|

市場調査レポート

商品コード

1755193

テクニカルテキスタイル生産設備の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Technical Textile Production Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| テクニカルテキスタイル生産設備の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月27日

発行: Global Market Insights Inc.

ページ情報: 英文 155 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

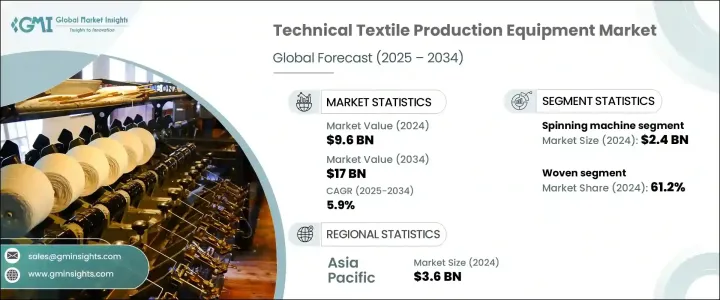

テクニカルテキスタイル生産設備の世界市場規模は、2024年に96億米ドルとなり、CAGR 5.9%で成長し、2034年には170億米ドルに達すると推定されます。

同市場の成長は、自動車、ヘルスケア、防衛、農業、建設などのセグメントにおける特殊繊維の需要増が大きな原動力となっています。産業が難燃性、耐久性、高い引張強度、生体適合性を備えた高性能材料を求める中、先進的繊維生産機械に対するニーズが高まっています。アラミド繊維、炭素繊維、超高分子量ポリエチレン繊維などの繊維技術の台頭は、テクニカルテキスタイルのすそ野を大きく広げています。さらに、環境にやさしくリサイクル可能な繊維製品に対する需要の高まりは、より先進的製造装置の必要性を後押ししています。生産プロセスにおける自動化とデジタル制御システムの開発は、効率性、カスタマイズ性、全体的な生産性の向上に役立っています。

紡績機セグメントは、原料繊維を高性能用途に必要な糸に変換する重要な役割によって、2024年に24億米ドルを生み出しました。これらの紡績機は、医療、防衛、自動車産業などの重要なセグメントで使用される繊維製品に必要な特殊糸の生産において極めて重要な役割を果たしています。炭素繊維やアラミド繊維のような先端材料へのニーズが高まるにつれ、紡績機械の需要が高まっています。これらの機械は、繊維の混紡、撚糸、技術用繊維の厳しい仕様を満たす糸の生産において高い精度を保証するからです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 96億米ドル |

| 予測金額 | 170億米ドル |

| CAGR | 5.9% |

2024年には、織物セグメントが61.2%のシェアで市場をリードします。織布は、機械的強度、構造的完全性、幅広い高性能用途への適応能力で支持されています。高い引張強度、耐久性、寸法安定性により、産業用フィルター、防弾具、シートベルト、ジオテキスタイルなどの製造に理想的です。さまざまな織りパターンや繊維配向によって織物を調整できるため、多様な用途に対応でき、先進的カスタマイズが可能です。織物市場は、自動車、航空宇宙、建設などの産業で幅広く使用されているため、拡大しています。

アジア太平洋テクニカルテキスタイル生産設備市場は2024年に36億米ドルを生み出し、37%のシェアを占めています。この地域の成長は、産業能力の拡大、技術の進歩、有利な政府施策に起因しています。中国は、発達したインフラ、低い人件費、繊維自動化への投資の増加により、この成長において重要な役割を果たしています。さらにインドは、生産連動奨励金(PLI)スキームや国家テクニカルテキスタイルミッション(NTTM)といった、テクニカルテキスタイルの生産と技術革新の促進に重点を置いた取り組みによって成長を推進しています。日本、韓国、ベトナムのような国もこの地域の成長に貢献しており、技術革新と輸出成長の両方を後押ししています。

テクニカルテキスタイル生産設備世界市場の主要企業は以下の通り:Andritz, Itema SpA, Dilo Group, BRUCKNER, Trutzschler Group SE, Staubli International AG, Reifenhauser Reicofil, Graute GmbH, Voith GmbH & Co.KGaA、Santex Rimar Group、KARL MAYER、川之江造機株式会社、SINCILON、Kusters Calico、UMPESLです。市場ポジションを強化するために、テクニカルテキスタイル生産設備産業の企業はいくつかの戦略に重点を置いています。最先端技術への投資や生産プロセスの効率化などです。企業はまた、流通網を拡大し、市場への浸透を高めるために、繊維や製造部門の主要企業とパートナーシップを結んでいます。もう一つの重要なアプローチは、精度を向上させ、コストを削減し、顧客に高度にカスタマイズ可能なソリューションを提供するために、自動化とデジタル化に投資することです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- 影響要因

- 促進要因

- テクニカルテキスタイルの需要増加

- 製造技術の進歩

- 自動車産業の成長

- 医療グレード繊維の需要増加

- 産業の潜在的リスク・課題

- 初期投資額が高め

- 原料費の変動

- 促進要因

- 成長可能性分析

- 技術概要

- 価格分析

- 規制情勢

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 産業構造と集中

- 競争強度評価

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 製品の位置付け

- 価格性能比ポジショニング

- 地理的プレゼンス

- イノベーション能力

- 戦略的ダッシュボード

- 競争力ベンチマーク

- 戦略的イニシアチブの評価

- 主要企業の SWOT 分析

- 将来の競争力見通し

第5章 市場推定・予測:機種別、2021~2034年

- 主要動向

- 押出機

- 紡績機

- 編み機

- 織機

- 不織布機械

- コーティング機

- ラミネート機

- 複合材と接着装置

- その他

第6章 市場推定・予測:プロセスタイプ別、2021~2034年

- 主要動向

- 織り

- ニット

- 不織布

- 複合

- その他

第7章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 自動車用繊維

- 建設用繊維

- 医療用繊維

- スポーツテキスタイル

- 産業用繊維

- 農業用繊維

- 保護繊維

- その他

第8章 市場推定・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接販売

- 間接販売

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Andritz

- BRUCKNER

- Dilo Group

- Graute GmbH

- Itema SpA

- KARL MAYER

- Kawanoe Zoki Co Ltd

- Kusters Calico

- Reifenhauser Reicofil

- Santex Rimar Group

- SINCILON

- Staubli International AG

- Trutzschler Group SE

- UMPESL

- Voith GmbH & Co. KGaA

The Global Technical Textile Production Equipment Market was valued at USD 9.6 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 17 billion by 2034. The growth of the market is largely driven by the increasing demand for specialized textiles in sectors like automotive, healthcare, defense, agriculture, and construction. As industries look for high-performance materials that offer flame resistance, durability, high tensile strength, and biocompatibility, there is a growing need for advanced textile production machinery. The rise of fiber technologies, including aramid fiber, carbon fiber, and ultra-high molecular weight polyethylene fibers, is significantly broadening the scope for technical textiles. Furthermore, the growing demand for eco-friendly and recyclable textiles pushes for more sophisticated manufacturing equipment. The development of automation and digital control systems in production processes has helped improve efficiency, customization, and overall productivity.

The spinning machine segment generated USD 2.4 billion in 2024, driven by its crucial role in converting raw fibers into yarns needed for high-performance applications. These machines play a pivotal role in the production of specialized yarns that are required for textiles used in critical sectors such as medical, defense, and automotive industries. With the growing need for advanced materials like carbon and aramid fibers, the demand for spinning machines is rising, as these machines ensure high precision in fiber blending, twisting, and producing yarns that meet the stringent specifications of technical textiles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.6 Billion |

| Forecast Value | $17 Billion |

| CAGR | 5.9% |

In 2024, the woven fabric segment led the market with a share of 61.2%. Woven fabrics are favored for their mechanical strength, structural integrity, and ability to adapt to a wide range of high-performance applications. Their high tensile strength, durability, and dimensional stability make them ideal for manufacturing products such as industrial filters, ballistic gear, seat belts, and geotextiles. The ability to tailor woven textiles through various weave patterns and fiber orientations makes them versatile and highly customizable for diverse applications. The market for woven fabrics is expanding due to their broad usage in industries like automotive, aerospace, and construction.

Asia Pacific Technical Textile Production Equipment Market generated USD 3.6 billion in 2024, holding a 37% share. The region's growth can be attributed to expanding industrial capabilities, technological advancements, and favorable government policies. China plays a significant role in this growth due to its developed infrastructure, lower labor costs, and increased investments in textile automation. Additionally, India's progress is being propelled by initiatives such as the Production Linked Incentive (PLI) Scheme and the National Technical Textiles Mission (NTTM), which focus on boosting production and innovation in technical textiles. Countries like Japan, South Korea, and Vietnam also contribute to this regional growth, helping drive both technological innovation and export growth.

Leading players in the Global Technical Textile Production Equipment Market include: Andritz, Itema SpA, Dilo Group, BRUCKNER, Trutzschler Group SE, Staubli International AG, Reifenhauser Reicofil, Graute GmbH, Voith GmbH & Co. KGaA, Santex Rimar Group, KARL MAYER, Kawanoe Zoki Co Ltd, SINCILON, Kusters Calico, and UMPESL. To strengthen their market position, companies in the technical textile production equipment industry focus on several strategies. These include investing in cutting-edge technology and enhancing the efficiency of production processes to meet the growing demand for advanced materials. Firms are also forming partnerships with key players in the textile and manufacturing sectors to expand their distribution networks and increase market penetration. Another critical approach is investing in automation and digitalization to improve precision, reduce costs, and offer highly customizable solutions for their customers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.4.2.1 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for technical textiles

- 3.2.1.2 Advancements in manufacturing technologies

- 3.2.1.3 Growth in the automotive industry

- 3.2.1.4 Increased demand for medical-grade textiles

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment

- 3.2.2.2 Fluctuating raw material costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technological overview

- 3.5 Pricing analysis

- 3.6 Regulatory landscape

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Industry structure and concentration

- 4.3 Competitive intensity assessment

- 4.4 Company market share analysis

- 4.5 Competitive positioning matrix

- 4.5.1 Product positioning

- 4.5.2 Price-performance positioning

- 4.5.3 Geographic presence

- 4.5.4 Innovation capabilities

- 4.6 Strategic dashboard

- 4.6.1 Competitive benchmarking

- 4.6.1.1 Manufacturing capabilities

- 4.6.1.2 Product portfolio strength

- 4.6.1.3 Distribution network

- 4.6.1.4 R&D investments

- 4.6.2 Strategic initiatives assessment

- 4.6.3 SWOT analysis of key players

- 4.6.4 Future competitive outlook

- 4.6.1 Competitive benchmarking

Chapter 5 Market Estimates & Forecast, By Machine Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Extrusion machine

- 5.3 Spinning machine

- 5.4 Knitting machine

- 5.5 Weaving machine

- 5.6 Nonwoven machinery

- 5.7 Coating machine

- 5.8 Laminating machine

- 5.9 Composite and bonding equipment

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Process Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Woven

- 6.3 Knitted

- 6.4 Nonwoven

- 6.5 Composite

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Automotive textiles

- 7.3 Construction textiles

- 7.4 Medical textiles

- 7.5 Sports textiles

- 7.6 Industrial textiles

- 7.7 Agro textiles

- 7.8 Protective textiles

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Andritz

- 10.2 BRUCKNER

- 10.3 Dilo Group

- 10.4 Graute GmbH

- 10.5 Itema SpA

- 10.6 KARL MAYER

- 10.7 Kawanoe Zoki Co Ltd

- 10.8 Kusters Calico

- 10.9 Reifenhauser Reicofil

- 10.10 Santex Rimar Group

- 10.11 SINCILON

- 10.12 Staubli International AG

- 10.13 Trutzschler Group SE

- 10.14 UMPESL

- 10.15 Voith GmbH & Co. KGaA