|

市場調査レポート

商品コード

1740784

メタマテリアル吸収材料の市場機会、成長促進要因、産業動向分析、予測、2025~2034年Metamaterial Absorbers Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| メタマテリアル吸収材料の市場機会、成長促進要因、産業動向分析、予測、2025~2034年 |

|

出版日: 2025年04月24日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

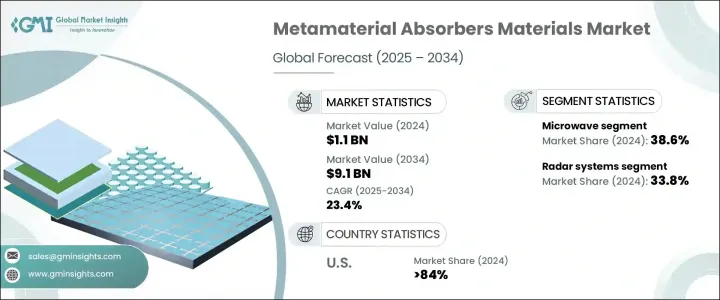

メタマテリアル吸収材料の世界市場規模は、2024年に11億米ドルとなり、特に5Gネットワークやその他の先進システム向けの電磁干渉シールドの需要増加や高周波通信インフラへの投資増加により、CAGR 23.4%で成長し、2034年には91億米ドルに達すると推定されます。

防衛、通信、自動車、エネルギーなどの分野では、性能を向上させ信号の乱れを減らすために、電波吸収技術への注目が高まっています。従来の材料が高周波電磁波への対応に苦戦する中、メタマテリアル吸収材料は、正確な共振周波数で高い吸収効率を実現することで、有望なソリューションを提供します。継続的な研究と技術革新の努力により、これらの材料の信頼性と応用範囲が強化され、現代のインフラの課題に対応する軽量で高性能な吸収技術の開発が可能になっています。

これらの先端材料は、設計された構造で電磁波を操作することにより、ほぼ完全な吸収性能を実現します。このような吸収体は現在、民間および軍事用途の両方において、ステルス性能を向上させ、反射を最小限に抑えるために不可欠なものとなっています。最近の技術動向では、先進的な製造プロセスによって広帯域吸収体が製造され、環境電磁制御やレーダー遮断に利用されています。設計の柔軟性と強力な性能により、メタマテリアル吸収材料は次世代の航空宇宙、自動車、防衛システムに統合されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 11億米ドル |

| 予測金額 | 91億米ドル |

| CAGR | 23.4% |

周波数セグメント別では、マイクロ波周波数吸収材料が2024年に38.6%の最大シェアを占めました。これは、軽量で軍事用途に適応しながら、電磁波を効果的に減衰させる能力があるためです。これらの材料は、レーダー断面積を最小化することでレーダー探知を低減する効果が高く、防衛用途におけるステルス能力を高めます。その効率性と統合の容易さにより、安全保障に重点を置く業界全体で好まれる選択肢となっています。この分野での市場の優位性は、角度範囲と帯域幅を拡大する継続的な技術革新によって強化されています。

レーダーシステムアプリケーションセグメントは、2024年に33.8%のシェアを占め、検出精度を高め、レーダー断面シグネチャを低減するメタマテリアルの比類ない能力がその原動力となっています。これらの材料は、優れた電磁波吸収を実現しながら消費電力の少ない軽量でコンパクトなコンポーネントを統合することで、レーダーシステムを効果的に運用することを可能にします。メタマテリアル吸収材料の性能上の利点は、スピード、精度、ステルス性が重要な現代のレーダーアプリケーションに理想的です。国防省や国土安全保障省からの継続的な資金援助により、探知可能性を最小限に抑えながらシステムの感度を高めることに戦略的重点を置いた技術革新が加速しています。調査が深まるにつれ、レーダー統合はメタマテリアル吸収材料市場の成長を促進する主要分野として際立ってきています。

米国のメタマテリアル吸収材料市場は2024年に84%のシェアを占め、2億米ドルの売上を計上しました。米国は、高性能防衛および通信システム用メタマテリアルの開発と展開の最前線にいます。継続的な技術革新により、研究開発への戦略的投資、防衛近代化プログラム、政府機関と民間企業の利害関係者の積極的な協力を通じて、この地域はリードを維持しています。

この市場の主要企業には、Kymeta、Meta Materials Inc.、Metamagnetics、TeraView、Echodyneなどがあります。これらの企業は、独自の技術に投資し、製品ポートフォリオを拡大し、戦略的提携を結び、政府が支援する研究開発プログラムを活用することで前進しています。また、国際競争力を強化するために、生産能力を拡大し、防衛等級の認定を模索しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税の影響- 構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 5Gと次世代通信の拡大

- 小型の吸収体を必要とする小型電子機器の使用増加

- 業界の潜在的リスク&課題

- 製造コストが高く、処理が複雑

- 生産と製造における高いエネルギー消費

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:周波数別、2021-2034年

- 主要動向

- 周波数

- 電子レンジ

- テラヘルツ

- 赤外線(IR)

- その他

第6章 市場推定・予測:材料タイプ別、2021-2034年

- 主要動向

- 電磁メタマテリアル

- フォトニックメタマテリアル

- キラルメタマテリアル

- その他

第7章 市場推定・予測:アプリケーション別、2021-2034年

- 主要動向

- レーダーシステム

- ステルス技術

- 無線通信

- 医療画像

- ソーラーエネルギーハーベスティング

- その他

第8章 市場推定・予測:地域別、2021-2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Echodyne

- Entuple Technologies

- E-SONG EMC

- JEM Engineering

- Kymeta

- Meta Materials

- Metamagnetics

- MetaShield

- Microwave Measurement System

- Nanohmics

- Phoebus Optoelectronics

- TeraView

The Global Metamaterial Absorbers Materials Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 23.4% to reach USD 9.1 billion by 2034, driven by the increasing demand for electromagnetic interference shielding and rising investments in high-frequency communication infrastructure, particularly for 5G networks and other advanced systems. In sectors like defense, telecommunications, automotive, and energy, there is a growing focus on wave-absorbing technologies to enhance performance and reduce signal disruptions. As traditional materials struggle to cope with high-frequency electromagnetic waves, metamaterial absorbers offer a promising solution by delivering high absorption efficiency at precise resonance frequencies. Continued research and innovation efforts are enhancing the reliability and range of applications for these materials, enabling the development of lightweight, high-performance absorption technologies that address modern infrastructure challenges.

These advanced materials deliver near-complete absorption performance by manipulating electromagnetic waves with engineered structures. Such absorbers are now essential for improving stealth capabilities and minimizing reflection in both civil and military uses. Recent technological developments have produced broadband absorbers through advanced manufacturing processes, making them valuable for environmental electromagnetic control and radar blocking. With design flexibility and strong performance, metamaterial absorbers integrate into next-generation aerospace, automotive, and defense systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 23.4% |

Based on frequency segmentation, microwave frequency absorbers held the largest share at 38.6% in 2024 due to their ability to effectively dampen electromagnetic waves while being lightweight and adaptable for military use. These materials are highly effective in reducing radar detection by minimizing the radar cross-section, which enhances stealth capabilities in defense applications. Their efficiency and ease of integration make them the preferred choice across security-focused industries. Market dominance in this segment has been reinforced through ongoing innovation expanding angular range and bandwidth.

The radar system applications segment held a 33.8% share in 2024, driven by metamaterials' unmatched ability to enhance detection precision and reduce radar cross-section signatures. These materials allow radar systems to operate effectively by integrating lightweight, compact components that consume less power while delivering superior electromagnetic wave absorption. The performance benefits of metamaterial absorbers make them ideal for modern radar applications where speed, accuracy, and stealth are vital. Ongoing funding from defense and homeland security departments is accelerating innovation, with strategic emphasis on increasing system sensitivity while minimizing detectability. As research deepens, radar integration continues to stand out as a prime sector fueling growth in the metamaterial absorbers materials market.

United States Metamaterial Absorbers Materials Market held an 84% share in 2024 and generated USD 200 million reinforced by advanced military capabilities, a robust scientific infrastructure, and dedicated support from federal agencies for next-generation defense technologies. The U.S. has been at the forefront of developing and deploying metamaterials for high-performance defense and communication systems. With continued innovation, the region maintains its lead through strategic investment in R&D, defense modernization programs, and active collaboration between government institutions and private industry stakeholders.

Key companies in this market include Kymeta, Meta Materials Inc., Metamagnetics, TeraView, and Echodyne. These players are advancing by investing in proprietary technologies, expanding their product portfolios, forming strategic alliances, and leveraging government-backed R&D programs. They are also scaling production capacities and exploring defense-grade certifications to enhance global competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.1.1 Country 1

- 3.3.1.2 Country 2

- 3.3.1.3 Country 3

- 3.3.2 Major importing countries

- 3.3.2.1 Country 1

- 3.3.2.2 Country 2

- 3.3.2.3 Country 3

- 3.3.1 Major exporting countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Expansion of 5g and next-gen communications

- 3.7.1.2 Growing use of miniaturized electronics requiring compact absorbers

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High manufacturing cost and complex processing

- 3.7.2.2 High energy consumption in production and fabrication

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Frequency, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Frequency

- 5.3 Microwave

- 5.4 Terahertz

- 5.5 Infrared (IR)

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Electromagnetic metamaterials

- 6.3 Photonic metamaterials

- 6.4 Chiral metamaterials

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Radar systems

- 7.3 Stealth technology

- 7.4 Wireless communication

- 7.5 Medical imaging

- 7.6 Solar energy harvesting

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Echodyne

- 9.2 Entuple Technologies

- 9.3 E-SONG EMC

- 9.4 JEM Engineering

- 9.5 Kymeta

- 9.6 Meta Materials

- 9.7 Metamagnetics

- 9.8 MetaShield

- 9.9 Microwave Measurement System

- 9.10 Nanohmics

- 9.11 Phoebus Optoelectronics

- 9.12 TeraView