補強用腐食抑制剤の市場機会と促進要因、産業動向分析、2025年~2034年予測

Corrosion Inhibitors for Reinforcement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801862

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

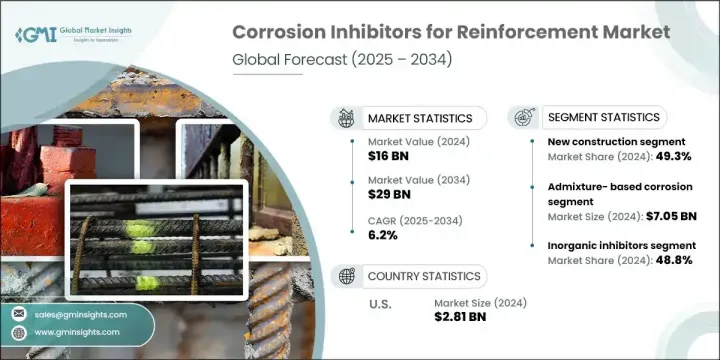

補強用腐食抑制剤の世界市場は、2024年には160億米ドルと評価され、CAGR 6.2%で成長し、2034年には290億米ドルに達すると推定されています。

この市場には、鉄筋コンクリート構造物の腐食を防止するために特別に設計された、表面塗布型抑制剤、混和剤ベース製剤、移行システムなど、さまざまな種類のソリューションが含まれます。開発、都市化の進展、耐久性の向上と補修頻度の低減を目的とした規制要求の高まりが市場成長の原動力となっています。

より厳格な建築基準や持続可能性の目標を実施する国が増えるにつれ、建設・土木セグメント全体において、先進的抑制剤を使用して鉄筋コンクリート構造物の寿命を延ばす必要性が不可欠となっています。北米、欧州、アジア太平洋のなどの地域では、耐久性が高く長持ちする建材に対する需要が高まっており、腐食防止技術に対する強い機運が高まっています。環境的に安全でサステイナブル腐食防止剤ソリューションへのシフトは、技術革新を加速させています。メーカーは、世界の環境コンプライアンス目標に沿った、より新しい送達メカニズムやグリーンケミストリーの開発を進めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 160億米ドル |

| 予測金額 | 290億米ドル |

| CAGR | 6.2% |

さまざまな製品タイプの中で、混和剤ベース腐食防止剤セグメントは2024年に44%のシェアを占めました。これらは、コンクリート混合物への組み込みが容易であることと、特に新しく建設された構造物に対して長期的な内部保護を提供する能力があることから支持されています。また、メンテナンス用途にも効果的に使用されています。対照的に、表面塗布型ソリューションは、古いコンクリート資産の改修や保全に広く使用されています。

用途別では、新築セグメントが2024年に49.3%のシェアを占めました。コンクリート混合時に抑制剤を使用することで、構造物の弾力性が大幅に向上し、腐食の発生を遅らせることができます。この予防的アプローチは、近代的な建設手法の重要な一部となりつつあります。

米国の補強用腐食抑制剤2024年の市場規模は28億1,000万米ドル。同国は、大手メーカーの強い存在感と、製品性能の向上、持続可能性、規制との整合に焦点を当てた強力な調査努力から利益を得ています。インフラの近代化が国家的な優先事項となるにつれて、耐久性があり、メンテナンスが容易なコンクリート構造物に対する需要は増加の一途をたどっています。先進的なインヒビター技術は、交通システム、商業ビル、土木インフラ、住宅開発などで採用が進んでおり、性能に関する義務に準拠し、修繕費を削減することができます。

補強用腐食抑制剤市場で事業を展開している主要企業には、GCP Applied Technologies Inc.、BASF SE、Halliburton(生産化学品部門)、Sika AG、Penetron International Ltd.、Pidilite Industries Limited、Clariant AG、MAPEI S.p.A.、ChemTreat Inc.、Arkema Group、Ecolab Inc.(Nalco Water)、Dow Inc.、CEMEX S.A.B. de C.V.、Evonik Industries AGなどがあります。

市場セグメンテーションセグメントの各社は、市場での存在感を高めるため、イノベーション、持続可能性、オーダーメイドの製品ソリューションを中心とした戦略的イニシアチブを実施しています。グリーンビルディング規制に適合し、環境への影響を低減する、環境に優しく無害な配合の開発に大きな焦点が当てられています。企業は、インフラ需要の高い新興市場に参入することで、世界の足跡を拡大しています。建設会社や研究開発機関との戦略的提携は、製品の性能や応用技術の向上に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 耐久性の高いインフラ資材の需要増加

- 阻害剤製剤の技術的進歩

- サステイナブル建設化学品の規制強化

- 産業の潜在的リスク・課題

- コンクリート配合設計の適合性の問題

- 価格競争市場におけるコスト感度

- 市場機会

- スマート建設とモニタリングシステムとの統合

- 環境に優しくサステイナブルソリューションへの需要の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:製品タイプ別、2021~2034年

- 主要動向

- 混和剤ベース腐食抑制剤

- 亜硝酸カルシウム系阻害剤

- 有機混和剤抑制剤

- リン酸系混和剤

- その他の化学混和剤

- 表面塗布型腐食防止剤

- 浸透阻害剤

- バリア形成阻害剤

- 二相阻害剤

- 移行性腐食抑制剤

- 有機移動阻害剤

- 無機移動システム

- 新興技術

- スマート/応答性阻害剤

- ナノ強化システム

- バイオベース阻害剤

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 新築用途

- コンクリートミキシングステージの統合

- 施工前の表面治療

- リハビリテーションと修復

- 表面塗布方法

- 注入と含浸技術

- メンテナンスと保護

- 予防保守プログラム

- 緊急修理用途

第7章 市場推定・予測:化学タイプ別、2021~2034年

- 主要動向

- 無機阻害剤

- 亜硝酸塩ベースシステム

- リン酸系化合物

- ケイ酸塩系阻害剤

- 有機阻害剤

- アミノアルコールベースシステム

- アミンカルボン酸阻害剤

- 有機酸誘導体

- ハイブリッドと先進的システム

- 有機無機の組み合わせ

- ナノ強化製剤

- スマートリリースシステム

第8章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- インフラと交通

- 橋梁と高速道路構造物

- トンネルと地下建設

- 海洋と港湾施設

- 空港インフラ

- 住宅建設

- 高層ビル

- 住宅開発

- 改修プロジェクト

- 商業・産業用

- オフィスビルと複合施設

- 産業施設

- 倉庫と配送センター

- 特殊用途

- 石油・ガス施設

- 発電所

- 水処理インフラ

- 化学処理工場

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- Arkema Group

- BASF SE

- ChemTreat Inc.

- CEMEX S.A.B. de C.V.

- Clariant AG

- Dow Inc.

- Ecolab Inc.(Nalco Water)

- Evonik Industries AG

- GCP Applied Technologies Inc

- Halliburton(Production Chemicals Division)

- MAPEI S.p.A

- Penetron International Ltd.

- Pidilite Industries Limited

- Sika AG

目次

The Global Corrosion Inhibitors for Reinforcement Market was valued at USD 16 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 29 billion by 2034. This market includes various types of solutions such as surface-applied inhibitors, admixture-based formulations, and migrating systems specifically designed to prevent corrosion in reinforced concrete structures. Market growth is fueled by increasing infrastructure development, urbanization, and heightened regulatory demands aimed at boosting durability and reducing repair frequency.

As more countries implement stricter building codes and sustainability goals, the need to extend the life of reinforced concrete structures using advanced inhibitors has become essential across the construction and civil engineering sectors. In regions like North America, Europe, and Asia-Pacific, there's a rising demand for durable and long-lasting building materials, creating strong momentum for corrosion prevention technologies. The shift toward environmentally safe, sustainable corrosion inhibitor solutions is accelerating innovation. Manufacturers are developing newer delivery mechanisms and green chemistries that align with global eco-compliance goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16 Billion |

| Forecast Value | $29 Billion |

| CAGR | 6.2% |

Among the different product types, the admixture-based corrosion inhibitors segment held a 44% share in 2024. These are favored for their ease of integration into concrete mixes and their ability to provide long-term internal protection, particularly for newly built structures. They are also used effectively in maintenance applications. In contrast, surface-applied solutions are widely used for rehabilitating and preserving older concrete assets.

In terms of application, the new construction segment held a 49.3% share in 2024. The use of inhibitors during concrete mixing significantly improves structural resilience and delays the onset of corrosion, minimizing lifecycle costs and aligning with broader efforts to raise infrastructure quality standards over extended timelines. This preventative approach is becoming a critical part of modern construction practices.

U.S. Corrosion Inhibitors for Reinforcement Market generated USD 2.81 billion in 2024. The country benefits from a strong presence of leading manufacturers and robust research efforts focused on improving product performance, sustainability, and regulatory alignment. As infrastructure modernization gains national priority, the demand for durable, low-maintenance concrete structures continues to rise. Advanced inhibitor technologies are being increasingly adopted across transportation systems, commercial buildings, civil infrastructure, and residential developments to comply with performance mandates and lower repair expenditures.

Key companies operating in the Corrosion Inhibitors for Reinforcement Market include GCP Applied Technologies Inc., BASF SE, Halliburton (Production Chemicals Division), Sika AG, Penetron International Ltd., Pidilite Industries Limited, Clariant AG, MAPEI S.p.A., ChemTreat Inc., Arkema Group, Ecolab Inc. (Nalco Water), Dow Inc., CEMEX S.A.B. de C.V., and Evonik Industries AG.

To enhance market presence, companies in the corrosion inhibitors for reinforcement segment are implementing strategic initiatives centered around innovation, sustainability, and tailored product solutions. A significant focus is placed on developing eco-friendly, non-toxic formulations that comply with green building regulations and reduce environmental impact. Businesses are expanding their global footprint by entering emerging markets with high infrastructure demand. Strategic collaborations with construction firms and R&D institutes help improve product performance and application techniques.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application method

- 2.2.3 Chemistry type

- 2.2.4 End use industry

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for long-lasting infrastructure materials

- 3.2.1.2 Technological advancements in inhibitor formulations

- 3.2.1.3 Regulatory push for sustainable construction chemicals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Compatibility issues with concrete mix designs

- 3.2.2.2 Cost sensitivity in price-competitive markets

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with smart construction and monitoring systems

- 3.2.3.2 Rising demand for eco-friendly and sustainable solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Admixture-based corrosion inhibitors

- 5.2.1 Calcium nitrite-based inhibitors

- 5.2.2 Organic admixture inhibitors

- 5.2.3 Phosphate-based admixtures

- 5.2.4 Other chemical admixtures

- 5.3 Surface-applied corrosion inhibitors

- 5.3.1 Penetrating inhibitors

- 5.3.2 Barrier-forming inhibitors

- 5.3.3 Dual-phase inhibitors

- 5.4 Migrating corrosion inhibitors

- 5.4.1 Organic migrating inhibitors

- 5.4.2 Inorganic migrating systems

- 5.5 Emerging technologies

- 5.5.1 Smart/responsive inhibitors

- 5.5.2 Nano-enhanced systems

- 5.5.3 Bio-based inhibitors

Chapter 6 Market Estimates and Forecast, By Application Method, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 New construction applications

- 6.2.1 Concrete mixing stage integration

- 6.2.2 Pre-construction surface treatment

- 6.3 Rehabilitation and repair

- 6.3.1 Surface application methods

- 6.3.2 Injection and impregnation techniques

- 6.4 Maintenance and protection

- 6.4.1 Preventive maintenance programs

- 6.4.2 Emergency repair applications

Chapter 7 Market Estimates and Forecast, By Chemistry Type, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Inorganic inhibitors

- 7.2.1 Nitrite-based systems

- 7.2.2 Phosphate-based compounds

- 7.2.3 Silicate-based inhibitors

- 7.3 Organic inhibitors

- 7.3.1 Aminoalcohol-based systems

- 7.3.2 Amine carboxylate inhibitors

- 7.3.3 Organic acid derivatives

- 7.4 Hybrid and advanced systems

- 7.4.1 Organic-inorganic combinations

- 7.4.2 Nano-enhanced formulations

- 7.4.3 Smart release systems

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Infrastructure and transportation

- 8.2.1 Bridge and highway structures

- 8.2.2 Tunnels and underground construction

- 8.2.3 Marine and port facilities

- 8.2.4 Airport infrastructure

- 8.3 Residential construction

- 8.3.1 High-rise buildings

- 8.3.2 Housing developments

- 8.3.3 Renovation projects

- 8.4 Commercial and industrial

- 8.4.1 Office buildings and complexes

- 8.4.2 Industrial facilities

- 8.4.3 Warehouses and distribution centers

- 8.5 Specialty applications

- 8.5.1 Oil and gas facilities

- 8.5.2 Power generation plants

- 8.5.3 Water treatment infrastructure

- 8.5.4 Chemical processing plants

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arkema Group

- 10.2 BASF SE

- 10.3 ChemTreat Inc.

- 10.4 CEMEX S.A.B. de C.V.

- 10.5 Clariant AG

- 10.6 Dow Inc.

- 10.7 Ecolab Inc. (Nalco Water)

- 10.8 Evonik Industries AG

- 10.9 GCP Applied Technologies Inc

- 10.10 Halliburton (Production Chemicals Division)

- 10.11 MAPEI S.p.A

- 10.12 Penetron International Ltd.

- 10.13 Pidilite Industries Limited

- 10.14 Sika AG

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日