|

市場調査レポート

商品コード

1721561

貨物鉄道車両補修市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Freight Railcar Repair Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 貨物鉄道車両補修市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月01日

発行: Global Market Insights Inc.

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

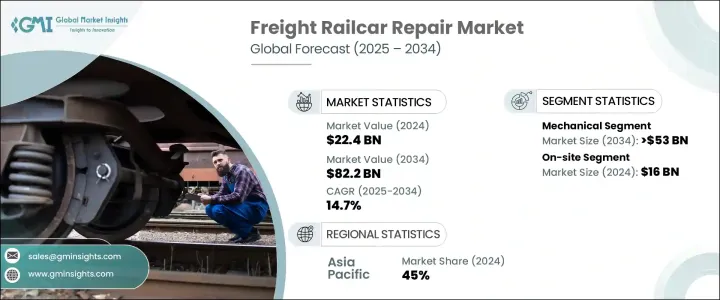

貨物鉄道車両補修の世界市場規模は、2024年に224億米ドルとなり、CAGR 14.7%で成長し、2034年には822億米ドルに達すると予測されています。

修理サービスの需要は、一般的に30~50年使用され続ける貨物鉄道車両の老朽化によってますます高まっています。しかし、高荷重、過酷な環境条件、継続的な運行に頻繁にさらされるため、摩耗や損傷が加速し、タイムリーな修理が不可欠となっています。このような一貫したメンテナンスの必要性の高まりは、鉄道業界が鉄道車両のライフサイクル管理にどのように取り組むかを大きく変えつつあります。世界の貨物輸送量が増加し続ける中、企業は最高の運行効率を維持し、安全コンプライアンスを確保し、サプライチェーンの混乱を最小限に抑えることをより重視しています。

規制上の義務や安全基準はより厳しくなっており、利害関係者は定期的な検査、修理、アップグレードを優先するようになっています。そのため、修理・改修市場は貨物鉄道エコシステムの重要な柱として台頭しており、車両の近代化とスマート鉄道インフラへの投資の拡大に支えられています。発展途上国や先進国を横断する貨物路線の拡大とデジタル保守プラットフォームの統合により、鉄道車両の修理サービスは、より広範な輸送とロジスティクスの展望における重要な成長分野として位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 224億米ドル |

| 予測金額 | 822億米ドル |

| CAGR | 14.7% |

IoTセンサーやAI駆動型診断などの予知保全技術の統合は、運用パフォーマンスの向上において極めて重要な役割を果たしています。これらのツールは、リアルタイムの故障検出と分析を可能にし、ダウンタイムを削減し、鉄道車両の全体的な耐用年数を延ばします。部品の故障を事前に予測することで、鉄道事業者はメンテナンスに対してより積極的なアプローチを取ることができ、コストのかかるサービスの中断や予定外のオーバーホールを回避することができます。

市場は、機械修理、構造物修理、内装修理など、修理サービスの種類によって区分されます。機械的修理が市場の60%を占め、2034年までに530億米ドルに達すると予測されています。極端な高温、高荷重、ノンストップの使用など、過酷な運転条件にさらされることの多い鉄道車両は、車軸、ブレーキ、連結器、サスペンション・システムなどの重要部品が著しく摩耗する傾向があります。こうしたフリートが成熟するにつれ、安全基準を維持し、継続的な生産性を確保するために、機械的な修理がますます必要になってくる。この需要の急増は、機械修理セグメントの成長軌道を強化しています。

サービス提供セグメントでは、オンサイト修理サービスが2024年に160億米ドルを生み出しました。これらのサービスは、運転遅延を最小限に抑えることができるため、好まれる選択肢になりつつあります。保守のために鉄道車両を敷地外に輸送することは、特に広大な鉄道網を管理する鉄道事業者にとっては、時間も費用もかかります。オンサイト・ソリューションは、迅速なターンアラウンドタイムとサプライチェーンの効率化を可能にし、高い評価を得ています。

2024年の世界貨物鉄道車両補修市場は、アジア太平洋地域が45%のシェアを占め、中国が圧倒的な強さを見せています。インフラ拡張と産業開発により鉄道貨物産業が活況を呈している同国では、修理・保守サービスへの需要が高まっています。貨物量の増加により、この地域全体で運行の信頼性を支えるためのタイムリーな修理、アップグレード、部品交換の必要性が高まっています。

世界貨物鉄道車両補修市場の主要企業には、シーメンス、ワブテック・コーポレーション、アルストム、プログレス・レール、TTX、トリニティ・インダストリーズ、ワトコ・カンパニーズ、ユニオン・タンクカー・カンパニー(UTLX)、グリーンブライヤー・カンパニーズ、キャスカート・レールなどがあります。これらの企業は、IoT対応センサー、AI診断、自動監視ツールなどの先進技術を統合し、予知保全機能を提供しています。さらに、サービス提供を改善し、進化する顧客ニーズに対応するため、現場での修理能力を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 鉄道車両メーカーおよびOEM

- 鉄道車両の修理・メンテナンス業者

- 鉄道事業者および物流会社

- 規制当局およびコンプライアンス機関

- 最終用途

- サプライヤーの情勢

- 利益率分析

- テクノロジーとイノベーションの情勢

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 安全機能に対する需要の増加

- 貨物需要の増加

- AIと機械学習の統合

- 政府の規制とインセンティブの拡大

- 業界の潜在的リスク&課題

- データのプライバシーとセキュリティに関する懸念

- 実装コストが高め

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 機械

- ブレーキシステム

- 連結器とドラフトギア

- ベアリングと車軸

- ホイールとホイールセット

- ドアとハッチ

- 空気圧システム

- その他

- 構造的

- ボディとフレームの修理

- 溶接と金属加工

- 腐食防止と補修

- ルーフ、サイド、アンダーボディの修理

- その他

- インテリア

- 床材と床下地

- 内装ライニングと断熱材

- 照明および電気システム

- その他

- その他

第6章 市場推計・予測:サービス別、2021-2034

- 主要動向

- モバイル

- 現場

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第8章 企業プロファイル

- A&B Rail Services

- Alstom

- American Industrial Transport

- Apache Railway Company

- Cathcart Rail

- CF Rail Services

- GATX

- Herzog Services

- Progress Rail

- Quality Rail Service

- Railserve

- Rescar Companies

- Road &Rail Services

- Siemens

- The Greenbrier Companies

- Trinity Industries

- TTX Company

- Union Tank Car Company(UTLX)

- Wabtec

- Watco Companies

The Global Freight Railcar Repair Market was valued at USD 22.4 billion in 2024 and is estimated to grow at a CAGR of 14.7% to reach USD 82.2 billion by 2034. The demand for repair services is being increasingly driven by the aging fleet of freight railcars, which typically remain in service for 30 to 50 years. However, frequent exposure to heavy loads, harsh environmental conditions, and continuous operations accelerates wear and tear, making timely repairs essential. This rising need for consistent maintenance is reshaping how the industry approaches railcar lifecycle management. As global freight activity continues to rise, companies are placing greater emphasis on maintaining peak operational efficiency, ensuring safety compliance, and minimizing disruptions in supply chains.

Regulatory mandates and safety standards are becoming more stringent, prompting stakeholders to prioritize routine inspections, repairs, and upgrades. As such, the repair and refurbishment market is emerging as a critical pillar of the freight rail ecosystem, supported by growing investments in fleet modernization and smart rail infrastructure. The expansion of freight routes across developing and developed nations, alongside the integration of digital maintenance platforms, is positioning railcar repair services as a key growth area in the broader transportation and logistics landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.4 Billion |

| Forecast Value | $82.2 Billion |

| CAGR | 14.7% |

The integration of predictive maintenance technologies, such as IoT sensors and AI-driven diagnostics, is playing a pivotal role in boosting operational performance. These tools enable real-time fault detection and analytics, reduce downtime, and extend the overall service life of the railcars. By anticipating component failures before they happen, rail operators can take a more proactive approach to maintenance, avoiding costly service interruptions and unplanned overhauls.

The market is segmented based on the type of repair services, including mechanical, structural, and interior repairs. Mechanical repairs dominate the segment, accounting for 60% of the market, and are projected to reach USD 53 billion by 2034. Railcars frequently exposed to demanding operational conditions, such as extreme temperatures, heavy cargo loads, and non-stop usage, tend to experience significant wear on critical components like axles, brakes, couplers, and suspension systems. As these fleets mature, mechanical repairs become increasingly necessary to maintain safety standards and ensure continued productivity. This demand surge is reinforcing the growth trajectory of the mechanical repair segment.

In the service delivery segment, on-site repair services generated USD 16 billion in 2024. These services are becoming the preferred choice due to their ability to minimize operational delays. Transporting railcars off-site for maintenance is both time-consuming and expensive, especially for operators managing expansive rail networks. On-site solutions allow faster turnaround times and enhanced supply chain efficiency, making them a highly valued offering.

The Asia Pacific region led the global freight railcar repair market in 2024, holding a 45% share, with China emerging as the dominant force. The country's booming rail freight industry-fueled by infrastructure expansion and industrial development-is generating increased demand for repair and maintenance services. Growing freight volumes are pushing the need for timely repairs, upgrades, and component replacements to support operational reliability across the region.

Key players in the Global Freight Railcar Repair Market include Siemens, Wabtec Corporation, Alstom, Progress Rail, TTX, Trinity Industries, Watco Companies, Union Tank Car Company (UTLX), The Greenbrier Companies, and Cathcart Rail. These companies are integrating advanced technologies like IoT-enabled sensors, AI diagnostics, and automated monitoring tools to offer predictive maintenance capabilities. Additionally, they are expanding their on-site repair capacities to improve service delivery and meet evolving customer needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Railcar manufacturers & OEMS

- 3.1.2 Railcar repair & maintenance providers

- 3.1.3 Rail operators & logistics companies

- 3.1.4 Regulatory authorities & compliance bodies

- 3.1.5 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing demand for safety features

- 3.7.1.2 Increasing demand for freight

- 3.7.1.3 Integration of AI and machine learning

- 3.7.1.4 Growing government regulations and incentives

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Data privacy and security concerns

- 3.7.2.2 High cost of implementation

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034, ($Bn)

- 5.1 Key trends

- 5.2 Mechanical

- 5.2.1 Brake systems

- 5.2.2 Couplers & draft gears

- 5.2.3 Bearings & axles

- 5.2.4 Wheels & wheelsets

- 5.2.5 Doors & hatches

- 5.2.6 Pneumatic systems

- 5.2.7 Others

- 5.3 Structural

- 5.3.1 Body & frame repairs

- 5.3.2 Welding & metalwork

- 5.3.3 Corrosion prevention and repair

- 5.3.4 Roof, sides, and underbody repairs

- 5.3.5 Others

- 5.4 Interiors

- 5.4.1 Flooring & subflooring

- 5.4.2 Interior lining & insulation

- 5.4.3 Lighting & electrical systems

- 5.4.4 Others

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Service, 2021-2034, ($Bn)

- 6.1 Key trends

- 6.2 Mobile

- 6.3 On-site

Chapter 7 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Russia

- 7.3.7 Nordics

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 ANZ

- 7.4.6 Southeast Asia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 UAE

- 7.6.2 South Africa

- 7.6.3 Saudi Arabia

Chapter 8 Company Profiles

- 8.1 A&B Rail Services

- 8.2 Alstom

- 8.3 American Industrial Transport

- 8.4 Apache Railway Company

- 8.5 Cathcart Rail

- 8.6 CF Rail Services

- 8.7 GATX

- 8.8 Herzog Services

- 8.9 Progress Rail

- 8.10 Quality Rail Service

- 8.11 Railserve

- 8.12 Rescar Companies

- 8.13 Road & Rail Services

- 8.14 Siemens

- 8.15 The Greenbrier Companies

- 8.16 Trinity Industries

- 8.17 TTX Company

- 8.18 Union Tank Car Company (UTLX)

- 8.19 Wabtec

- 8.20 Watco Companies