米ドルに達すると予測されています。

世界中の産業が、コスト効率と高い製品保護を提供する、軽量で耐久性があり持続可能な代替包装に傾倒しているため、市場は急速な変化を経験しています。オンラインショッピングプラットフォームの浸透により、商品の保管、出荷、配送方法が変化し、輸送中の商品を緩衝するだけでなく、さまざまな製品の形状やサイズに容易に適応する包装に対するニーズが高まっています。消費者は、環境への影響を最小限に抑えながら、より迅速な配送を求めており、フレキシブル保護包装は、性能と持続可能性のバランスを求める企業にとって好ましいソリューションとなっています。リサイクル可能、堆肥化可能、生分解性パッケージの革新は着実に進んでおり、ブランドは規制基準や消費者の期待に応えています。小売業者がオムニチャネルでのフルフィルメントを優先する中、フレキシブル包装は戦略的な優位性を提供しています。

プラスチック廃棄物の削減と環境に優しい慣行の推進に対する規制圧力の高まりは、マーケットの主要な成長触媒となっています。多くの企業が、硬くて頑丈なフォーマットから、カスタマイズが容易で低コストで出荷できる、よりスマートで柔軟なオプションへと積極的にシフトしています。新興経済圏、特にアジア太平洋地域では、こうした動向はさらに顕著であり、オンライン小売の急増により、保護性と経済性を兼ね備えたパッケージへの需要が加速しています。気泡緩衝材、発泡インサート、パッド入りメーラー、エアピローなどのフレキシブル保護包装フォーマットは、より少ない材料消費で強力な緩衝性を提供するため、人気を集めています。省スペースという特性は、物流コストを押し下げるだけでなく、輸送時の二酸化炭素排出量の削減にも貢献しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 138億米ドル |

| 予測金額 | 235億米ドル |

| CAGR | 5.6% |

米国以前の通商政権下で導入された継続的な関税政策は、輸入原材料に依存する国内メーカーにコスト圧力を加えました。これらの関税は、企業にサプライチェーンの再考を促し、調達戦略の転換や地域の製造拠点への投資につながりました。そうすることで、メーカー各社はコスト効率を最適化しつつ、回復力を高めています。競合情勢において、競合情勢は重要な役割を担っています。材料使用量を削減し、寸法出荷コストを下げ、製品ラインを容易に拡張できるようにすることで、企業は進化する市場において競争優位に立つことができます。

材料の種類の中では、プラスチックが引き続きフレキシブル保護包装の分野を支配しており、2024年には48億米ドルを生み出します。ポリエチレン、ポリプロピレン、ポリスチレンなどの一般的なプラスチック樹脂は、低コスト、耐久性、高い耐衝撃性により、依然として人気が高いです。これらの材料は、エアピロー、発泡インサート、プチプチなどの包装ソリューションに広く使用されており、長距離輸送中の壊れやすい品物の保護に不可欠です。特に家電や化粧品などの分野でのデジタル小売の台頭により、これらの軽量で高性能な素材への需要が減速する兆しはないです。

フォームラップ分野は2034年までに56億米ドルを生み出すと予測されており、フレキシブル保護包装で最も急成長している分野の一つとなっています。フォームラップは、その軽量性と強力なクッション性により広く使用されており、輸送中のデリケートな物品の保護に最適です。不規則な形状にもフィットするため、かさばることなく緩衝性を保つことができます。医療機器、電子機器、高級ガラス製品などの精密機器を扱う業界では、破損、返品、顧客不満足などのリスクを軽減するため、発泡ラップへの依存度が高まっています。

米国では、強力なeコマース・エコシステムと持続可能な包装を重視する国の高まりに後押しされ、フレキシブル保護包装市場は2034年までに52億米ドルを生み出すと予測されています。オンラインショッピングの習慣が強まるにつれ、企業は食品、医薬品、消費財などの業界全体の需要を満たすために、生分解性ラップ、紙ベースの緩衝材、リサイクル可能なポリメーラーを急速に採用しています。これらの分野では、製品の完全性を保護するだけでなく、環境意識の高い価値観やコンプライアンス要件に沿ったパッケージング・ソリューションが求められています。

競争力を維持するため、Amcor、Smurfit Kappa、Mondi、Sealed Air、Pregisなどの業界大手は、研究開発、持続可能性の革新、カスタマイズされたパッケージングシステムに多額の投資を行っています。また、オムニチャネル小売モデルに対応し、複雑なロジスティクス需要に対応するため、各地域の製造拠点を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- eコマースの拡大

- 持続可能性と規制遵守

- コストと運用効率

- 材料科学の進歩

- 家電製品と生鮮食品の成長

- 業界の潜在的リスク&課題

- リサイクルインフラのギャップ

- 原材料価格の変動

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材質別、2021-2034

- プラスチック

- 紙と板紙

- フォーム

- アルミホイル

第6章 市場推計・予測:製品タイプ別、2021-2034

- エアクッション

- プチプチ

- フォームラップ

- メーラー

- シュリンクラップ

- ストレッチフィルム

- その他

第7章 市場推計・予測:機能別、2021-2034

- 隙間埋め

- ブロッキングとブレース

- ラッピング

- 絶縁

- クッション

- 表面保護

第8章 市場推計・予測:最終用途別、2021-2034

- eコマースと小売

- 食品と飲料

- 医薬品・ヘルスケア

- 消費者

- 自動車

- 産業

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Sealed Air Corporation

- Pregis LLC

- Smurfit Kappa Group

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Sonoco Products Company

- ProAmpac LLC

- Storopack Hans Reichenecker GmbH

- DS Smith Plc

- Winpak Ltd.

- Mondi Flexible Packaging

- Rengo Co.、Ltd.

- AptarGroup、Inc.

- Toray Plastics(America)、Inc.

- Schur Flexibles Group

The Global Flexible Protective Packaging Market was valued at USD 13.8 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 23.5 billion by 2034, driven by the expanding e-commerce sector and advancements in last-mile delivery networks. The market is experiencing a rapid shift as industries across the globe lean toward lightweight, durable, and sustainable packaging alternatives that offer cost-efficiency and high product protection. The growing penetration of online shopping platforms has transformed how goods are stored, shipped, and delivered-fueling a strong need for packaging that not only cushions items in transit but also adapts easily to varying product shapes and sizes. Consumers are demanding faster deliveries with minimal environmental impact, making flexible protective packaging a preferred solution for businesses looking to strike a balance between performance and sustainability. Innovations in recyclable, compostable, and biodegradable packaging are emerging at a steady pace, helping brands meet regulatory benchmarks and consumer expectations alike. As retailers prioritize omnichannel fulfillment, flexible packaging is offering a strategic advantage-reducing shipping weights, limiting waste, and enhancing overall operational agility.

Rising regulatory pressure on reducing plastic waste and promoting eco-friendly practices has become a key growth catalyst for the market. Many businesses are proactively shifting from rigid, heavy-duty formats to smarter, flexible options that can be easily customized and shipped at lower costs. Across emerging economies-especially in Asia-Pacific-these trends are even more pronounced, where the spike in online retail activity is accelerating demand for packaging that is both protective and economical. Flexible protective packaging formats such as bubble wraps, foam inserts, padded mailers, and air pillows are gaining traction because they offer strong cushioning with less material consumption. Their space-saving nature not only drives down logistics costs but also helps reduce carbon emissions during transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.8 billion |

| Forecast Value | $23.5 billion |

| CAGR | 5.6% |

Ongoing tariff policies introduced during earlier U.S. trade administrations have added cost pressures on domestic manufacturers relying on imported raw materials. These tariffs have prompted companies to rethink their supply chains, leading to a shift in sourcing strategies and investments in regional manufacturing hubs. In doing so, manufacturers are enhancing their resilience while optimizing cost-efficiency. Flexible protective packaging plays a vital role in this landscape-it helps reduce material usage, lowers dimensional shipping costs, and allows easy scalability across product lines, giving businesses a competitive edge in an evolving market.

Among material types, plastic continues to dominate the flexible protective packaging space, generating USD 4.8 billion in 2024. Common plastic resins such as polyethylene, polypropylene, and polystyrene remain popular due to their low cost, durability, and high impact resistance. These materials are extensively used in packaging solutions like air pillows, foam inserts, and bubble wraps, which are essential for protecting fragile items during long-haul shipments. With the rise of digital retail, particularly in sectors like consumer electronics and cosmetics, the demand for these lightweight, high-performance materials shows no signs of slowing down.

The foam wraps segment is projected to generate USD 5.6 billion by 2034, making it one of the fastest-growing areas in flexible protective packaging. Foam wraps are widely used due to their lightweight nature and strong cushioning properties, which are ideal for safeguarding delicate items during transit. These wraps effortlessly mold to irregular shapes, ensuring that items remain securely cushioned without adding excessive bulk. Industries handling precision equipment-such as medical devices, electronics, and luxury glassware-are increasingly depending on foam wraps to reduce the risk of breakage, returns, and customer dissatisfaction.

In the U.S., the flexible protective packaging market is forecasted to generate USD 5.2 billion by 2034, fueled by a strong e-commerce ecosystem and the nation's growing emphasis on sustainable packaging. As online shopping habits intensify, businesses are rapidly adopting biodegradable wraps, paper-based cushioning, and recyclable poly mailers to meet demand across industries such as food, pharmaceuticals, and consumer goods. These sectors require packaging solutions that not only protect product integrity but also align with eco-conscious values and compliance requirements.

To maintain a competitive edge, industry leaders like Amcor, Smurfit Kappa, Mondi, Sealed Air, and Pregis are heavily investing in R&D, sustainability innovation, and customized packaging systems. They are also expanding their regional manufacturing footprint to better serve omnichannel retail models and address complex logistics demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 E-commerce expansion

- 3.3.1.2 Sustainability and regulatory compliance

- 3.3.1.3 Cost and operational efficiency

- 3.3.1.4 Advancements in material science

- 3.3.1.5 Growth in consumer electronics and perishables

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Recycling infrastructure gaps

- 3.3.2.2 Volatility in raw material prices

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Million and Units)

- 5.1 Plastic

- 5.2 Paper & paperboard

- 5.3 Foam

- 5.4 Aluminum foil

Chapter 6 Market estimates & forecast, By Product Type, 2021 - 2034 (USD Billion and Units)

- 6.1 Air cushions

- 6.2 Bubble wraps

- 6.3 Foam wraps

- 6.4 Mailers

- 6.5 Shrink wraps

- 6.6 Stretch films

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Function, 2021 - 2034 (USD Billion and Units)

- 7.1 Void Fill

- 7.2 Blocking & bracing

- 7.3 Wrapping

- 7.4 Insulation

- 7.5 Cushioning

- 7.6 Surface protection

Chapter 8 Market estimates & forecast, By End Use, 2021 - 2034 (USD Billion and Units)

- 8.1 E-commerce & retail

- 8.2 Food & beverages

- 8.3 Pharmaceuticals & healthcare

- 8.4 Consumer

- 8.5 Automotive

- 8.6 Industrial

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion and Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Sealed Air Corporation

- 10.2 Pregis LLC

- 10.3 Smurfit Kappa Group

- 10.4 Amcor plc

- 10.5 Mondi Group

- 10.6 Huhtamaki Oyj

- 10.7 Sonoco Products Company

- 10.8 ProAmpac LLC

- 10.9 Storopack Hans Reichenecker GmbH

- 10.10 DS Smith Plc

- 10.11 Winpak Ltd.

- 10.12 Mondi Flexible Packaging

- 10.13 Rengo Co., Ltd.

- 10.14 AptarGroup, Inc.

- 10.15 Toray Plastics (America), Inc.

- 10.16 Schur Flexibles Group