|

市場調査レポート

商品コード

1740836

複合繊維製造装置市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Composite Textile Production Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 複合繊維製造装置市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

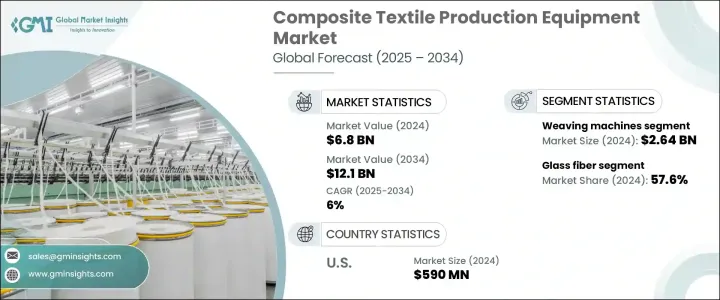

複合繊維製造装置の世界市場規模は、2024年に68億米ドルとなり、CAGR 6%で成長し、2034年には121億米ドルに達すると予測されています。

複数の産業で燃費の向上と構造重量の軽減への注目が高まっていることが、複合繊維の需要を促進しており、ひいては生産設備の成長にも拍車をかけています。航空宇宙、自動車、風力エネルギー、スポーツなどの産業は、その卓越した強度対重量比と耐腐食性により、これらの先端素材を採用しています。これらの特性は、メーカーが性能を高め、エネルギー効率を改善し、排出ガスを削減するのに役立っています。運輸や航空などの分野では、より軽い素材が燃費の向上や二酸化炭素排出量の削減に直結するため、複合繊維は現代の製造業において重要な要素となっています。これらの素材を製造するための機器もまた急速に進化しており、生産性と精度を向上させる自動化やスマート技術が統合されています。

最新の複合繊維機械には、CNC機能と自動化されたロボット工学がますます組み込まれています。これらのシステムは人的ミスを減らし、生産効率を高め、一貫した製品品質を維持します。また、異なる織物パターンや織物構造間の迅速な移行をサポートすることで、メーカーは生産ニーズの変化に迅速に対応することができます。この俊敏性は、カスタマイズされた複雑な複合材料の需要が増加し続ける中で、特に重要です。産業界が精度と拡張性を優先する中、自動化されたソリューションは市場の期待に応えるために不可欠になっています。リアルタイムでオペレーションを微調整できるこれらのシステムは、一貫性や効率を犠牲にすることなく生産を拡大する上で欠かせないものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 68億米ドル |

| 予測金額 | 121億米ドル |

| CAGR | 6% |

機器のタイプ別に見ると、市場は織機、編機、編組機、プリプレグ機、その他に区分されます。織機は2024年に26億4,000万米ドルの売上を占め、支配的なセグメントとして浮上し、2034年まで約6.4%のCAGRで成長すると予測されます。製織は、糸を高強度で構造的に安定した織物に変える能力があるため、複合繊維生産の中核工程の1つであり続けています。ニットや不織布の製法に比べ、織物は耐久性と耐ストレス性に優れ、要求の厳しい用途に理想的です。カーボン、ガラス、アラミドなどのマテリアルを使用した複雑な繊維交絡パターンを扱うことができるため、性能が重要視される環境での重要性が増しています。特に高性能の複合繊維を生産するためには、精度とスピードを保証する高度な織機へのニーズが高まっています。

また、市場は繊維の種類によって炭素繊維、ガラス繊維、アラミド繊維、天然繊維、その他に分類されます。2024年にはガラス繊維がこの分野を支配し、市場シェアの57.6%を占める。ガラス繊維は、手頃な価格と幅広い用途で信頼できる性能により、広く使用され続けています。高価な繊維とは異なり、ガラス繊維はコスト効率、強度、耐久性の理想的な組み合わせを提供します。自動車、海洋、建築などの分野における大規模生産に適しています。また、織物、ニット、不織布など、さまざまな繊維加工技術への適応性も魅力です。メーカーは、既存の機械との互換性により、特殊な生産設備の必要性を減らし、設備投資を最小限に抑えられるという利点があります。

最終用途の観点から見ると、2024年には輸送セクターが市場をリードしており、2034年までその主導権を維持すると予想されます。軽量・高強度複合材料に対する需要は、構造効率が燃費と安全性能の向上に直結するこの産業で特に高いです。自動車、列車、船舶は繊維強化織物をより広範囲に採用するようになっており、耐食性とエネルギー吸収性を備えた材料が好まれています。排出ガス規制が世界的に強化されるにつれて、運輸部門のメーカーは複合材料と、それを大規模に生産するのに必要な特殊機械にますます目を向けるようになっています。

北米では、米国が2024年の評価額5,900億米ドルで地域市場をリードし、CAGR5.9%で成長しました。防衛、自動車、航空宇宙分野での軽量複合材用途の増加が、繊維生産技術の国内技術革新を引き続き促進しています。自動化、持続可能性、デジタル化への投資が、最小限のエネルギー使用と廃棄物削減のために設計された次世代装置の開発を支えています。

業界各社は、無溶剤システムや精密ベースの繊維配置など、エネルギー効率の高いプロセスに注力しています。また、投入資材のリサイクル性を高め、環境に優しい素材を統合する取り組みも行われています。透明性、トレーサビリティ、国際的な環境基準への準拠が重視されるようになり、メーカーの購買決定に影響を与え、市場はよりクリーンで責任ある生産方法へと向かっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 貿易分析

- 利益率分析

- 技術概要

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 軽量で燃費の良い素材の需要の高まり

- 自動化とスマートテクノロジーの進歩

- 航空宇宙および防衛用途の拡大

- 再生可能エネルギー分野での利用増加

- 業界の潜在的リスク&課題

- 初期資本投資額が高め

- 環境と規制の圧力

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:機器種別、2021-2034

- 主要動向

- 織機

- 編み機

- 編組機

- プリプレグマシン

- その他

第6章 市場推計・予測:繊維の種類別、2021-2034

- 主要動向

- 炭素繊維

- ガラス繊維

- アラミド繊維

- 天然繊維

- その他

第7章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- 航空宇宙および防衛

- 交通機関

- 工事

- スポーツとレジャー

- 医学

- その他

第8章 市場推計・予測:技術レベル別、2021-2034

- 主要動向

- 手動機器

- 半自動システム

- 完全自動化された機器

第9章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接

- 間接的

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Changzhou Run Feng Yuan Textile Machinery Manufacturing Co.、Ltd.

- Cygnet Texkimp

- Dashmesh Jacquard And Powerloom Pvt. Ltd.

- Griffith Textile Machines

- Hangzhou Dengte Textile Machinery Co.、Ltd

- IMESA S.r.l.

- Itema Group

- KARL MAYER Holding SE &CO2 KG

- Lamiflex S.p.A.

- Lindauer DORNIER GmbH

- McCO2 Machinery Company、Inc.

- Optima3D Ltd

- Sino Textile Machinery

- Trutzschler Nonwovens GmbH

- TSUDAKOMA Europe s.r.l.

The Global Composite Textile Production Equipment Market was valued at USD 6.8 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 12.1 billion by 2034. Increasing focus on improving fuel efficiency and reducing structural weight across multiple industries is driving the demand for composite textiles, which, in turn, fuels the growth of production equipment. Industries like aerospace, automotive, wind energy, and sports are adopting these advanced materials due to their exceptional strength-to-weight ratio and resistance to corrosion. These characteristics help manufacturers enhance performance, improve energy efficiency, and reduce emissions. In sectors like transportation and aviation, lighter materials are directly tied to better fuel economy and lower carbon emissions, making composite textiles a critical component in modern manufacturing. The equipment used to manufacture these materials is also evolving rapidly, integrating automation and smart technologies that improve productivity and precision.

Modern composite textile machinery increasingly incorporates CNC capabilities and automated robotics. These systems reduce human error, boost output efficiency, and maintain consistent product quality. They also support quick transitions between different textile patterns or structures, enabling manufacturers to adapt quickly to shifting production needs. This agility is especially important as demand for customized and complex composite materials continues to rise. As industries prioritize precision and scalability, automated solutions are becoming essential for meeting market expectations. The ability to fine-tune operations in real-time makes these systems vital in scaling production without sacrificing consistency or efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.8 Billion |

| Forecast Value | $12.1 Billion |

| CAGR | 6% |

In terms of equipment type, the market is segmented into weaving machines, knitting machines, braiding machines, prepreg machines, and others. Weaving machines emerged as the dominant segment in 2024, accounting for USD 2.64 billion in revenue and projected to grow at a CAGR of approximately 6.4% through 2034. Weaving remains one of the core processes in composite textile production due to its ability to transform yarn into high-strength, structurally stable fabric. Compared to knitted or nonwoven methods, woven textiles offer better durability and stress resistance, making them ideal for demanding applications. Their capability to handle complex fiber interlacing patterns using materials like carbon, glass, and aramid reinforces their importance in performance-critical environments. The need for advanced weaving equipment that ensures accuracy and speed is growing, particularly for producing high-performance composite fabrics.

The market is also categorized based on fiber type into carbon fiber, glass fiber, aramid fiber, natural fibers, and others. Glass fiber dominated this segment in 2024, representing 57.6% of the market share. It continues to be widely used due to its affordability and reliable performance across a range of applications. Unlike more expensive fibers, glass fiber offers an ideal combination of cost-efficiency, strength, and endurance. It suits large-scale production in sectors such as automotive, marine, and construction. Its adaptability to various textile processing techniques-such as weaving, knitting, and nonwoven formats-adds to its appeal. Manufacturers benefit from its compatibility with existing machinery, reducing the need for specialized production equipment and minimizing capital investment.

From an end-use perspective, the transportation sector led the market in 2024 and is expected to maintain its leadership through 2034. Demand for lightweight, high-strength composite materials is particularly high in this industry, where structural efficiency translates directly into improved fuel economy and safety performance. Vehicles, trains, and ships are incorporating fiber-reinforced textiles more extensively, favoring materials that offer corrosion resistance and energy absorption. As emissions regulations tighten globally, manufacturers in the transportation sector are increasingly turning to composite materials and the specialized machinery required to produce them at scale.

In North America, the United States led the regional market with a valuation of USD 590 billion in 2024, growing at a CAGR of 5.9%. The rise in lightweight composite applications across defense, automotive, and aerospace sectors continues to drive domestic innovation in textile production technologies. Investments in automation, sustainability, and digitalization are supporting the development of next-generation equipment designed for minimal energy use and waste reduction.

Industry players are focusing on energy-efficient processes such as solvent-free systems and precision-based fiber placement. Efforts are also being made to enhance the recyclability of inputs and integrate eco-friendly materials. Growing emphasis on transparency, traceability, and compliance with international environmental standards is influencing the purchasing decisions of manufacturers, pushing the market toward cleaner, more responsible production methods.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.5 Demand-side impact (selling price)

- 3.2.2.6 Price transmission to end markets

- 3.2.2.7 Market share dynamics

- 3.2.2.8 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Trade Analysis

- 3.5 Profit margin analysis

- 3.6 Technological overview

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising demand for lightweight and fuel-efficient materials

- 3.9.1.2 Advancements in automation and smart technologies

- 3.9.1.3 Expansion in aerospace and defense applications

- 3.9.1.4 Increasing use in renewable energy sector

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial capital investment

- 3.9.2.2 Environmental and regulatory pressures

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Weaving machines

- 5.3 Knitting machines

- 5.4 Braiding machines

- 5.5 Prepreg machines

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Fiber Type, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Carbon fiber

- 6.3 Glass fiber

- 6.4 Aramid fiber

- 6.5 Natural fibers

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Aerospace & defense

- 7.3 Transportation

- 7.4 Construction

- 7.5 Sports & leisure

- 7.6 Medical

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Technology Level, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Manual equipment

- 8.3 Semi-automated systems

- 8.4 Fully automated equipment

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Changzhou Run Feng Yuan Textile Machinery Manufacturing Co., Ltd.

- 11.2 Cygnet Texkimp

- 11.3 Dashmesh Jacquard And Powerloom Pvt. Ltd.

- 11.4 Griffith Textile Machines

- 11.5 Hangzhou Dengte Textile Machinery Co., Ltd

- 11.6 IMESA S.r.l.

- 11.7 Itema Group

- 11.8 KARL MAYER Holding SE & CO2 KG

- 11.9 Lamiflex S.p.A.

- 11.10 Lindauer DORNIER GmbH

- 11.11 McCO2 Machinery Company, Inc.

- 11.12 Optima3D Ltd

- 11.13 Sino Textile Machinery

- 11.14 Trutzschler Nonwovens GmbH

- 11.15 TSUDAKOMA Europe s.r.l.