|

市場調査レポート

商品コード

1851318

テキスタイル用化学品:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Textile Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| テキスタイル用化学品:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

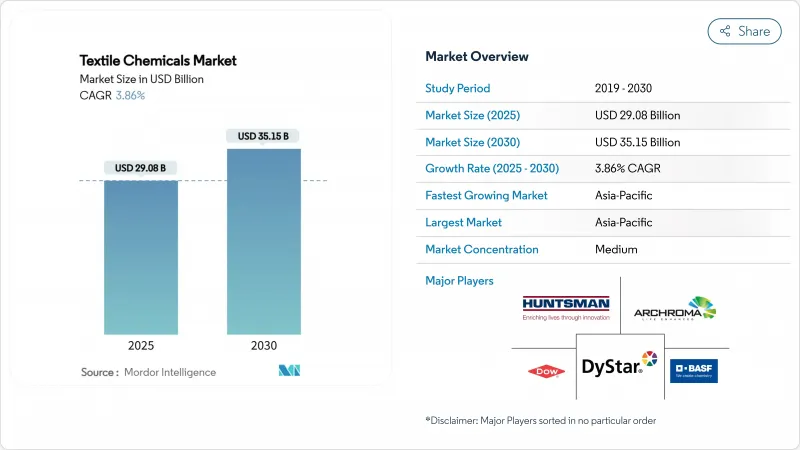

テキスタイル用化学品の市場規模は2025年に290億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.86%で、2030年には351億5,000万米ドルに達すると予測されます。

この緩やかな成長は、環境規制の強化や持続可能な製造に対する需要の高まりに適応しつつある成熟セクターを反映しています。アジア太平洋地域の堅調な拡大、デジタル印刷の採用拡大、機能性仕上げへの注目の高まりが、テキスタイル用化学品市場全体の競合の優先順位を再形成しています。現在進行中のPFASの段階的廃止と石油化学製品の価格変動は、短期的な勢いを弱めているが、バイオ酵素技術と水性技術への持続的な投資により、テキスタイル用化学品市場の長期的な成長の可能性は維持されると予想されます。

世界のテキスタイル用化学品市場の動向と洞察

アジア太平洋地域における繊維生産の力強い成長

アジア太平洋地域のテキスタイル用化学品市場は、急速な生産能力増強と政府による支援策によって活性化しています。中国の2024年の繊維製品輸出は5.7%増の1,419億6,000万米ドルで、コーティング、サイジング、着色剤事業における大規模な化学薬品消費を支えています。インドでは、人造繊維に10,683カロールインドルピーを計上する生産連動奨励金制度があり、高機能仕上げ剤への長期的な需要に舵を切っています。アジア太平洋地域に集中するサプライチェーンは、バイオベースと低VOC化学物質の迅速な導入を可能にし、世界のテキスタイル用化学品市場におけるアジア太平洋地域の中心性を強めています。

工業用繊維製品に対する需要の高まり

自動車の軽量化や医療衛生の要求により、難燃性、抗菌性、耐熱性の化学物質に対する新たな仕様基準が設定されつつあります。産業用テキスタイル分野のCAGRは4.11%で、テキスタイル用化学品市場がコモディティ量からプレミアム価格となる用途別処方へと移行しつつあることを浮き彫りにしています。ナノテクノロジーに対応した仕上げ加工は、性能の閾値をさらに引き上げ、専門サプライヤー間の研究開発競争を激化させています。

染色と仕上げにおける汚染防止コスト

事業者がCODとBODの排出規制値を下げようと努力しているため、廃水処理のアップグレードは、現在、多額の資本支出を吸収しています。生物学的技術や膜技術に資金を供給できない小規模の加工業者は、撤退や合併を進め、化学薬品需要をコンプライアンス対応の大規模バイヤーに集約しています。この再編により、テキスタイル用化学品市場の参入障壁が高まり、スイッチング・コストが上昇しています。

セグメント分析

コーティングおよびサイジング用薬品は、2024年の売上高の28.54%を占め、織物やニットラインの処理能力を下支えしています。その偏在性が安定した基礎需要を確保し、ファッションサイクルの低迷期でもテキスタイル用化学品市場を安定させています。しかし、技術革新が最も顕著なのは仕上げ剤で、撥水性、伸縮性、抗菌性の機能性を1浴で実現したいという顧客の要望により、2030年までCAGR 4.35%の成長が見込まれます。

環境性能が製品パイプラインを差別化しており、多機能シリコーンポリマーハイブリッドがフッ素系撥水剤を駆逐しています。脱脂剤は、廃水負荷を低減するバイオ酵素代替品へとシフトしています。このような進歩は、マージンを高めながら収益の中核を維持し、テキスタイル用化学品市場に豊富なビジネスチャンスをもたらしています。

地域分析

アジア太平洋は2024年に71.25%の売上を獲得し、中国の3,011億米ドルの輸出基盤とインドの2030年までに3,500億米ドルの産業が予測されることに支えられています。地域政府は生産能力拡大やテクニカル・テキスタイル・クラスターへの助成を続けており、CAGR4.01%を維持して世界のテキスタイル用化学品市場を支えています。繊維の紡績から衣服の組み立てに至るサプライチェーンの厚みは、新しいグリーンケミストリーの迅速な適合を可能にし、アジア太平洋地域の持続的なリーダーシップを確実なものにしています。

北米は小規模ながら戦略的に重要なシェアを占めており、仕様遵守が単価に優先する防護、航空宇宙、医療用繊維に特化しています。メキシコの米国ブランドへのニアショアリングの勢いは、地域の染色工場への投資を再燃させ、高付加価値助剤の新たなルートを開いています。カリフォルニアとニューヨークのPFAS規則が水性撥水剤の採用を加速させ、北米をテキスタイル用化学品市場の次世代持続可能な選択肢の実験場として位置づけています。

欧州の成熟セクターは、先進的な機械設備と、循環型社会を支持する強固な規制枠組みから恩恵を受けています。繊維から繊維へのリサイクル化学薬品への投資は増加傾向にあり、ドイツとイタリアはポリエステル解重合プラントのパイオニアです。好調な高級品と技術分野は、低インパクト仕上げの研究開発に資金を提供し、世界基準における欧州の影響力を維持しています。南米と中東の新興地域は生産量を拡大しつつあるが、インフラ格差による制約が残っており、テキスタイル用化学品市場への完全統合を遅らせています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- アジア太平洋繊維生産の力強い成長

- 技術用/工業用繊維製品に対する需要の高まり

- 低VOC化学物質に有利な世界的規制の強化

- デジタルテキスタイル印刷インキと助剤のブーム

- バイオ酵素処理ソリューションの急速な採用

- 市場抑制要因

- 染色加工における公害防止コスト

- 不安定な石油化学原料価格

- PFASとその他の物質の段階的廃止が改質コストを引き上げる

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 供給企業の交渉力

第5章 市場規模と成長予測

- タイプ別

- コーティング&サイジングケミカル

- 着色剤および助剤

- 仕上げ剤

- 脱糊剤

- その他のタイプ(糸用潤滑剤、漂白剤など)

- 原材料別

- 天然繊維

- 合成繊維

- バイオベース

- 特殊化学品

- 用途別

- アパレル

- ホームファニシング

- 自動車用テキスタイル

- 産業用テキスタイル

- その他の用途(医療・衛生テキスタイル、スポーツテキスタイルなど)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Achitex Minerva SpA

- Albemarle Corporation

- Archroma

- BASF

- Bozzetto Group

- CHT Group

- Clariant AG

- Covestro AG

- Croda International PLC

- Dow Inc.

- DyStar Group

- Evonik Industries AG

- Huntsman International LLC

- Kemira Oyj

- Kiri Industries Ltd

- K-Tech(India)Ltd

- L. N. Chemical Industries

- Nouryon

- Rudolf GmbH

- Sarex

- Sumitomo Chemical Co. Ltd

- Tanatex Chemicals BV

- Wacker Chemie AG